Blazing Star Merger Sub completes Walgreens debt tender offer

Introduction & Market Context

Euronet Worldwide Inc (NASDAQ:EEFT) released its first quarter 2025 financial results on April 24, showing continued revenue growth across all business segments while facing pressure on its adjusted earnings per share. The financial technology company, which operates in payment processing and money transfer services, reported a 7% increase in revenue but a 12% decrease in adjusted EPS compared to the same period last year.

The results come after a strong fourth quarter 2024, when Euronet surpassed analyst expectations with an EPS of $2.08 and revenue of $1.05 billion. While Q1 typically represents a seasonal low point for the company, Euronet maintained its growth trajectory in terms of top-line performance.

Euronet’s stock closed at $97.49 on the day of the earnings release, down 1.8% from the previous close, suggesting investors may have had mixed reactions to the results, particularly the EPS decline.

Quarterly Performance Highlights

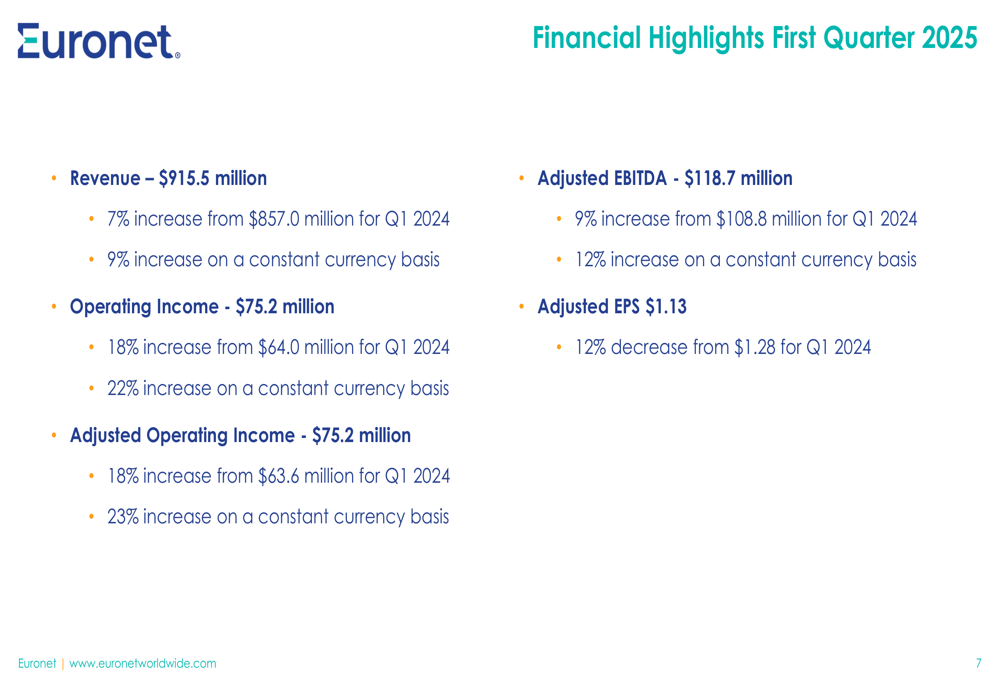

Euronet reported Q1 2025 revenue of $915.5 million, a 7% increase from $857.0 million in Q1 2024. On a constant currency basis, revenue growth was even stronger at 9%. Operating income and adjusted operating income both increased by 18% to $75.2 million, while adjusted EBITDA grew 9% to $118.7 million.

As shown in the following financial highlights chart:

Despite the strong revenue and operating income growth, adjusted earnings per share declined 12% to $1.13 from $1.28 in Q1 2024. This decline in EPS contrasts with the company’s previously stated projection of 12-16% EPS growth for 2025, potentially raising questions about full-year performance expectations.

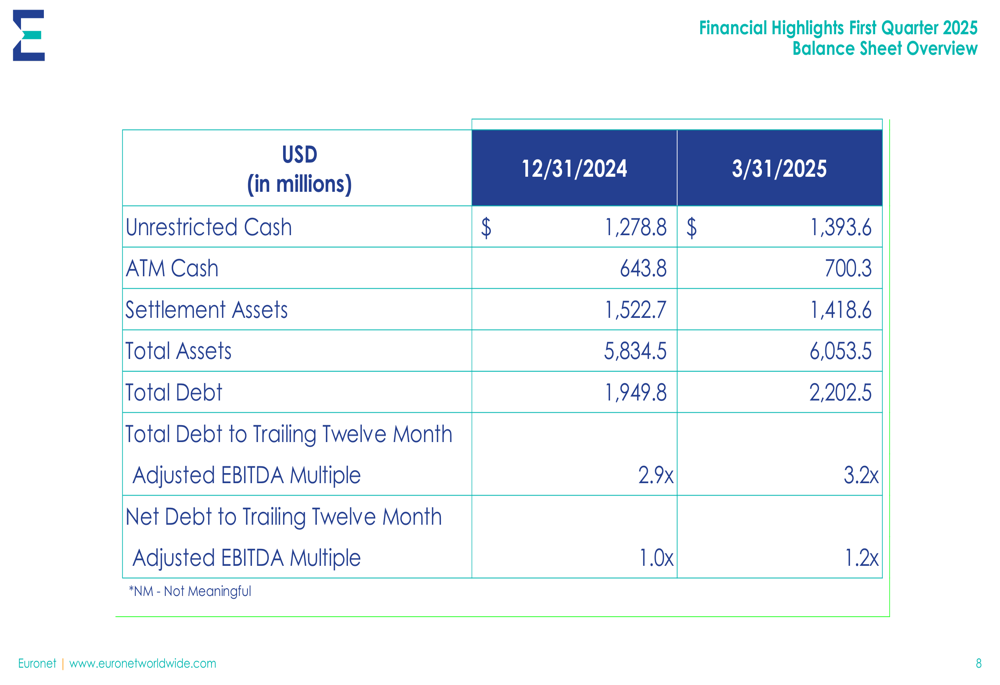

The company’s balance sheet remained solid with $1,393.6 million in unrestricted cash as of March 31, 2025, though total debt increased to $2,202.5 million from $1,949.8 million at the end of 2024. This resulted in a slight increase in leverage ratios, with the total debt to trailing twelve-month adjusted EBITDA multiple rising from 2.9x to 3.2x.

The following balance sheet overview illustrates these changes:

Segment Performance Analysis

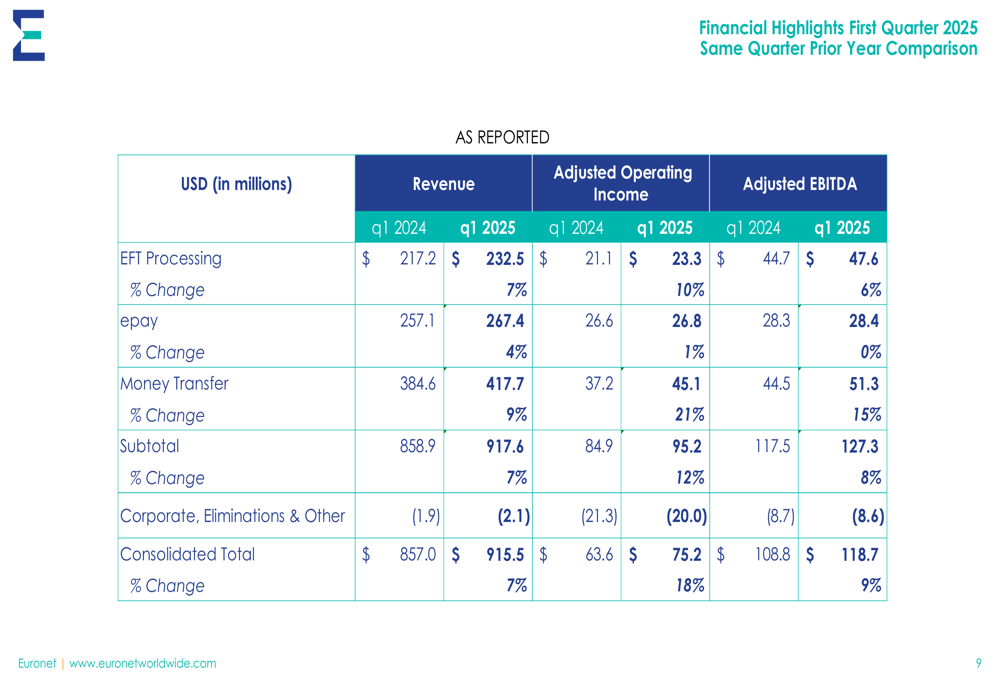

All three of Euronet’s business segments contributed to the overall revenue growth, though with varying performance levels. The Money Transfer segment led with 9% revenue growth, followed by EFT Processing at 7% and epay at 4%.

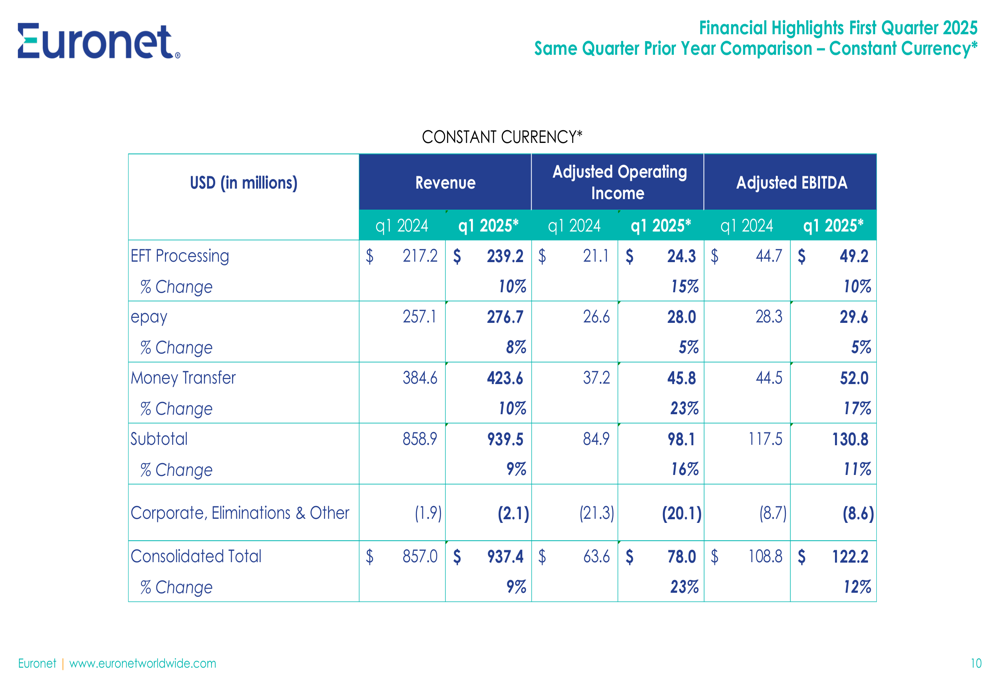

When viewed on a constant currency basis, the growth rates were even more impressive, with both EFT Processing and Money Transfer segments achieving 10% growth, while epay grew by 8%. This demonstrates the underlying strength of the business when excluding currency fluctuations.

The detailed segment comparison reveals the performance metrics across all business lines:

The constant currency comparison provides a clearer picture of the organic growth across segments:

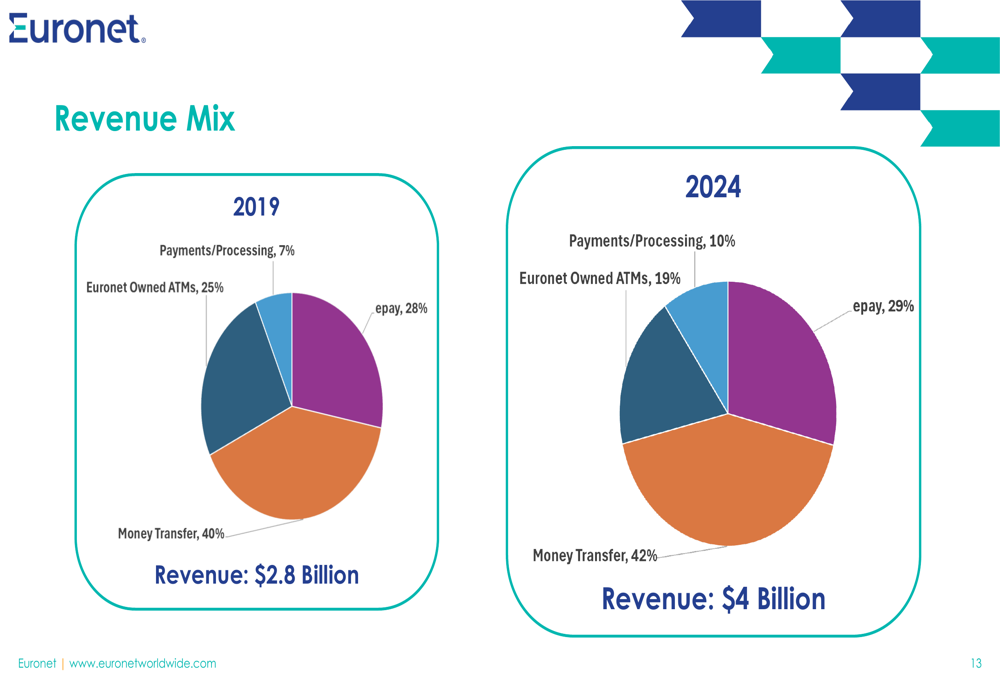

Over the past five years, Euronet has been gradually shifting its revenue mix toward higher-growth digital payment services. The comparison between 2019 and 2024 revenue mix shows an increase in the Payments/Processing segment from 7% to 10% and Money Transfer from 40% to 42%, while Euronet Owned ATMs decreased from 25% to 19%.

This strategic shift in revenue composition is illustrated in the following chart:

Strategic Initiatives and Partnerships

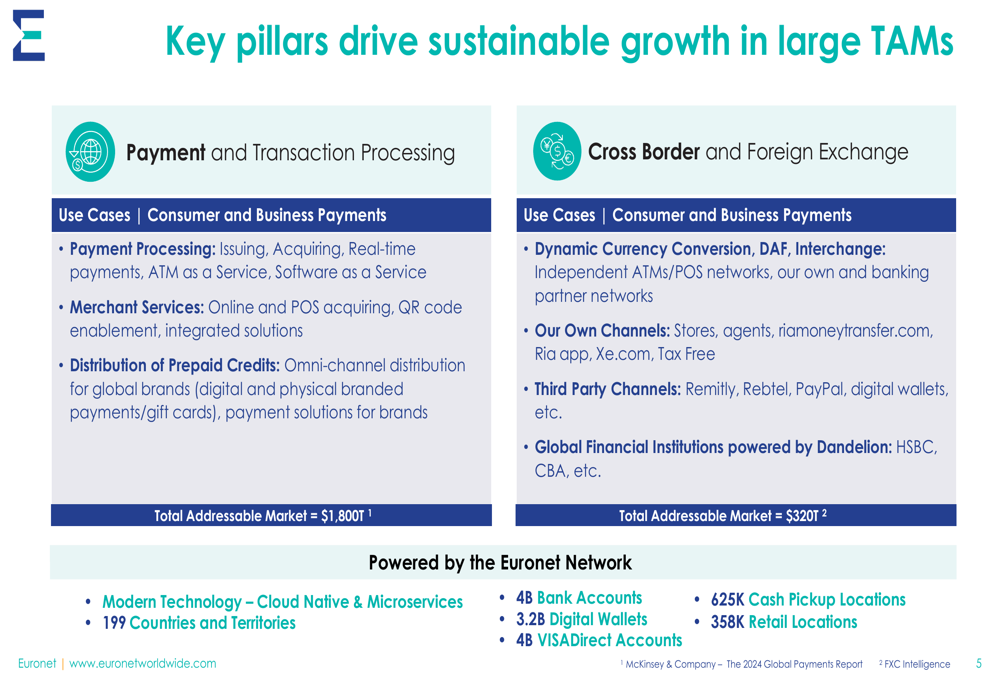

Euronet continues to expand its global network and service offerings through strategic partnerships and new product launches. The company operates in large addressable markets, with Payment and Transaction (JO:NTUJ) Processing estimated at $1,800 trillion and Cross Border and Foreign Exchange at $320 trillion.

The company’s growth strategy is built on expanding its global network, which now reaches 199 countries and territories, connects to 4 billion bank accounts, 3.2 billion digital wallets, and 4 billion VISA Direct accounts, as shown in this overview:

In the EFT Processing segment, Euronet launched independent ATM networks, signed network participation agreements, and renewed ATM service agreements. The company also expanded its merchant services in Greece, signing 6,800 merchants, and secured a five-year renewal with Avolta AG.

The epay segment signed new contracts with Sony (NYSE:SONY) in Turkey, Mission:Control, and a payment processing contract with Munich Airport.

In the Money Transfer segment, Ria signed 22 agreements across 20 countries, while the Dandelion network added Skyee as a partner. Ria also launched 13 partners in 11 countries and expanded its Visa (NYSE:V) Direct capabilities, potentially reaching four billion debit cards globally.

Forward-Looking Statements

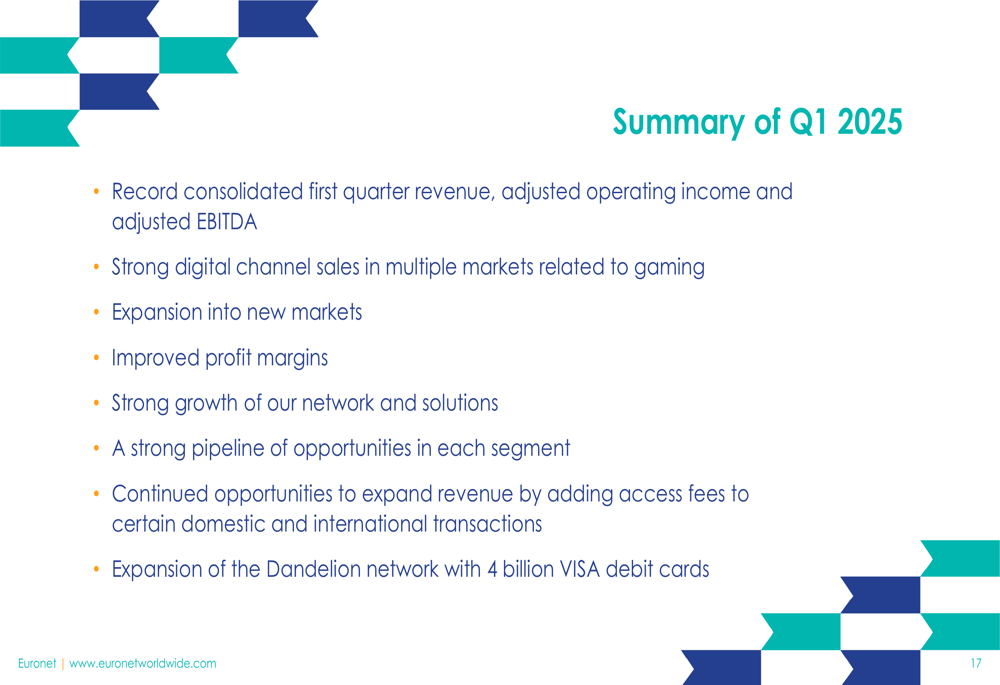

Euronet’s management highlighted several positive developments and opportunities for future growth. The company achieved record consolidated first quarter revenue, adjusted operating income, and adjusted EBITDA. Strong digital channel sales were reported in multiple markets, particularly related to gaming.

The company emphasized its continued expansion into new markets and improved profit margins. Management also pointed to a strong pipeline of opportunities across all segments and plans to expand revenue by adding access fees to certain domestic and international transactions.

The summary of Q1 2025 results and outlook is captured in this slide:

While the company faces challenges, including the unexpected decline in adjusted EPS and increased debt levels, Euronet’s diversified business model and global expansion strategy position it to capitalize on growth opportunities in the digital payments ecosystem.

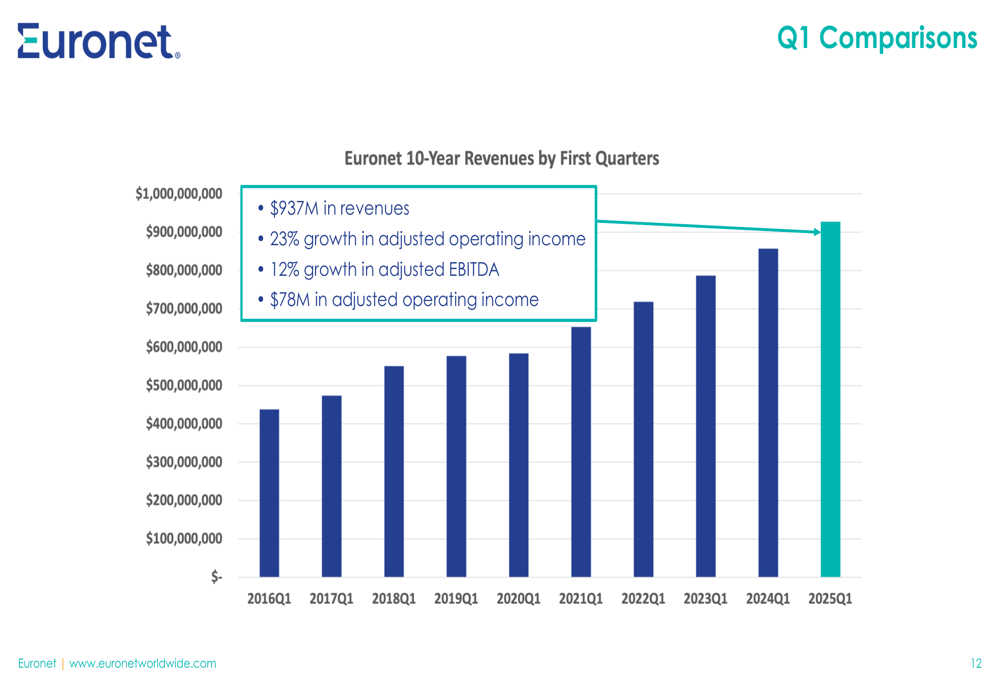

The 10-year revenue trend for first quarters shows Euronet’s consistent growth trajectory, with Q1 2025 revenue reaching approximately $937 million on a constant currency basis:

Looking ahead, investors will likely focus on whether Euronet can reverse the EPS decline in coming quarters to achieve its previously stated 12-16% EPS growth target for 2025, while continuing to expand its global network and service offerings in an increasingly competitive payments landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.