SoFi stock falls after announcing $1.5B public offering of common stock

Introduction & Market Context

Fasadgruppen Group AB (FG) presented its second quarter 2025 results on August 14, 2025, revealing significant profitability improvements despite ongoing challenges in organic growth. The company's stock responded positively, surging 18.12% following the presentation, reflecting investor confidence in the company's strategic direction.

The Nordic facade specialist continues to navigate a challenging market environment characterized by low new build activity, particularly in Sweden. Despite these headwinds, Fasadgruppen has maintained its focus on improving profitability and reducing leverage while pursuing strategic growth opportunities.

Quarterly Performance Highlights

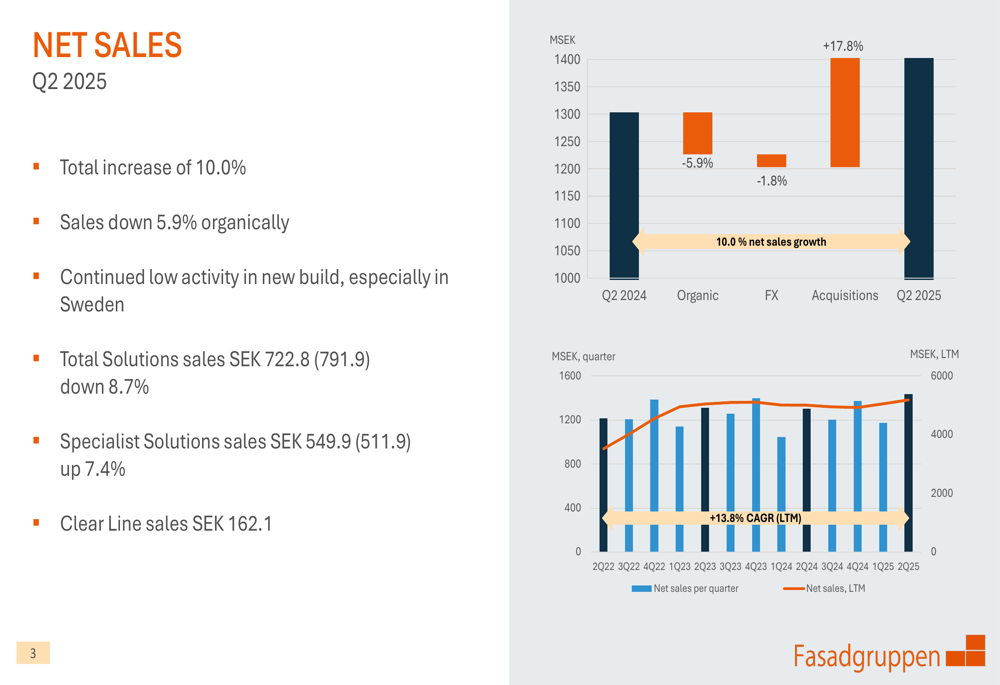

Fasadgruppen reported a 10.0% increase in net sales for Q2 2025, though organic sales declined by 5.9%. The growth was primarily driven by acquisitions, which contributed 17.8% to the overall sales increase, while currency effects had a negative impact of 1.8%.

As shown in the following chart of quarterly net sales growth:

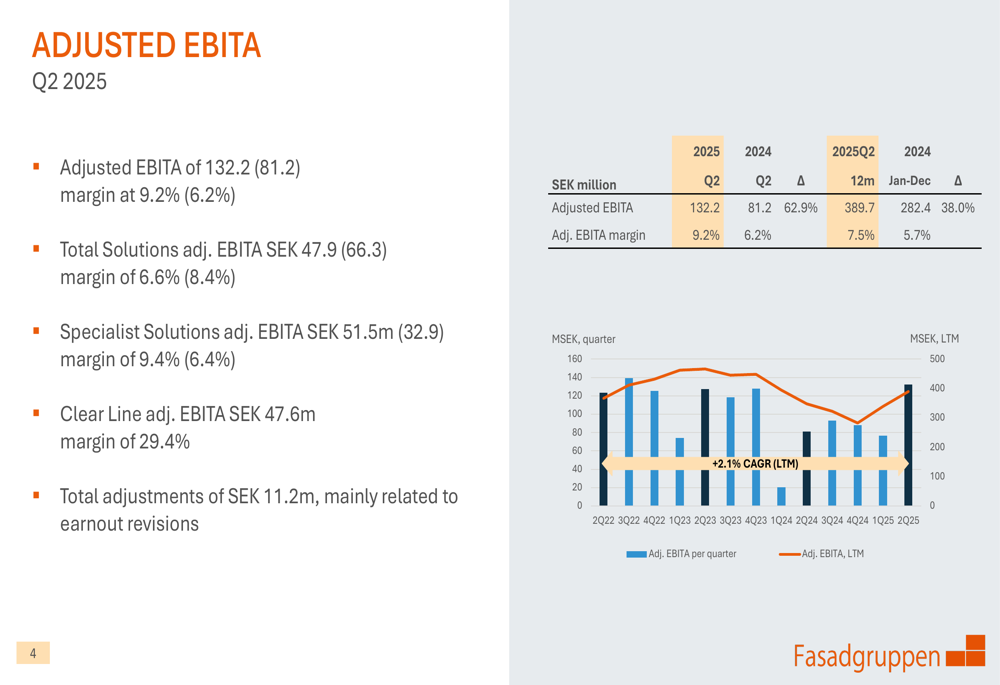

The company's profitability showed remarkable improvement, with adjusted EBITA reaching 132.2 million SEK compared to 81.2 million SEK in Q2 2024. This represents a significant margin expansion from 6.2% to 9.2%, underscoring the effectiveness of the company's profitability initiatives.

The following chart illustrates the adjusted EBITA development:

CEO Martin Jacobsson noted during the presentation that while the company has "much to be proud of," there is still "much left to prove," signaling a balanced perspective on the company's achievements and challenges ahead.

Segment Performance

Fasadgruppen's performance varied across its three business segments. The Total Solutions segment experienced an 8.7% decline in sales to 722.8 million SEK, with adjusted EBITA falling to 47.9 million SEK from 66.3 million SEK in the previous year. The segment's margin contracted from 8.4% to 6.6%.

In contrast, the Specialist Solutions segment showed strong performance with a 7.4% increase in sales to 549.9 million SEK. Adjusted EBITA for this segment rose significantly to 51.5 million SEK from 32.9 million SEK, with the margin expanding from 6.4% to 9.4%.

The Clear Line segment, which represents the company's UK operations, contributed 162.1 million SEK in sales with an impressive adjusted EBITA of 47.6 million SEK and a margin of 29.4%. However, the segment faced challenges due to delays from the Building Safety Regulator (BSR) impacting its order backlog.

Order Backlog and Future Work

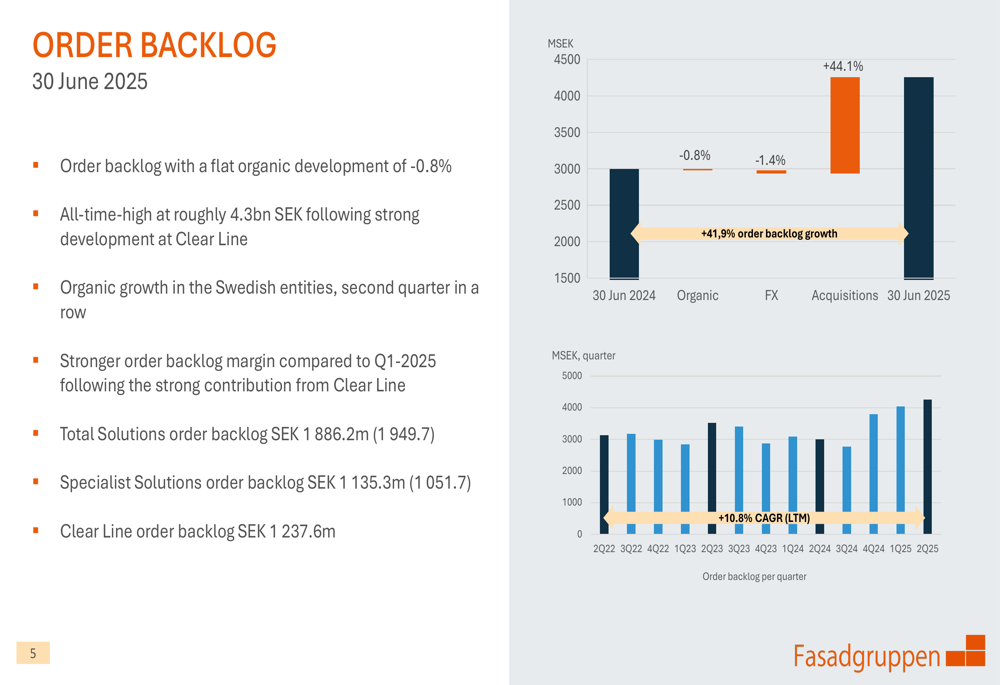

Despite market challenges, Fasadgruppen reported an all-time high order backlog of approximately 4.3 billion SEK as of June 30, 2025. The organic development was relatively flat at -0.8%, but acquisitions contributed 44.1% to the overall growth of 41.9% compared to the previous year.

The order backlog data is visualized in the following chart:

The company noted stronger order backlog margins compared to Q1 2025, primarily due to the strong contribution from Clear Line. Additionally, Swedish entities showed organic growth in their order backlog for the second consecutive quarter, suggesting potential stabilization in the company's home market.

Financial Position

Fasadgruppen demonstrated strong cash flow performance in Q2 2025, with operating cash flow increasing by 95.9% to 180.7 million SEK compared to 92.2 million SEK in the same period last year. The cash conversion rate improved to 115.9% from 84.2%.

The company's cash flow development is illustrated in the following chart:

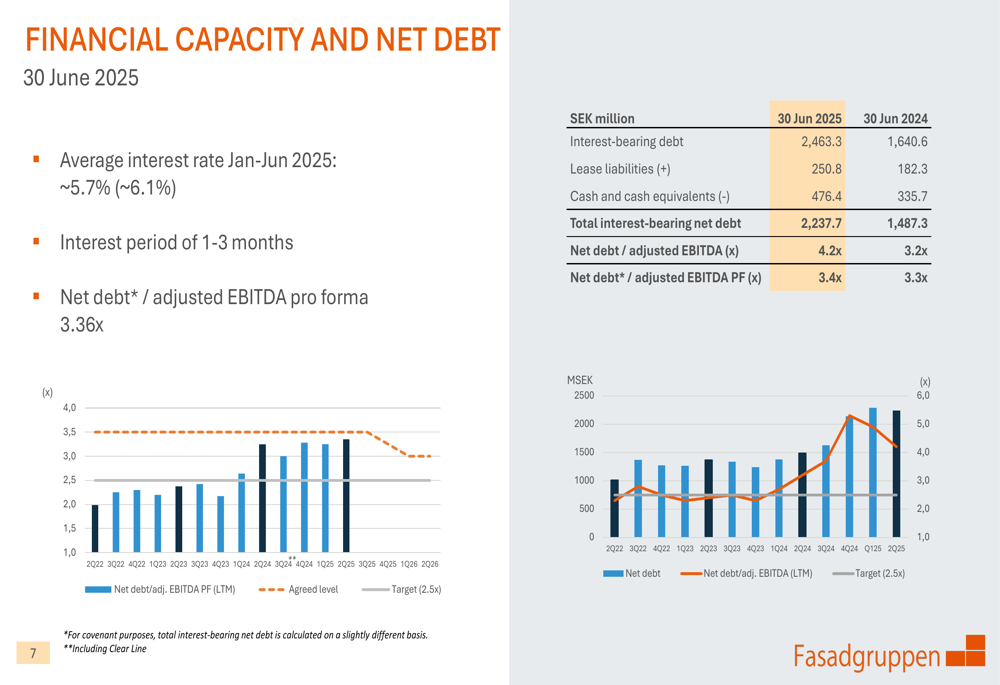

The company's leverage remains a key focus area, with net debt to adjusted EBITDA pro forma standing at 3.36x. Management emphasized their commitment to reducing this ratio below the target of 2.5x. The company also secured a two-quarter extension on its covenant step down, providing additional financial flexibility.

The following chart shows the company's net debt development:

Strategic Initiatives

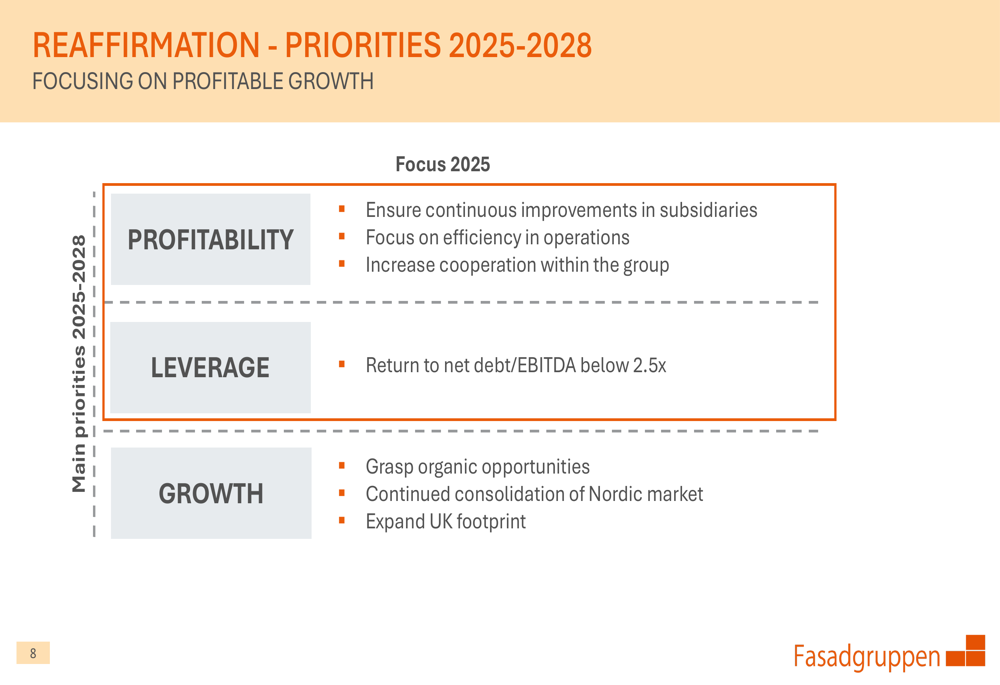

Fasadgruppen reaffirmed its strategic priorities for 2025-2028, focusing on three key areas: profitability, leverage, and growth. The company's immediate focus for 2025 is on ensuring continuous improvements in subsidiaries, enhancing operational efficiency, and increasing cooperation within the group.

The strategic priorities are outlined in the following image:

In terms of growth, Fasadgruppen plans to continue its consolidation of the Nordic market while expanding its footprint in the UK. However, the company emphasized that deleveraging remains a priority before pursuing aggressive expansion.

Forward-Looking Statements

Looking ahead, Fasadgruppen faces both challenges and opportunities. The company acknowledged the continued low activity in the new build sector, particularly in Sweden, and regulatory delays affecting its UK operations. However, the record-high order backlog provides a solid foundation for future performance.

Management expressed confidence in their ability to improve profitability through operational efficiencies and increased cooperation within the group. The company also highlighted the potential for organic growth opportunities alongside its strategic acquisitions.

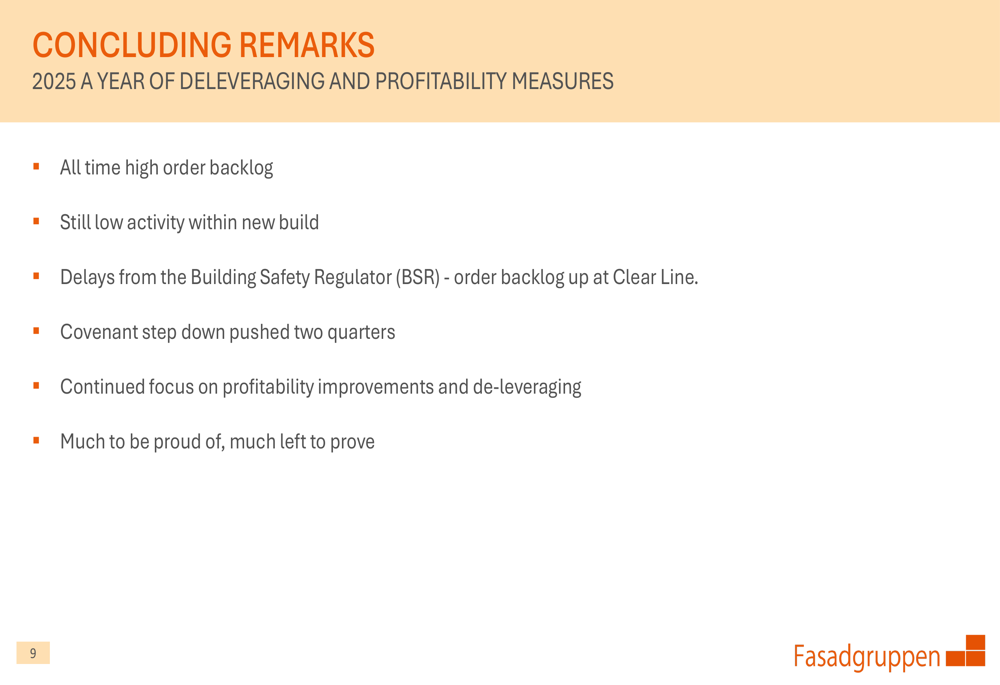

As summarized in the concluding remarks of the presentation:

Fasadgruppen's performance in Q2 2025 demonstrates the company's resilience in challenging market conditions. While organic growth remains under pressure, significant improvements in profitability and a record order backlog position the company well for future growth once it achieves its deleveraging targets. Investors appear to share this optimism, as reflected in the substantial stock price increase following the presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.