Broadcom named strategic vendor for Walmart virtualization solutions

ESCO Technologies Inc (NYSE:ESE) reported strong second-quarter fiscal 2025 results on May 7, showing double-digit growth in orders, EBIT, and earnings per share. Despite the positive performance, the company’s stock fell sharply in after-hours trading.

Executive Summary

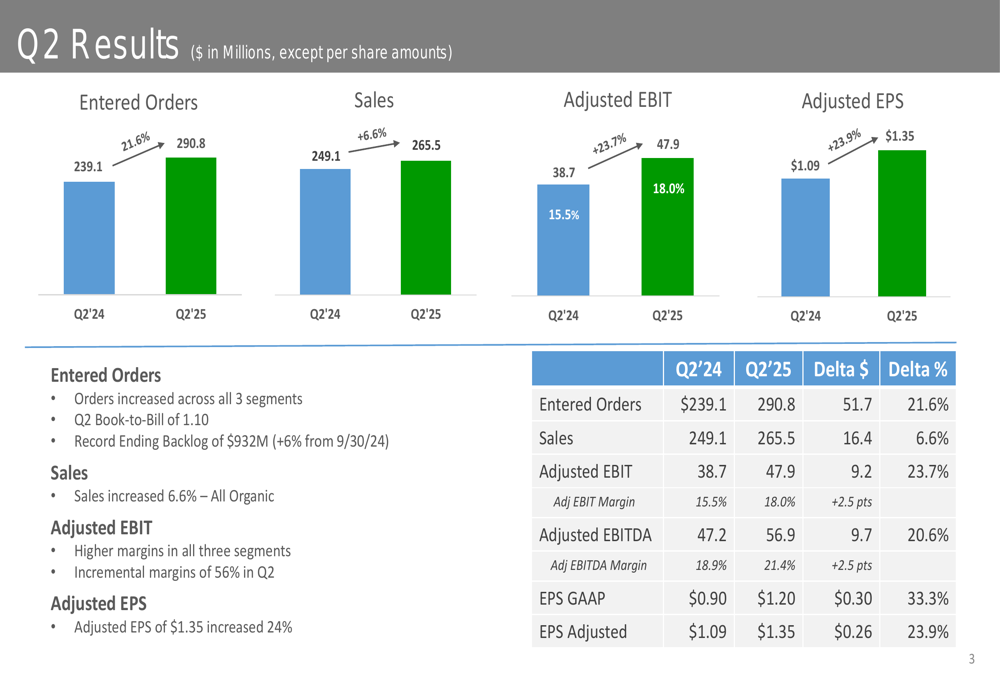

ESCO Technologies delivered impressive Q2 FY2025 results with entered orders increasing 21.6% to $290.8 million and sales rising 6.6% to $265.5 million compared to the same period last year. Adjusted EBIT grew 23.7% to $47.9 million, with margins expanding from 15.5% to 18.0%. Adjusted earnings per share increased 23.9% to $1.35.

The company’s book-to-bill ratio stood at 1.10 for the quarter, with total backlog reaching $932 million, up 6% from September 30, 2024. All three business segments – Aerospace & Defense, Utility Solutions Group, and Test – showed growth in orders, sales, and EBIT.

As shown in the following chart of quarterly financial performance:

Despite these strong results, ESCO’s stock dropped 14.39% in after-hours trading to $140, suggesting investors may have had higher expectations or concerns about future performance.

Quarterly Performance Highlights

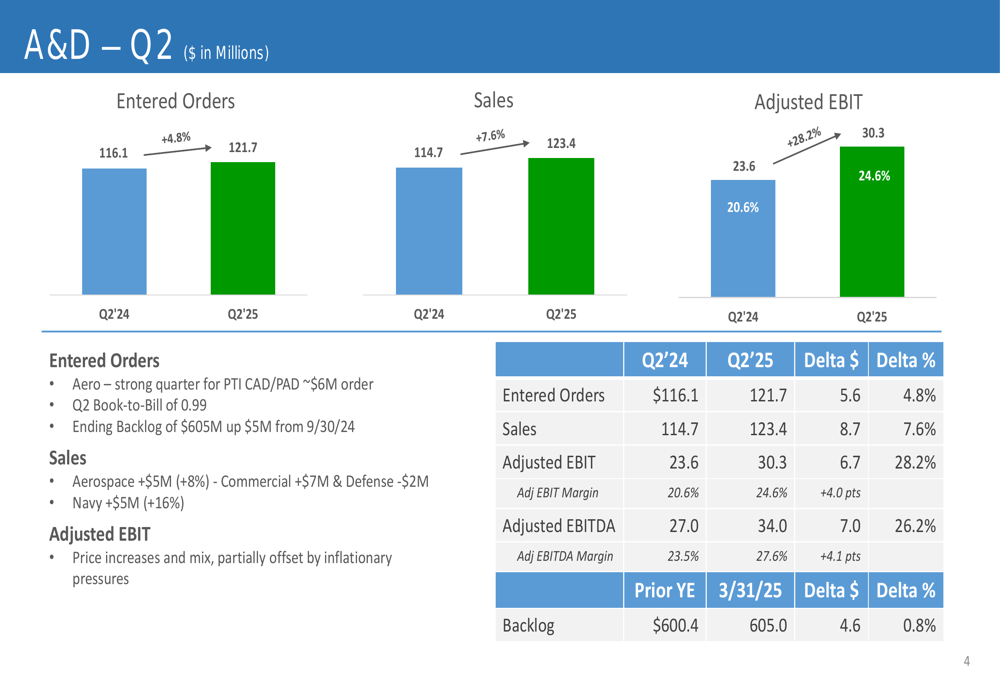

The Aerospace & Defense segment continued its strong performance with sales increasing 7.6% to $123.4 million and adjusted EBIT rising 28.2% to $30.3 million. The segment’s EBIT margin expanded significantly from 20.6% to 24.6%. Aerospace sales were up $5 million (8%), with commercial aerospace growing by $7 million, partially offset by a $2 million decline in defense. Navy-related sales increased by $5 million (16%).

The segment’s performance is illustrated in this breakdown:

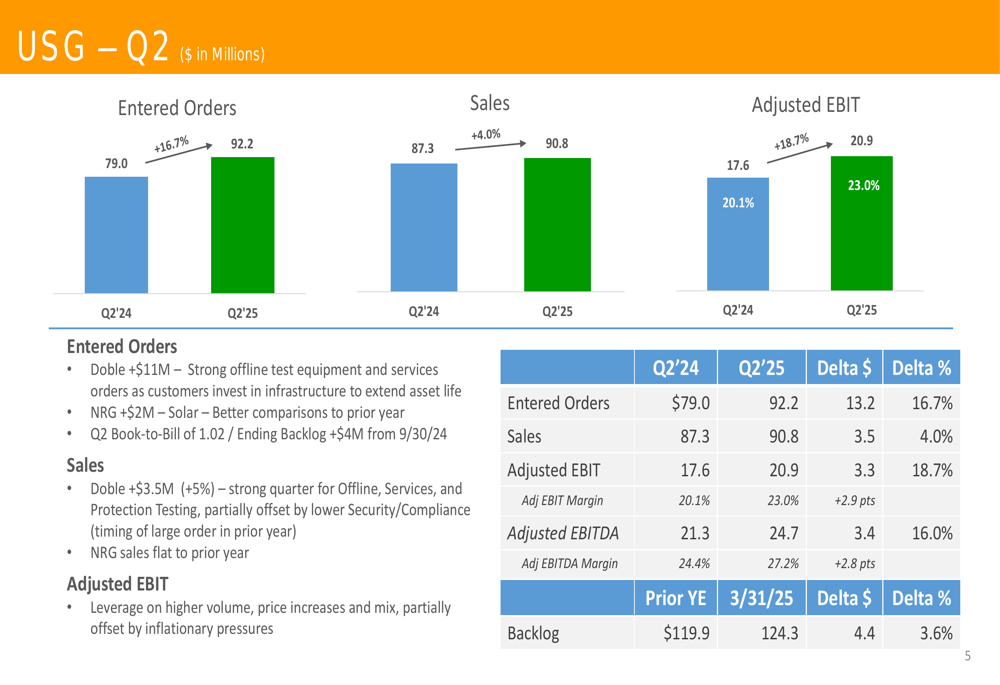

The Utility Solutions Group also delivered solid results with sales increasing 4.0% to $90.8 million and adjusted EBIT growing 18.7% to $20.9 million. EBIT margins improved from 20.1% to 23.0%. Doble sales increased by $3.5 million (5%), partially offset by lower security/compliance revenue, while NRG sales remained flat year-over-year.

The following chart details the USG segment performance:

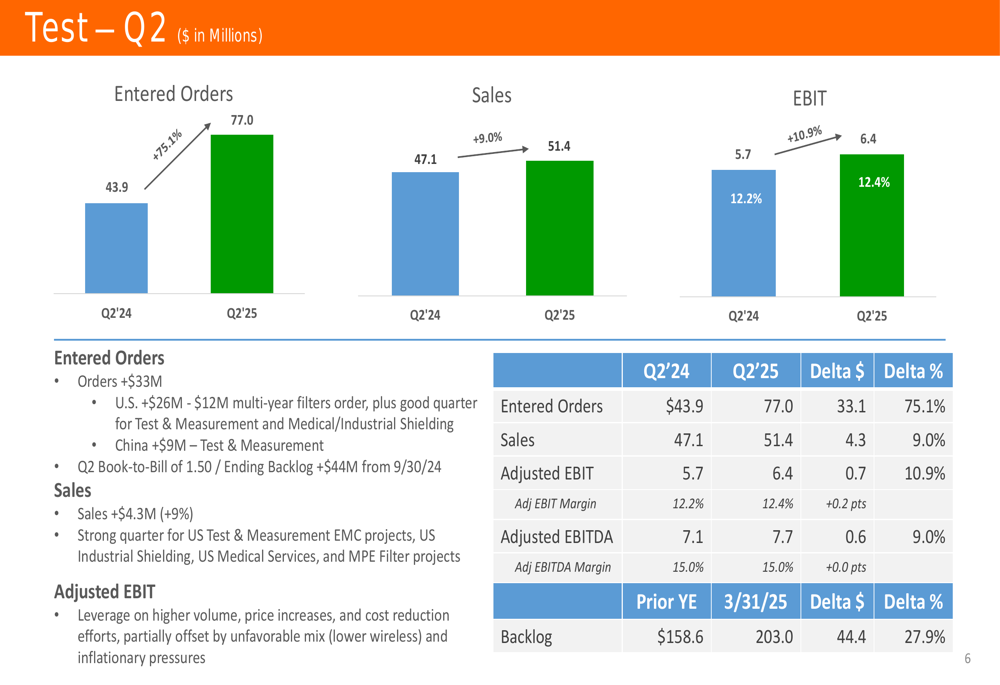

The Test segment showed the most dramatic improvement in order intake, with entered orders surging 75.1% to $77.0 million. Sales increased 9.0% to $51.4 million, and adjusted EBIT grew 10.9% to $6.4 million. EBIT margins slightly improved from 12.2% to 12.4%. The segment saw significant order growth in the U.S. (+$26 million) and China (+$9 million).

The Test segment’s quarterly performance is shown here:

Detailed Financial Analysis

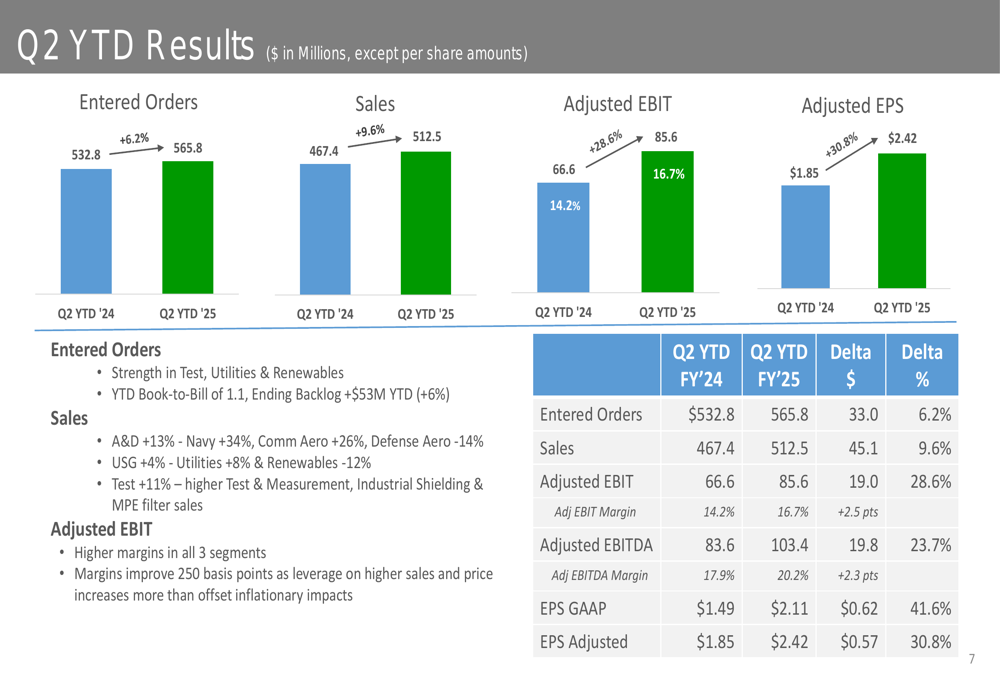

On a year-to-date basis through Q2, ESCO’s performance has been equally impressive. Entered orders increased 6.2% to $565.8 million, while sales grew 9.6% to $512.5 million. Adjusted EBIT rose 28.6% to $85.6 million, with margins expanding from 14.2% to 16.7%. Adjusted EPS increased 30.8% to $2.42.

The year-to-date performance across all metrics is illustrated in this comprehensive chart:

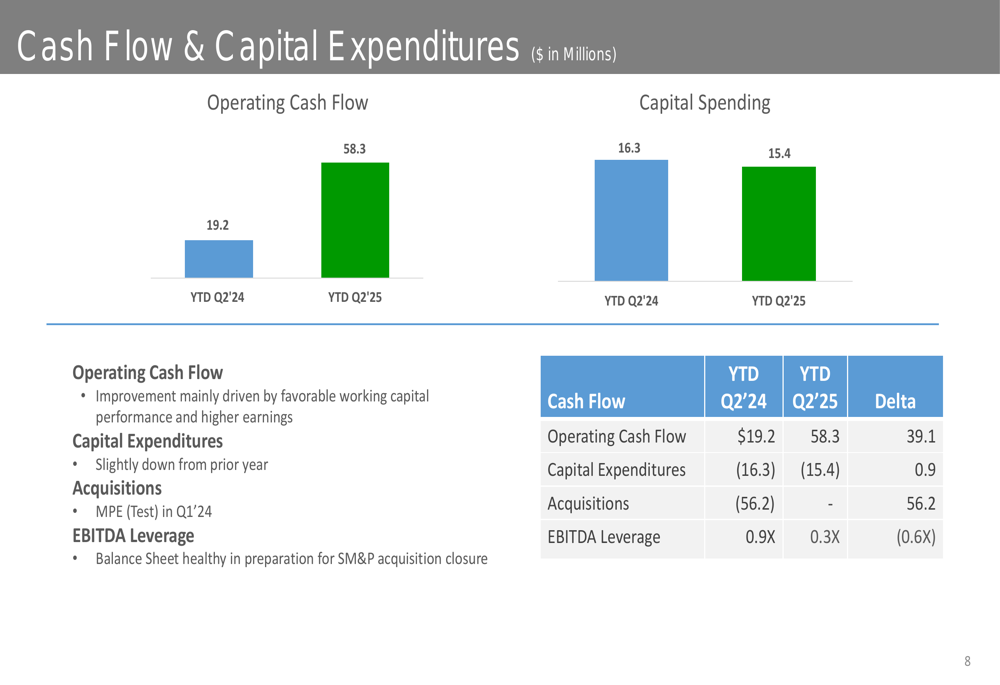

Cash flow generation showed significant improvement, with operating cash flow increasing from $19.2 million in the first half of fiscal 2024 to $58.3 million in the comparable period of fiscal 2025. Capital spending decreased slightly from $16.3 million to $15.4 million. The company reported $56.2 million in acquisition spending, while EBITDA leverage improved from 0.9x to 0.3x, indicating a stronger balance sheet.

The following chart details the cash flow and capital expenditure performance:

Forward-Looking Statements

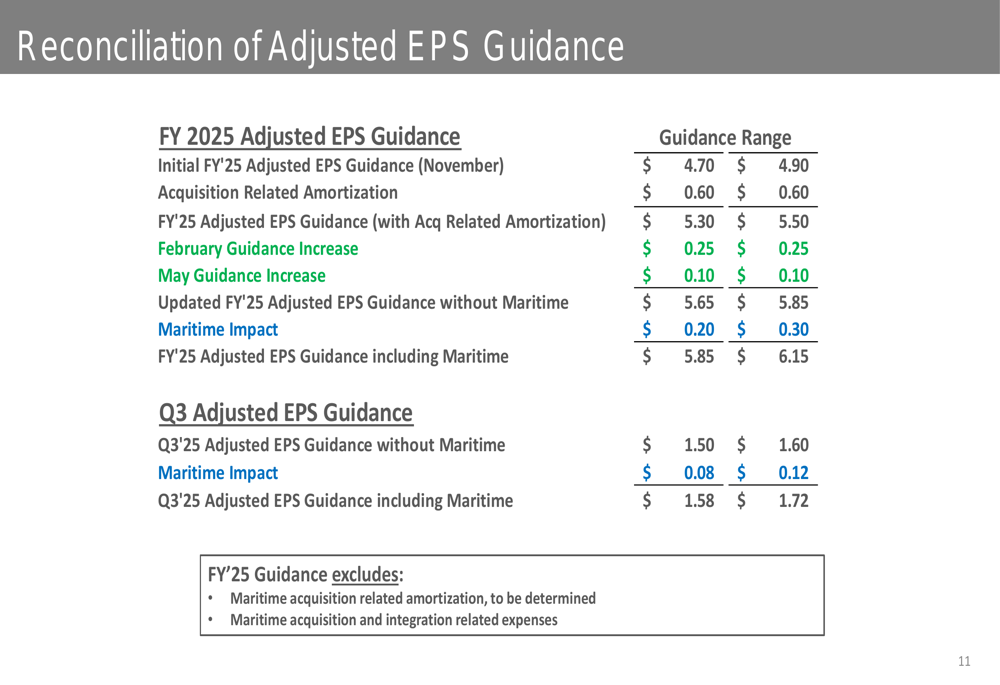

ESCO Technologies raised its full-year fiscal 2025 guidance, now expecting revenue (excluding Maritime) to increase by 6%-8% to a range of $1.09 billion to $1.11 billion. The Maritime business is expected to contribute an additional $90 million to $100 million in revenue.

Adjusted EPS guidance (excluding Maritime) was increased by $0.10 to a range of $5.65 to $5.85. Including the Maritime impact of $0.20 to $0.30, full-year adjusted EPS is expected to be between $5.85 and $6.15. For the third quarter, adjusted EPS is projected to be $1.50 to $1.60 excluding Maritime, or $1.58 to $1.72 including Maritime.

This represents a significant increase from the company’s initial guidance provided in November 2024, which projected adjusted EPS of $4.70 to $4.90. The guidance has been raised twice since then, with increases of $0.25 in February and $0.10 in May.

The detailed reconciliation of the company’s adjusted EPS guidance is presented here:

Market Reaction and Analysis

Despite the strong quarterly performance and raised guidance, ESCO Technologies’ stock fell 14.39% in after-hours trading to $140, a significant drop from its regular session close of $164.06. This negative reaction suggests investors may have had concerns not addressed in the presentation or had expected even stronger results or guidance.

The sharp decline is particularly surprising given that the company has now raised its earnings guidance twice this fiscal year and is showing strong performance across all business segments. The stock had been trading near its 52-week high of $171.28 before the earnings release, indicating high investor expectations.

In the previous earnings call for Q4 2024, ESCO reported surpassing $1 billion in sales for the first time, with the Aerospace & Defense segment reaching a record backlog of over $600 million. The current results show continued momentum in this segment, with the backlog now at $605 million as of March 31, 2025.

The Maritime acquisition appears to be progressing well and is expected to contribute significantly to both revenue and earnings in fiscal 2025. However, investors may be concerned about integration risks or the sustainability of the strong performance across all segments in the face of potential economic headwinds.

Overall, ESCO Technologies continues to demonstrate strong operational execution and financial discipline, with impressive growth in orders, sales, earnings, and cash flow. The company’s ability to expand margins while growing revenue suggests effective cost management and pricing power in its markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.