Gold prices edge higher; Russia-Ukraine, Jackson Hole symposium in spotlight

Introduction & Market Context

Elutia Inc. (NASDAQ:ELUT) presented its second-quarter 2025 earnings on August 14, highlighting the commercial success of its EluPro product line while facing challenges with overall revenue growth and cash position. The company, which focuses on developing biologic envelopes and drug-eluting technologies, reported flat year-over-year revenue but showed significant sequential growth in its flagship product line.

The presentation, led by CEO C. Randal Mills and CFO Matt Ferguson, emphasized Elutia’s progress in hospital adoption, strategic partnerships, and pipeline development while acknowledging ongoing financial constraints.

Quarterly Performance Highlights

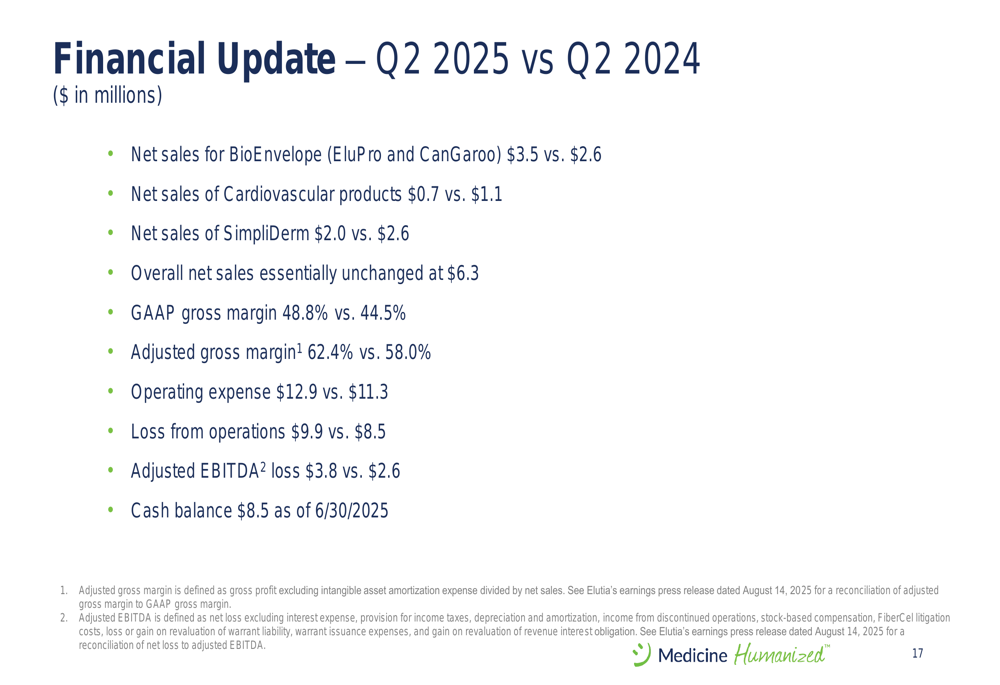

Elutia reported Q2 2025 net sales of $6.3 million, essentially unchanged from the same period last year. However, the company’s BioEnvelope segment, which includes EluPro and CanGaroo products, showed strong performance with sales of $3.5 million, up from $2.6 million in Q2 2024, representing a 33% year-over-year increase.

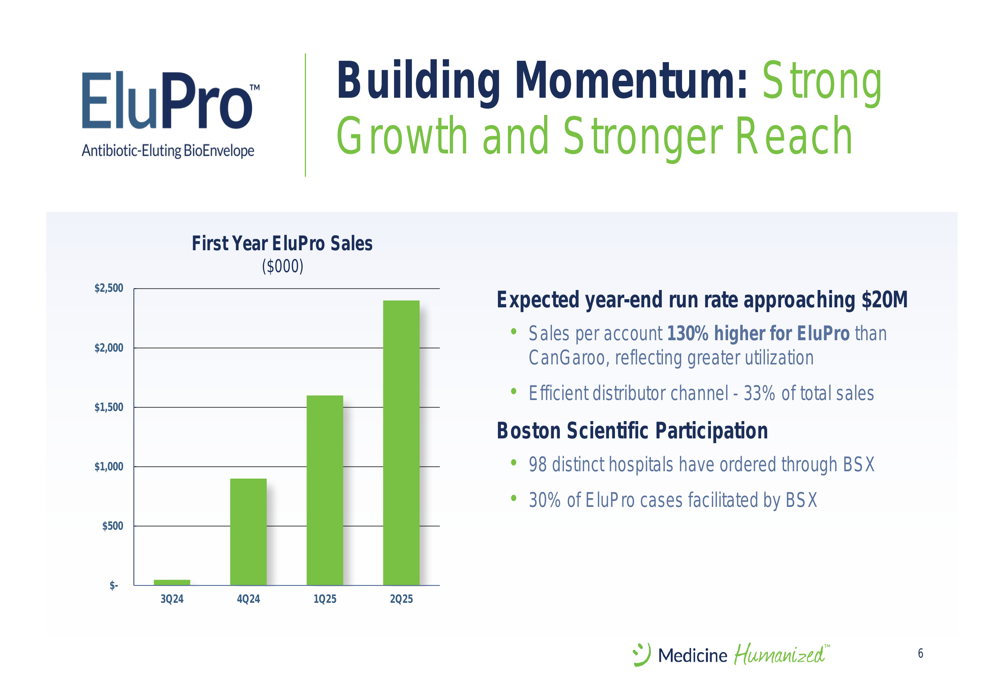

The company highlighted EluPro’s impressive 49% sequential growth, with the product now accounting for 68% of BioEnvelope revenue. This growth trajectory suggests an expected year-end run rate approaching $20 million for the EluPro line.

As shown in the following chart of EluPro’s quarterly sales growth:

Gross margins showed improvement, with GAAP gross margin increasing to 48.8% from 44.5% in the prior year, and adjusted gross margin rising to 62.4% from 58.0%. However, operating expenses also increased to $12.9 million from $11.3 million, resulting in a larger loss from operations of $9.9 million compared to $8.5 million in Q2 2024.

The company’s detailed financial performance is summarized in this slide:

A concerning trend is Elutia’s cash position, which stood at $8.5 million as of June 30, 2025, down significantly from the $17.4 million reported at the end of Q1 2025. This rapid cash burn rate could present challenges for the company’s growth initiatives if not addressed through additional financing or operational improvements.

Strategic Initiatives

Elutia’s partnership with Boston Scientific continues to drive adoption of the EluPro product. According to the presentation, 98 distinct hospitals have ordered through Boston Scientific, with 30% of EluPro cases facilitated by this partnership.

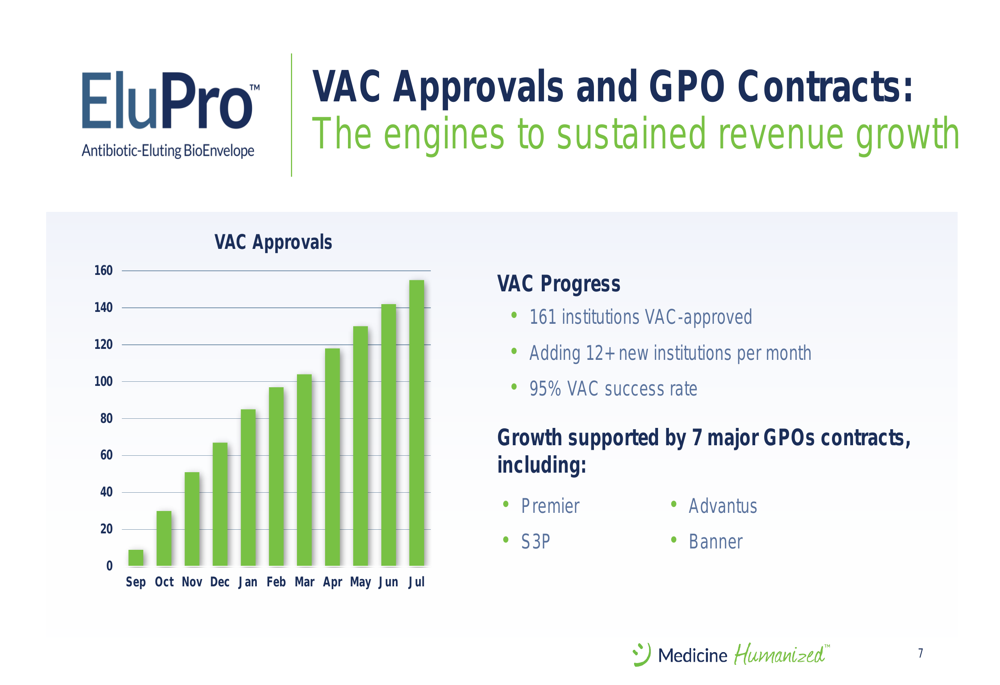

The company has made significant progress in securing hospital approvals through Value Analysis Committees (VACs), with 161 institutions now VAC-approved and adding more than 12 new institutions per month. Elutia reports a 95% VAC success rate, indicating strong clinical acceptance of their products.

The following slide illustrates the company’s VAC approval progress:

Supporting this hospital adoption strategy, Elutia has secured seven national Group Purchasing Organization (GPO) contracts, including with major organizations like Premier, S3P, Advantus, and Banner. These contracts are crucial for facilitating broader hospital access and streamlining the procurement process.

Pipeline Development

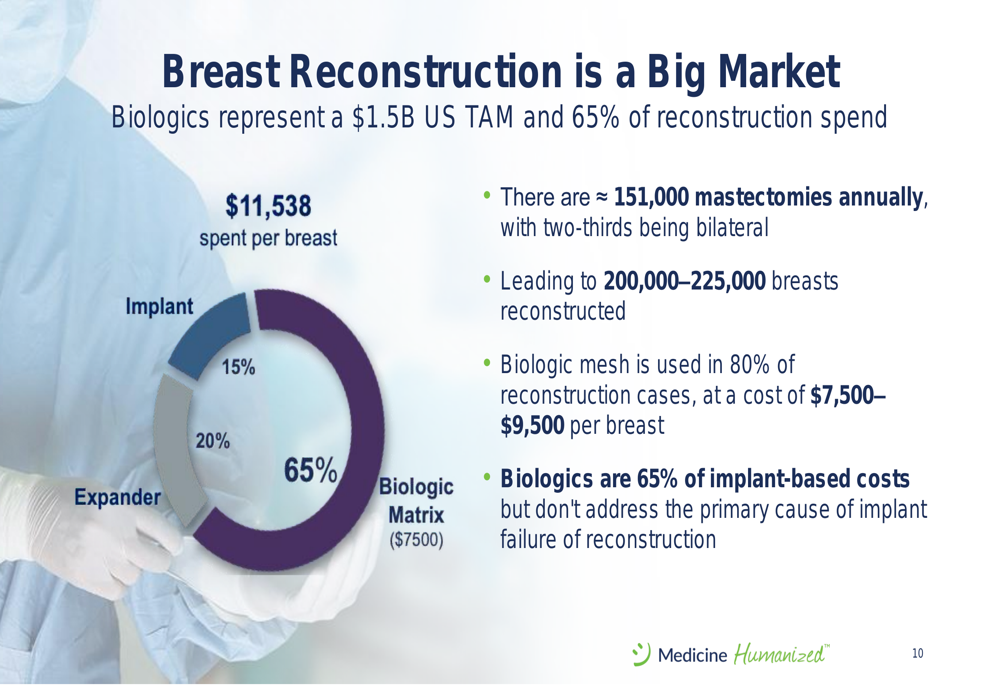

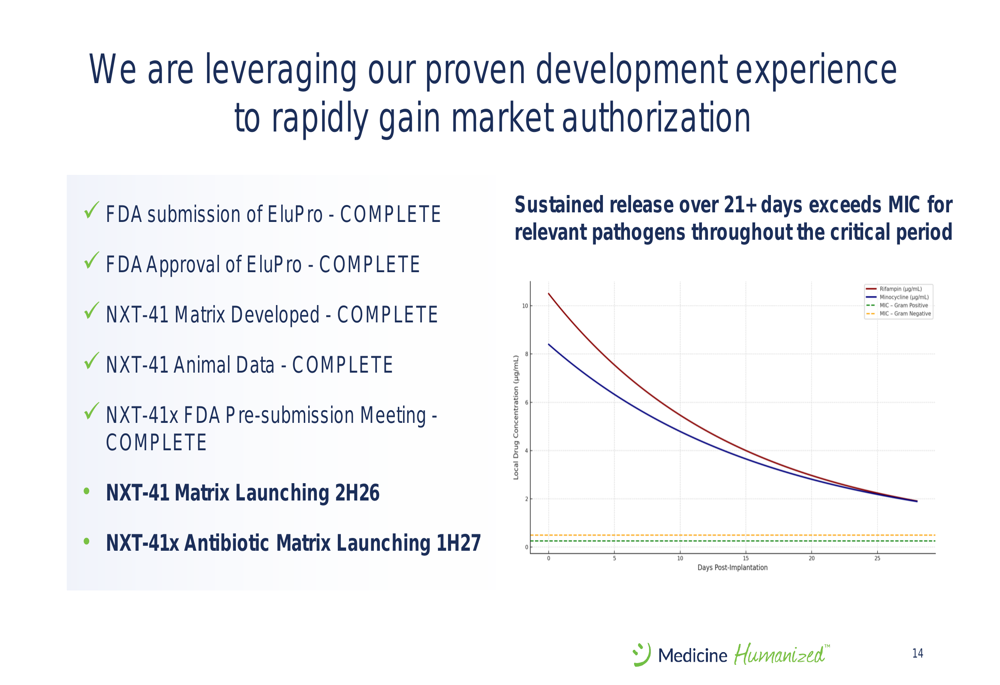

A significant portion of the earnings presentation focused on Elutia’s pipeline development, particularly the NXT product line targeting the breast reconstruction market. The company highlighted the substantial market opportunity, noting that biologics represent a $1.5 billion U.S. total addressable market and account for 65% of reconstruction spending.

The breast reconstruction market represents a compelling opportunity as illustrated in this market breakdown:

Elutia is developing NXT as a solution to address the high complication rates in breast reconstruction, where 1 in 3 patients suffer serious complications, including infection (10-14%), capsular contraction (19-29%), and implant loss (up to 21%).

The company introduced its NXT product, building on the technology from EluPro:

The development timeline shows that Elutia plans to launch the NXT-41 Matrix in the second half of 2026, followed by the NXT-41x Antibiotic Matrix in the first half of 2027. The company has completed several key milestones, including FDA approval of EluPro, development of the NXT-41 Matrix, animal data collection, and an FDA pre-submission meeting.

Detailed Financial Analysis

While Elutia emphasized growth in its BioEnvelope segment, the company’s overall financial picture shows mixed results. The flat year-over-year revenue of $6.3 million falls significantly short of the $7.8 million that was forecasted for Q2 2025 in previous guidance.

The revenue breakdown shows:

- BioEnvelope (EluPro and CanGaroo): $3.5 million vs. $2.6 million in Q2 2024

- Cardiovascular products: $0.7 million vs. $1.1 million in Q2 2024

- SimpliDerm: $2.0 million vs. $2.6 million in Q2 2024

The decline in non-BioEnvelope product lines offset the growth in the EluPro segment, resulting in flat overall revenue. The increased operating expenses and larger adjusted EBITDA loss ($3.8 million vs. $2.6 million) indicate that the company is investing heavily in growth initiatives at the expense of near-term profitability.

Forward-Looking Statements

Elutia outlined five strategic priorities for the future:

1. Drive topline EluPro growth by expanding VAC and GPO coverage

2. Continue building momentum through direct sales channels and Boston Scientific engagement

3. Increase production capacity and lower cost of goods sold for EluPro

4. Advance the NXT-41 pipeline of drug-eluting biologic solutions for reconstructive surgery

5. Advance one or more strategic opportunities toward conclusion

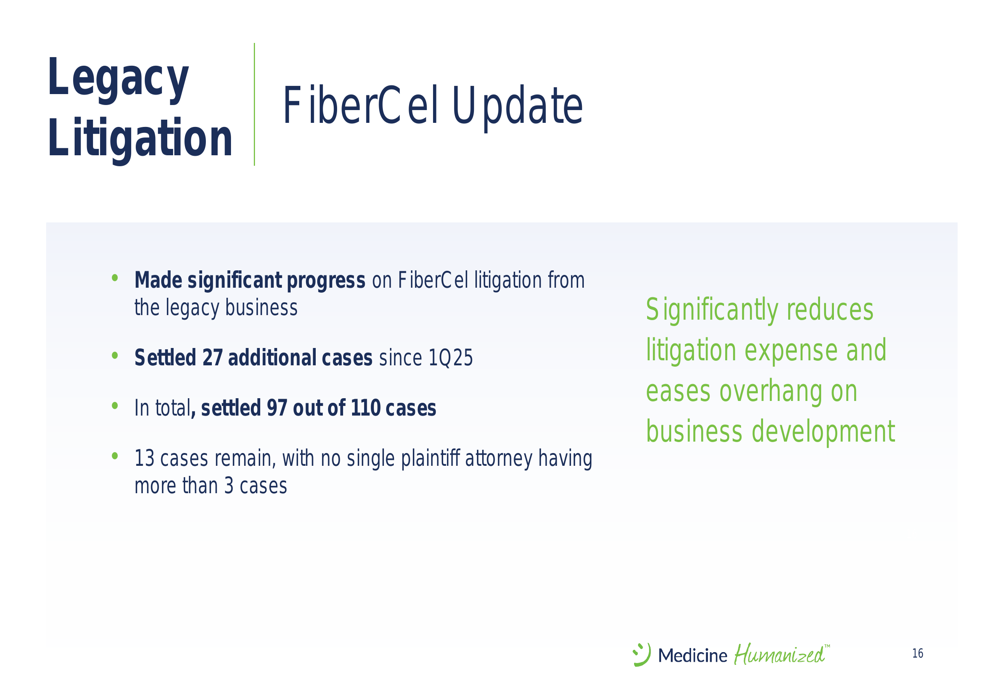

The company also reported progress on its FiberCel litigation from its legacy business, having settled 97 out of 110 cases, with only 13 cases remaining. This progress should reduce litigation expenses and remove an overhang on business development.

Conclusion

Elutia’s Q2 2025 presentation paints a picture of a company with promising product growth in its core EluPro line and an ambitious pipeline targeting large markets, particularly breast reconstruction. However, the flat overall revenue, increased operating losses, and rapidly diminishing cash position present significant challenges that the company will need to address.

The stock closed at $2.16 on August 14, 2025, near its 52-week low of $1.61, suggesting investor concerns about the company’s financial trajectory despite the positive developments in product adoption and pipeline progress. Investors will likely be watching closely for signs of improvement in overall revenue growth and cash management in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.