Gold is 2025’s best performer. UBS sees more upside

Introduction & Market Context

EOG Resources, Inc. (NYSE:EOG) presented its first quarter 2025 earnings results on May 2, 2025, highlighting the company’s continued focus on capital discipline and operational efficiency. The oil and gas producer delivered solid financial results while optimizing its capital program to enhance free cash flow generation and shareholder returns.

The company’s presentation comes amid a challenging commodity price environment, with EOG’s stock trading at $111.68 as of May 1, 2025, showing a 1.22% increase. In premarket trading on May 2, the stock rose an additional 0.44% to $112.17, suggesting a positive initial reaction to the quarterly results.

Quarterly Performance Highlights

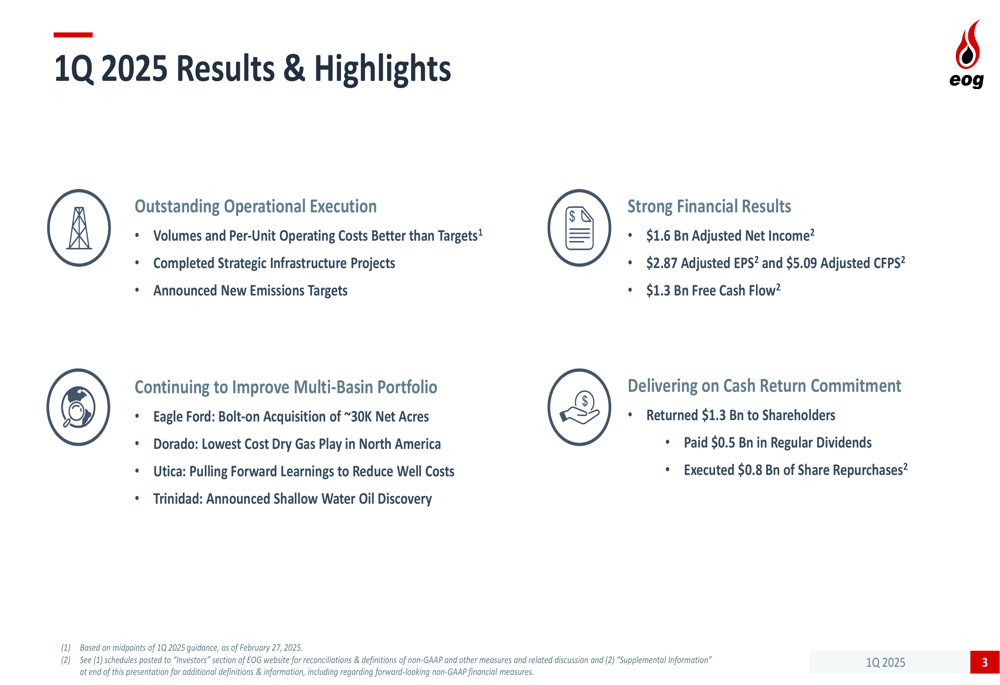

EOG reported strong financial results for Q1 2025, with $1.6 billion in adjusted net income, translating to $2.87 adjusted earnings per share and $5.09 adjusted cash flow per share. The company generated $1.3 billion in free cash flow during the quarter, maintaining its position as one of the industry’s leading cash flow generators.

As shown in the following comprehensive overview of the quarter’s achievements:

Operational execution was a standout in the quarter, with production volumes and per-unit operating costs both exceeding targets. The company also completed strategic infrastructure projects and announced new emissions targets, reinforcing its commitment to sustainable operations.

Strategic Capital Allocation

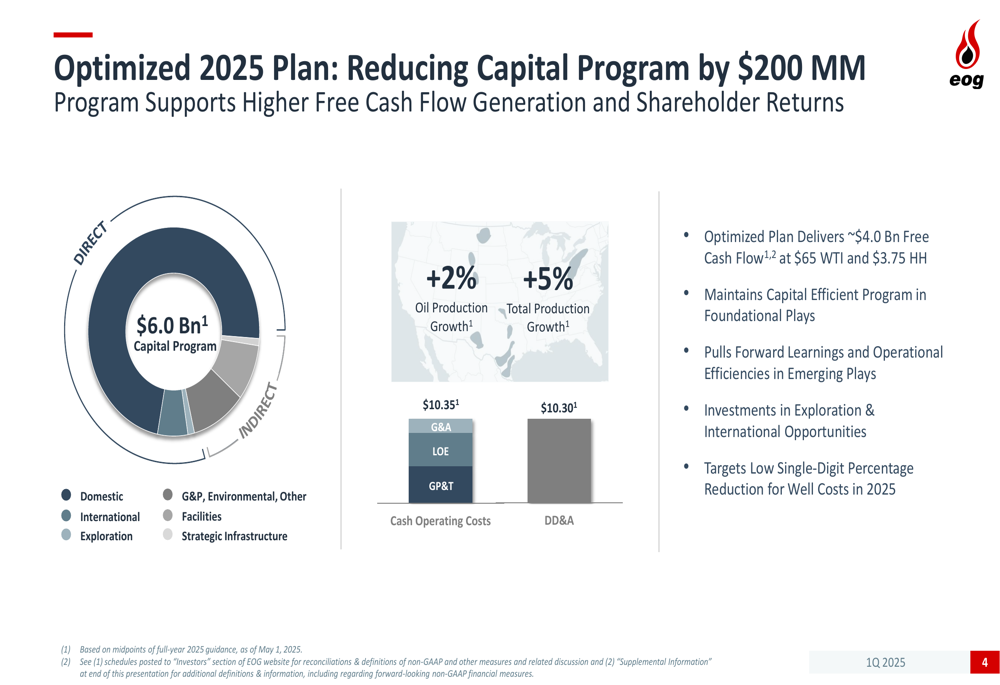

A key highlight of EOG’s presentation was its optimized 2025 capital plan, which reduces spending while maintaining production growth. The company lowered its capital program by $200 million to $6.0 billion, which is expected to deliver approximately $4.0 billion in free cash flow at $65 WTI oil and $3.75 Henry Hub natural gas prices.

The revised capital program supports oil production growth of 2% and total production growth of 5% for 2025, while targeting a low single-digit percentage reduction in well costs:

EOG’s disciplined approach to capital allocation has consistently delivered peer-leading returns on capital employed (ROCE), although this metric has declined from its peak in 2022, following industry trends. The company emphasized that its portfolio delivers a 10% ROCE at less than $45 WTI, demonstrating resilience in lower price environments.

Multi-Basin Portfolio Development

EOG continues to enhance its multi-basin portfolio with high-return opportunities. The company highlighted its Eagle Ford bolt-on acquisition of approximately 30,000 net acres, expanding its core position in this prolific basin to 565,000 net acres.

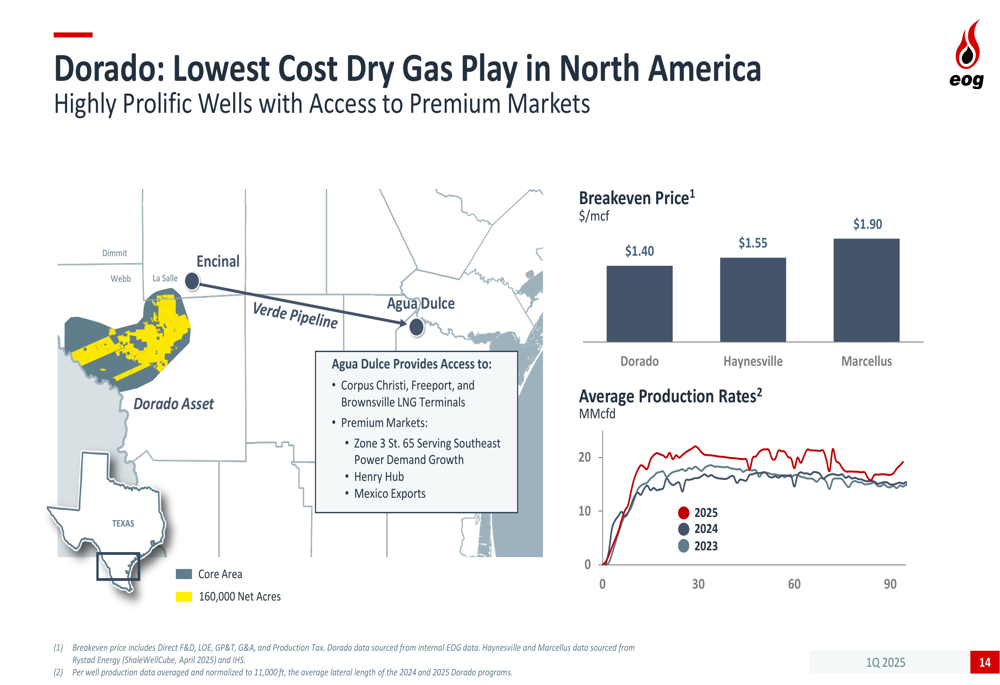

The company’s Dorado play stands out as the lowest-cost dry gas play in North America, with a breakeven price of just $1.40/mcf, providing significant competitive advantage in the natural gas market:

EOG also announced a new oil discovery in Trinidad, the Beryl discovery in the TSP Deep Area, which identified over 125 feet of high-quality, oil-bearing net pay. This adds to the company’s international portfolio and provides additional growth opportunities outside the U.S.

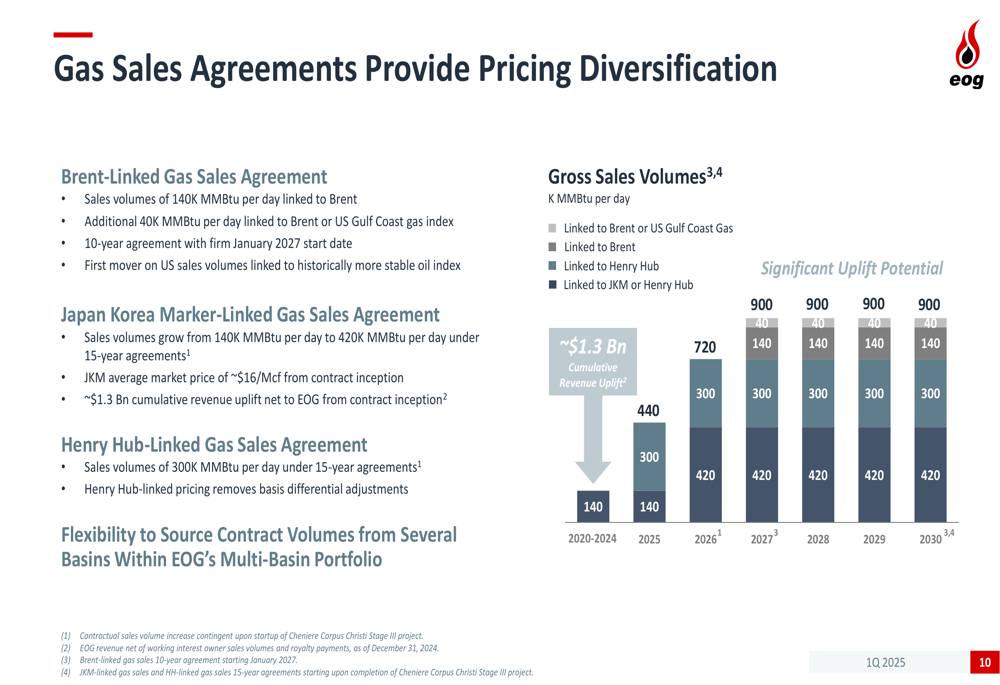

The company’s marketing strategy for natural gas has been particularly effective, with strategic sales agreements linked to global price markers providing significant revenue uplift:

These diversified pricing mechanisms have generated approximately $1.3 billion in cumulative revenue uplift, demonstrating EOG’s ability to capture premium pricing in global markets.

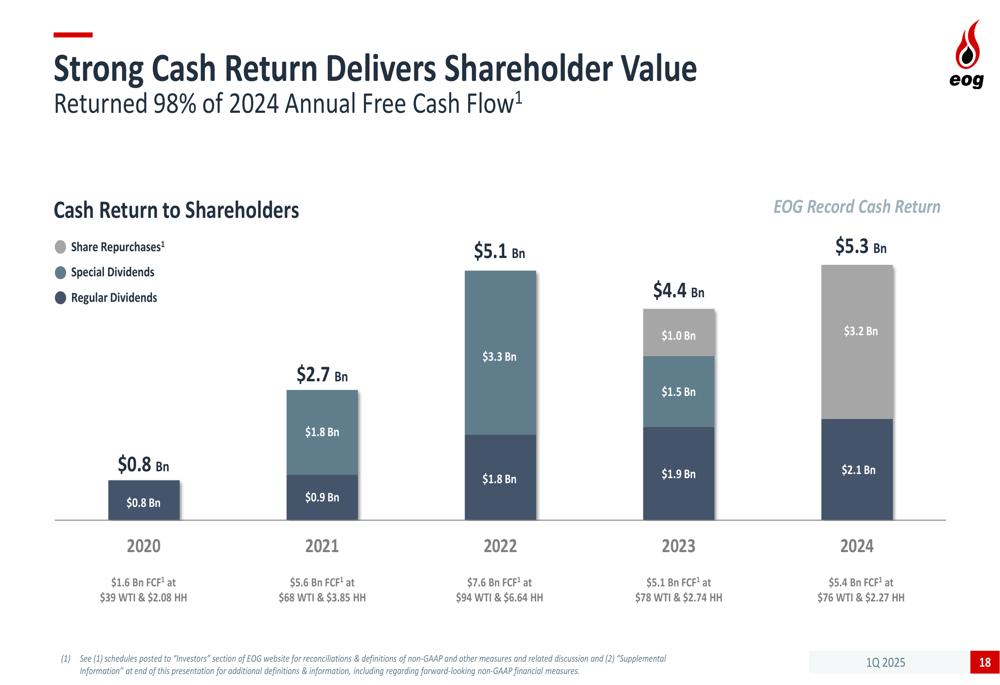

Cash Return Strategy

EOG remains committed to returning cash to shareholders, with $1.3 billion returned in Q1 2025 alone. This included $0.5 billion in regular dividends and $0.8 billion in share repurchases, fulfilling the company’s commitment to return a minimum of 70% of annual free cash flow to shareholders.

The company increased its regular dividend by 7% for 2025, marking 27 years of sustainable dividend growth. EOG’s dividend growth rate is twice the peer average, reinforcing its position as a leader in shareholder returns:

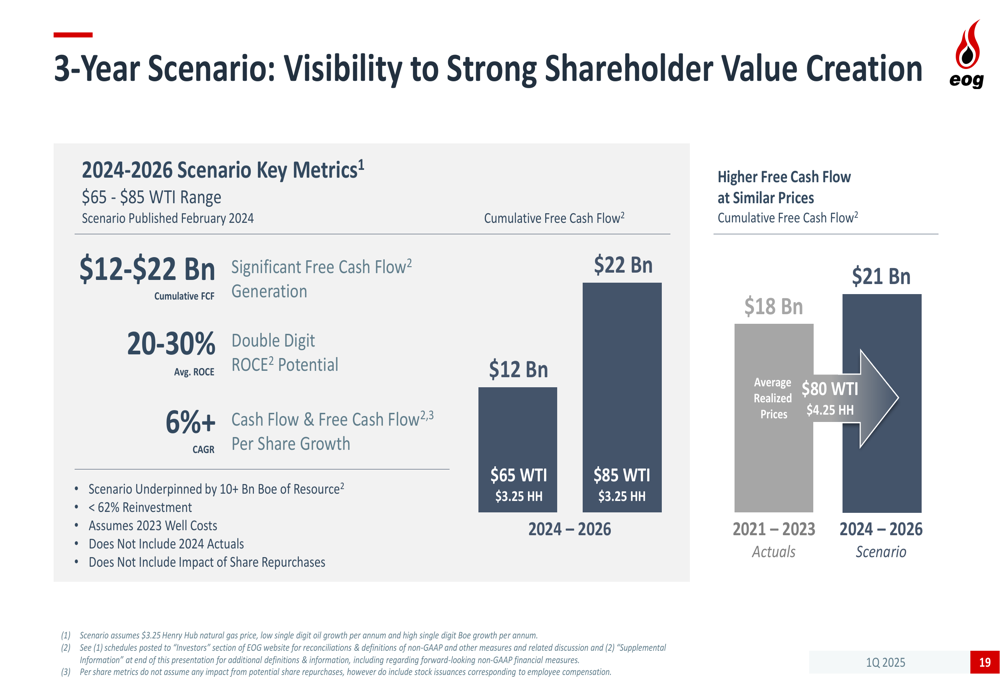

Looking ahead to the 2024-2026 period, EOG projects significant free cash flow generation of $12-22 billion (at $80 WTI and $4.25 Henry Hub), with double-digit return on capital employed and over 6% growth in cash flow and free cash flow per share:

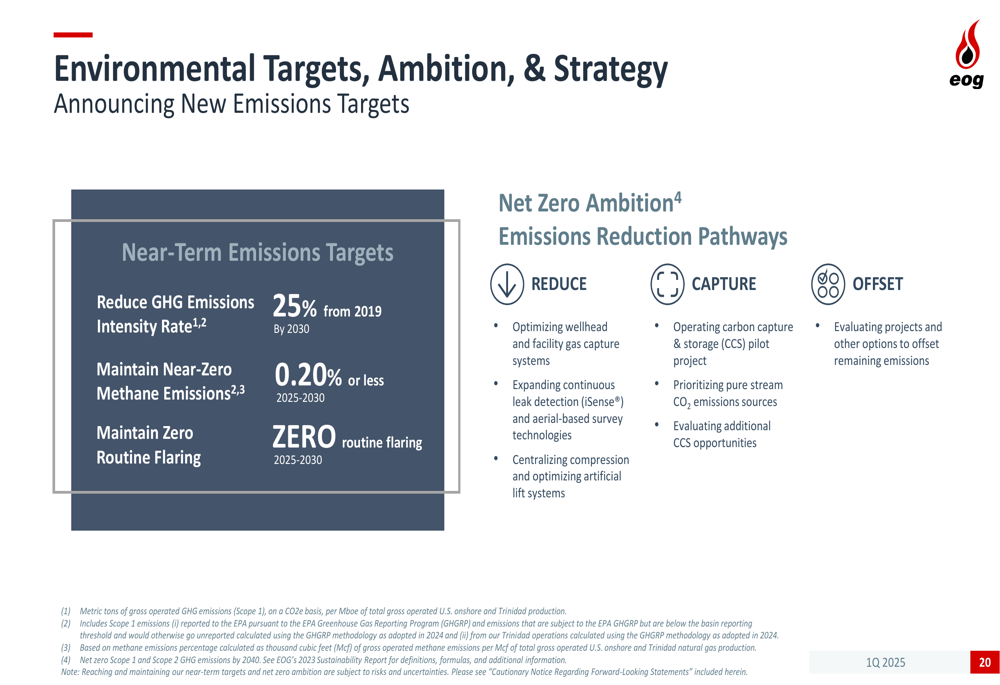

Environmental Targets and Long-Term Outlook

EOG outlined ambitious environmental goals as part of its sustainability strategy. The company aims to reduce greenhouse gas emissions intensity by 25% from 2019 to 2030, maintain near-zero methane emissions of 0.20% or less, and achieve zero routine flaring from 2025 to 2030:

These environmental initiatives are integrated into EOG’s broader strategy for sustainable value creation through industry cycles, which focuses on capital discipline, operational excellence, sustainability, and corporate culture.

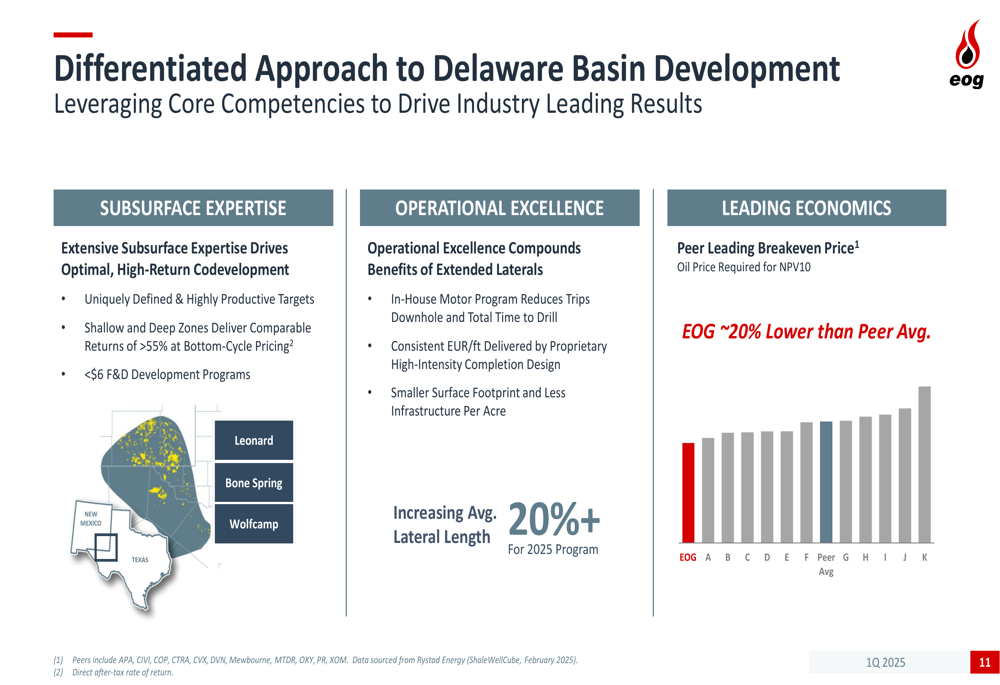

The company’s approach to the Delaware Basin development exemplifies its operational excellence, with extensive subsurface expertise driving optimal, high-return codevelopment and in-house technology reducing drilling time and costs:

EOG’s differentiated approach has resulted in peer-leading breakeven prices approximately 20% lower than the peer average in the Delaware Basin, reinforcing the company’s position as one of the lowest-cost producers in the industry.

As EOG navigates through 2025 and beyond, its focus on capital efficiency, operational excellence, and shareholder returns positions the company to create sustainable value across commodity price cycles while advancing its environmental objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.