ServiceNow nears deal to acquire Veza for at least $1 bln - The Information

Introduction & Market Context

Electromagnetic Geoservices ASA (OB:EMGS) presented its first quarter 2025 results on May 13, showing steady revenue performance while unveiling a significant strategic expansion into the subsea construction market. The company’s stock closed at 1.76, down 2.27% on the day of the presentation, as investors digested both the quarterly performance and the substantial vessel acquisition announcement.

EMGS, traditionally focused on electromagnetic offshore services, is positioning itself to capitalize on the growing subsea construction market amid forecasts of increased demand for subsea tree installations and construction vessels through 2027.

Quarterly Performance Highlights

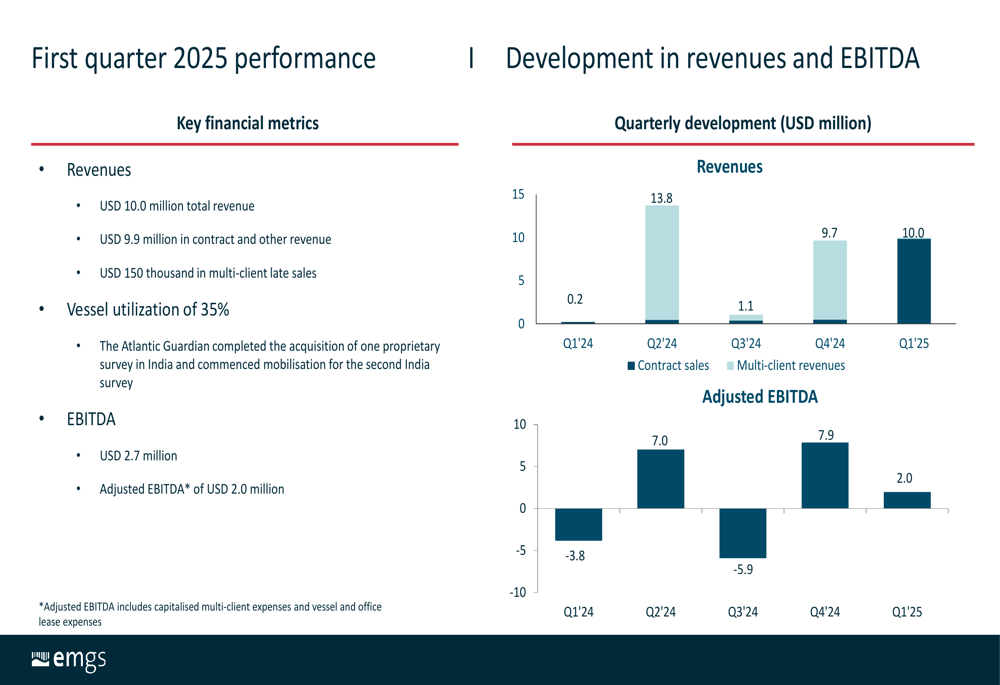

EMGS reported Q1 2025 revenues of USD 10 million, maintaining relatively consistent performance compared to the USD 9.7 million achieved in Q4 2024. However, adjusted EBITDA decreased to USD 2.0 million from USD 7.9 million in the previous quarter, reflecting increased operational costs.

The company completed the first of two proprietary acquisitions in India during the quarter and began mobilization for the second acquisition. Vessel utilization stood at 35%, with contract and other revenue accounting for USD 9.9 million of total revenue, while multi-client late sales contributed a modest USD 150,000.

As shown in the following chart of quarterly financial performance, EMGS has experienced significant fluctuations in both revenue and adjusted EBITDA over the past five quarters:

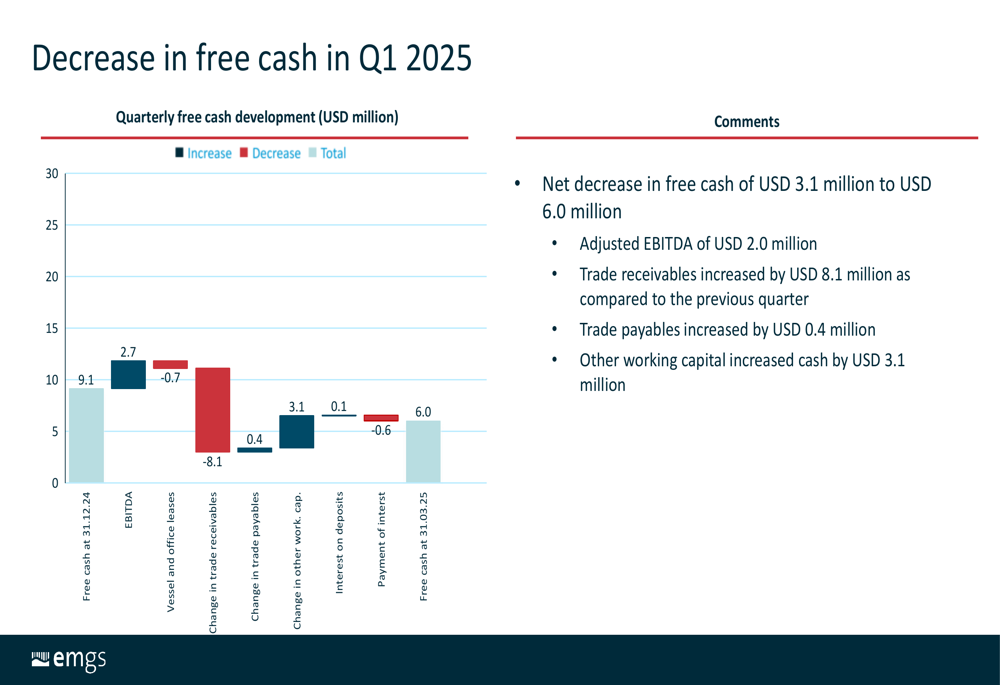

The company’s free cash position decreased by USD 3.1 million during the quarter, ending at USD 6.0 million. This reduction was primarily driven by an USD 8.1 million increase in trade receivables, partially offset by positive adjusted EBITDA and working capital changes.

The following cash flow breakdown illustrates the key factors affecting the company’s liquidity position:

Operational costs increased to USD 8.0 million in Q1 2025, up USD 3.3 million from Q4 2024. Management noted that USD 1.5 million in transit costs were capitalized in Q4 2024 and subsequently recognized in Q1 2025, contributing to this increase.

Strategic Expansion into Subsea Construction

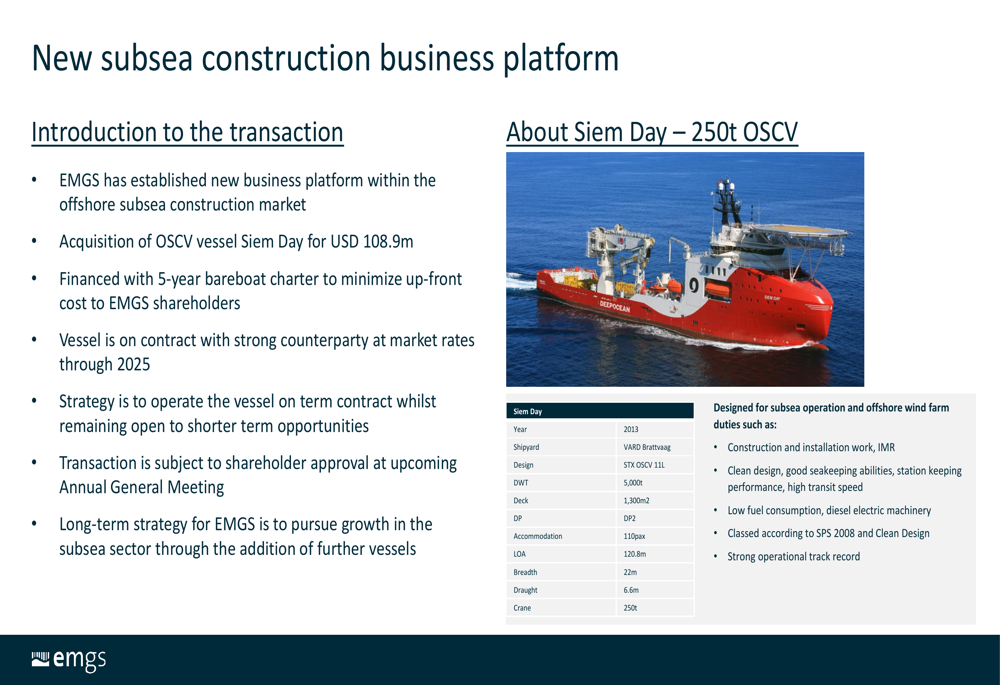

The most significant announcement in the presentation was EMGS’s establishment of a new business platform in the offshore subsea construction market through the acquisition of the OSCV vessel Siem Day for USD 108.9 million. This strategic move represents a major diversification for the company.

The following slide details the vessel specifications and transaction rationale:

The Siem Day, built in 2013, is a 250-ton offshore subsea construction vessel (OSCV) designed for subsea operations and offshore wind farm duties. The vessel is currently under contract through 2025, providing immediate revenue contribution to EMGS’s operations.

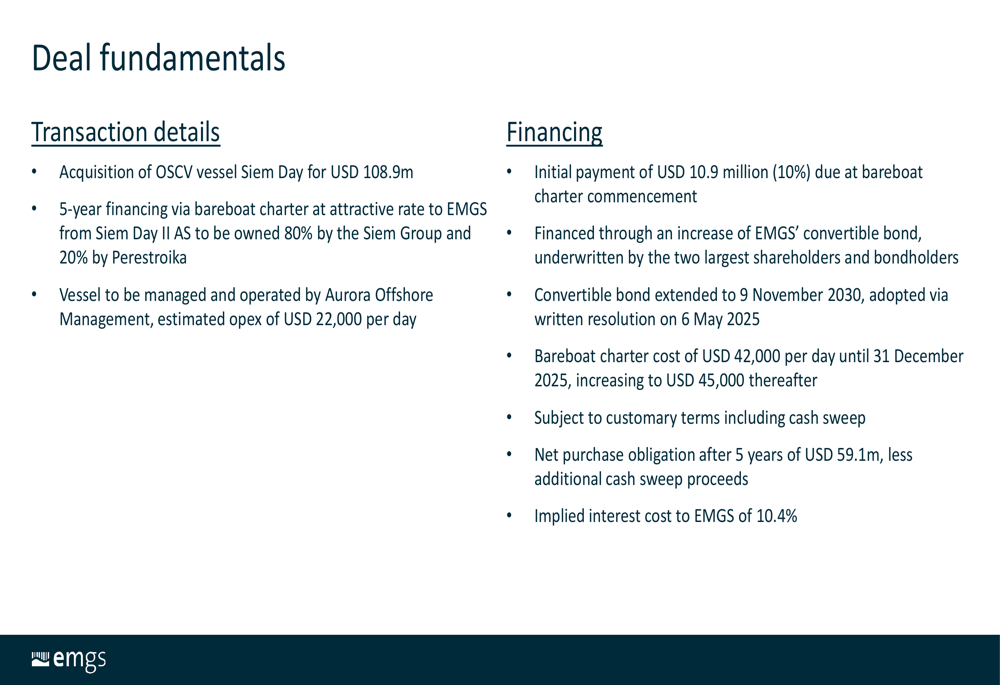

The acquisition financing structure includes an initial payment of USD 10.9 million funded through a convertible bond, with the remainder financed via a 5-year bareboat charter at USD 42,000 per day until December 2025, increasing to USD 45,000 thereafter. The implied interest cost to EMGS is 10.4%, with a net purchase obligation of USD 59.1 million after five years.

The transaction details and financing structure are outlined in the following slide:

Market Outlook and Forward-Looking Statements

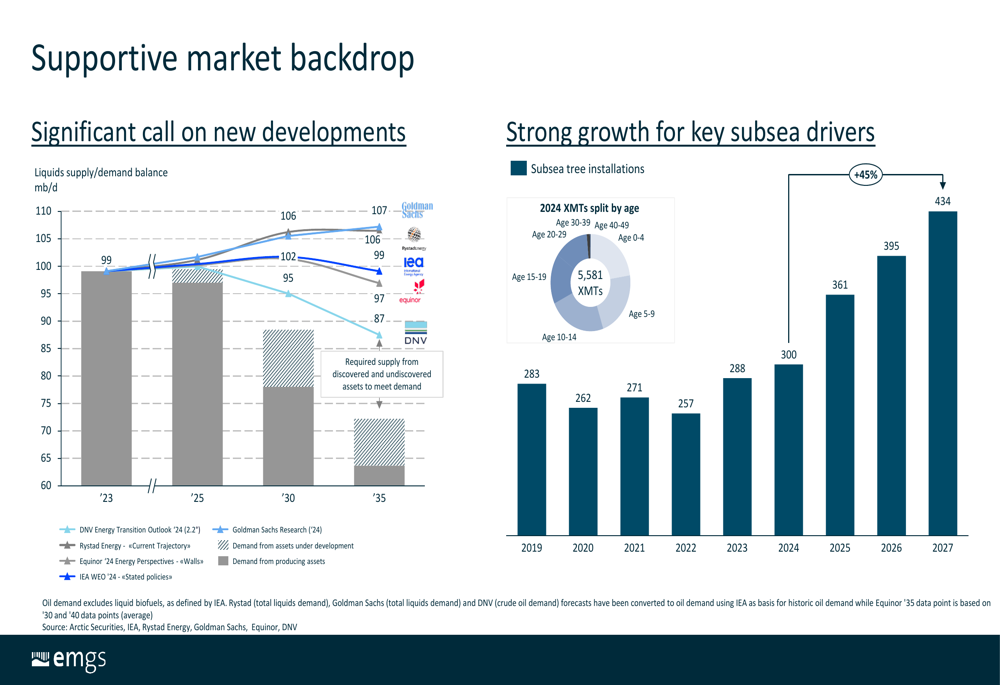

EMGS presented a bullish outlook for the subsea construction market, supporting its strategic expansion. The company highlighted forecasts showing significant demand for new offshore developments and strong growth in subsea tree installations, projected to increase by 45% from 283 in 2019 to 434 in 2027.

The market dynamics supporting this expansion are illustrated in the following chart:

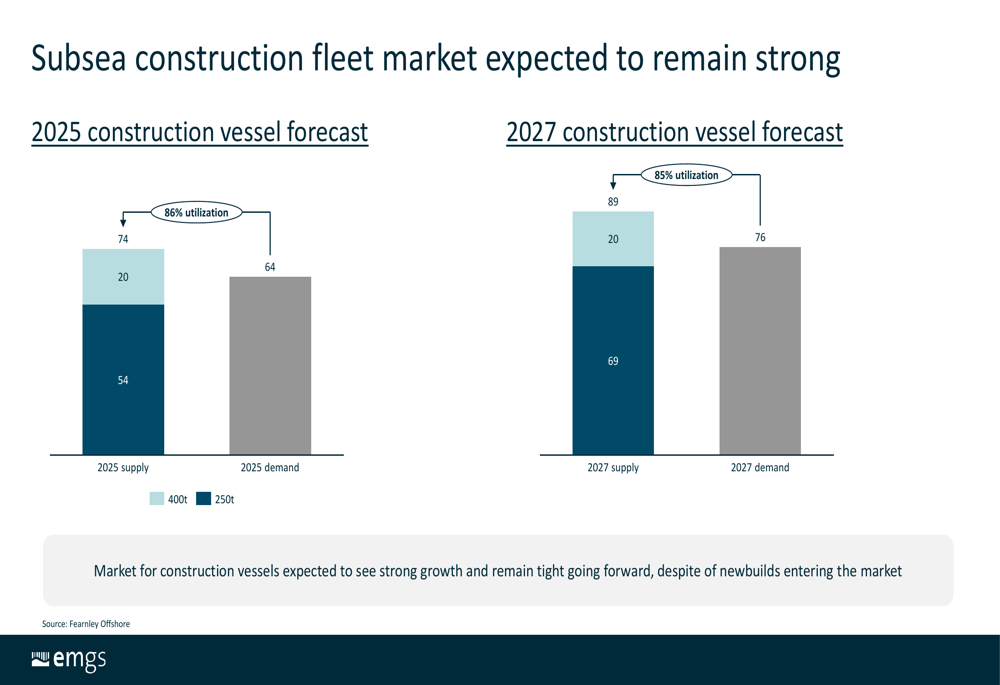

For the construction vessel market specifically, EMGS projects high utilization rates through 2027. The 2025 forecast shows a supply of 74 vessels against demand for 64 vessels, resulting in an 86% utilization rate. By 2027, despite an increase in vessel supply to 89 units, demand is expected to reach 76 vessels, maintaining a strong 85% utilization rate.

The following slide demonstrates the projected supply-demand balance in the construction vessel market:

Management emphasized that the market for construction vessels is expected to remain tight despite newbuilds, creating favorable conditions for EMGS’s entry into this sector. The company’s strategy includes operating the Siem Day on term contracts and pursuing further growth opportunities in the subsea sector.

Forward-Looking Statements

In addition to the vessel acquisition, EMGS announced the extension of its Senior Unsecured Convertible Bond (EMGS03) to November 2030, improving its long-term debt profile. The company expects to complete its second India acquisition at the beginning of June, after which the vessel will depart from India.

While the strategic expansion into subsea construction represents a significant opportunity, investors will likely focus on how EMGS manages the substantial financial commitment of the vessel acquisition alongside its existing operations, particularly given the decrease in free cash during Q1 2025 and the cyclical nature of its revenue performance over recent quarters.

The transaction remains subject to shareholder approval, with management positioning it as part of a long-term strategy to diversify revenue streams and capitalize on growth in the subsea sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.