US stock futures inch lower after Wall St marks fresh records on tech gains

Introduction & Market Context

ESCO Technologies Inc (NYSE:ESE) reported strong third-quarter fiscal 2025 results on August 7, showcasing significant growth across key financial metrics. The company’s stock closed at $189.87, down 1.1% on the day of the earnings call, despite the positive results. ESCO’s shares have performed well over the past year, trading between $113.30 and $198.34, reflecting investor confidence in the company’s growth strategy.

The Q3 presentation, delivered by President & CEO Bryan Sayler and Senior VP & CFO Chris Tucker, highlighted substantial revenue growth, margin expansion, and a record backlog that provides strong visibility for future performance. This quarter’s results continue the momentum seen in Q2 2025, when the company reported 24% EPS growth and 6.6% sales growth.

Quarterly Performance Highlights

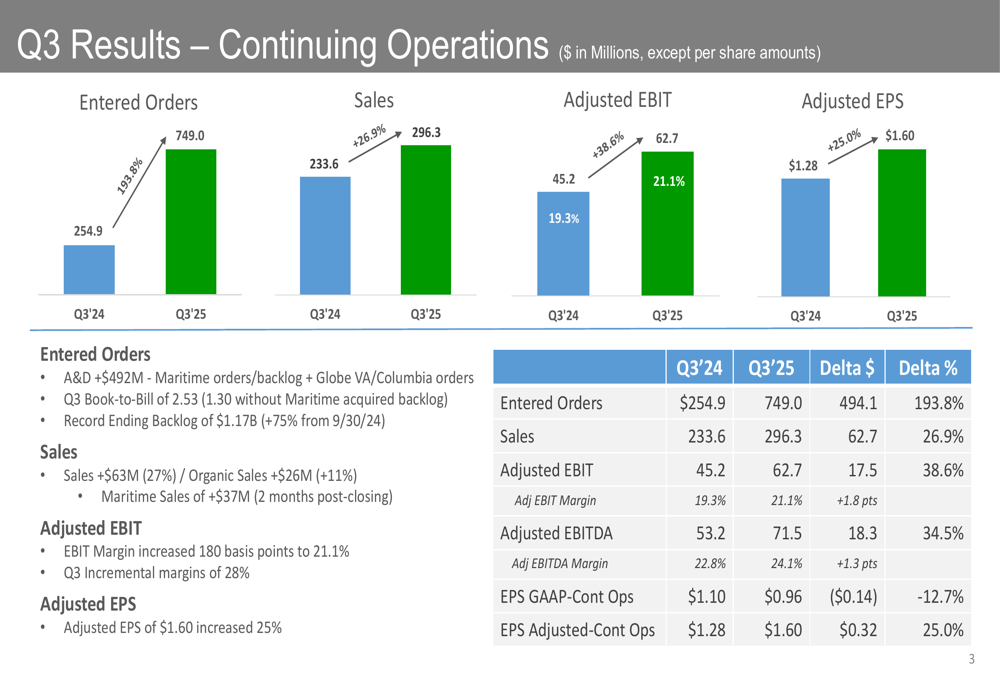

ESCO reported impressive Q3 results across all key financial metrics, with particularly strong performance in entered orders and sales growth. The company achieved $296.3 million in sales, representing a 26.9% increase compared to the same period last year. Organic sales grew by 11%, while the Maritime acquisition contributed an additional $37 million.

Adjusted EBIT rose 38.6% to $62.7 million, with margins expanding by 180 basis points to 21.1%. This margin improvement demonstrates the company’s operational efficiency and successful integration of acquisitions. Adjusted EBITDA increased 34.5% to $71.5 million.

As shown in the following chart of quarterly performance metrics:

Perhaps most notably, entered orders surged by 193.8% to $749 million, driven primarily by the Aerospace & Defense segment, which secured $492 million in Maritime orders. This exceptional order intake resulted in a book-to-bill ratio of 2.53 and a record backlog of $1.17 billion, representing a 75% increase from September 30, 2024.

Adjusted earnings per share grew 25% to $1.60, continuing the strong earnings momentum seen in previous quarters. GAAP EPS from continuing operations was $0.96, down 12.7% from the prior year, primarily due to one-time items related to acquisitions and restructuring.

Segment Analysis

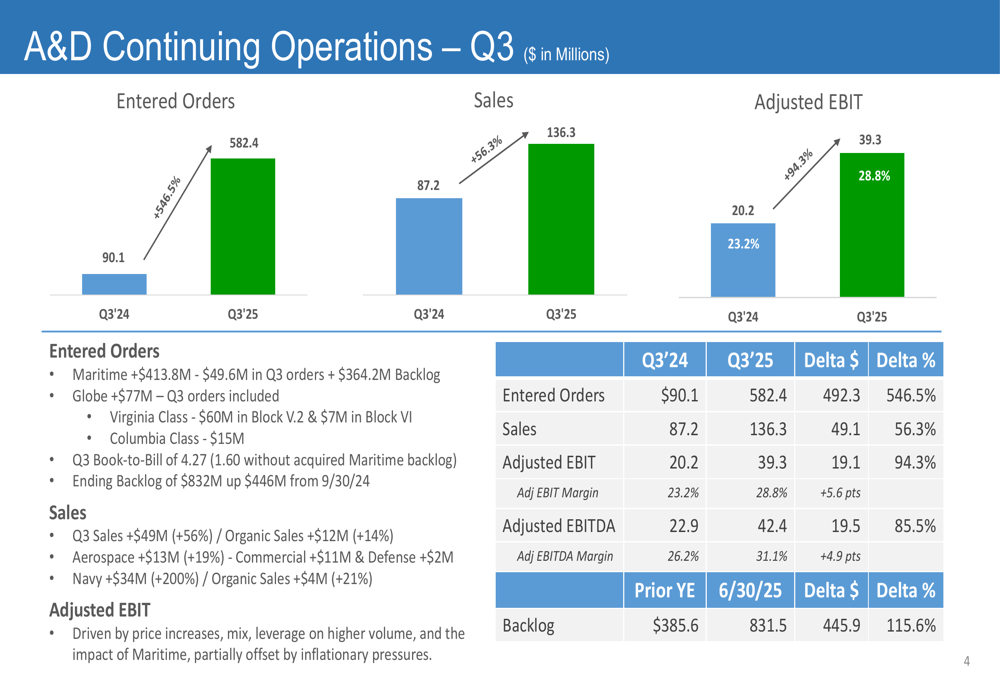

The Aerospace & Defense (A&D) segment delivered extraordinary performance in Q3, with entered orders increasing by 546.5% to $582.4 million. This remarkable growth was primarily driven by Maritime orders of $413.8 million and Globe orders of $77 million, resulting in a book-to-bill ratio of 4.27. Sales in the A&D segment increased 56.3% to $136.3 million, with significant contributions from both Aerospace and Navy programs.

The segment’s adjusted EBIT nearly doubled, growing 94.3% to $39.3 million, with margins expanding by 560 basis points to 28.8%. This exceptional performance underscores the strategic importance of ESCO’s recent Maritime acquisition and its strong positioning in defense markets.

The following chart illustrates the A&D segment’s outstanding quarterly performance:

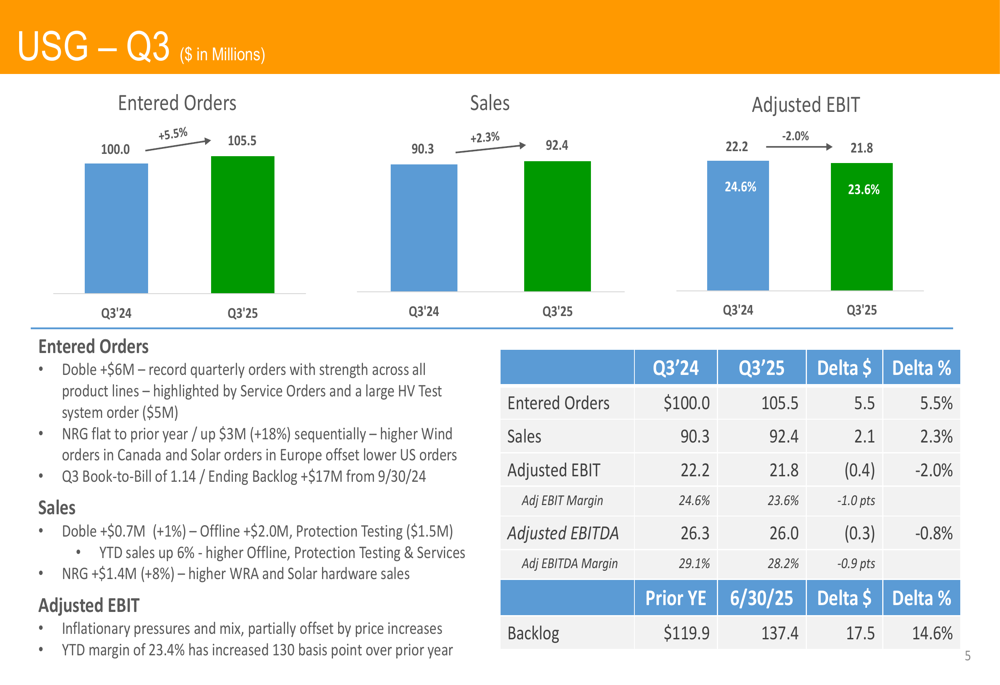

The Utility Solutions Group (USG) segment showed more modest growth, with entered orders increasing 5.5% to $105.5 million and sales rising 2.3% to $92.4 million. Doble, a key business within USG, saw orders increase by $6 million and sales grow by 1%. NRG sales increased by 8% or $1.4 million.

USG’s adjusted EBIT decreased slightly by 2.0% to $21.8 million, with margins contracting by 100 basis points to 23.6%. Despite this minor setback, the segment maintained a healthy backlog of $137.4 million, up 14.6% from the prior year-end.

The USG segment’s quarterly performance is illustrated in the following chart:

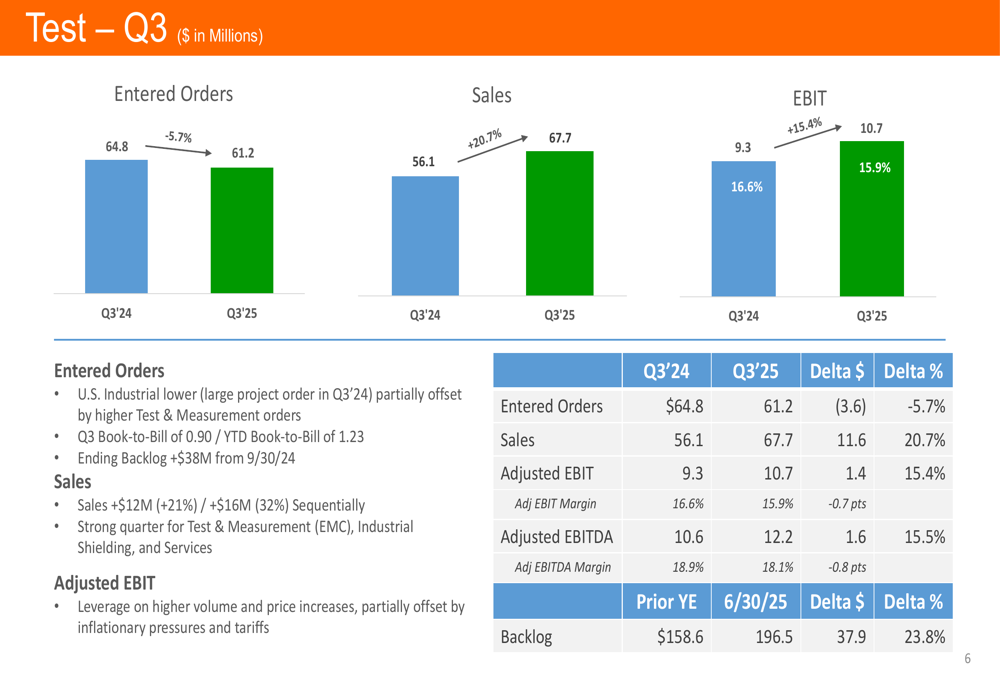

The Test segment delivered mixed results, with entered orders decreasing 5.7% to $61.2 million but sales increasing 20.7% to $67.7 million. Adjusted EBIT grew 15.4% to $10.7 million, though margins contracted slightly by 70 basis points to 15.9%. The segment’s backlog increased 23.8% to $196.5 million, providing a solid foundation for future growth.

The Test segment’s quarterly performance is shown in the following chart:

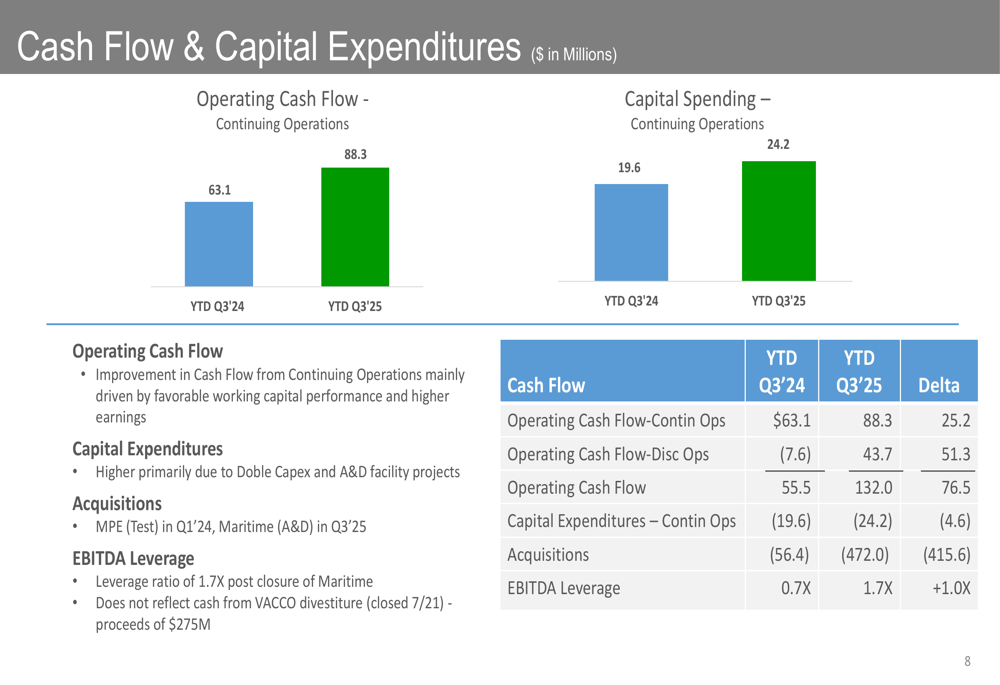

Financial Health & Cash Flow

ESCO demonstrated strong financial health in Q3, with operating cash flow from continuing operations increasing to $88.3 million for the year-to-date period, compared to $63.1 million in the prior year. Total (EPA:TTEF) operating cash flow reached $132.0 million, up from $55.5 million. Capital expenditures for continuing operations increased to $24.2 million from $19.6 million, reflecting continued investment in growth initiatives.

The company’s EBITDA leverage ratio increased to 1.7x from 0.7x, primarily due to the acquisition of Maritime Solutions. Despite this increase, ESCO maintains a strong balance sheet with ample liquidity to support its growth strategy.

The following chart details ESCO’s cash flow and capital expenditures:

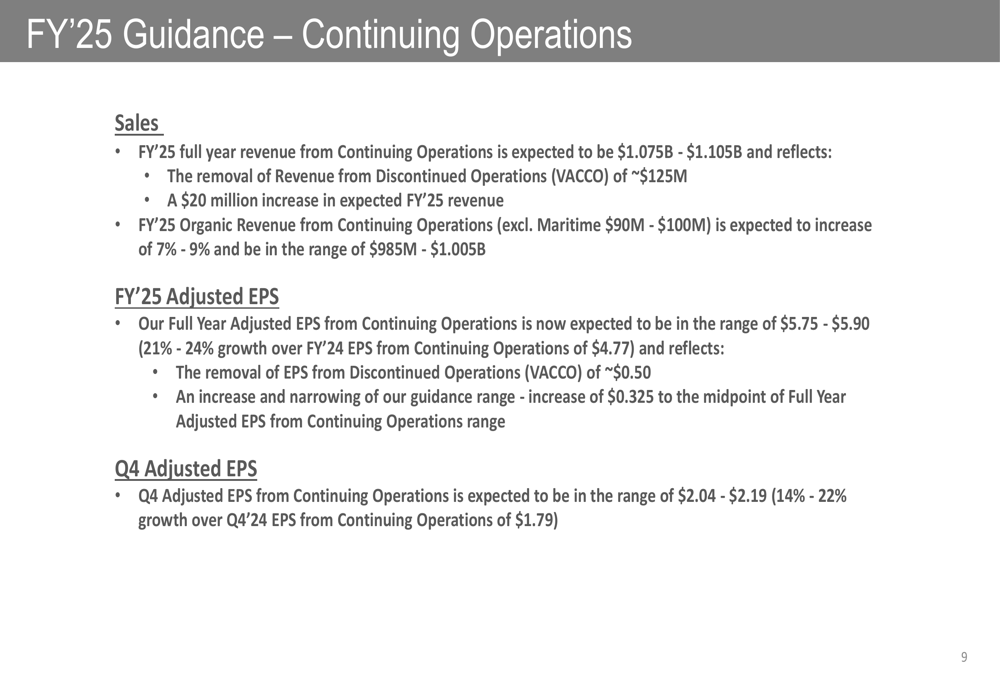

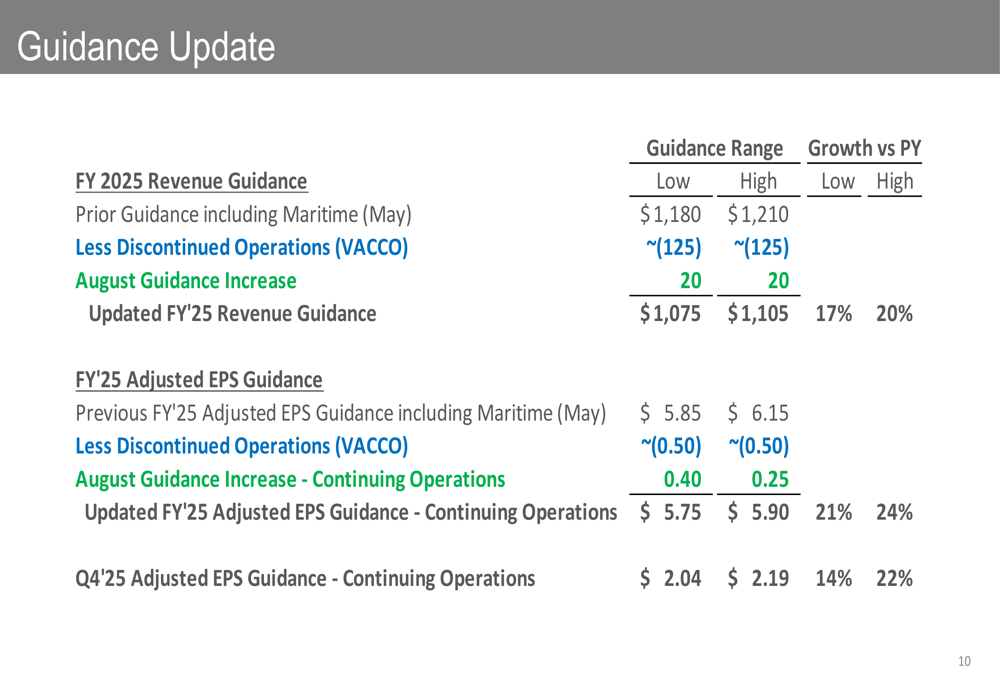

Forward Guidance & Outlook

Following the strong Q3 performance, ESCO raised its fiscal 2025 guidance. The company now expects sales to reach $1.075-$1.105 billion, representing a $20 million increase from previous guidance. Organic revenue (excluding Maritime) is projected to grow 7-9% to $985-$1.005 billion.

Adjusted EPS is expected to be in the range of $5.75-$5.90, representing 21-24% growth over fiscal 2024. For the fourth quarter, the company anticipates adjusted EPS of $2.04-$2.19, reflecting 14-22% growth compared to Q4 2024.

It’s worth noting that the updated guidance reflects the reclassification of the VACCO business as discontinued operations, which reduced the revenue guidance by approximately $125 million and EPS by about $0.50. Despite this adjustment, the core business outlook remains strong, as evidenced by the guidance increase.

The following chart details ESCO’s updated guidance for fiscal 2025:

The guidance update breakdown, showing the transition from previous to current guidance, is illustrated in the following chart:

In conclusion, ESCO Technologies delivered exceptional Q3 2025 results, driven primarily by the strong performance of its Aerospace & Defense segment. The record backlog of $1.17 billion provides significant visibility for future growth, while the raised guidance reflects management’s confidence in the company’s strategic direction. Despite the reclassification of VACCO as discontinued operations, ESCO’s core business momentum remains strong, positioning the company for continued success in the remainder of fiscal 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.