US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

Enpro Industries (NYSE:NPO) presented its second-quarter 2025 earnings results on August 5, 2025, reporting solid revenue growth but facing some margin pressure across its business segments. The company’s stock closed at $214.88 prior to the earnings release, representing a 2.37% gain on the previous trading day and continuing its strong performance from earlier in the year.

The industrial manufacturer, which specializes in sealing technologies and advanced surface solutions, has seen its stock trade near its 52-week high of $218.93, reflecting investor confidence in the company’s growth trajectory. This follows a strong first quarter where Enpro exceeded analyst expectations with an EPS of $1.90 against a forecast of $1.73.

Quarterly Performance Highlights

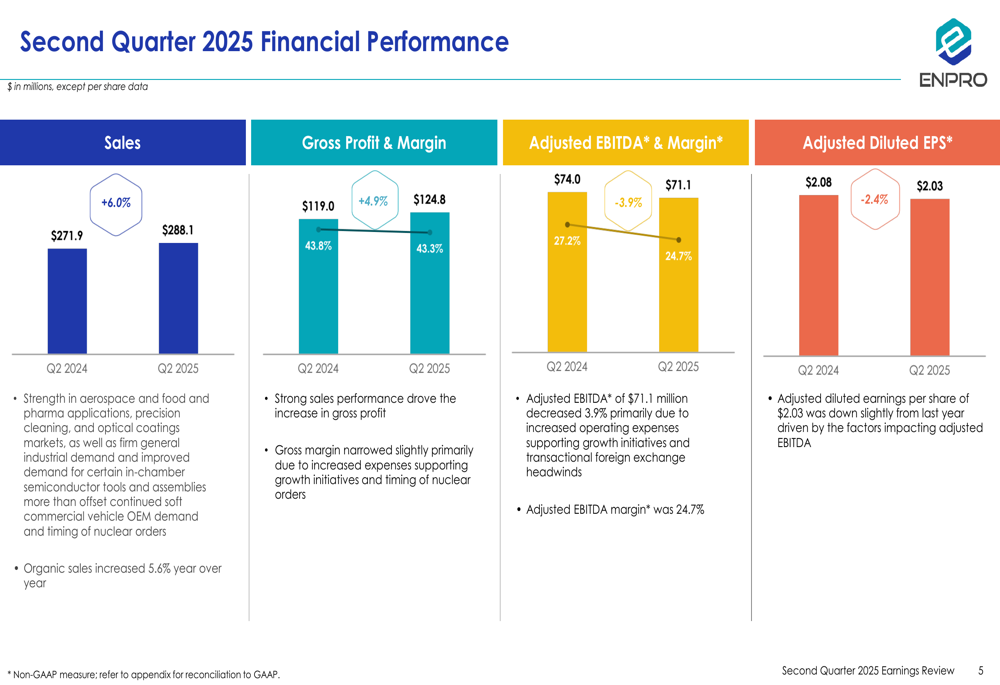

Enpro reported second-quarter sales of $288.1 million, representing a 6.0% increase compared to $271.9 million in the same period last year. Organic sales growth was slightly lower at 5.6%, indicating minimal contribution from acquisitions.

As shown in the following financial performance summary:

While revenue growth was robust, profitability metrics showed some pressure. Gross profit increased 4.9% to $124.8 million, but gross margin contracted slightly to 43.3% from 43.8% in Q2 2024. More notably, adjusted EBITDA decreased 3.9% to $71.1 million, with the adjusted EBITDA margin falling to 24.7% from 27.2% in the prior-year period. Adjusted diluted EPS also declined slightly by 2.4% to $2.03 from $2.08.

The company attributed its revenue growth to strength in aerospace, food and pharmaceutical markets, precision cleaning solutions, optical coatings, and improved demand for certain semiconductor tools and assemblies. General industrial demand also contributed positively to the results.

Segment Analysis

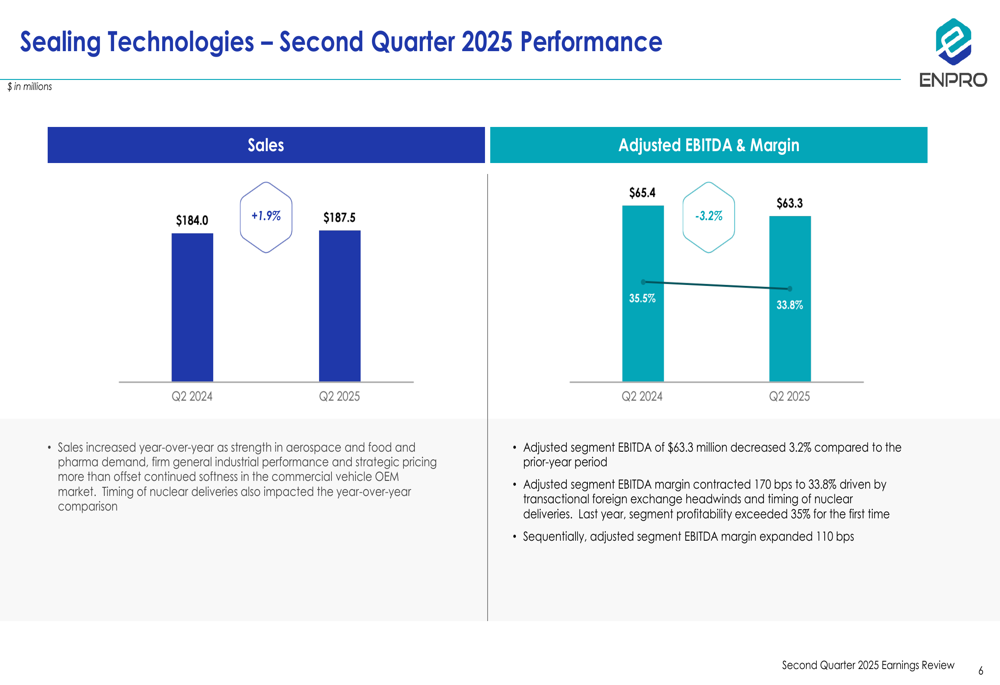

Enpro’s performance showed significant divergence between its two main business segments. The Sealing Technologies segment, which represents approximately 65% of total revenue, reported modest growth but faced margin challenges as illustrated in this segment breakdown:

Sealing Technologies sales increased 1.9% to $187.5 million, driven by strength in aerospace and food and pharma demand, along with general industrial performance. However, this growth was partially offset by continued softness in the commercial vehicle OEM market. The segment’s adjusted EBITDA decreased 3.2% to $63.3 million, with margin contraction of 170 basis points to 33.8%. Management cited transactional foreign exchange headwinds and the timing of nuclear deliveries as factors impacting the segment’s profitability.

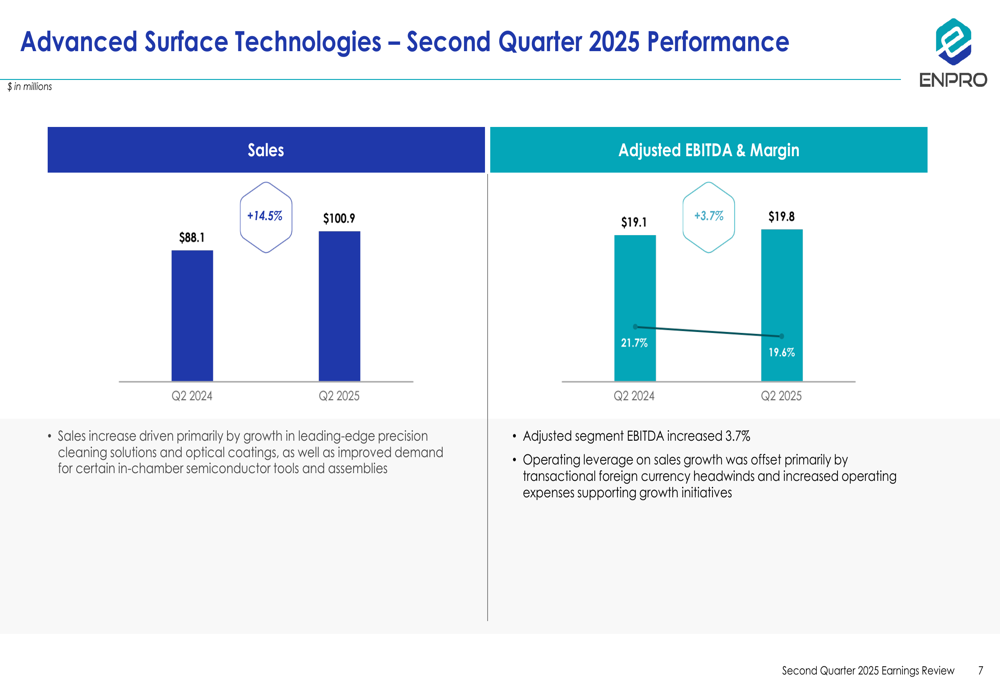

In contrast, the Advanced Surface Technologies segment delivered exceptional growth:

This segment, which accounts for 35% of total revenue, saw sales surge 14.5% to $100.9 million, primarily driven by growth in leading-edge precision cleaning solutions and optical coatings, as well as improved demand for certain in-chamber semiconductor tools and assemblies. Adjusted EBITDA increased 3.7% to $19.8 million, though margin decreased from 21.7% to 19.6%. The company explained that operating leverage on sales growth was offset by transactional foreign currency headwinds and increased operating expenses supporting growth initiatives.

Balance Sheet and Cash Flow

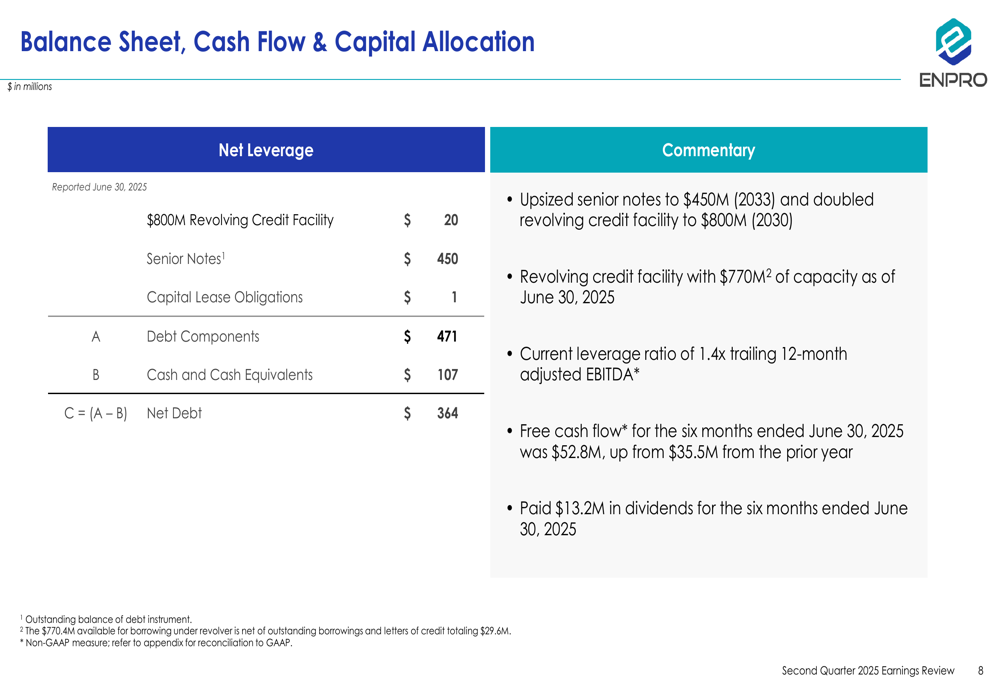

Enpro maintained a strong financial position in the second quarter, as detailed in the following balance sheet and cash flow summary:

The company reported net debt of $364 million, resulting in a leverage ratio of 1.4x trailing 12-month adjusted EBITDA, indicating a conservative financial position. Notably, Enpro has upsized its senior notes to $450 million (due 2033) and doubled its revolving credit facility to $800 million (due 2030), with $770 million of capacity available as of June 30, 2025.

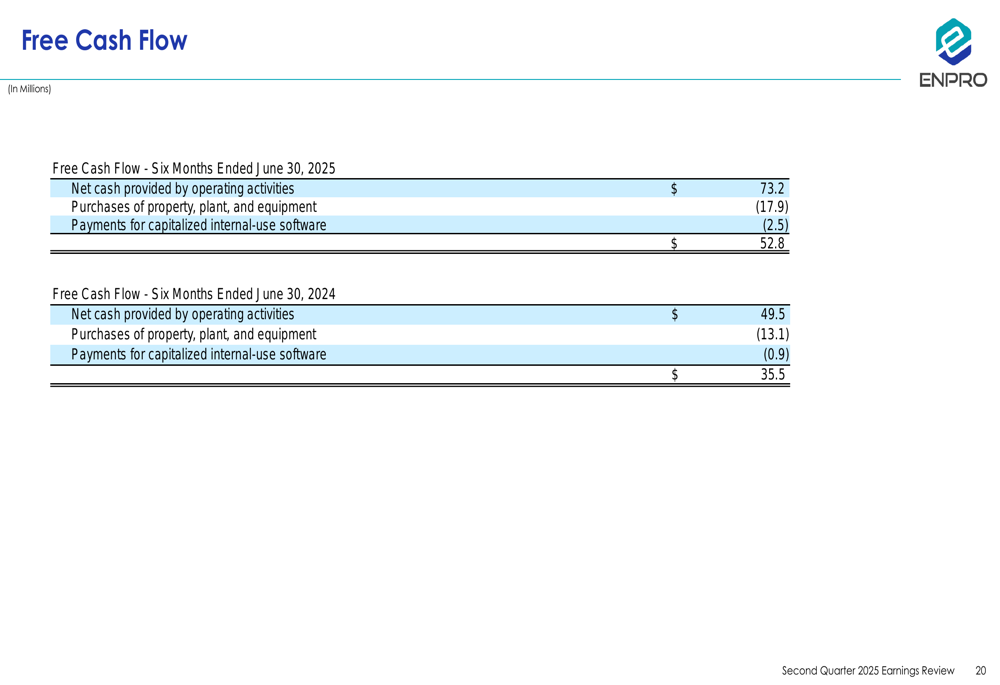

Free cash flow performance showed significant improvement:

For the six months ended June 30, 2025, free cash flow reached $52.8 million, up substantially from $35.5 million in the prior-year period. This 48.7% increase demonstrates the company’s improved operational efficiency and cash generation capabilities. During this period, Enpro paid $13.2 million in dividends, continuing its 11-year streak of dividend payments.

Updated Guidance and Outlook

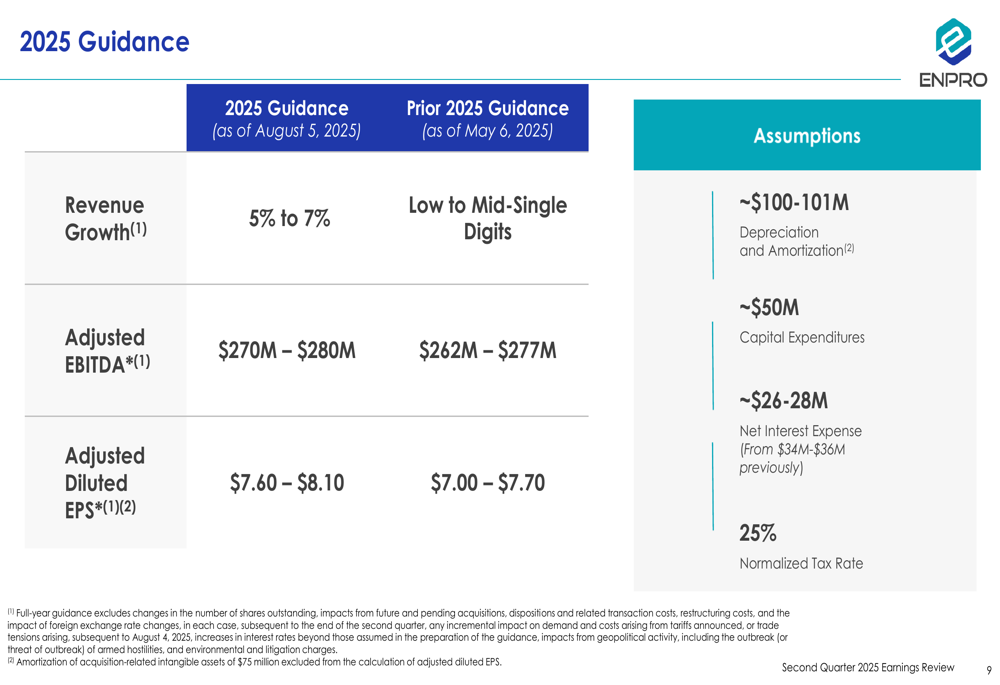

Despite the mixed quarterly results, Enpro raised its full-year 2025 guidance across all metrics, suggesting management confidence in the company’s outlook for the second half of the year:

The updated guidance projects revenue growth of 5% to 7%, increased from the previous guidance of "low to mid-single digits" provided in May. Adjusted EBITDA is now expected to be between $270 million and $280 million, up from the prior range of $262 million to $277 million. Similarly, adjusted diluted EPS guidance was raised to $7.60-$8.10 from $7.00-$7.70.

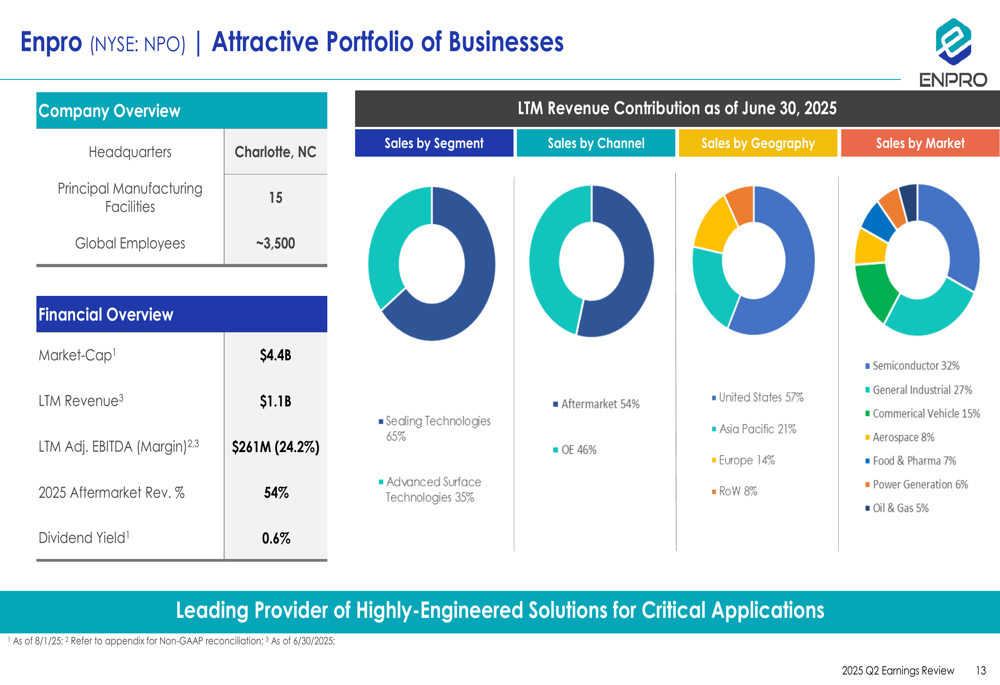

The company’s portfolio remains well-diversified across markets and geographies, providing some insulation against sector-specific downturns:

With semiconductor and general industrial markets representing the largest portions of revenue (32% and 27% respectively), Enpro is positioned to benefit from continued growth in these sectors. The company’s aftermarket business, which accounts for 54% of sales, provides a stable revenue base and typically carries higher margins than original equipment sales.

Looking ahead, Enpro appears well-positioned to navigate potential challenges in the commercial vehicle market while capitalizing on growth opportunities in aerospace, semiconductor, and food and pharmaceutical sectors. The increased guidance suggests management expects margin pressures to ease in the second half of 2025, potentially through pricing actions, operational efficiencies, or improved foreign exchange conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.