Raymond James raises Fulgent Genetics stock price target to $36 on strong performance

Introduction & Market Context

Enovis Corporation (NASDAQ:ENOV) reported solid third-quarter 2025 results on November 6, highlighting 9% year-over-year revenue growth and raised guidance for the full year. Despite beating analyst expectations with adjusted earnings per share of $0.75 against a forecast of $0.649, Enovis shares declined 3.6% in regular trading, following a 1.24% drop in pre-market activity.

The medical technology company, which focuses on orthopedic implants and rehabilitation products, delivered revenue of $549 million for the quarter, exceeding analyst projections of $538.61 million. However, a non-cash goodwill impairment charge of $548 million overshadowed some of the positive operational performance.

Quarterly Performance Highlights

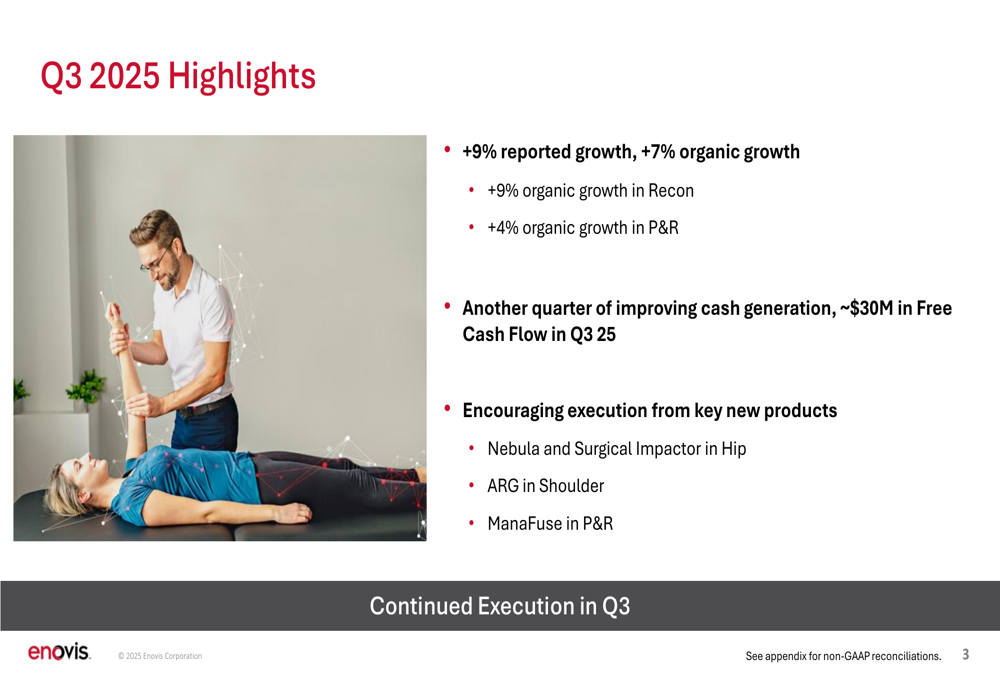

Enovis reported strong organic growth of 7% in the third quarter, with its Reconstructive segment leading the way at 9% organic growth while the Prevention & Recovery (P&R) segment contributed 4% organic growth.

The company’s adjusted gross profit margin expanded by 140 basis points year-over-year, reaching 60.3% in Q3 2025 compared to 58.9% in Q3 2024. This improvement reflects the company’s focus on operational excellence and product mix optimization.

As shown in the following quarterly highlights slide, Enovis also generated approximately $30 million in free cash flow during the quarter, demonstrating improving cash generation capabilities:

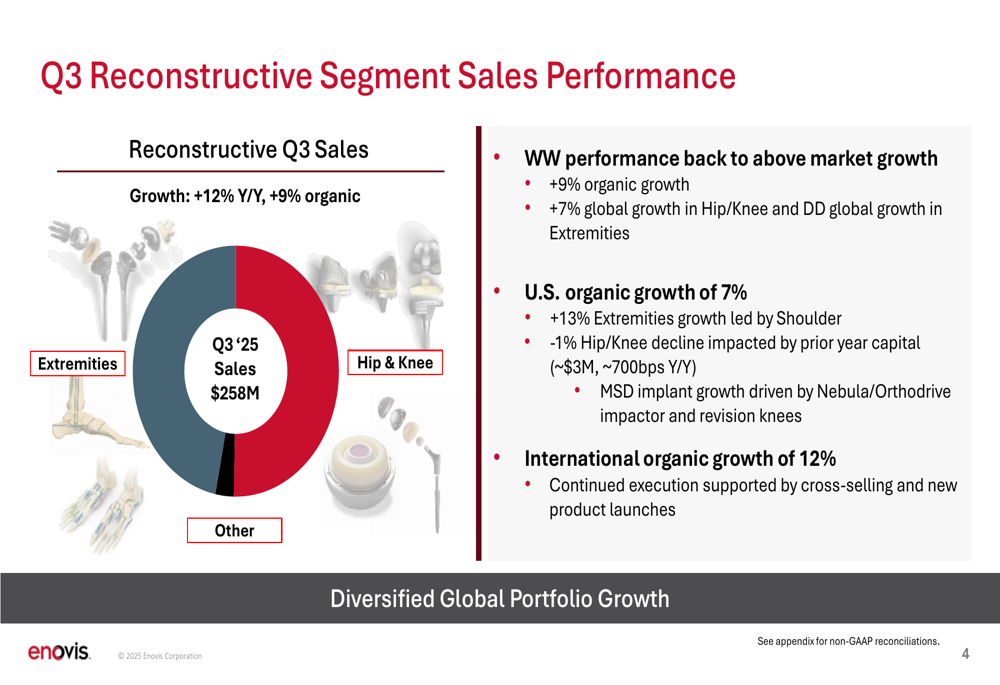

The Reconstructive segment, which includes extremities, hip, and knee products, delivered particularly strong results with 12% year-over-year growth (9% organic). International markets showed robust organic growth of 12%, supported by cross-selling initiatives and new product launches. U.S. organic growth reached 7%, with extremities growing at 13%, though hip and knee sales declined slightly by 1% due to prior year capital impacts.

The following slide details the Reconstructive segment’s performance:

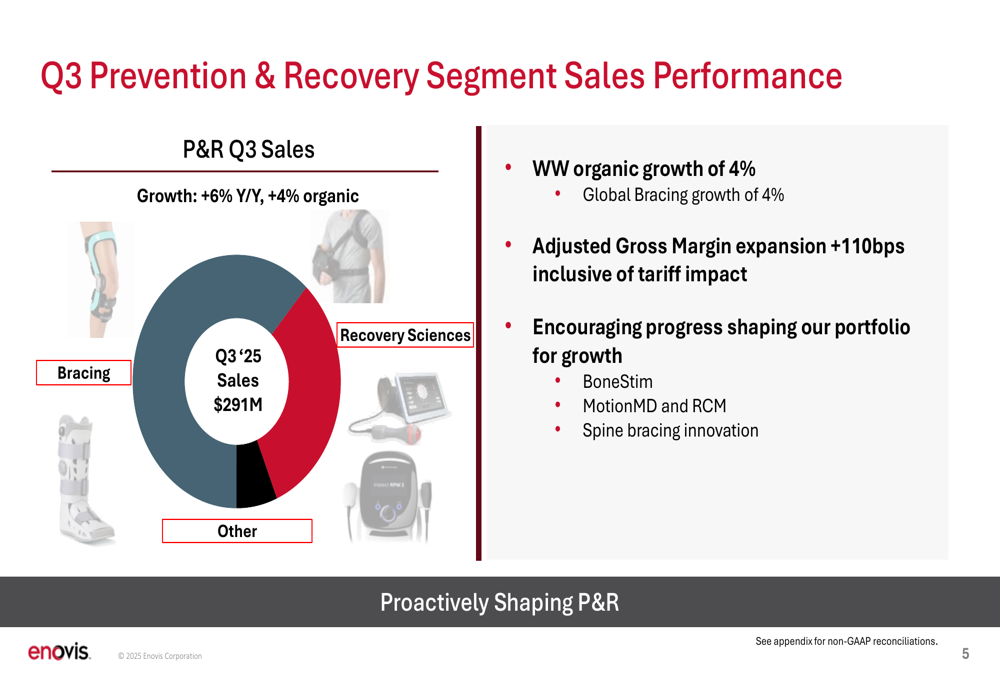

The Prevention & Recovery segment, which focuses on bracing and recovery sciences, grew 6% year-over-year (4% organic). The segment achieved adjusted gross margin expansion of 110 basis points despite tariff impacts, with encouraging progress in portfolio optimization through BoneStim, MotionMD, RCM, and spine bracing innovations.

The P&R segment’s performance is illustrated in this breakdown:

Detailed Financial Analysis

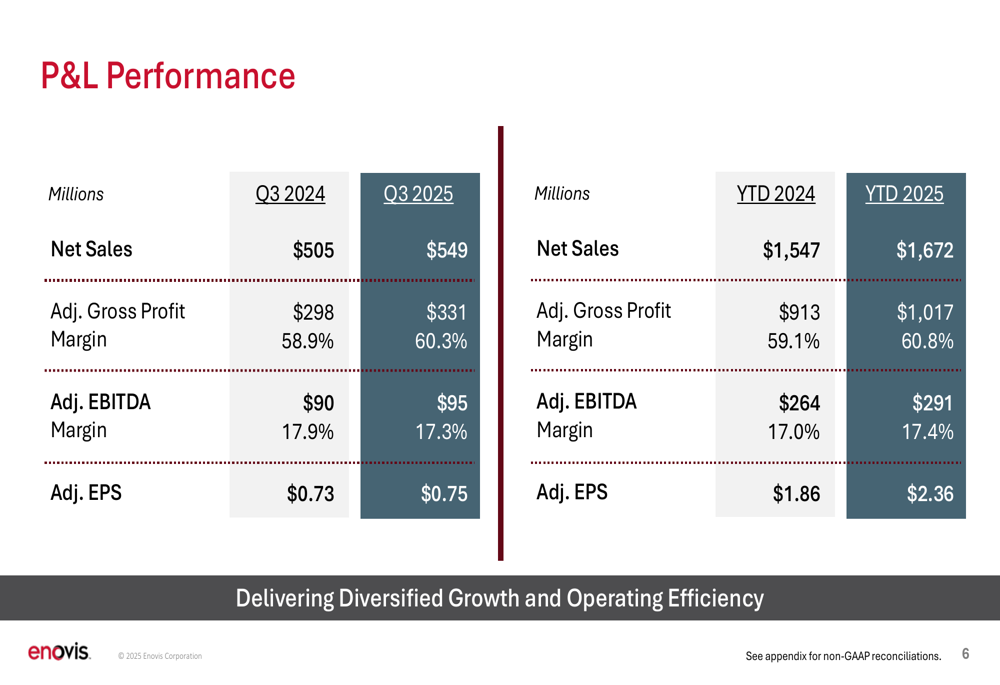

Enovis’s P&L performance shows improvement across several key metrics compared to the prior year. While adjusted EBITDA margin slightly decreased from 17.9% to 17.3% year-over-year for Q3, the year-to-date figure improved from 17.0% to 17.4%.

The company’s adjusted EPS increased from $0.73 in Q3 2024 to $0.75 in Q3 2025, representing a 2.7% improvement. Year-to-date adjusted EPS showed more substantial growth, rising from $1.86 to $2.36, a 26.9% increase.

The comprehensive P&L performance is detailed in the following slide:

The financial results reflect Enovis’s ability to navigate a dynamic global macroeconomic environment while continuing to invest in growth initiatives. The slight compression in quarterly EBITDA margin appears to be a strategic trade-off for revenue growth and long-term positioning.

Strategic Initiatives

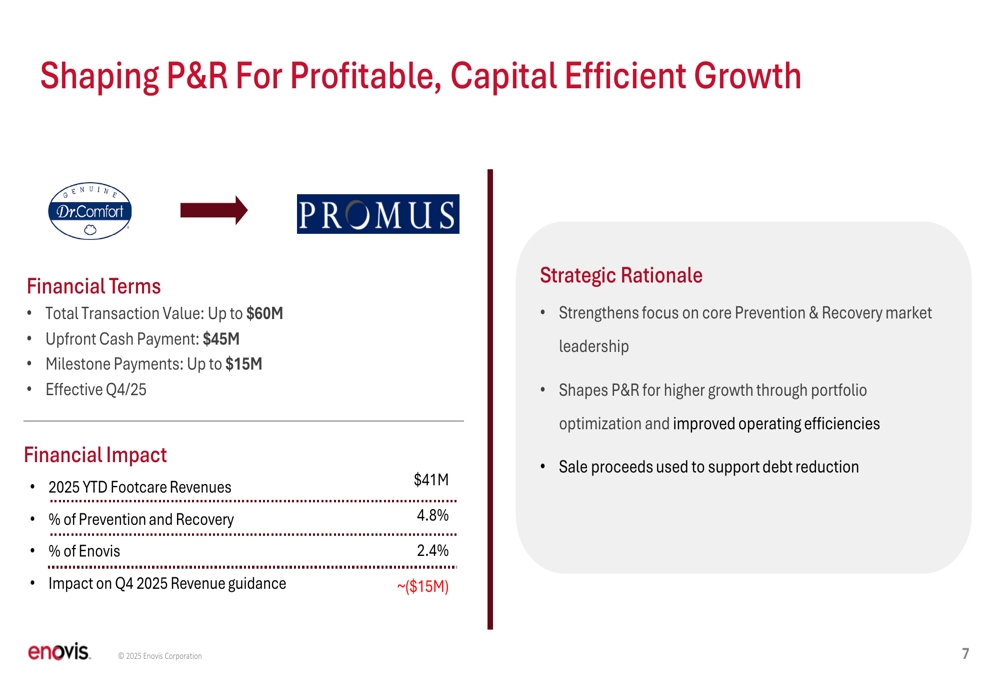

A significant strategic development announced during the quarter is Enovis’s divestiture of its Diabetic Footwear business for up to $60 million, comprising a $45 million upfront payment and potential milestone payments of up to $15 million. The transaction, effective in Q4 2025, involves the sale of a business that generated $41 million in revenue year-to-date, representing 4.8% of the Prevention & Recovery segment and 2.4% of total Enovis revenue.

This strategic move aims to strengthen the company’s focus on core Prevention & Recovery market leadership while shaping the segment for higher growth through portfolio optimization and improved operating efficiencies. The proceeds from the sale will support debt reduction efforts.

The details of this strategic transaction are outlined in this slide:

Enovis continues to emphasize innovation as a growth driver, with encouraging execution from key new products including Nebula and Surgical Impactor in Hip, ARG in Shoulder, and ManaFuse in the Prevention & Recovery segment. These product launches are expected to fuel continued above-market growth, particularly in the Reconstructive segment.

Forward-Looking Statements

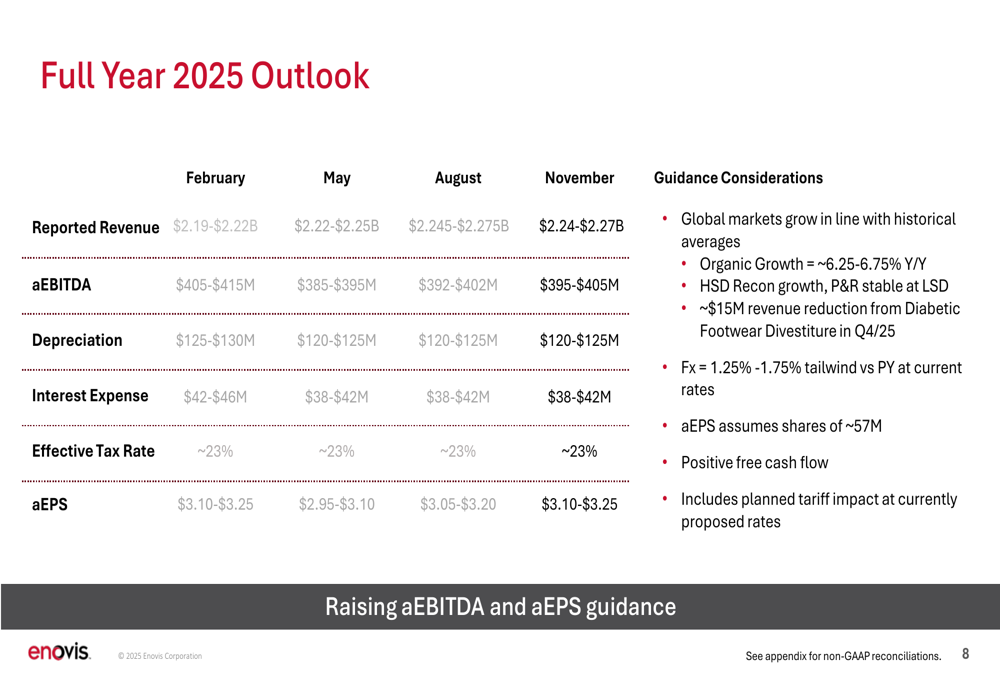

Enovis has raised its full-year 2025 guidance for adjusted EBITDA and adjusted EPS, reflecting management’s confidence in the company’s operational performance and growth trajectory. The updated outlook projects:

- Revenue of $2.24-$2.27 billion (maintained from August guidance)

- Adjusted EBITDA of $395-$405 million (raised from $392-$402 million)

- Adjusted EPS of $3.10-$3.25 (raised from $3.05-$3.20)

The guidance accounts for approximately $15 million in revenue reduction from the Diabetic Footwear divestiture in Q4 2025, as well as planned tariff impacts at currently proposed rates. The company expects organic growth of approximately 6.25-6.75% year-over-year, with high single-digit growth in the Reconstructive segment and low single-digit growth in Prevention & Recovery.

The evolution of the company’s 2025 guidance is presented in this comprehensive outlook slide:

Enovis’s management summarized the quarter by highlighting solid execution demonstrating the power of its diversified portfolio, global Reconstructive growth above market fueled by recent launches, continued management of the dynamic global macroeconomic environment, raised guidance, and improving cash flow.

Despite the positive operational performance and raised guidance, the market reaction suggests investors may be concerned about the goodwill impairment charge or potential headwinds in the broader orthopedic market. The company’s focus on portfolio optimization and innovation, however, positions it to potentially deliver long-term value beyond current market sentiment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.