US stock futures muted with Jackson Hole, retail earnings on tap

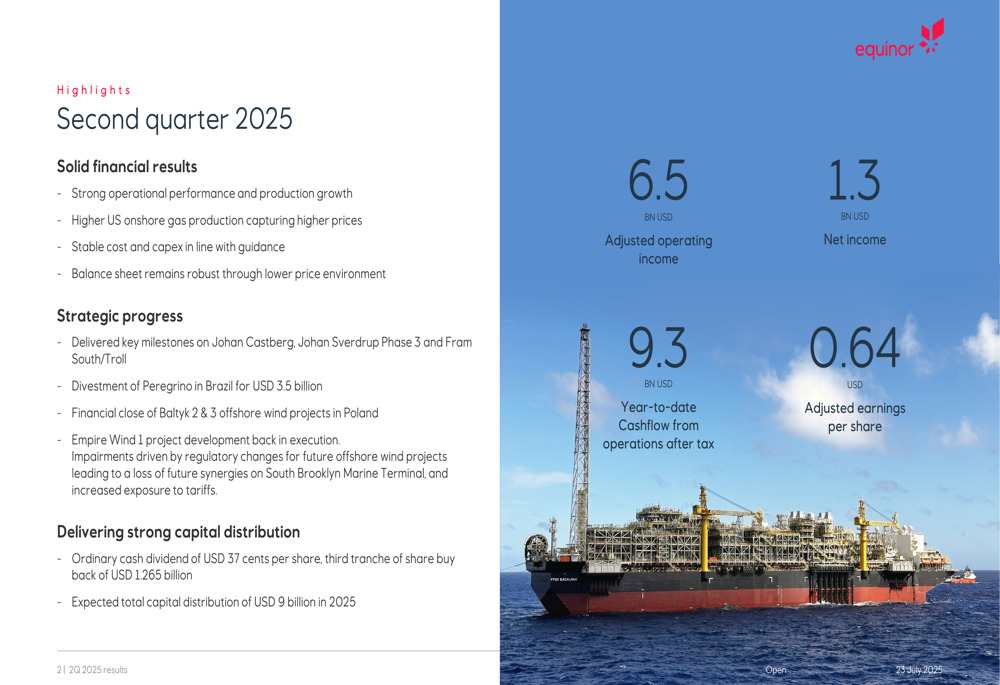

Equinor ASA (NYSE:EQNR) presented its second quarter 2025 results on July 23, highlighting solid financial performance despite a challenging oil price environment. The Norwegian energy giant reported adjusted operating income of $6.5 billion and announced continued strong capital distribution plans for shareholders.

Quarterly Performance Highlights

Equinor delivered adjusted operating income of $6.5 billion in Q2 2025, down from $7.5 billion in the same period last year. Net income stood at $1.3 billion, with adjusted earnings per share reaching $0.64. Year-to-date cash flow from operations after tax amounted to $9.3 billion.

"We’ve maintained solid financial results through strong operational performance and production growth, while navigating a lower price environment for liquids," said Torgrim Reitan, Chief Financial Officer of Equinor, during the presentation.

The company reported over 2% growth in oil and gas production compared to Q2 2024, with particularly strong performance from international assets. Renewable power generation increased by 26% year-over-year, reflecting Equinor’s continued diversification efforts.

As shown in the following quarterly highlights slide:

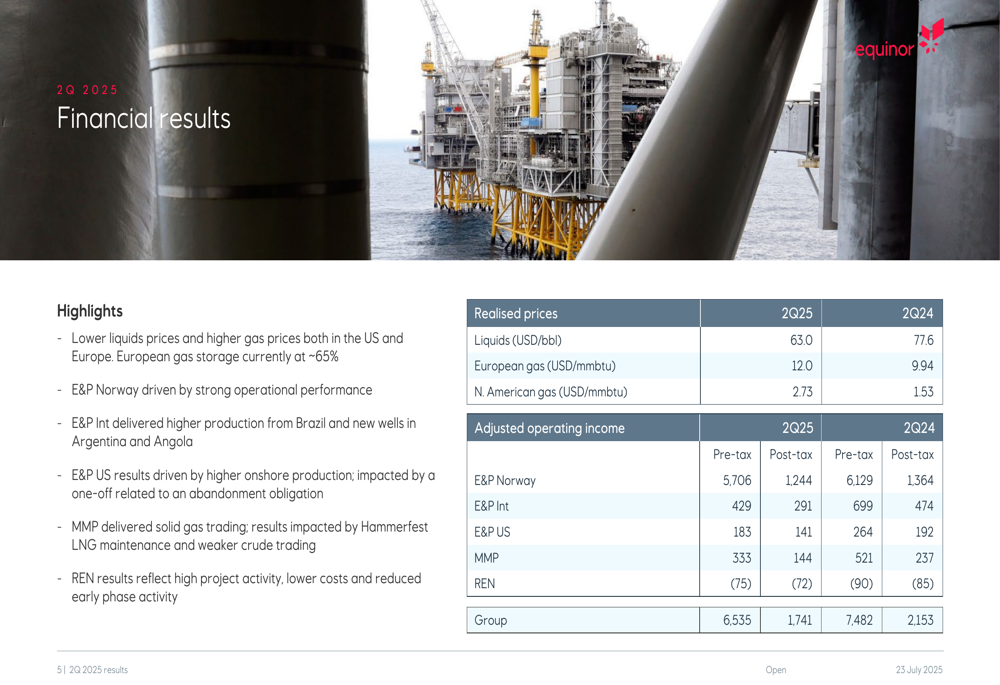

Detailed Financial Analysis

Equinor’s Q2 results reflect the impact of lower oil prices offset by higher gas prices in both Europe and North America. The company realized an average liquids price of $63.0 per barrel, down from $77.6 in Q2 2024. Meanwhile, European gas prices rose to $12.0 per MMBtu from $9.94, and North American gas prices increased to $2.73 per MMBtu from $1.53 in the same period last year.

The exploration and production segment in Norway delivered strong operational performance, while international E&P operations benefited from higher production in Brazil and new wells in Argentina and Angola. The U.S. segment saw higher onshore production but was impacted by a one-off related to an abandonment obligation.

The following slide details the company’s financial results across segments:

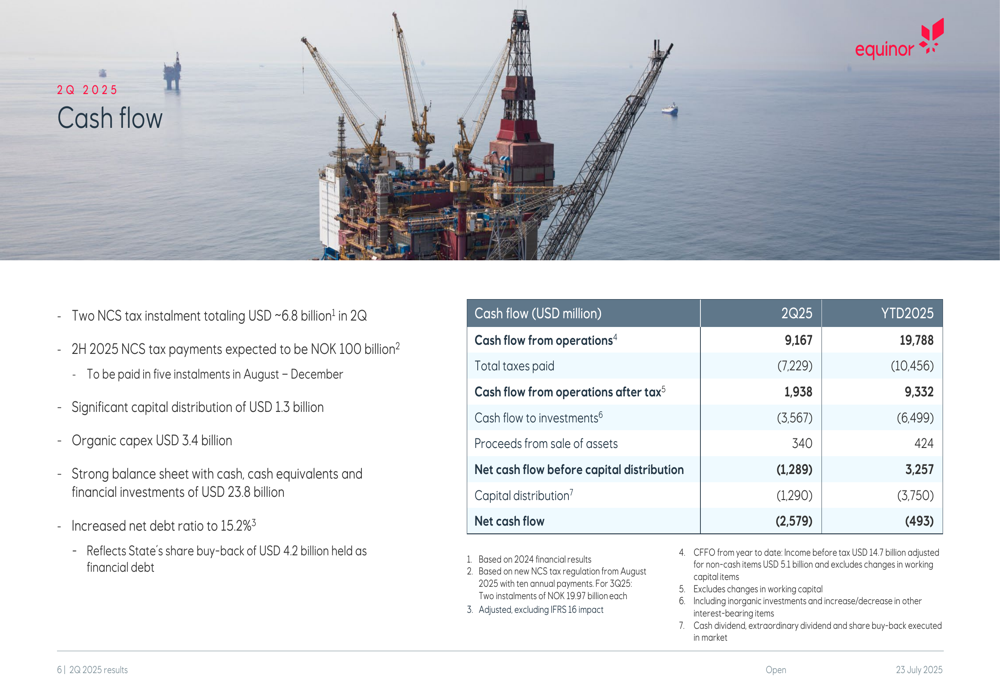

Equinor’s cash flow was significantly impacted by two Norwegian Continental Shelf tax installments totaling approximately $6.8 billion in the second quarter. The company expects second-half 2025 NCS tax payments to reach NOK 100 billion. Despite these substantial tax payments, Equinor maintained a strong balance sheet with cash, cash equivalents, and financial investments of $23.8 billion, though its net debt ratio increased to 15.2%.

The cash flow breakdown is illustrated in this slide:

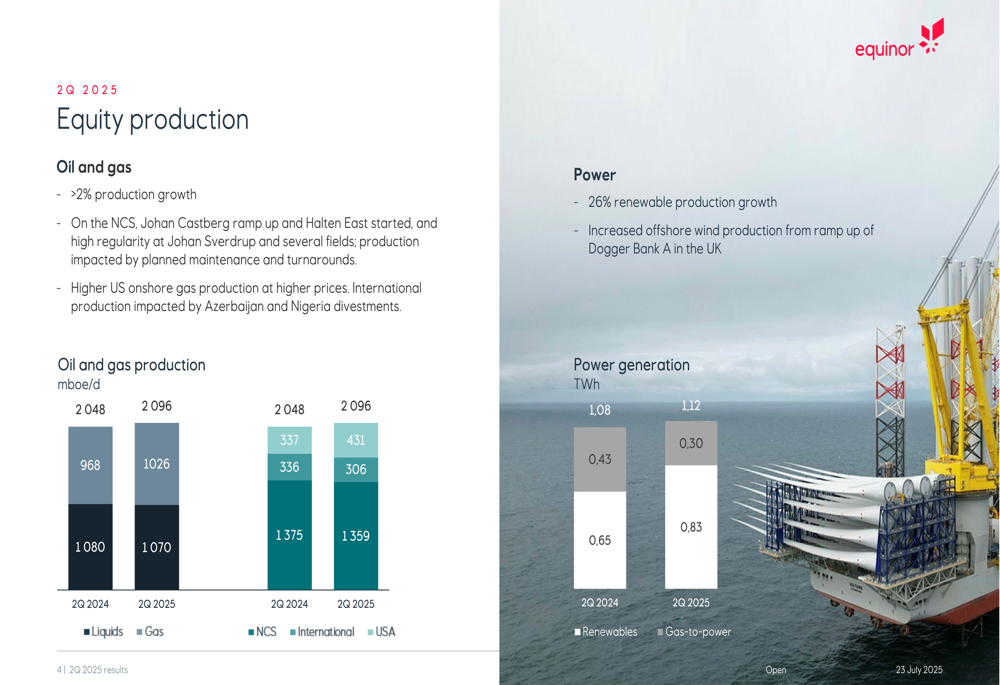

Production Performance

Equinor’s equity production showed notable growth in the second quarter of 2025. Liquids production increased to 1,026 mboe/d from 968 mboe/d in Q2 2024, while gas production slightly decreased to 1,070 mboe/d from 1,080 mboe/d. International production saw a significant jump to 431 mboe/d from 337 mboe/d, primarily driven by assets in Brazil and new wells in Argentina and Angola.

The company’s power generation also showed growth, with total production reaching 1.12 TWh compared to 1.08 TWh in Q2 2024. While renewable power generation decreased to 0.30 TWh from 0.43 TWh, gas-to-power generation increased to 0.83 TWh from 0.65 TWh.

The following slide provides a detailed breakdown of Equinor’s production figures:

Strategic Initiatives

Equinor reported significant strategic progress during the quarter, including the delivery of key milestones on major projects such as Johan Castberg, Johan Sverdrup Phase 3, and Fram South/Troll. The company also completed the divestment of its Peregrino assets in Brazil for $3.5 billion, strengthening its financial position.

In the renewable energy sector, Equinor achieved financial close of the Baltyk 2 & 3 offshore wind projects in Poland and returned the Empire Wind 1 project to execution phase. However, the company noted impairments driven by regulatory changes for future offshore wind projects, which led to a loss of future synergies on South Brooklyn Marine Terminal and increased exposure to tariffs.

"We continue to balance our portfolio, focusing on high-value assets while advancing our position in the energy transition," Reitan explained during the presentation.

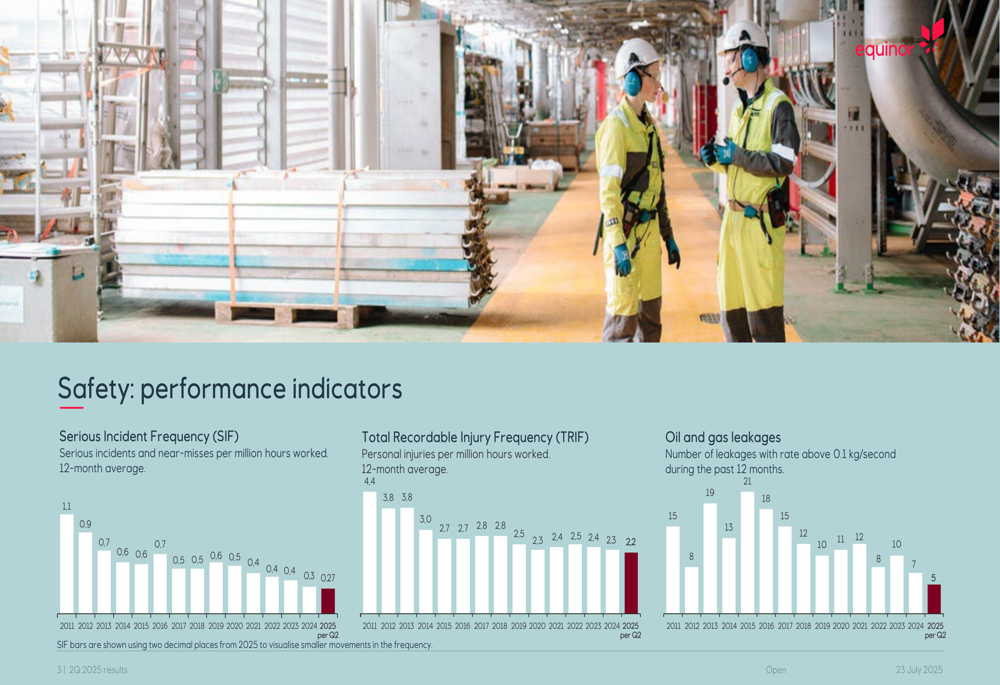

Safety Performance

Equinor maintained its focus on safety, reporting a Serious Incident Frequency (SIF) of 0.27 and a Total (EPA:TTEF) Recordable Injury Frequency (TRIF) of 2.2 for 2025. The company also reported 5 oil and gas leakages above 0.1 kg/second in 2025, showing improvement from historical figures.

The following slide illustrates Equinor’s safety performance indicators:

Forward-Looking Statements

Looking ahead, Equinor provided a positive outlook for the remainder of 2025, projecting organic capital expenditure of $13 billion and oil and gas production growth of 4 percent. The company expects total capital distribution to shareholders to reach $9 billion in 2025, including an ordinary cash dividend of $0.37 per share and the third tranche of a share buyback program amounting to $1.265 billion.

"Our robust operational performance and strategic progress position us well to deliver strong returns to shareholders while investing in future growth," said Reitan.

The company’s outlook is summarized in this slide:

Equinor’s stock closed at $25.58 on July 22, 2025, with a 0.08% increase on the day. In after-hours trading, the stock rose an additional 0.86% to $25.80, suggesting positive market reception to the company’s quarterly results and outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.