Asia FX moves little with focus on US-China trade, dollar steadies ahead of CPI

Introduction & Market Context

Enerflex Ltd. (TSX:EFX, NYSE:EFXT) presented its Q2 2025 corporate update on August 7, 2025, highlighting record adjusted EBITDA performance and strategic positioning in growing natural gas markets. The company’s stock rose 11.1% following the presentation, reflecting positive investor sentiment about its financial discipline and growth strategy.

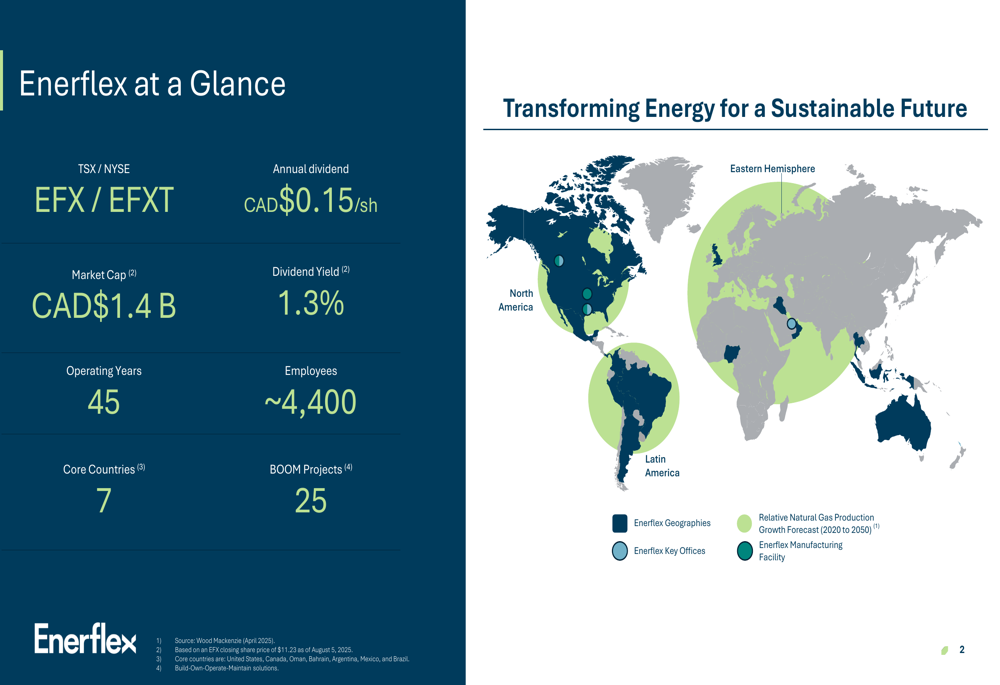

Operating for 45 years with approximately 4,400 employees across seven core countries, Enerflex has built a diversified energy infrastructure business with a market capitalization of CAD$1.4 billion. The company is strategically positioned to capitalize on the forecasted 15% growth in global natural gas demand over the next decade.

As shown in the following overview of Enerflex’s global presence and key metrics:

Financial Performance Highlights

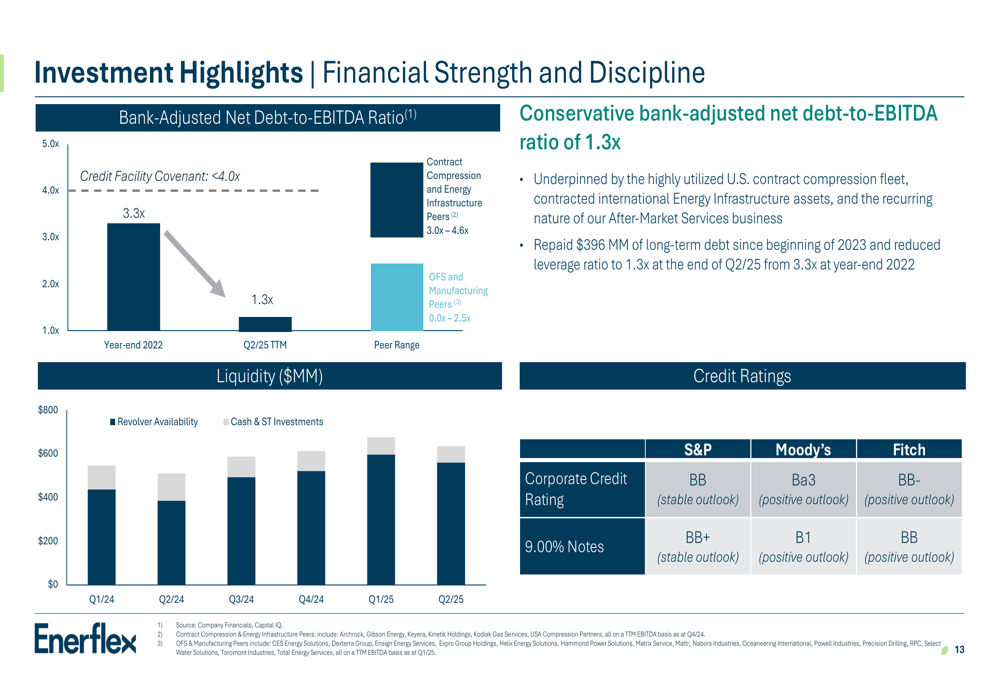

Enerflex reported record adjusted EBITDA of $130 million in Q2 2025, demonstrating the strength of its business model. The company has maintained a conservative financial position with a bank-adjusted net debt-to-EBITDA ratio of 1.3x, significantly lower than contract compression and energy infrastructure peers who range between 3.0x and 4.6x.

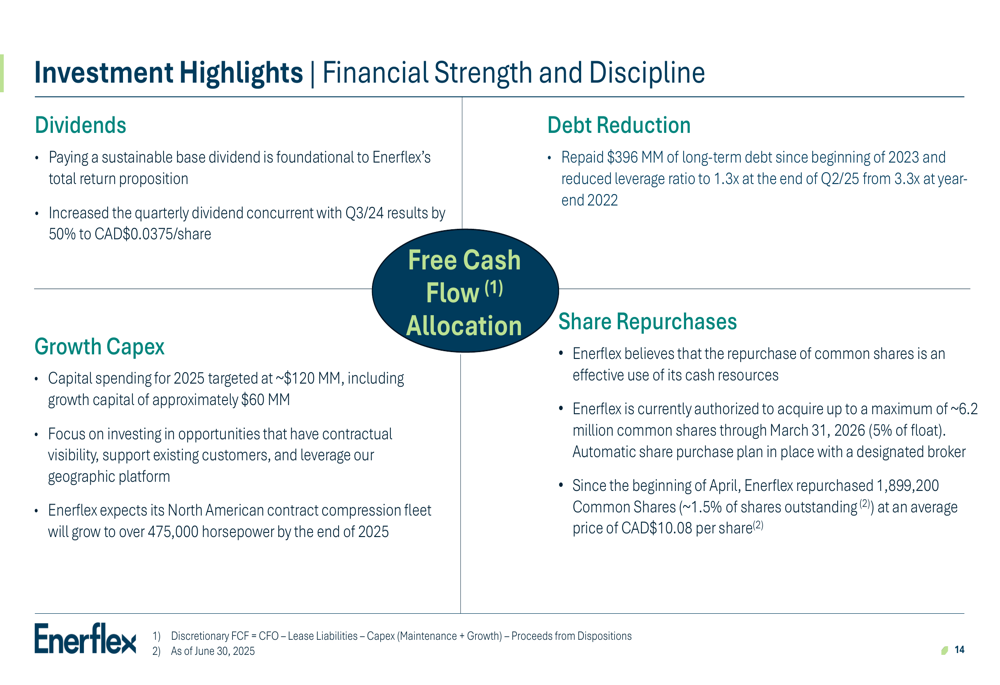

Since the beginning of 2023, Enerflex has repaid $396 million of long-term debt, improving its leverage ratio from 1.5x at the end of 2024 to the current 1.3x. This financial discipline has positioned the company to increase its quarterly dividend by 50% to CAD$0.0375 per share concurrent with Q3 2024 results.

The following chart illustrates Enerflex’s debt position relative to peers and its available liquidity:

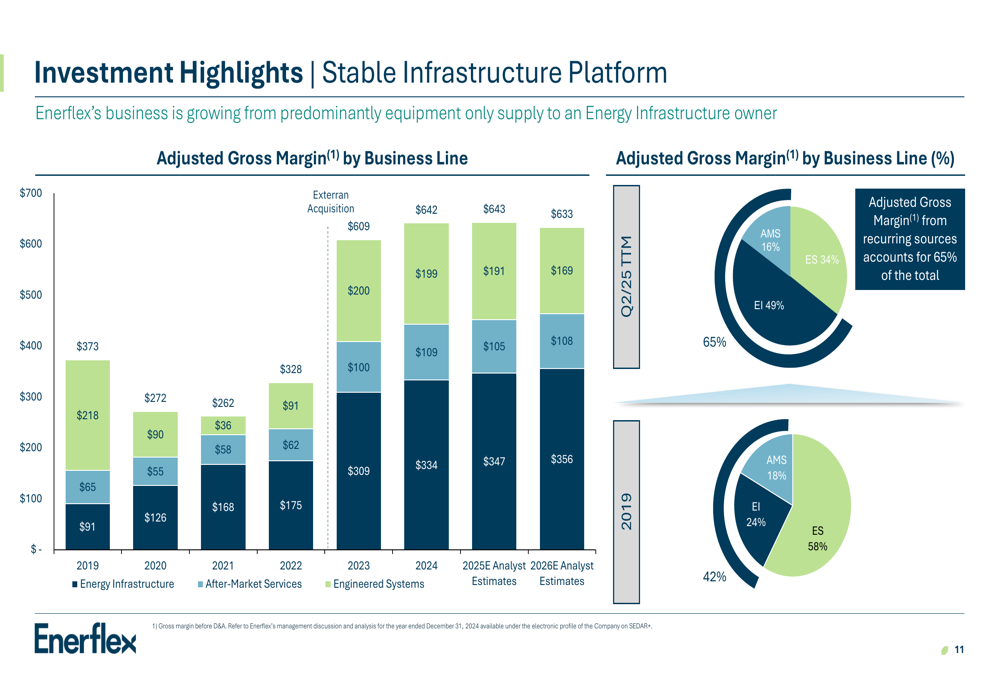

Enerflex’s business model provides stability through its diversified revenue streams. Energy Infrastructure and After-Market Services generated 66% of consolidated gross margin in Q2 2025, providing recurring revenue that balances the more cyclical Engineered Systems segment.

The company’s adjusted gross margin by business line shows the evolution of its revenue mix toward more stable, infrastructure-based earnings:

Growth Strategy and Market Positioning

Enerflex maintains strong relationships with major energy companies, with 100% of its top 10 customers being national oil companies or investment-grade corporations. These relationships average over 15 years in duration, providing stability and predictable revenue streams.

The company’s customer base includes industry leaders such as ExxonMobil (NYSE:XOM), Kinder Morgan (NYSE:KMI), Tourmaline, and Petrobras, as illustrated in the following customer overview:

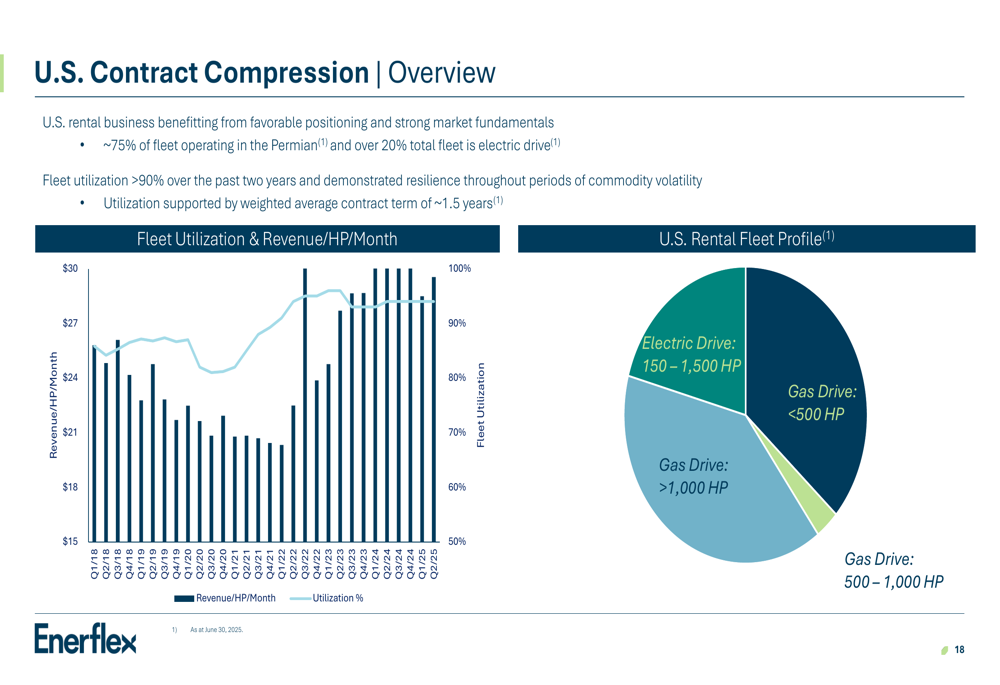

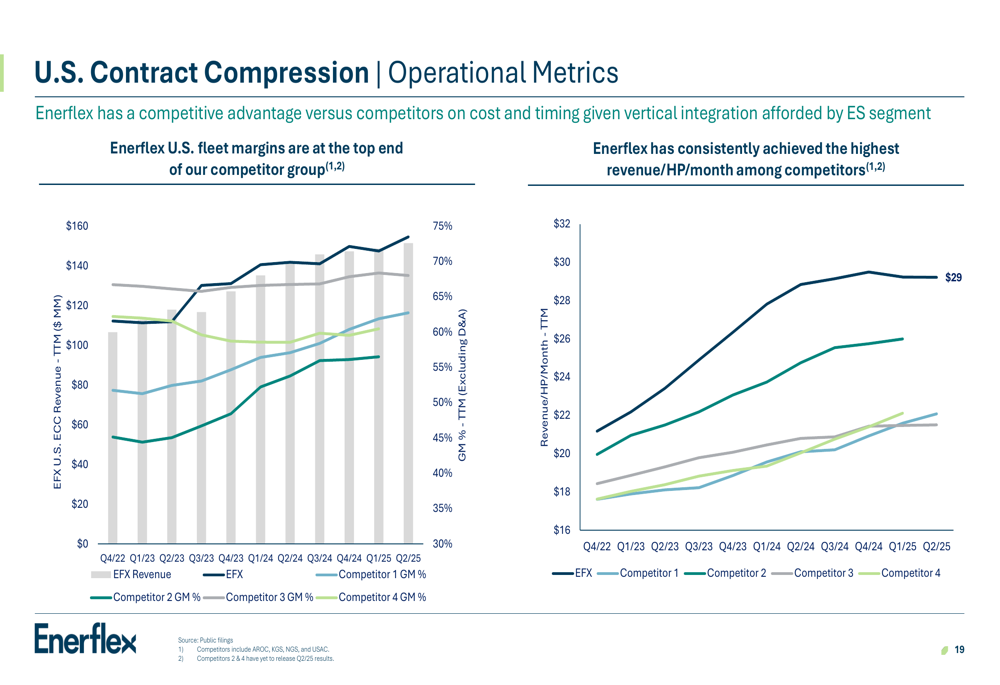

In the U.S., Enerflex’s contract compression business is performing exceptionally well, with approximately 75% of its fleet operating in the prolific Permian Basin. The company plans to expand its North American contract compression fleet to over 475,000 horsepower by the end of 2025, supported by strong market fundamentals.

The following chart shows the performance of Enerflex’s U.S. Contract Compression business:

Enerflex’s operational metrics in the U.S. contract compression market demonstrate its competitive advantage, with fleet margins at the top end of its competitor group:

Energy Transition Initiatives

While maintaining its core focus on natural gas infrastructure, Enerflex is strategically positioning itself to enable the energy transition through four key areas: Carbon Capture, Utilization and Storage (CCUS), Electrification, Bioenergy, and Methane Management.

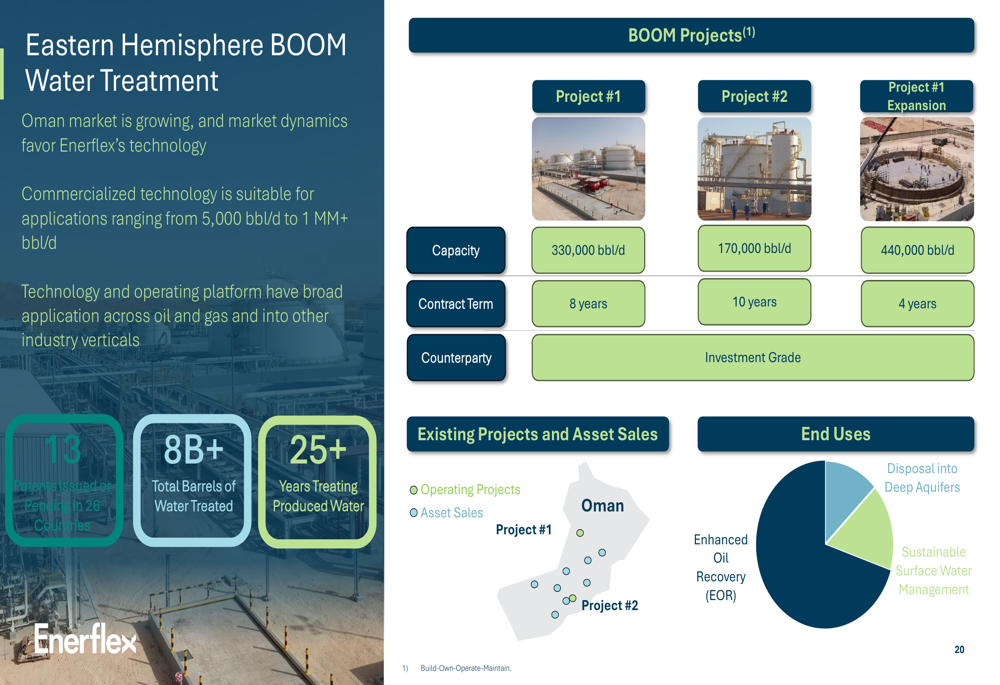

In the Eastern Hemisphere, Enerflex has established a growing presence in produced water treatment, with over 8 billion barrels of water treated across its operations. The company holds patents issued or pending in 26 countries related to water treatment technology.

The following slide details Enerflex’s Eastern Hemisphere BOOM Water Treatment operations:

Forward-Looking Statements

Looking ahead, Enerflex has outlined several priorities for 2025, including enhancing profitability in core operations, leveraging its positions to capitalize on natural gas and produced water volume growth, and maximizing free cash flow and returns for shareholders.

The company’s capital spending for 2025 is targeted at approximately $120 million, including growth capital of about $60 million. Additionally, Enerflex has initiated a share repurchase program authorized to acquire up to approximately 6.2 million common shares through March 31, 2026, representing 5% of its float. Since the beginning of April, the company has already repurchased 1,899,200 common shares at an average price of CAD$10.08 per share.

Enerflex’s capital allocation strategy balances growth investments, debt reduction, and shareholder returns:

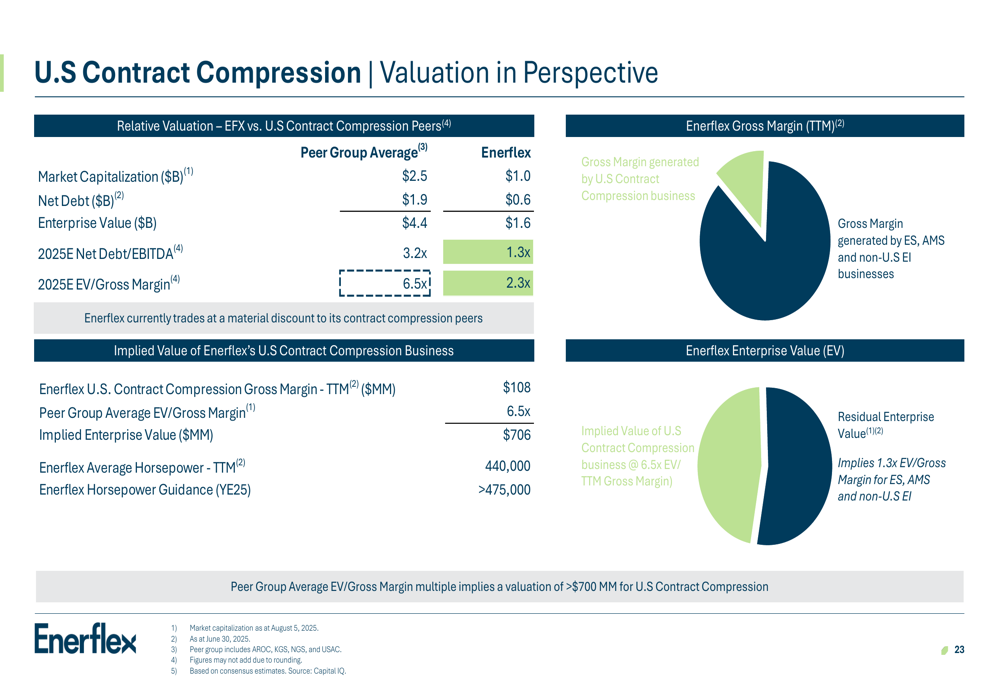

The company’s valuation appears attractive when compared to peers in the U.S. contract compression sector. Based on the company’s estimates, its U.S. contract compression business alone could be valued at approximately $706 million:

With strong financial discipline, strategic market positioning, and a focus on both traditional natural gas infrastructure and emerging energy transition opportunities, Enerflex appears well-positioned to capitalize on growing global energy demand while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.