D-Wave Quantum falls nearly 3% as earnings miss overshadows revenue beat

Energizer Holdings Inc (NYSE:ENR) shares jumped 10.57% in premarket trading Monday after the company released its Q3 fiscal 2025 earnings presentation, revealing stronger-than-expected results and an improved full-year outlook. The battery and auto care products manufacturer reported significant earnings growth and progress on strategic initiatives despite modest organic sales growth.

Quarterly Performance Highlights

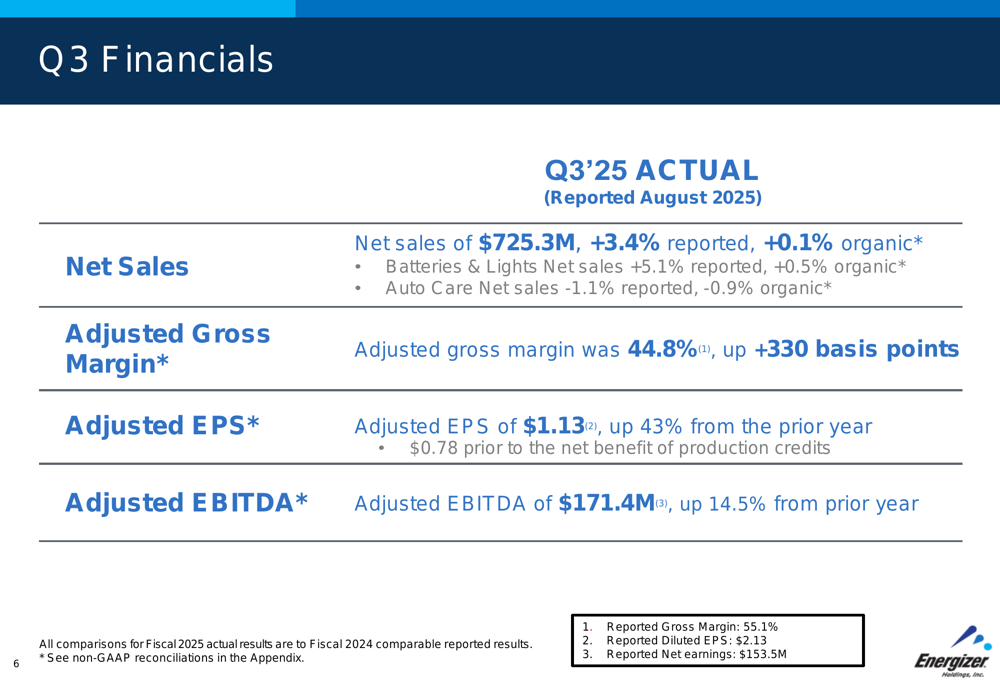

Energizer delivered a robust third quarter with results exceeding management’s expectations. Net sales reached $725.3 million, representing a 3.4% reported increase and a slight 0.1% organic growth compared to the same period last year. This marks a notable improvement from the flat sales reported in Q2 2025.

The company’s adjusted earnings per share surged 43% year-over-year to $1.13, significantly higher than the $0.67 reported in the previous quarter. Management noted that EPS would have been $0.78 prior to the net benefit of production credits. Adjusted EBITDA increased 14.5% to $171.4 million, while adjusted gross margin expanded 330 basis points to 44.8%.

As shown in the following financial results slide:

The battery and lights segment performed well with sales increasing 5.1% on a reported basis and 0.5% organically. However, the auto care segment experienced a decline of 1.1% reported and 0.9% organic, contrasting with the 5.5% organic growth reported in Q2.

Strategic Initiatives

Energizer continues to strengthen its market position through strategic acquisitions and product innovations. The company recently acquired a European battery business, expanding its footprint in key markets. This aligns with Energizer’s strategy to grow its global presence while maintaining financial discipline.

The company highlighted its growing battery market share in the U.S. while advancing its sustainability agenda with a plastic-free transition underway in the battery category:

In the auto care segment, Energizer has expanded its premium Armor All Podium Series to over 15,000 stores globally, demonstrating the company’s commitment to product innovation despite the segment’s recent sales challenges:

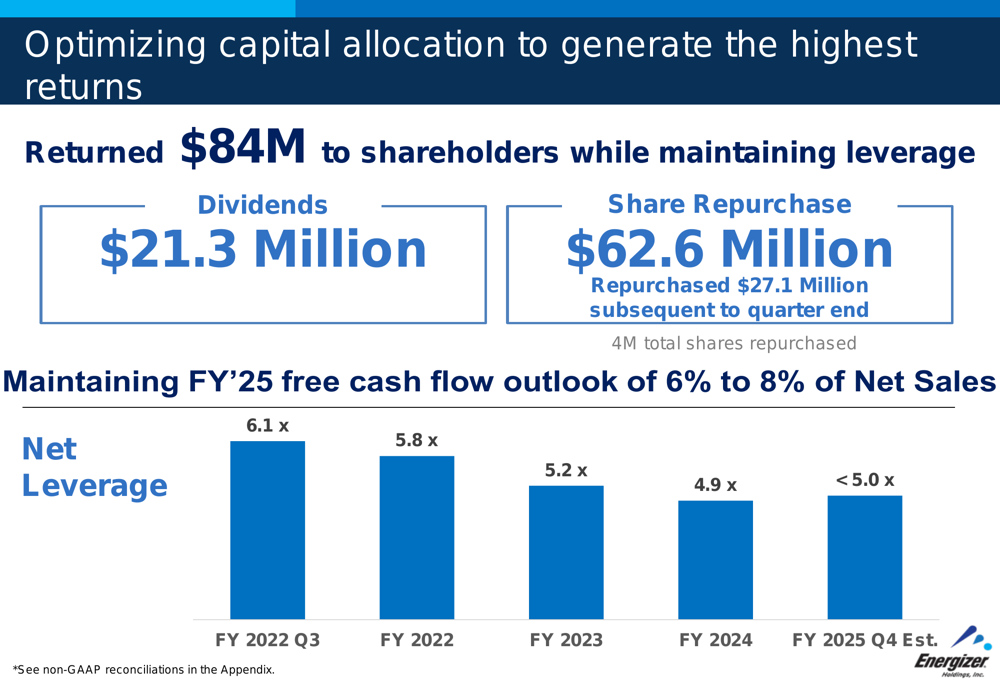

Capital Allocation and Shareholder Returns

Energizer returned $84 million to shareholders during the quarter while maintaining its leverage targets. This included $21.3 million in dividends and $62.6 million in share repurchases, with an additional $27.1 million in shares repurchased after the quarter ended. In total, the company has repurchased 4 million shares.

The company continues to make progress on reducing its debt burden, with net leverage expected to remain below 5.0x by the end of fiscal 2025, down significantly from 6.1x in Q3 fiscal 2022:

Forward-Looking Statements

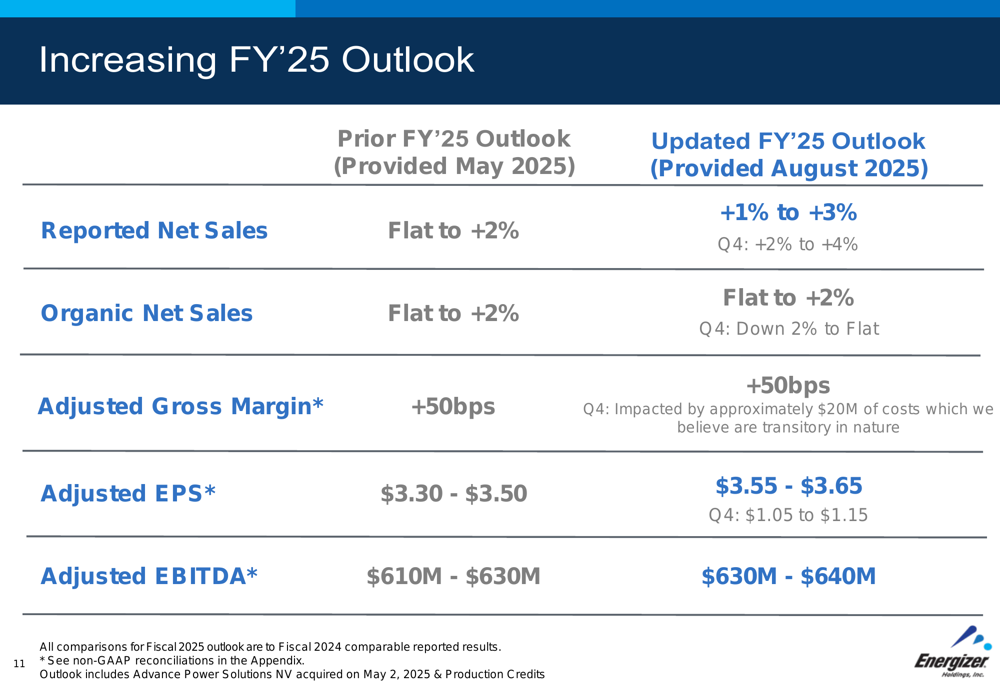

Following the strong quarterly performance, Energizer raised its full-year 2025 outlook across multiple metrics. The company now expects reported net sales to increase 1% to 3%, up from its previous guidance of flat to 2% growth. The organic net sales outlook remains unchanged at flat to 2% growth.

Adjusted earnings per share guidance was raised to $3.55-$3.65, compared to the previous range of $3.30-$3.50. Similarly, the adjusted EBITDA forecast was increased to $630-$640 million from $610-$630 million.

For the fourth quarter specifically, Energizer projects reported net sales growth of 2% to 4%, though organic net sales are expected to decline 2% to remain flat. The company also warned of approximately $20 million in costs during Q4 that management believes are "transitory in nature."

The updated outlook is detailed in the following slide:

Detailed Financial Analysis

Energizer’s financial position continues to strengthen, with the company maintaining its free cash flow outlook of 6% to 8% of net sales for fiscal 2025. This consistent cash generation supports both the company’s shareholder returns and strategic investments.

The company emphasized its ability to fully offset earnings impact from tariffs, positioning it for continued growth. Management expects to generate 7% to 10% adjusted EPS growth in 2025 and believes the company is "strongly positioned to drive earnings growth in 2026."

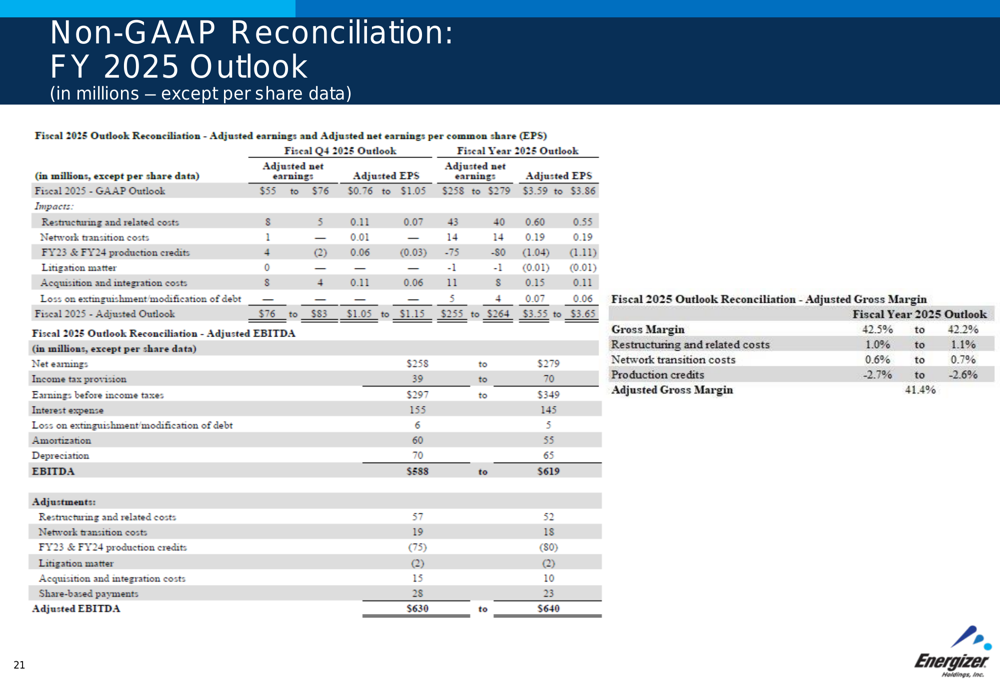

The financial reconciliation shows how production credits and other adjustments contributed to the company’s performance:

This quarter represents a significant improvement from Energizer’s Q2 results, when the stock fell 6.88% despite meeting earnings expectations. The contrast between the market reactions highlights investors’ positive reception to the company’s accelerating performance and raised guidance.

With its strategic European acquisition, ongoing production efficiencies, and improved financial outlook, Energizer appears to be successfully navigating industry challenges while positioning itself for sustained growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.