Bitcoin price today: gains to $120k, near record high on U.S. regulatory cheer

Introduction & Market Context

Empresa Nacional de Telecomunicaciones S.A. (Entel) presented its second quarter 2025 results on August 5, revealing a company maintaining strong market positions in Chile and Peru despite facing some financial headwinds. The telecommunications provider reported revenue growth and stable EBITDA margins, while continuing to invest heavily in strategic initiatives like fiber deployment and 5G expansion.

Entel’s stock (SNSE:ENTEL) has performed well over the past year, delivering a 38.11% return despite a slight 1.94% decline following the earnings announcement. The company continues to maintain its BBB- investment grade rating from S&P Global Ratings and offers an attractive 12.71% dividend yield.

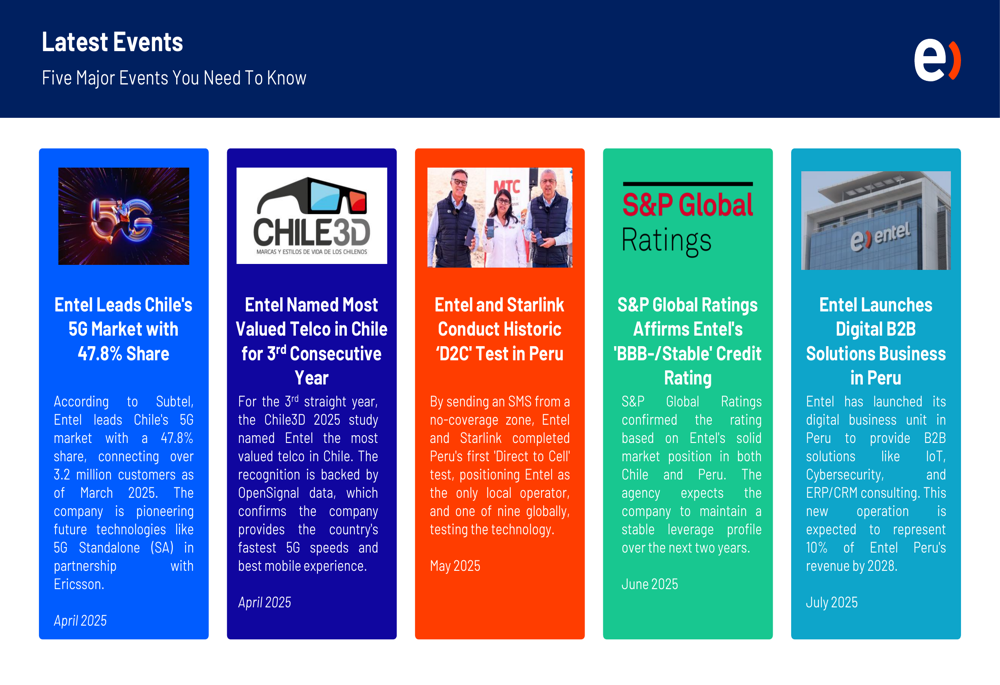

As shown in the following chart highlighting Entel’s key recent achievements, the company has secured a dominant position in Chile’s 5G market and is pioneering satellite connectivity solutions in Latin America:

Quarterly Performance Highlights

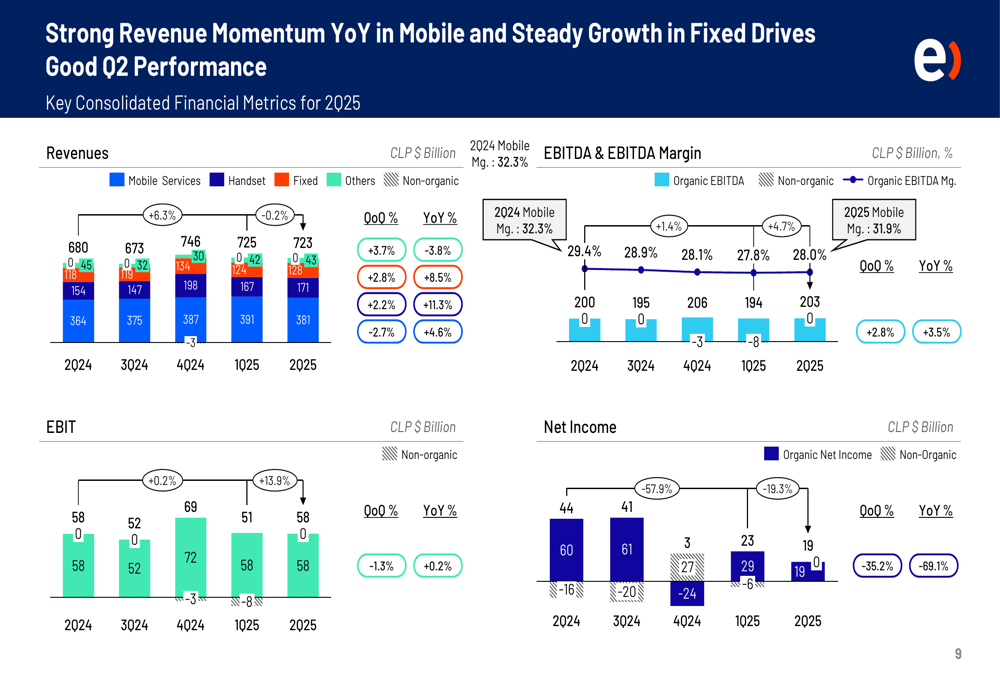

Entel reported consolidated revenues of 723 billion CLP for Q2 2025, representing a 3.7% increase quarter-over-quarter but a 3.8% decrease year-over-year. The company’s organic EBITDA reached 202.6 billion CLP, growing 2.8% QoQ and 3.5% YoY, with a margin of 28.0%. However, net income declined significantly to 19 billion CLP, down 35.2% QoQ and 69.1% YoY.

The following chart illustrates Entel’s revenue momentum and Q2 performance across key financial metrics:

Despite the mixed financial results, Entel’s operational metrics showed strength, particularly in high-value customer segments. The company’s postpaid mobile subscriber base grew by 1.6% QoQ and 8.4% YoY to 13.28 million, while prepaid subscribers declined by 7.0% QoQ and 9.1% YoY to 7.07 million. This shift toward postpaid customers aligns with the company’s strategic focus on higher-value segments.

Entel’s EBITDA performance was supported by positive business contributions of 11.3 billion CLP for the quarter, though these gains were partially offset by inflation effects (-2.2 billion CLP), lease adjustments (-3.6 billion CLP), and other factors including energy costs (-2.7 billion CLP). The company maintained positive free cash flow from operations at 59.2 billion CLP for the first half of 2025.

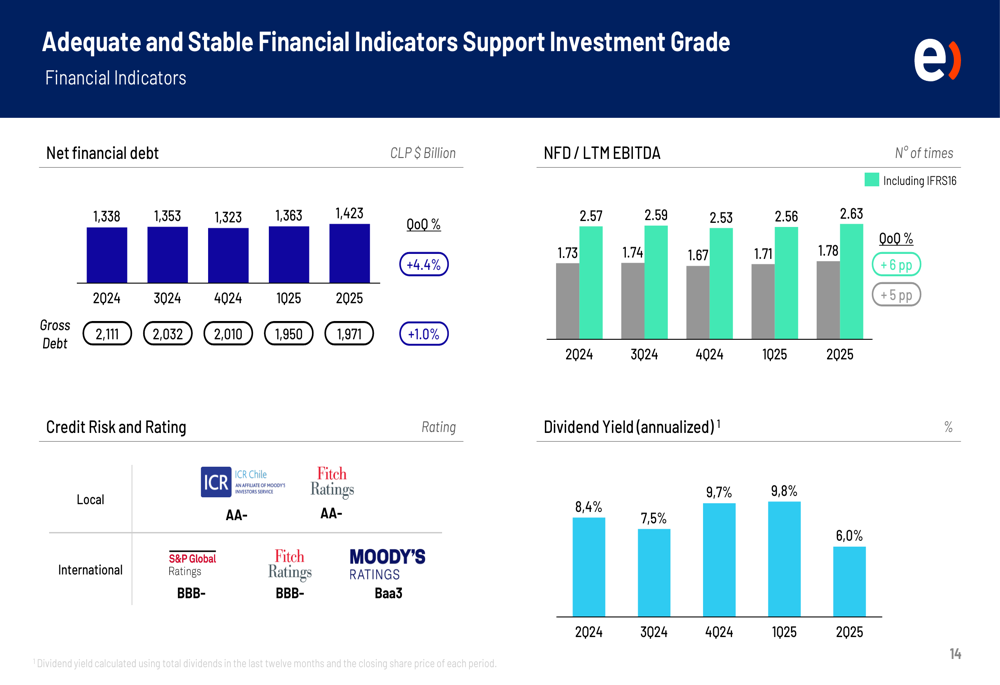

The following chart shows Entel’s financial indicators, highlighting the company’s stable debt position and attractive dividend yield:

Strategic Initiatives and Investments

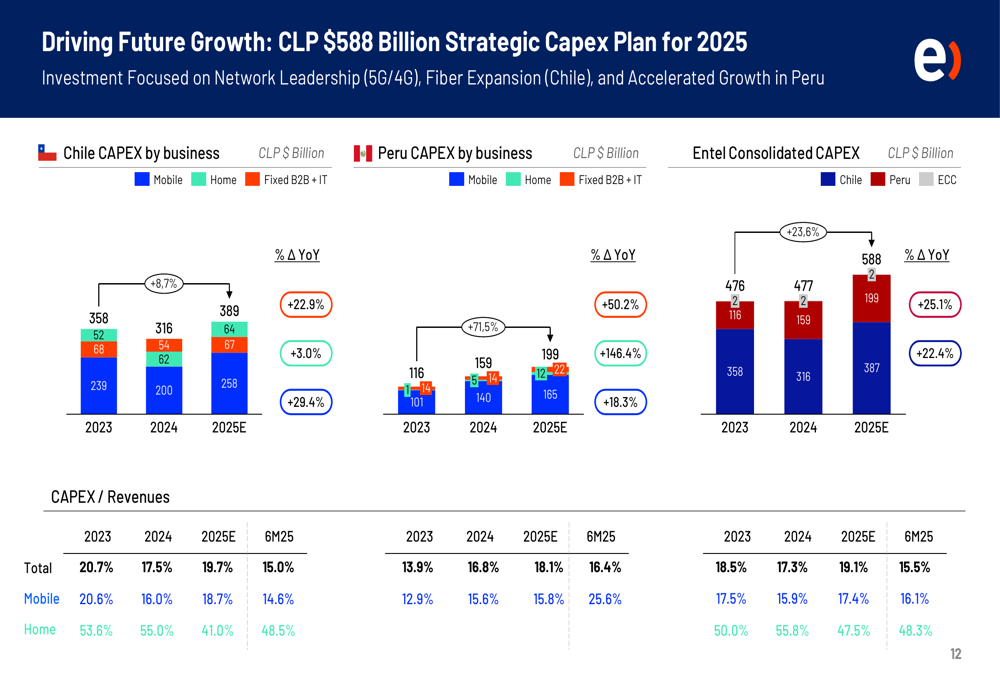

Entel continues to invest heavily in its network infrastructure and digital capabilities. The company has allocated 588 billion CLP for capital expenditures in 2025, representing a 25.1% increase year-over-year. These investments are strategically focused on mobile networks, home connectivity, and B2B solutions across both Chile and Peru.

As illustrated in the following strategic Capex plan breakdown, Entel is prioritizing investments in mobile infrastructure in Chile and B2B/IT solutions in Peru:

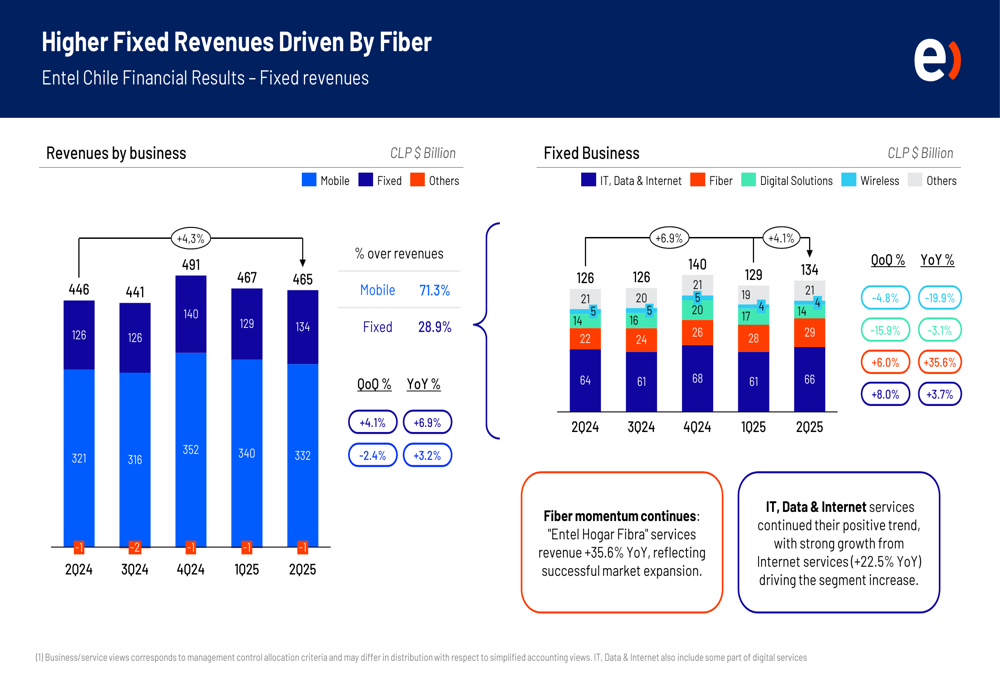

A key strategic initiative is Entel’s expansion of fiber-to-the-home (FTTH) services. The company has achieved a 45.5% market share in FTTH connections in Chile and continues to lead internet growth in a slow-growing, concentrated industry. This focus on fiber is driving higher fixed revenues, as shown in the following chart:

In Peru, Entel has launched a digital B2B solutions business that is expected to represent 10% of Entel Peru’s revenue by 2028. The company also completed Peru’s first "Direct to Cell" test with Starlink, positioning itself as the only Latin American telecommunications provider prepared to offer satellite messaging services in areas without terrestrial coverage.

Competitive Industry Position

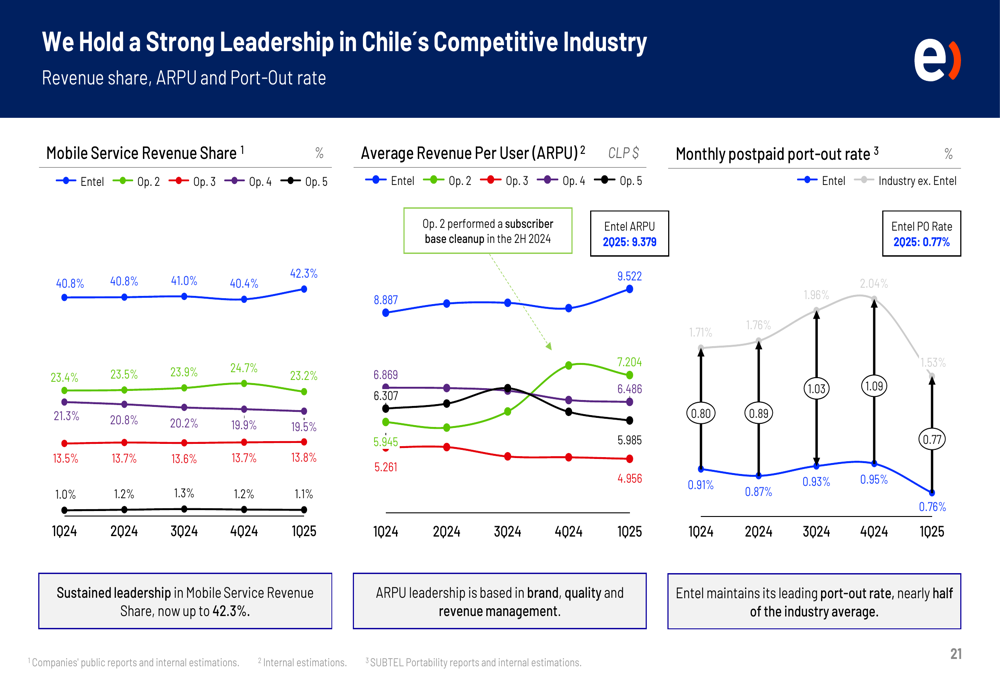

Entel maintains strong competitive positions in both Chile and Peru. In Chile, the company holds a 42.3% mobile service revenue share and leads the market in customer satisfaction with the lowest monthly postpaid port-out rate (0.77%) among competitors.

The following chart illustrates Entel’s leadership position in Chile’s competitive telecommunications industry:

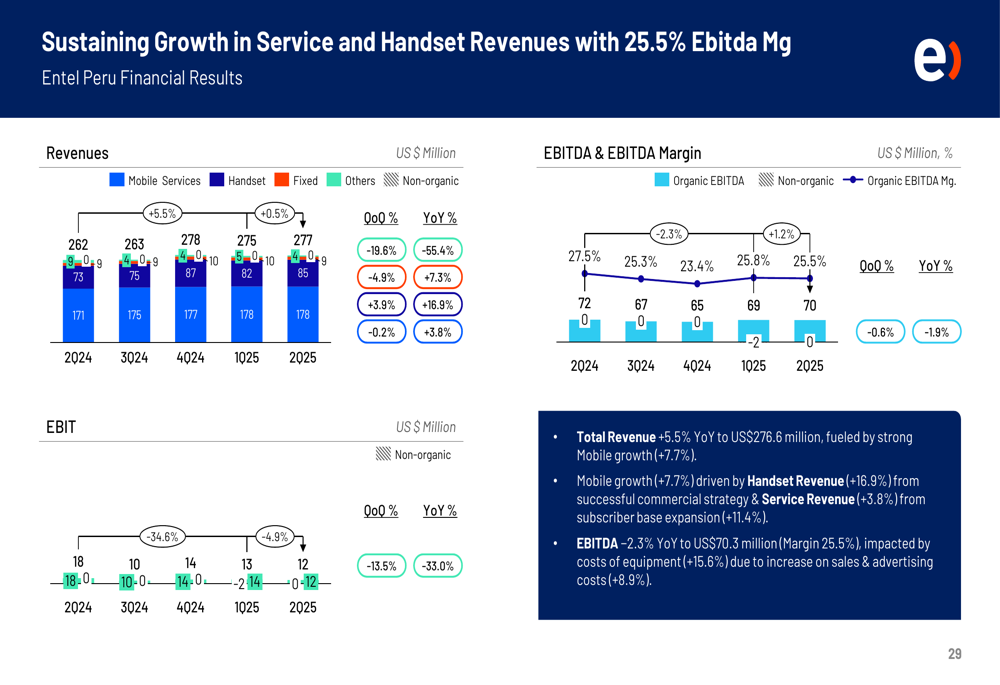

In Peru, Entel has achieved a 39.5% mobile service revenue share and maintains the second-highest position in brand power and customer satisfaction metrics. The company’s network quality leadership has helped drive continuous growth in postpaid subscribers despite intense competition.

As shown in the following chart, Entel Peru has sustained growth in both service and handset revenues:

Forward-Looking Statements

Looking ahead, Entel plans to continue expanding its fiber network and digital B2B solutions, particularly in Peru. The company expects to maintain stable EBITDA margins while carefully managing capital expenditures to support its strategic growth initiatives.

Entel’s management emphasized their focus on high-value customers and network quality during the earnings call. CFO Marcelo Bermudez stated, "Our strategy is to focus on high-value customers with the best network," and highlighted the company’s ability to navigate challenging market conditions: "We have been able to swim in these waters that are really turmoil pretty successfully."

The company will host its Investor Day on October 23, 2025, in Santiago, Chile, where it is expected to provide more details on its long-term strategic vision and growth targets.

In conclusion, while Entel faces challenges in terms of net income performance, its strong operational metrics, strategic investments in growth areas like fiber and 5G, and solid market positions in Chile and Peru position the company to maintain its competitive edge in the telecommunications sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.