German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Esprinet (BIT:PRT) presented its H1 2025 financial results on September 10, 2025, showcasing a significant improvement in profitability during the second quarter that helped offset a weaker first quarter. The company’s stock has responded positively, trading up 14.58% at €5.03, rebounding from its post-Q1 earnings slump when it fell nearly 10%.

The ICT distribution market in Europe has performed better than expected, with analysts now projecting low to mid-single-digit growth for the year. This improved market environment has provided a favorable backdrop for Esprinet’s operations across its Southern European markets.

Quarterly Performance Highlights

Esprinet’s Q2 2025 results marked a substantial improvement over Q1, with revenues reaching €969.1 million, a 5% increase compared to Q2 2024. This growth trajectory builds upon the momentum established in the first quarter, resulting in H1 2025 sales of €1,931.5 million, up 4% year-over-year.

The most notable aspect of Q2 performance was the significant profitability improvement. Q2 EBITDA Adjusted surged 38% compared to the same period last year, helping to drive H1 2025 EBITDA Adjusted to €25.1 million, a 2% increase over H1 2024.

As shown in the following comprehensive performance overview:

Gross profit for Q2 2025 increased by 9% year-over-year, with margins expanding to 5.83% from 5.59% in Q2 2024. This improvement helped lift H1 2025 gross profit to €110.9 million, 6% higher than the previous year, with an overall gross margin of 5.74%.

Net income for Q2 2025 reached €2.9 million, a dramatic improvement from just €0.1 million in Q2 2024. This strong performance helped H1 2025 net income reach €3.4 million, slightly above the €3.3 million recorded in H1 2024, despite a challenging first quarter.

Detailed Financial Analysis

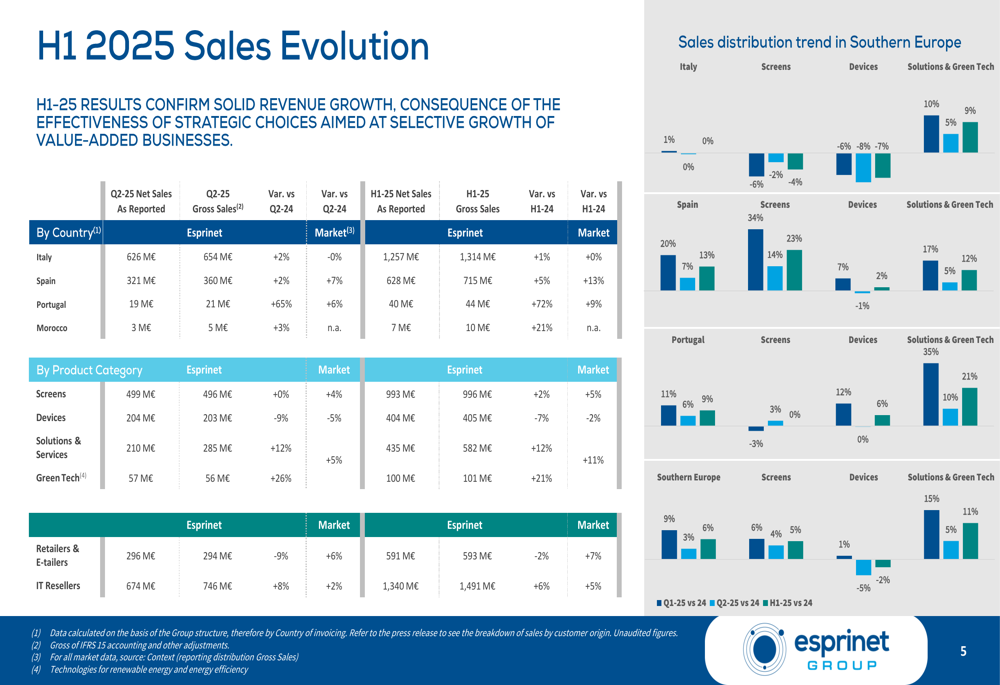

The company’s sales evolution across different regions and product categories reveals balanced growth, with particularly strong performance in high-value segments. The following breakdown illustrates the distribution of sales:

Italy remains Esprinet’s largest market, contributing €1,257 million in H1 2025 sales, followed by Spain with €628 million. The company’s product mix shows "Screens" as the dominant category with €993 million in H1 sales, while "Solutions & Services" generated €435 million, representing the company’s strategic shift toward higher-margin offerings.

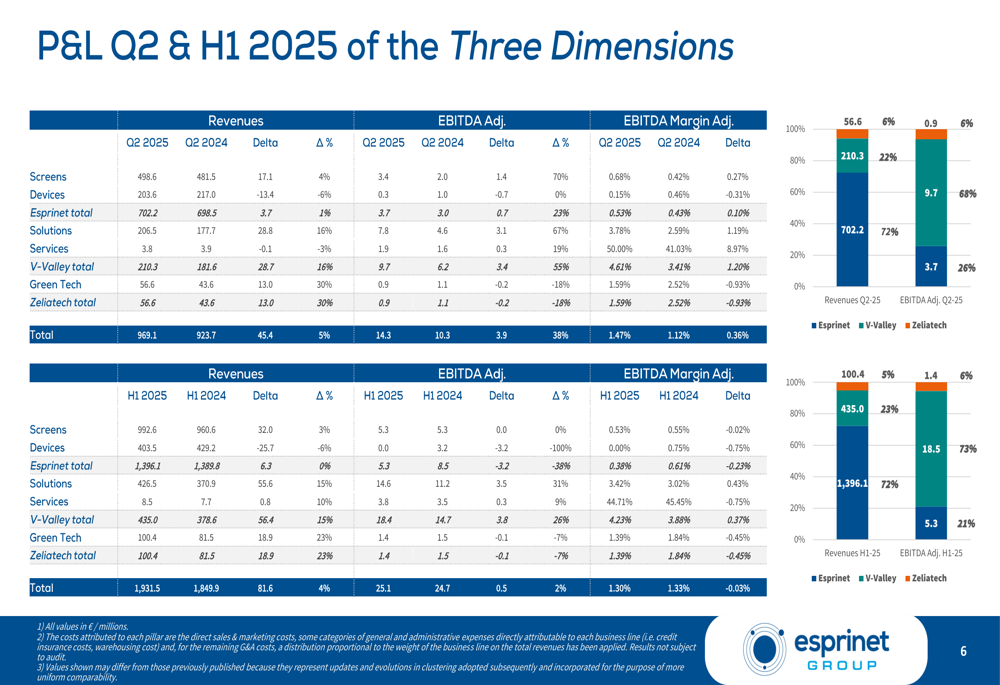

The P&L analysis across Esprinet’s three business dimensions—Esprinet, V-Valley, and Zeliatech—highlights the growth in specialized divisions:

The V-Valley division, focused on value-added distribution, recorded 12% growth in gross sales during H1 2025, while the Zeliatech division accelerated significantly with 26% growth in Q2 2025. These specialized divisions are central to Esprinet’s strategy of transitioning from volume to value-added distribution, a shift that was highlighted as challenging but necessary in the Q1 2025 earnings call.

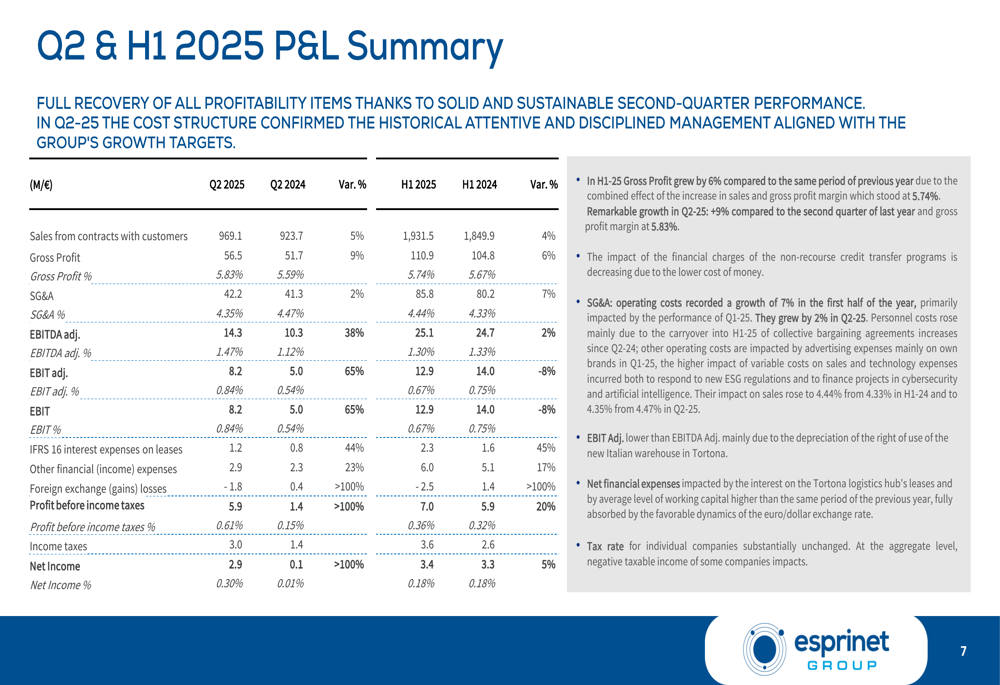

A detailed look at the P&L summary further illustrates the Q2 recovery:

Operating costs grew by 7% in H1 2025, but the company managed to limit this growth to just 2% in Q2 2025, demonstrating improved cost control. This addresses concerns raised after Q1 results about elevated general and administrative expenses impacting profitability.

Balance Sheet and Working Capital

Despite the operational improvements, Esprinet’s balance sheet shows some concerning trends. The net financial position deteriorated to negative €327.5 million as of June 30, 2025, compared to negative €164.0 million a year earlier, representing a significant increase in debt.

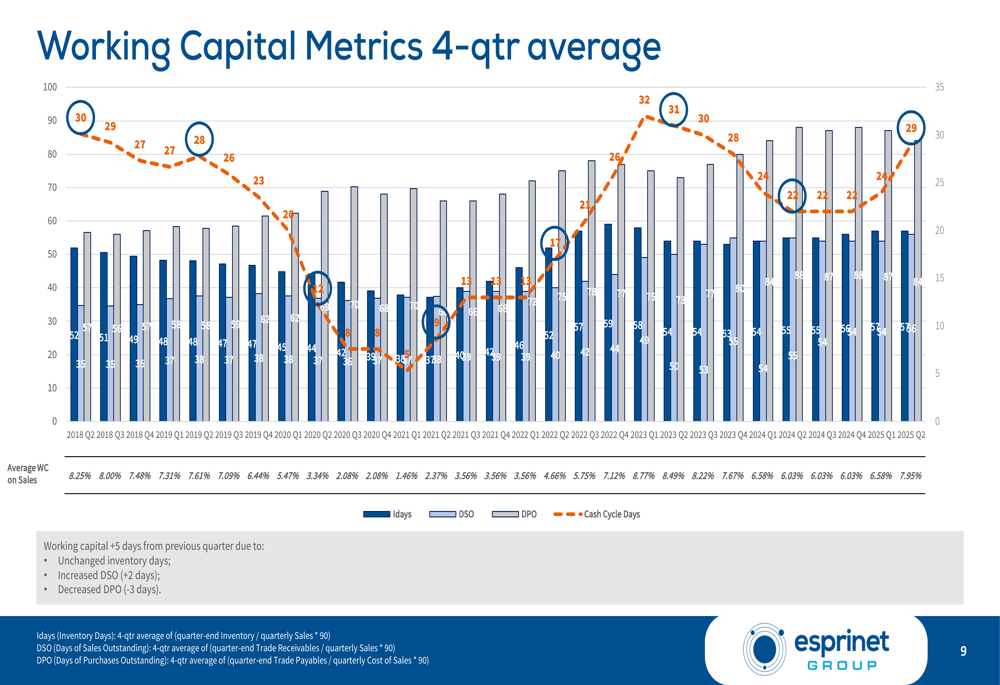

The company’s working capital metrics also show challenges, with the Cash Conversion Cycle extending to 29 days, 7 days longer than in Q2 2024. This increase is primarily due to unchanged inventory days, increased Days Sales Outstanding (+2 days), and decreased Days Payable Outstanding (-3 days).

The following chart illustrates the working capital trends:

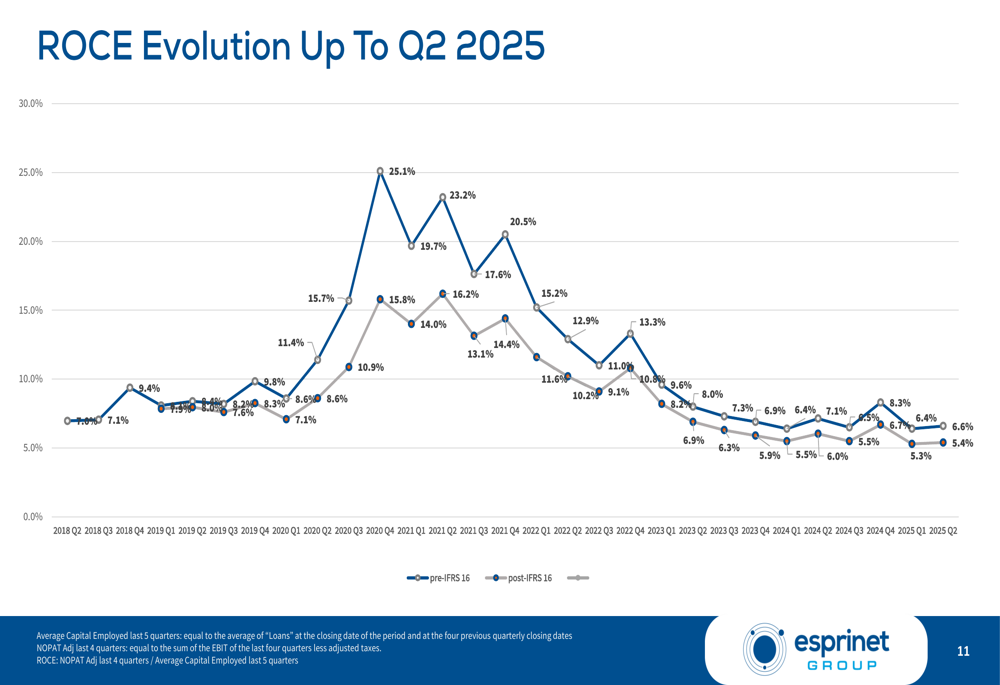

Return on Capital Employed (ROCE) stands at 6.6%, reflecting the impact of increased capital requirements on the company’s efficiency metrics:

Forward-Looking Statements

Esprinet’s outlook for the remainder of 2025 appears positive, with management noting that the revenue growth recorded in H1 2025 continued at an even more pronounced rate in July and August. The company has confirmed its EBITDA adjusted guidance of €63-71 million for the full year, focusing on the upper end of this range.

This guidance represents a more optimistic outlook compared to the cautious stance taken after Q1 results, reflecting the improved performance in Q2 and early Q3:

Industry analysts have revised their forecasts upward following stronger-than-expected market performance in Q2 2025, providing a supportive backdrop for Esprinet’s operations across Southern Europe.

Executive Summary

Esprinet’s H1 2025 results demonstrate a company in transition that is beginning to show signs of successful execution on its strategic shift toward higher-margin, value-added distribution. The significant improvement in Q2 profitability has helped offset a challenging Q1, resulting in modest growth for the half-year period.

While operational metrics show improvement, particularly in gross margins and cost control, the deterioration in the company’s financial position and working capital metrics presents ongoing challenges. The substantial increase in net debt compared to the previous year will require careful management to ensure long-term financial stability.

The market has responded positively to these results, with the stock rebounding significantly from its post-Q1 lows. As Esprinet continues to execute on its strategic transformation, investors will be watching closely to see if the improved profitability in Q2 can be sustained through the second half of 2025, particularly in light of the company’s more optimistic guidance focusing on the upper end of its EBITDA range.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.