IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

Edison International (NYSE:EIX) reported its second-quarter 2025 financial results on July 31, revealing a year-over-year decline in earnings while maintaining its long-term growth outlook. The company’s stock closed at $51.69, up 0.83% for the day, but has experienced significant pressure over recent months, trading well below its 52-week high of $88.77.

The utility company continues to navigate a complex regulatory environment in California while making substantial investments in grid infrastructure and wildfire mitigation. Despite facing near-term challenges, Edison remains focused on its role in supporting California’s clean energy transition and electrification goals.

Quarterly Performance Highlights

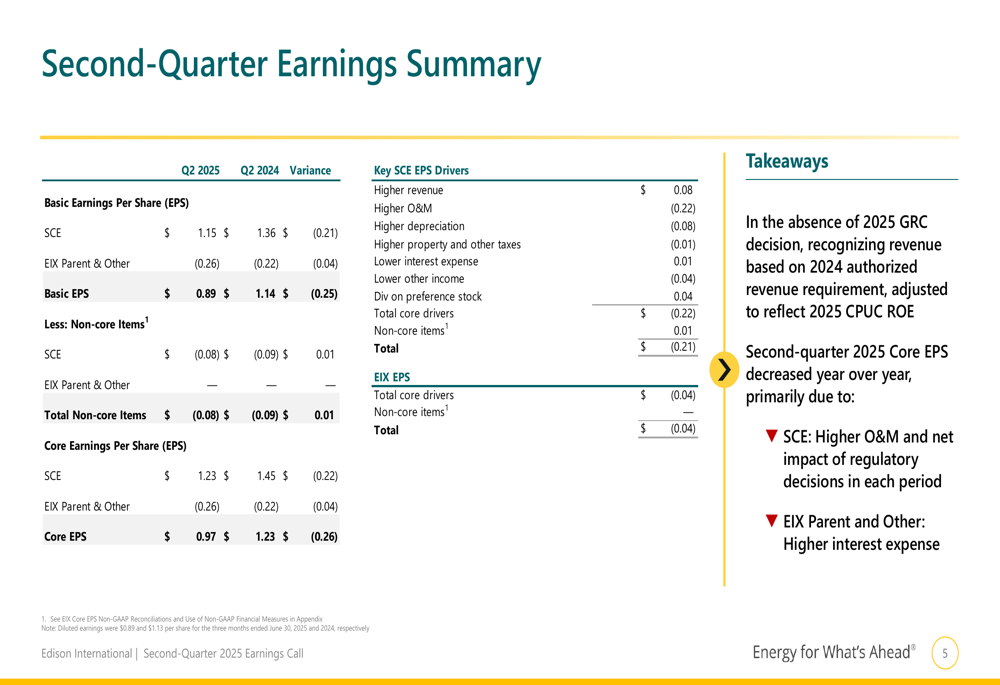

Edison International reported second-quarter 2025 GAAP earnings per share of $0.89, down from $1.14 in the same period last year. Core EPS, which excludes non-core items, came in at $0.97, compared to $1.23 in Q2 2024, representing a 21% year-over-year decrease.

The company attributed the earnings decline primarily to higher operations and maintenance expenses and the net impact of regulatory decisions at Southern California Edison (SCE). Higher interest expenses at the parent company level also contributed to the decrease.

As shown in the following quarterly earnings summary:

This performance follows a disappointing first quarter, where Edison reported EPS of $1.37, missing analyst expectations of $1.41, with revenue of $3.81 billion falling short of the $4.4 billion forecast.

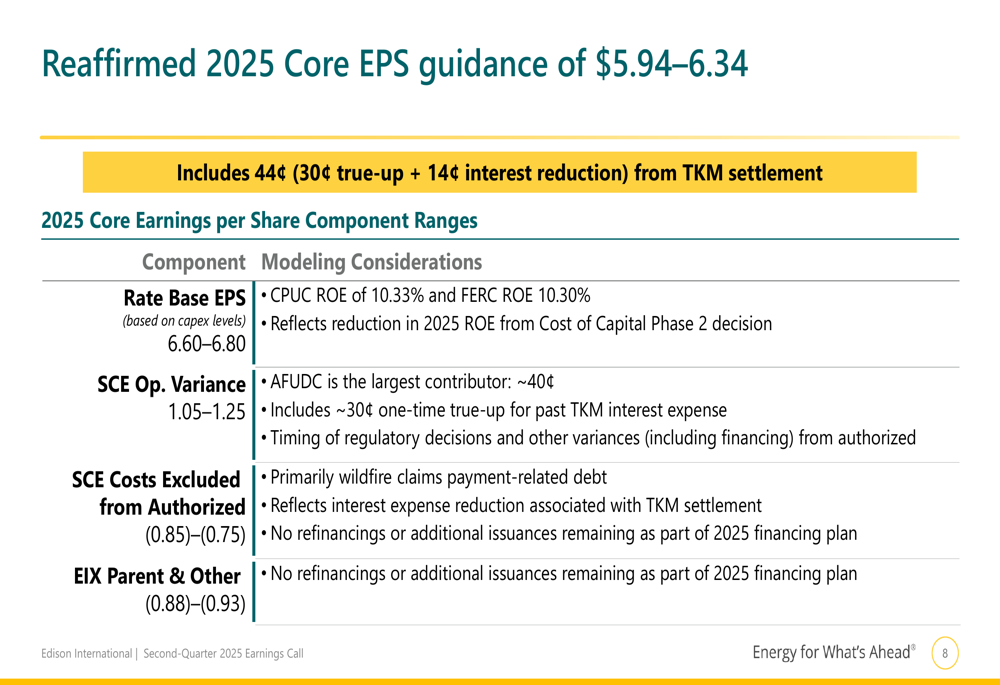

Despite these challenges, Edison International reaffirmed its 2025 Core EPS guidance range of $5.94 to $6.34. This guidance includes a 44¢ benefit (30¢ true-up plus 14¢ interest reduction) from the TKM settlement.

The components of the 2025 guidance are illustrated in this breakdown:

Regulatory Developments

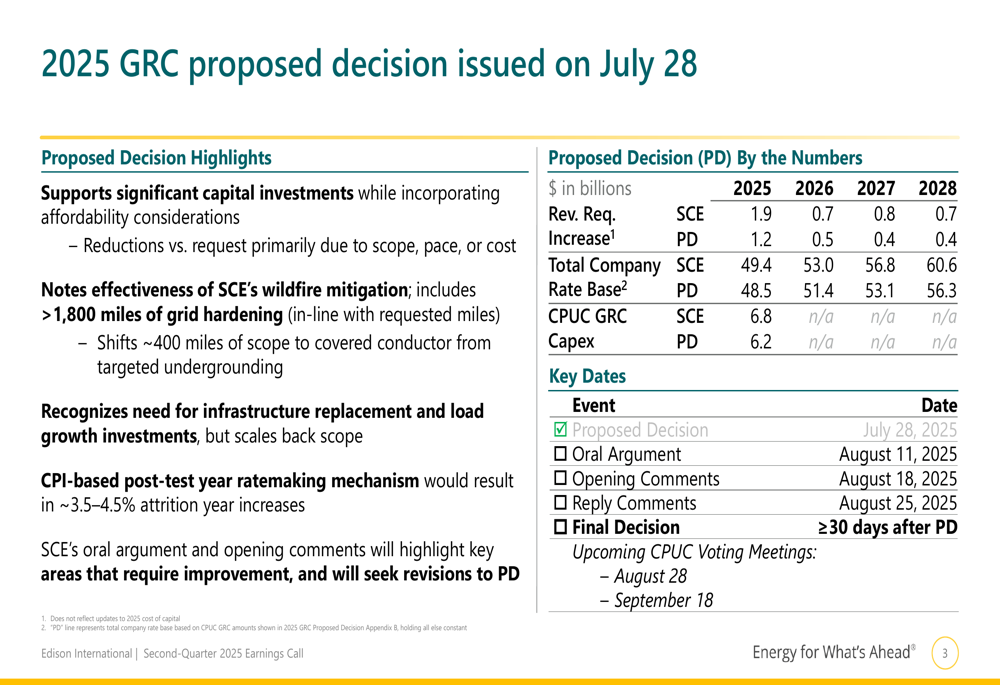

A significant development for Edison International is the proposed decision for the 2025 General Rate Case (GRC) issued on July 28, 2025. The proposal supports substantial capital investments while incorporating affordability considerations, with some reductions in scope, pace, or cost compared to the company’s request.

The proposed decision recognizes SCE’s effective wildfire mitigation efforts, including over 1,800 miles of grid hardening completed to date. It also acknowledges the need for infrastructure replacement and investments to support load growth, though at a scaled-back scope.

The financial impact of the proposed decision is detailed in the following chart:

The company expects a final decision on the GRC at least 30 days after the proposed decision, with upcoming California Public Utilities Commission (CPUC) voting meetings scheduled for August 28 and September 18.

Edison also highlighted progress in other key regulatory proceedings, including the approval of the WMCE settlement and a final decision in the WMVM proceeding. The company continues to address legacy wildfire issues, with ongoing investigations related to the Eaton (NYSE:ETN) Fire and plans to launch a Wildfire Recovery Compensation Program.

Strategic Initiatives & Capital Plans

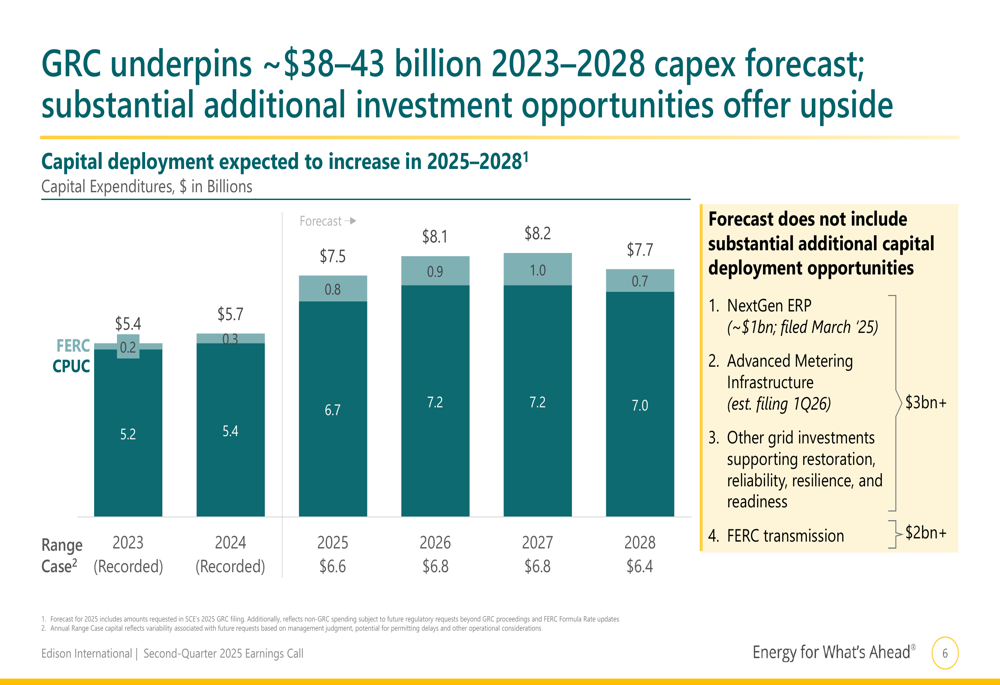

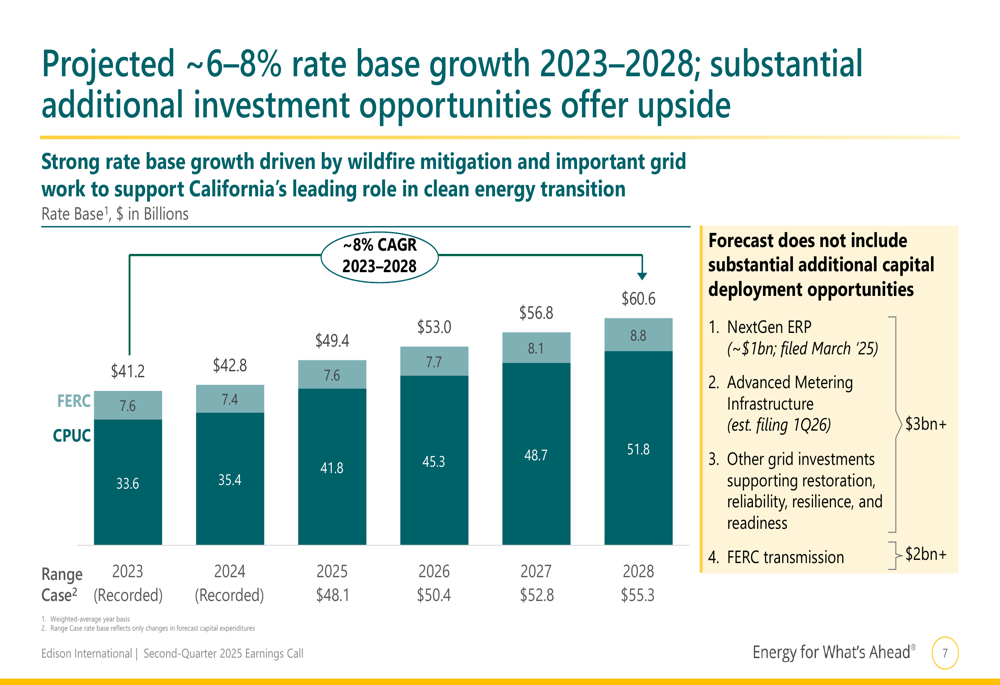

Edison International outlined an ambitious capital expenditure plan of approximately $38-43 billion for 2023-2028, with increasing investments planned for 2025-2028. This capital deployment is expected to drive rate base growth of approximately 6-8% over the same period.

The company’s capital expenditure forecast is illustrated in this chart:

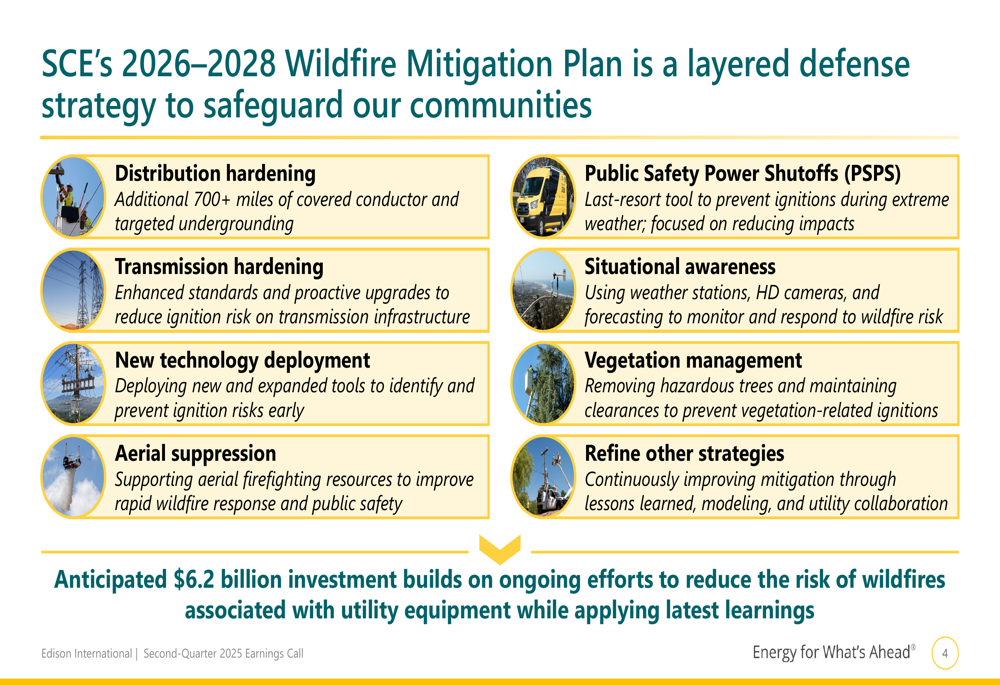

A key component of Edison’s strategy is its 2026-2028 Wildfire Mitigation Plan, which includes a $6.2 billion investment in a layered defense approach. The plan encompasses distribution hardening with over 700 miles of covered conductor and targeted undergrounding, transmission hardening, new technology deployment, aerial suppression support, and enhanced situational awareness.

The comprehensive wildfire mitigation strategy is detailed in this overview:

Edison International also emphasized its leading position in supporting California’s electrification goals, with industry-leading programs for transportation electrification and projections of 35% load growth by 2035 and 80% by 2045.

The company’s rate base growth projection, which underpins its earnings growth forecast, is shown here:

Forward-Looking Statements

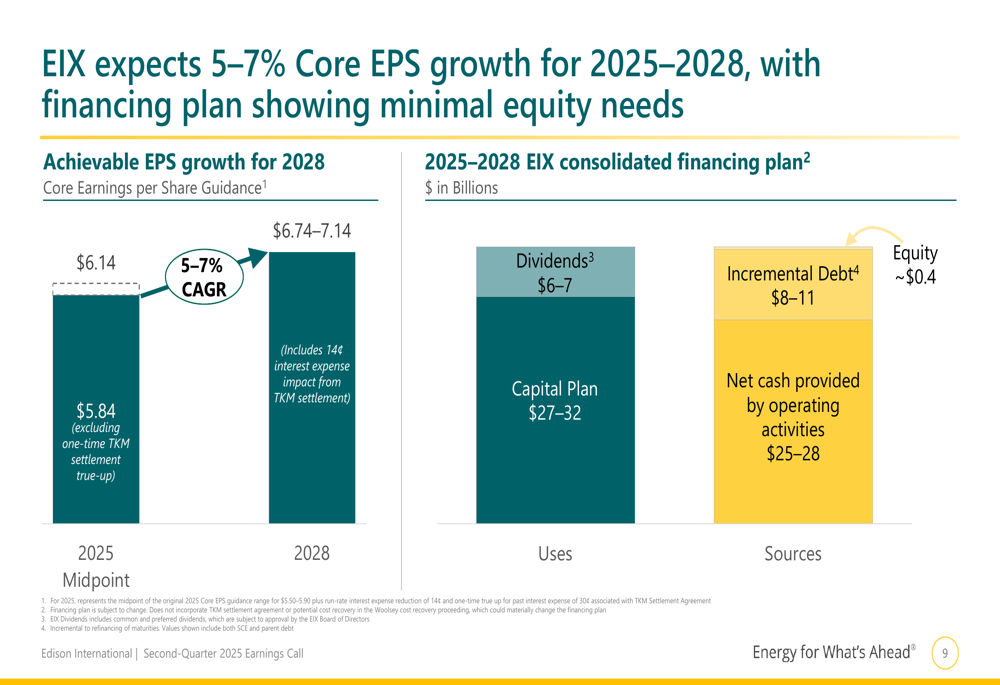

Despite near-term earnings challenges, Edison International maintained its confidence in delivering 5-7% Core EPS growth from 2025 to 2028, targeting $6.74-7.14 by 2028. This growth projection is supported by the company’s strong rate base expansion and capital investment plans.

The long-term earnings growth expectations are illustrated in this chart:

Edison’s financing plan for 2025-2028 shows minimal equity needs of approximately $0.4 billion, with the majority of capital coming from net cash provided by operating activities ($25-28 billion) and incremental debt ($8-11 billion).

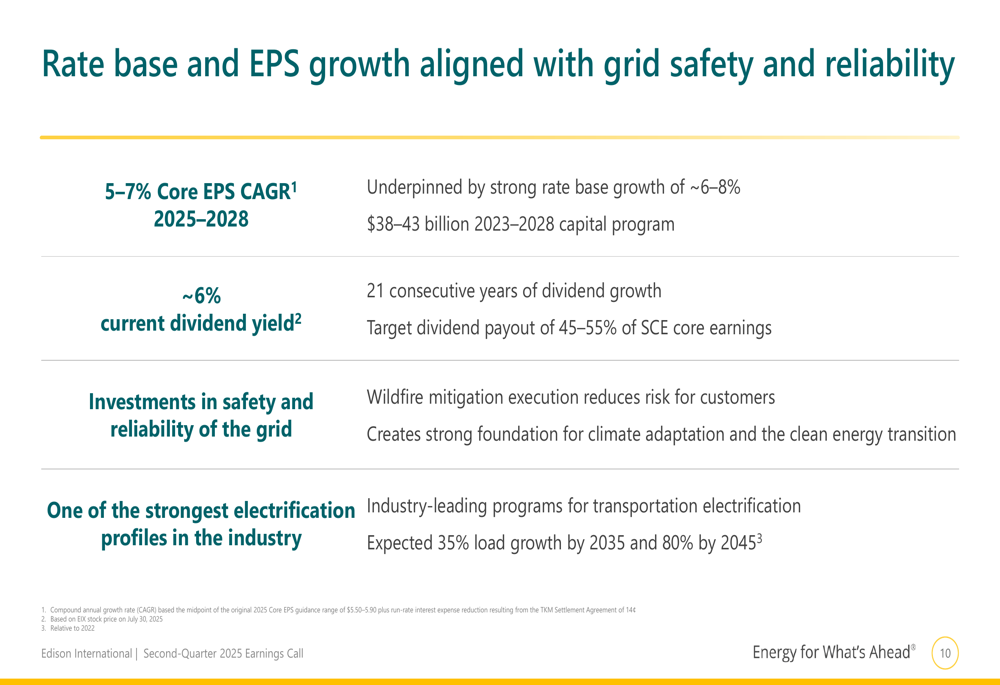

The company also highlighted its dividend track record, with 21 consecutive years of dividend growth and a current yield of approximately 6%. Edison targets a dividend payout ratio of 45-55% of SCE core earnings.

The alignment between rate base growth and EPS growth, which forms the foundation of Edison’s long-term outlook, is summarized here:

While Edison International faces near-term headwinds with declining quarterly earnings and ongoing regulatory challenges, the company remains focused on its long-term strategy of grid modernization, wildfire risk reduction, and supporting California’s clean energy transition. Investors will be closely watching the final decision on the 2025 GRC and progress on wildfire-related proceedings, which could significantly impact the company’s financial outlook and risk profile.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.