BitMine stock falls after CEO change and board appointments

Introduction & Market Context

Dynavax Technologies Corporation (NASDAQ:DVAX) released its Q1 2025 corporate presentation on May 6, highlighting continued growth in its hepatitis B vaccine business while advancing multiple pipeline candidates. The vaccine developer, which closed at $10.92 on May 6, down 3.11% for the day, reported significant year-over-year growth in its flagship HEPLISAV-B product despite broader market challenges.

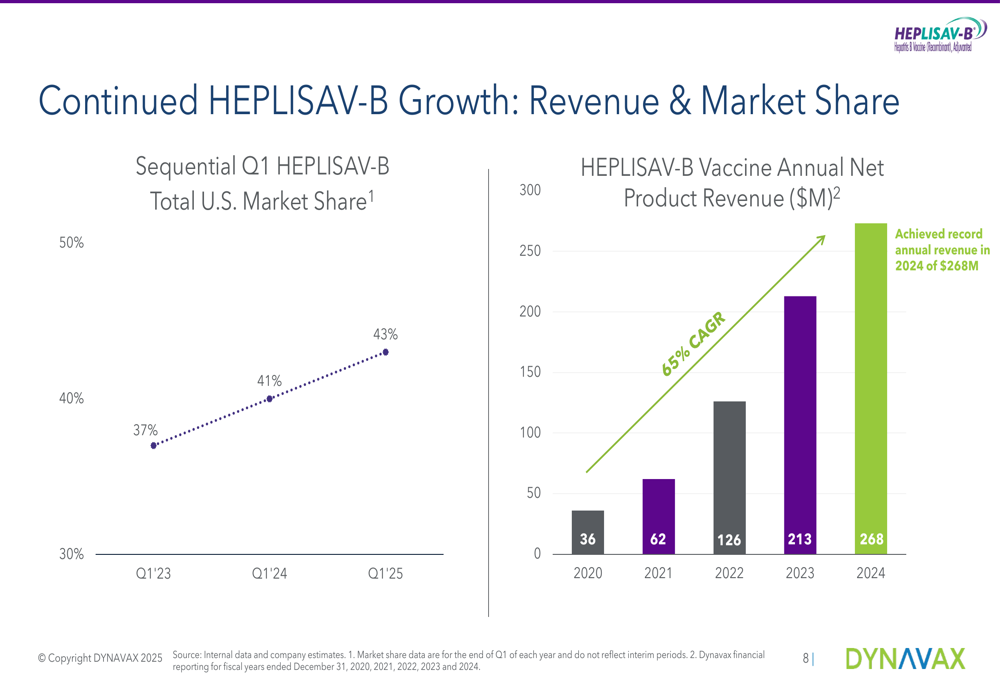

The company’s presentation emphasized its strategic focus on expanding HEPLISAV-B’s market share, which has grown to approximately 43% in Q1 2025, while advancing a diversified vaccine pipeline leveraging its proprietary CpG 1018 adjuvant technology.

Quarterly Performance Highlights

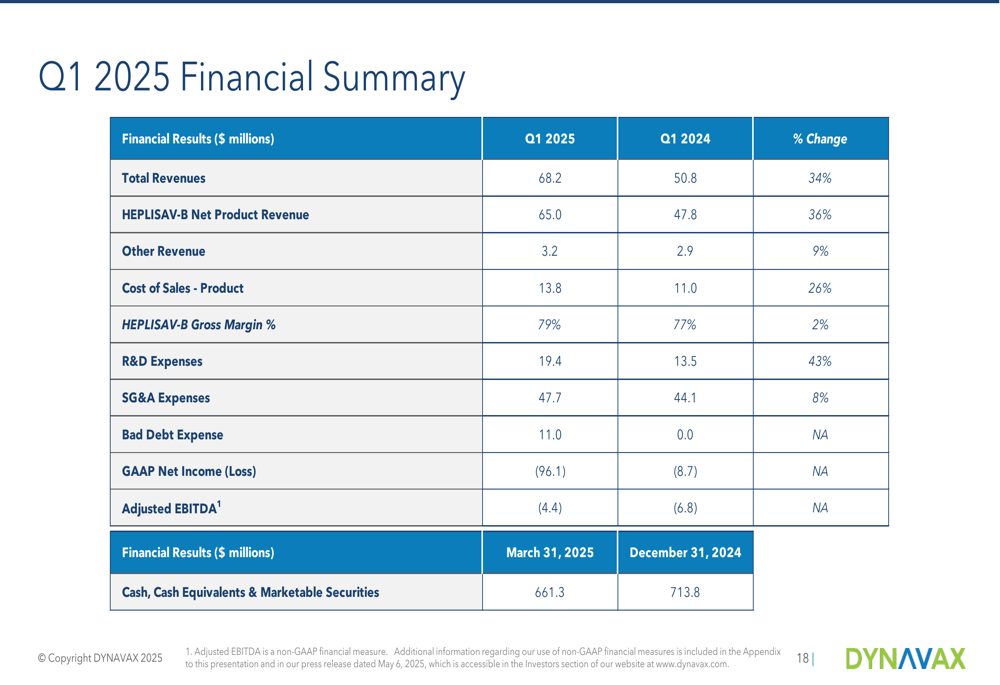

Dynavax reported total revenues of $68.2 million for Q1 2025, representing a 34% increase compared to the same period last year. HEPLISAV-B net product revenue reached $65.0 million, up 36% from $48 million in Q1 2024, continuing the product’s strong growth trajectory.

As shown in the following chart of quarterly revenue growth and market share gains:

Despite the revenue growth, the company reported a GAAP net loss of $(96,099) for the quarter, with Adjusted EBITDA at $(4,356). R&D expenses increased 43% to $19.4 million, reflecting the company’s intensified investment in pipeline development.

The company’s financial position remains strong with $661.3 million in cash, cash equivalents, and marketable securities as of March 31, 2025. Dynavax has also continued its commitment to shareholder returns, having repurchased $172 million of its $200 million share repurchase program as of May 5, 2025.

The quarterly financial summary shows the company’s performance across key metrics:

HEPLISAV-B Growth and Market Opportunity (SO:FTCE11B)

HEPLISAV-B continues to be Dynavax’s primary growth driver, with the company reporting record first-quarter sales. The vaccine has demonstrated consistent growth since its launch, achieving a 65% CAGR from 2020 to 2024, with annual net product revenue increasing from $36 million in 2020 to $268 million in 2024.

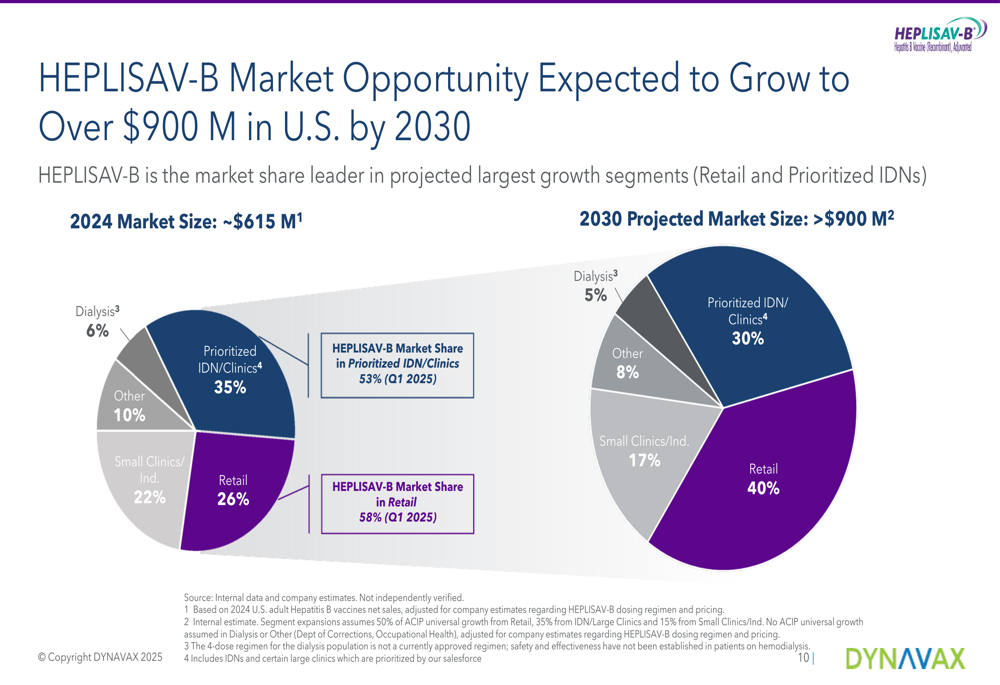

The company’s presentation outlined the expanding market opportunity for HEPLISAV-B, projecting the U.S. adult hepatitis B vaccine market to grow from approximately $615 million in 2024 to over $900 million by 2030. Dynavax expects to capture at least 60% of this market by 2030, up from 44% in 2024.

The following chart illustrates this projected market expansion:

Notably, HEPLISAV-B has established itself as the market share leader in the fastest-growing segments of the hepatitis B vaccine market. The vaccine currently holds 58% market share in the retail segment and 53% in prioritized IDN/clinics as of Q1 2025. The retail segment is expected to grow from 26% of the market in 2024 to 40% by 2030.

The breakdown of market opportunity by sector shows where Dynavax is focusing its commercial efforts:

Pipeline Development Progress

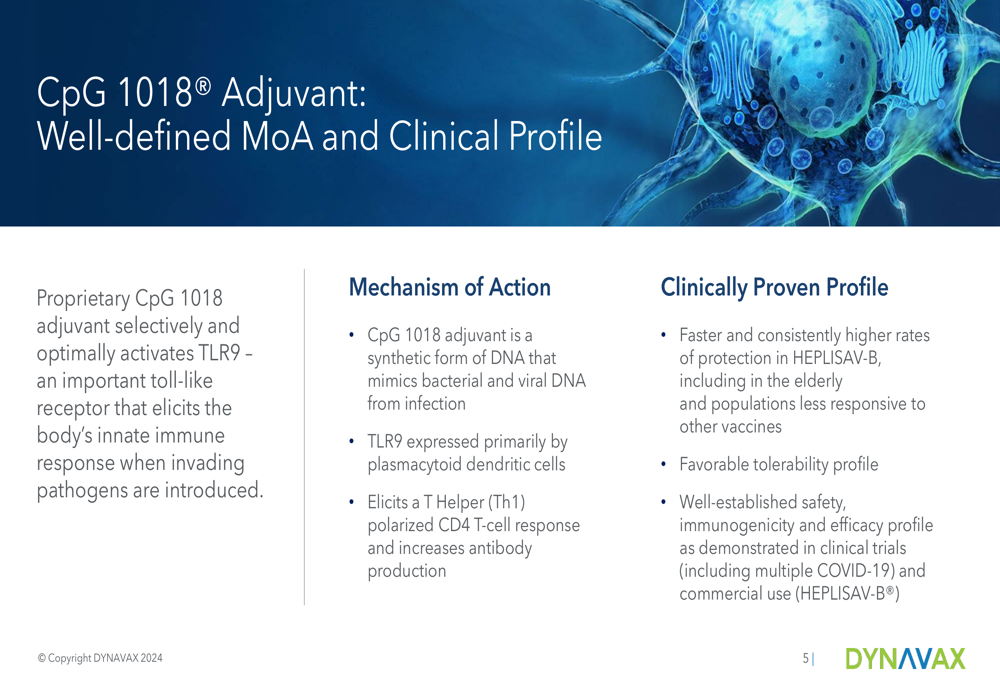

Beyond HEPLISAV-B, Dynavax is advancing several vaccine candidates utilizing its CpG 1018 adjuvant technology. The company’s proprietary adjuvant is designed to enhance immune response while maintaining a favorable safety profile.

As illustrated in the following explanation of the CpG 1018 mechanism:

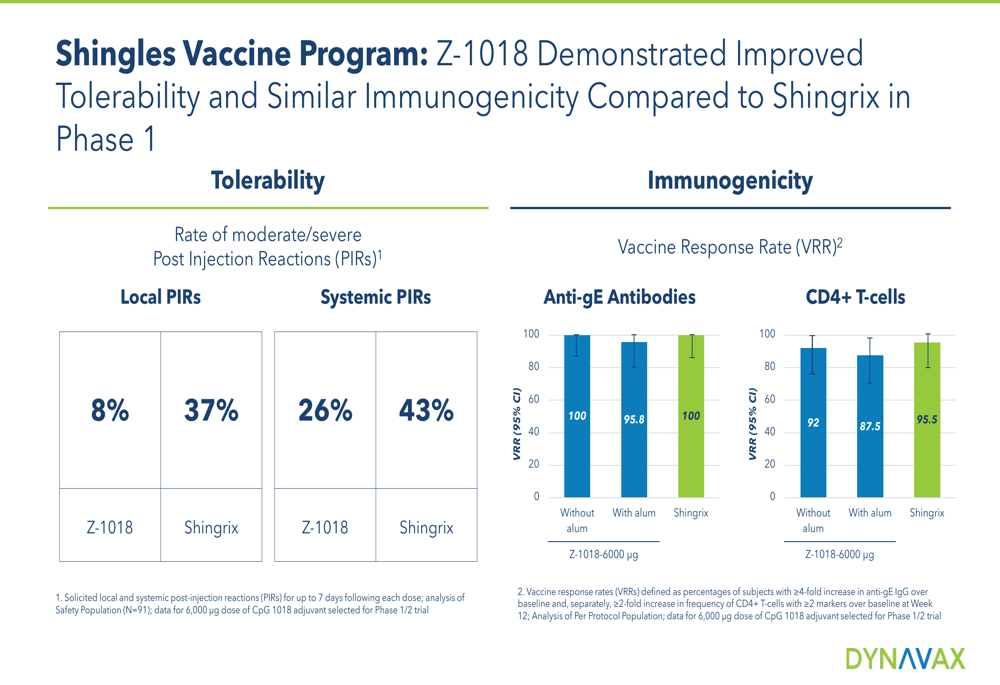

The company’s shingles vaccine program represents a significant opportunity to address limitations of the current market-leading vaccine. Dynavax has completed enrollment in Part 1 of a Phase 1/2 trial evaluating its Z-1018 vaccine candidate compared to Shingrix in 441 healthy adults aged 50 to 69. The company anticipates reporting top-line immunogenicity and safety data in Q3 2025.

Early data from the program suggests improved tolerability while maintaining similar immunogenicity compared to Shingrix:

Additional pipeline programs include:

1. A plague vaccine program in partnership with the U.S. Department of Defense, with a Phase 2 clinical trial expected to initiate in Q3 2025. This program is supported by approximately $30 million in funding through the first half of 2027.

2. A pandemic influenza adjuvant program, with plans to initiate Part 1 of a Phase 1/2 study in Q2 2025 to evaluate the safety and immunogenicity of an investigational H5N1 pandemic influenza vaccine adjuvanted with CpG 1018.

3. A Lyme disease vaccine program in preclinical development, with ongoing IND-enabling studies.

Financial Analysis and Outlook

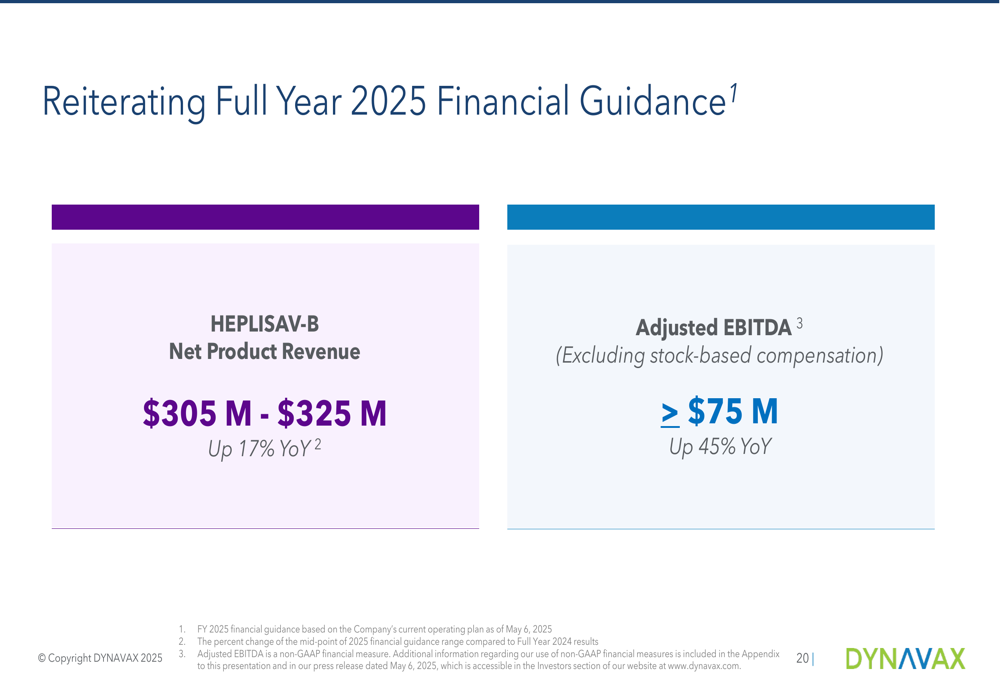

Dynavax reiterated its full-year 2025 financial guidance, projecting HEPLISAV-B net product revenue between $305 million and $325 million, representing approximately 17% year-over-year growth. The company also expects adjusted EBITDA to exceed $75 million for the full year.

The guidance reflects management’s confidence in continued commercial execution despite the Q1 net loss:

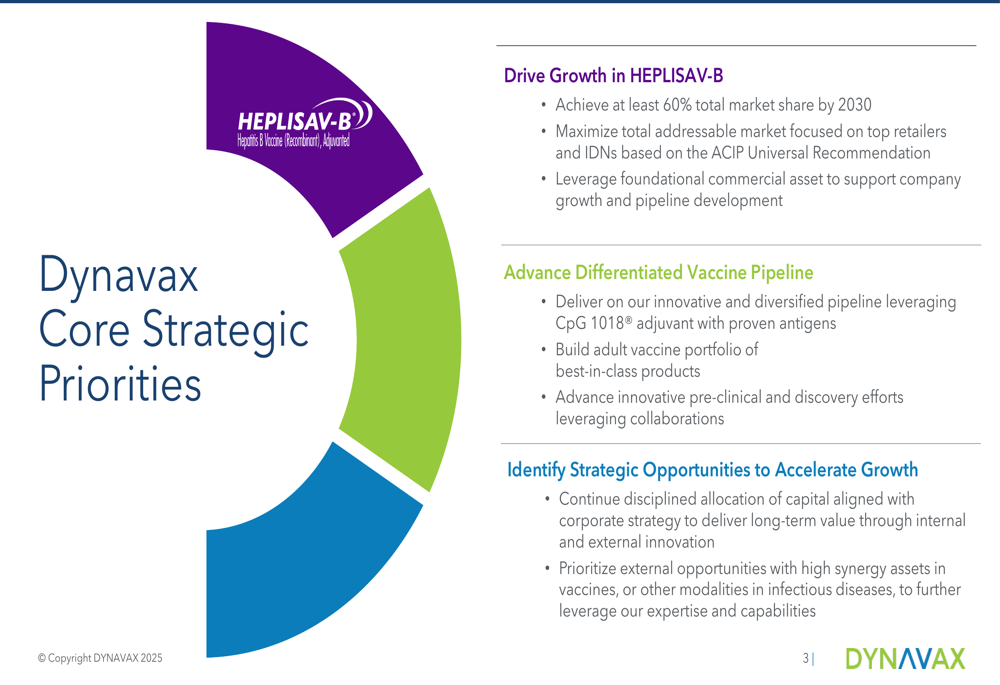

The company’s capital allocation strategy balances investment in growth initiatives with shareholder returns. Dynavax outlined four key priorities: maximizing HEPLISAV-B’s potential, investing in pipeline development leveraging CpG 1018, accessing late-stage assets in infectious diseases, and opportunistically returning capital to shareholders.

The company’s core strategic priorities emphasize both near-term commercial execution and long-term pipeline development:

While Dynavax’s Q1 2025 presentation highlighted strong revenue growth and pipeline advancement, investors should note the significant GAAP net loss for the quarter. The projected full-year adjusted EBITDA of over $75 million suggests management expects improved profitability in subsequent quarters, driven by continued HEPLISAV-B sales growth and potentially more favorable expense timing.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.