German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

DSV A/S (CPH:DSV) presented its half-year 2025 results on July 31, highlighting stable organic performance in a challenging market environment, with the newly acquired Schenker business making its first significant contribution to the company’s financial results.

The global logistics giant reported that while market conditions remain volatile, it has maintained its full-year guidance and is making steady progress with the Schenker integration, which is expected to deliver substantial synergies in the coming years.

DSV shares closed at DKK 1,537.50 on July 30, showing a slight decline of 0.71% ahead of the earnings presentation.

Quarterly Performance Highlights

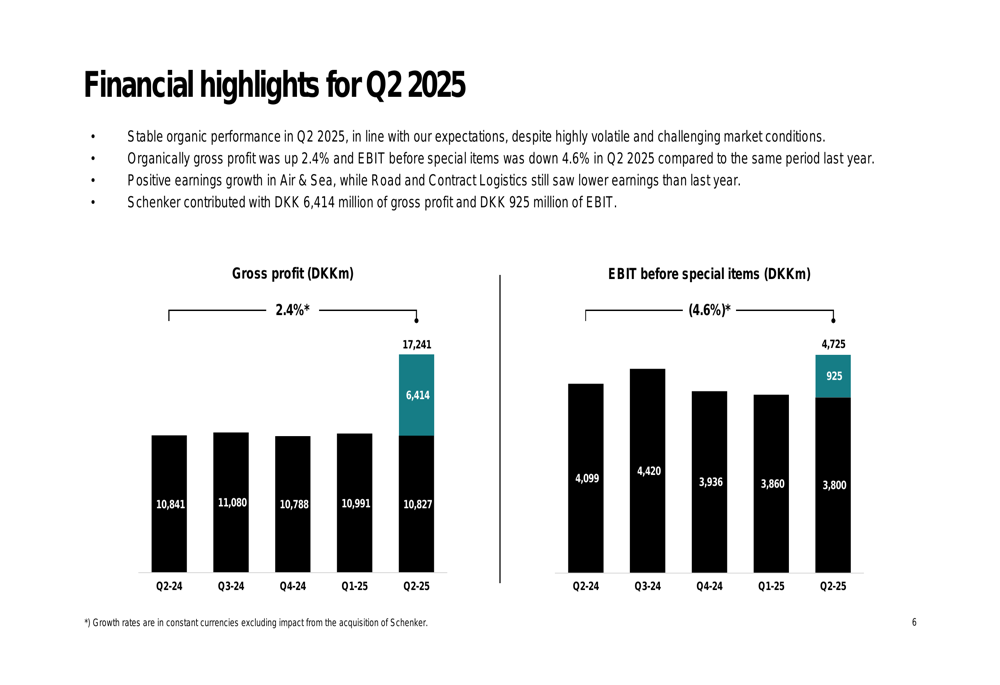

DSV reported stable organic financial performance for Q2 2025, with gross profit increasing by 2.4% organically, while EBIT before special items declined by 4.6% on an organic basis. The recently acquired Schenker business contributed significantly to the results, adding DKK 6,414 million to gross profit and DKK 925 million to EBIT.

As shown in the following financial highlights chart:

Total (EPA:TTEF) gross profit reached DKK 17,241 million in Q2 2025, compared to DKK 10,841 million in Q2 2024. EBIT before special items was DKK 4,725 million, up from DKK 4,099 million in the same period last year. These figures include two months of contribution from Schenker.

The company emphasized that it is on track for EPS growth (diluted and adjusted) and reported strong adjusted free cash flow, which is contributing to deleveraging efforts following the Schenker acquisition.

Schenker Integration Update

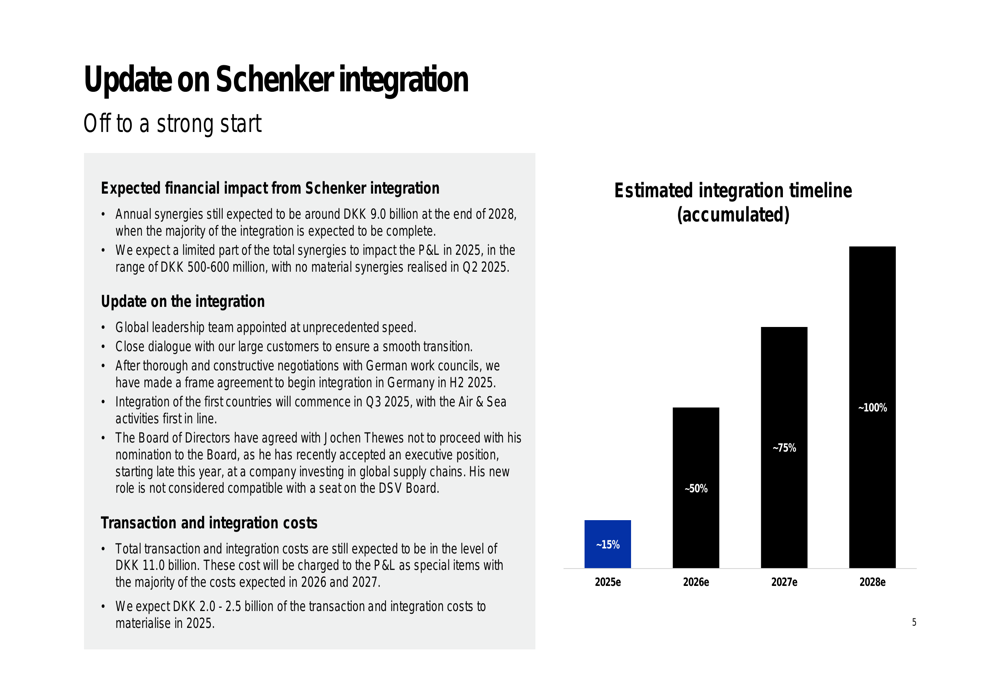

A key focus of the presentation was the progress of the Schenker integration, which DSV confirmed is off to a strong start. The company has appointed its global leadership team quickly and maintained close dialogue with customers throughout the transition.

The integration timeline and expected synergies are illustrated in the following chart:

DSV still expects annual synergies of approximately DKK 9.0 billion by the end of 2028, with limited impact on the P&L in 2025 (between DKK 500-600 million). The company has established a frame agreement to begin integration in Germany in the second half of 2025, with the first countries set to begin integration in Q3 2025.

The integration is expected to progress gradually, with approximately 15% completion by the end of 2025, 50% by 2026, 75% by 2027, and full completion by 2028.

Segment Performance Analysis

DSV’s presentation revealed varying performance across its business segments:

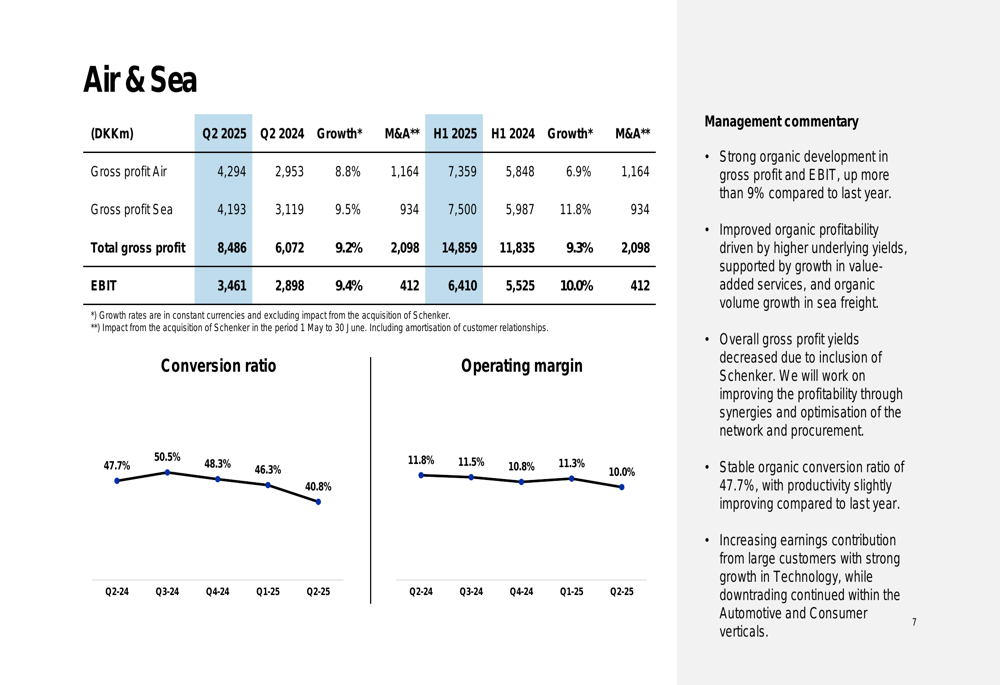

The Air & Sea segment demonstrated strong organic development in both gross profit and EBIT, with improved organic profitability despite decreasing gross profit yields. Air freight volumes grew by 46% (including Schenker), with gross profit improving by 9%. Sea freight saw total volume growth of 43% and an organic increase in gross profit of 10%.

The segment’s performance is detailed in the following chart:

The Road segment faced challenges, reporting an organic revenue decline of 4.1% and a gross profit decrease of 7.5%. Management noted operational issues with USA Truck (NASDAQ:USAK), though they also highlighted market share gains in certain regions.

The Contract Logistics segment experienced negative organic growth, with revenue declining by 14.9% and gross profit down by 3.7% organically. Management indicated that actions for improvements are underway.

Financial Position and Cash Flow

DSV reported significant improvements in cash flow from operating activities, which reached DKK 9,305 million in H1 2025 compared to DKK 4,218 million in H1 2024. This improvement was driven by higher EBITDA and a positive change in working capital of DKK 2,405 million, compared to a negative change of DKK 3,773 million in the previous year.

However, free cash flow was heavily impacted by the Schenker acquisition, resulting in a negative DKK 66,982 million for H1 2025, compared to a positive DKK 3,732 million in H1 2024.

The company’s financial position shows a net interest-bearing debt of DKK 93,280 million and a gearing ratio of 2.7x, reflecting the significant investment in acquiring Schenker.

Outlook and Forward Guidance

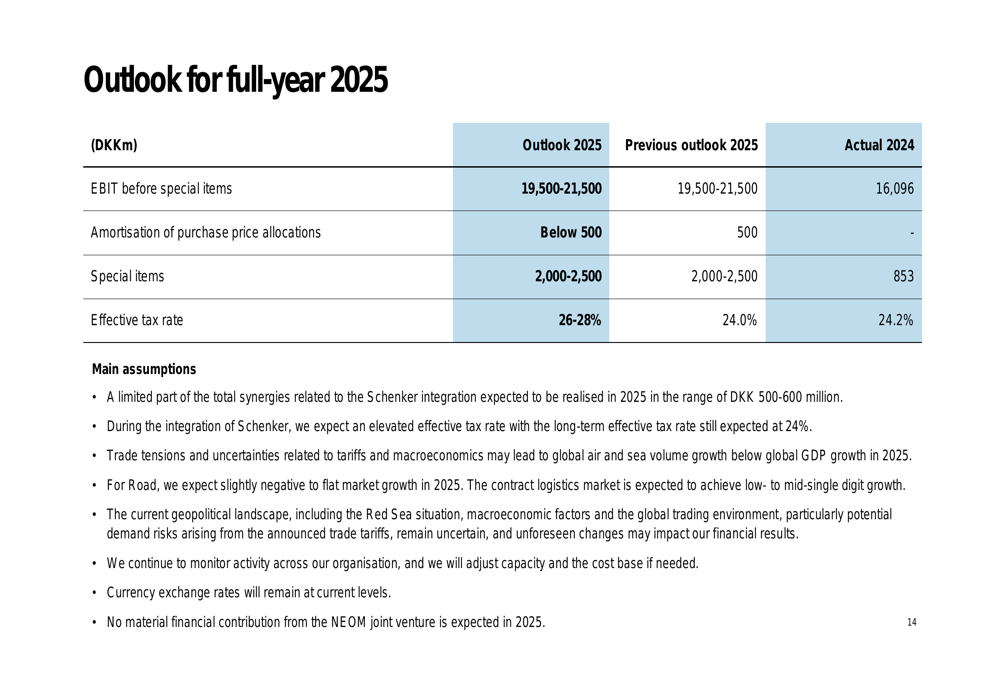

DSV reiterated its full-year 2025 guidance, expecting EBIT before special items to be in the range of DKK 19,500-21,500 million. This outlook is presented in the following chart:

The company expects amortization of purchase price allocations to be below DKK 500 million, with special items estimated between DKK 2,000-2,500 million. The effective tax rate is projected to be 26-28%.

Management emphasized that the guidance includes limited synergies from Schenker in 2025, with an elevated effective tax rate during the integration period. They also acknowledged potential impacts from trade tensions and the geopolitical landscape.

Key Takeaways

DSV concluded its presentation with these key messages:

The company emphasized its stable financial performance despite challenging market conditions, progress on financial deleveraging and EPS growth, and the strong start to the Schenker integration. Management expressed confidence in achieving the full-year guidance for 2025.

As DSV moves forward with the Schenker integration, investors will be closely watching the realization of synergies and the company’s ability to navigate ongoing market challenges while maintaining its financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.