Sun Valley Gold sells Vista Gold (VGZ) shares worth $2.16 million

Introduction & Market Context

Enterprise Products Partners LP (NYSE:EPD) released its third quarter 2025 earnings support slides on October 30, showcasing the company’s financial performance and strategic direction. The midstream energy giant reported mixed results, with revenue exceeding expectations at $12.02 billion despite an earnings per share (EPS) miss of $0.61 against a forecasted $0.67.

Following the announcement, EPD’s stock experienced a slight pre-market decline of 0.39%, trading at $31 per unit, within its 52-week range of $27.77 to $34.63. The company continues to position itself as a resilient player in the midstream energy sector, emphasizing its consistent distribution growth and strategic capital allocation.

Quarterly Performance Highlights

Enterprise Products Partners reported a Gross Operating Margin (GOM) of $2.385 billion for Q3 2025, representing a modest decrease from $2.454 billion in Q3 2024. Despite this decline, the company maintained its commitment to unitholder returns, declaring a quarterly distribution of $0.545 per unit, a 3.8% increase compared to Q3 2024.

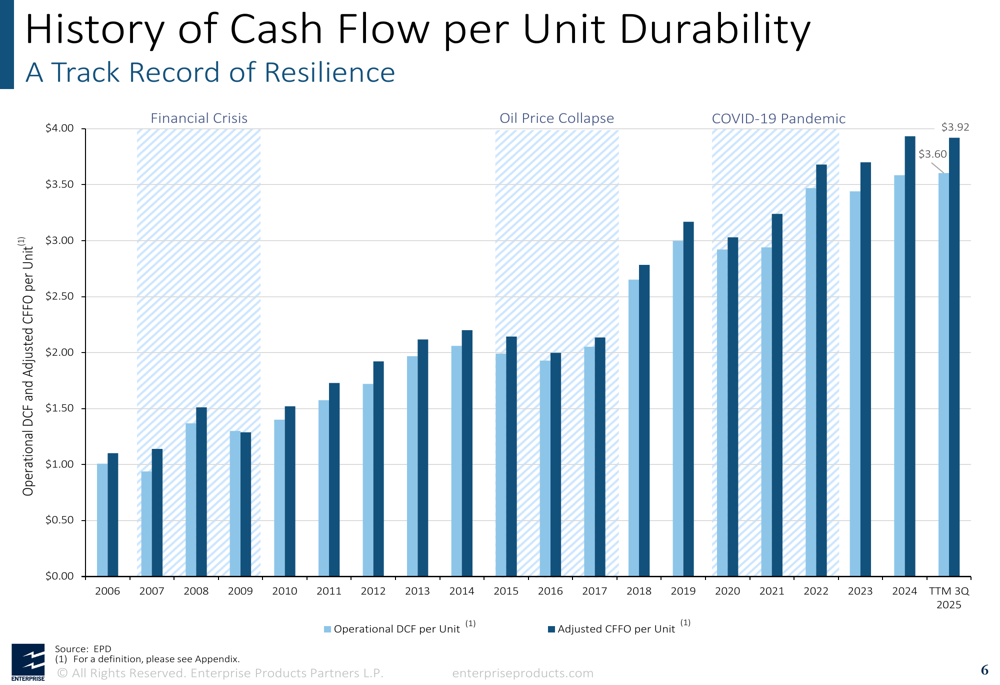

The company’s presentation highlighted its long-term cash flow durability through various economic cycles, including the Financial Crisis, Oil Price Collapse, and COVID-19 Pandemic. For 2024, Enterprise reported Operational Distributable Cash Flow (DCF) per unit of $3.60 and Adjusted Cash Flow from Operations (CFFO) per unit of $3.92.

As shown in the following chart of historical cash flow performance:

The company maintained a balanced approach to capital allocation, returning $5.0 billion to unitholders while investing $4.3 billion in growth capital expenditures for the trailing twelve months ended Q3 2025. This strategic balance is illustrated in the following chart:

Capital Allocation Strategy

Enterprise Products Partners emphasized its disciplined capital allocation strategy, focusing on three key areas: returning capital to investors, funding growth projects, and maintaining a strong balance sheet.

Since its IPO, EPD has returned $61 billion to equity investors through limited partner distributions and common unit buybacks. In Q3 2025 alone, the company repurchased 2.5 million common units for $80 million, with year-to-date buybacks totaling $250 million (8 million units). The company’s Distribution Reinvestment Plan (DRIP) and Employee Unit Purchase Plan (EUPP) purchased a combined 1.2 million units in Q3 2025.

The company’s capital allocation priorities are detailed in the following slide:

Enterprise maintains an A-rated balance sheet with a leverage ratio of 3.3x as of September 30, 2025, and available liquidity of $3.6 billion. The company’s debt portfolio features a 17-year average maturity, with 96% fixed-rate debt at a weighted average interest rate of 4.7%.

Segment Performance Analysis

Enterprise Products Partners’ presentation provided a detailed breakdown of performance across its four main business segments, all of which showed slight year-over-year declines in Q3 2025:

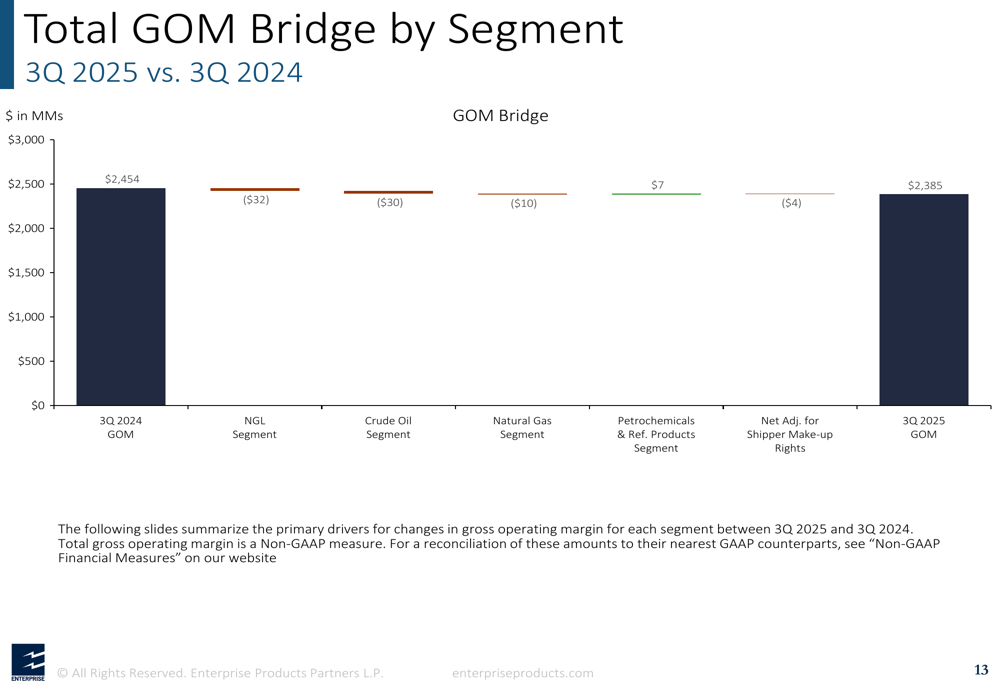

1. NGL Segment: GOM decreased from $1,335 million in Q3 2024 to $1,303 million in Q3 2025, with the Mont Belvieu Area NGL Fractionation Complex accounting for a $37 million decrease.

2. Crude Oil Segment: GOM fell from $401 million to $371 million year-over-year.

3. Natural Gas Segment: GOM declined from $349 million to $339 million.

4. Petrochemical & Refined Products Segment: This was the only segment showing growth, with GOM increasing from $363 million to $370 million.

The following bridge chart illustrates the changes in total GOM across segments:

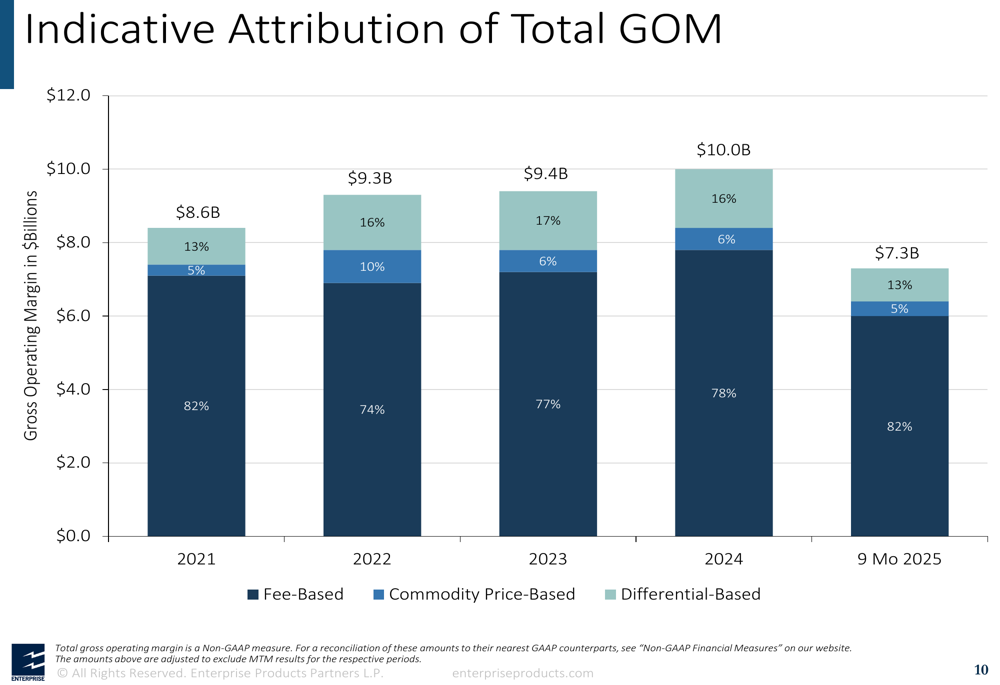

Despite these quarterly fluctuations, Enterprise highlighted the stability of its revenue composition, with fee-based activities consistently accounting for 82% of total GOM, while commodity price-based and differential-based activities represented 5% and 13%, respectively.

This revenue stability is visualized in the following chart:

Growth Projects and Outlook

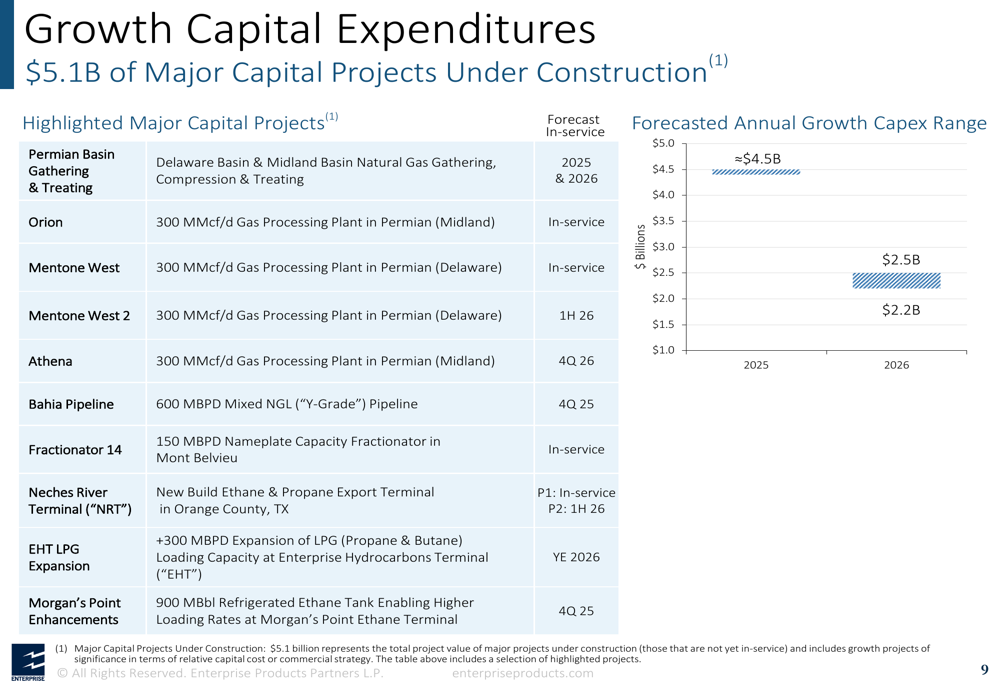

Enterprise Products Partners outlined an ambitious growth strategy with approximately $5.1 billion in major capital projects currently under construction. These projects span the Permian Basin, including gathering and treating infrastructure, multiple gas processing plants, pipeline expansions, and terminal enhancements.

The company forecasts growth capital expenditures of approximately $4.5 billion in 2025, normalizing to between $2.2 billion and $2.5 billion in 2026 as projects reach completion. This investment strategy is expected to drive continued volume growth across the company’s integrated value chain.

The following slide details Enterprise’s major capital projects under construction:

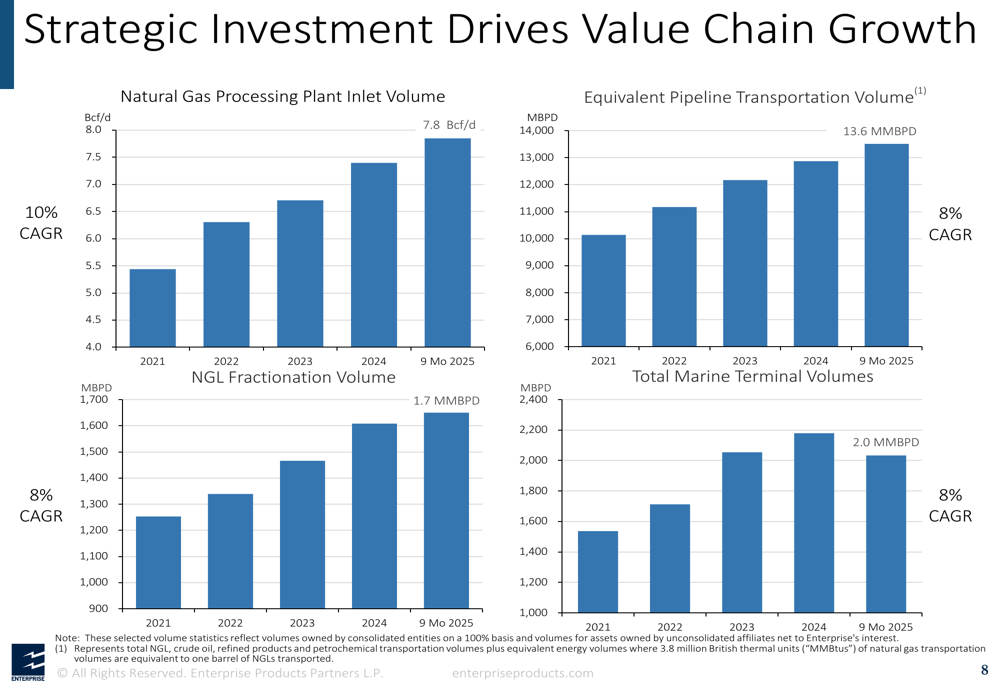

These strategic investments have already driven significant operational growth, as illustrated by increases in natural gas processing, pipeline transportation, NGL fractionation, and marine terminal volumes:

During the earnings call, Co-CEO Jim Teague emphasized the company’s strategic approach to market dynamics, stating, "Price creates supply, and price creates demand." Meanwhile, Co-CEO Randy Fowler highlighted the importance of the PDP wedge, calling it "the most underappreciated thing in the industry."

While Enterprise Products Partners continues to navigate short-term challenges, as evidenced by the Q3 2025 EPS miss, the company’s presentation emphasized its long-term strategic positioning, operational resilience, and commitment to sustainable distribution growth, which now stands at 27 consecutive years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.