Elastic launches GPU-accelerated inference service for AI workflows

Introduction & Market Context

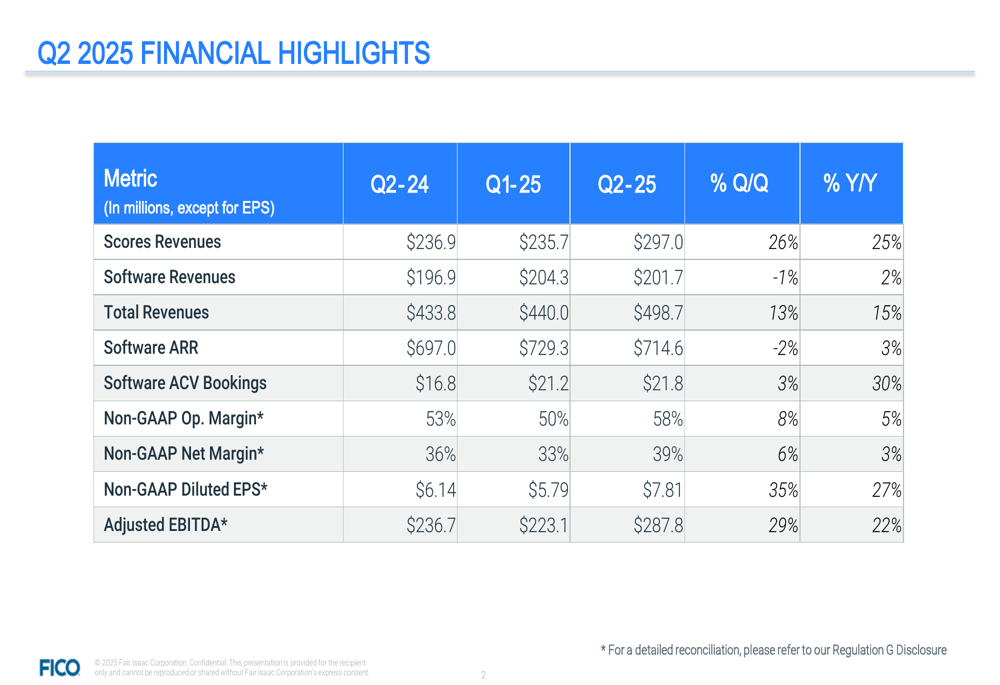

Fair Isaac Corporation (NYSE:FICO) released its Q2 2025 financial results on April 29, 2025, showing a strong recovery from its disappointing Q1 performance. The company reported total revenues of $498.7 million, up 15% year-over-year and 13% quarter-over-quarter, significantly outpacing the previous quarter’s performance when the company missed analyst expectations. Following the release, FICO’s stock traded at $1,953.70 in the after-market session, showing a slight decline of 0.14%.

The results mark a substantial improvement from Q1 2025, when FICO missed EPS expectations by 4.8% and saw its stock fall by 7.17%. This quarter’s performance demonstrates the company’s resilience and ability to rebound, particularly through its Scores segment.

Quarterly Performance Highlights

FICO’s Q2 2025 financial results show substantial growth across key metrics compared to both the previous quarter and the same period last year. The company’s non-GAAP diluted EPS reached $7.81, representing a 27% increase year-over-year and an impressive 35% jump quarter-over-quarter.

As shown in the following comprehensive financial highlights table:

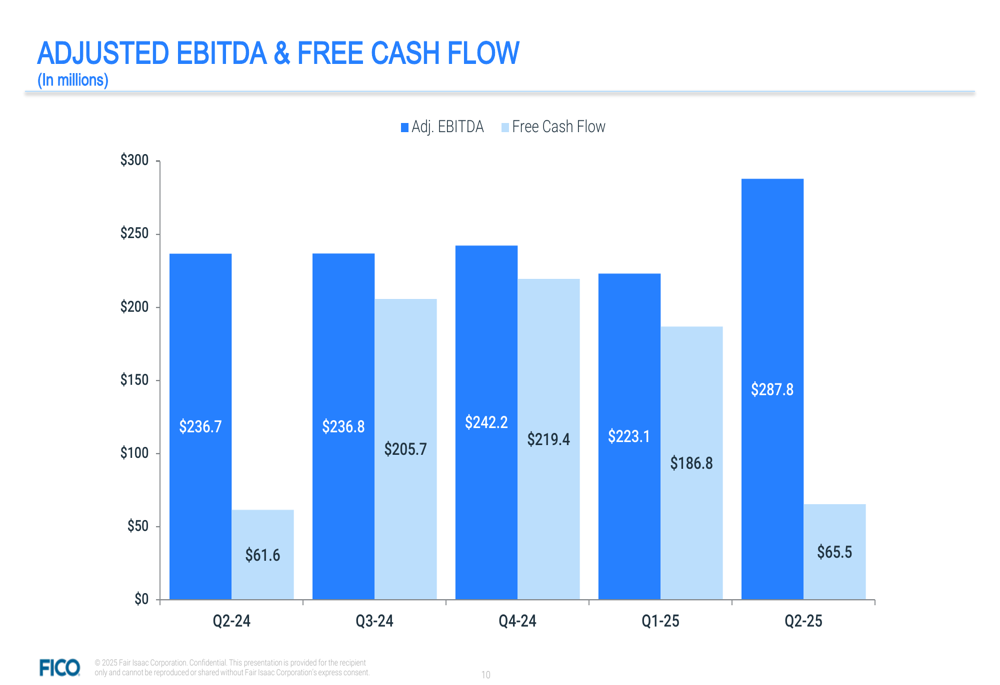

Total (EPA:TTEF) revenues increased to $498.7 million, up 15% from Q2 2024 and 13% from Q1 2025. Adjusted EBITDA rose to $287.8 million, a 22% increase year-over-year and 29% quarter-over-quarter. The company’s non-GAAP operating margin expanded to 58%, up 5 percentage points year-over-year and 8 percentage points sequentially.

The following chart illustrates the positive trajectory across key operating metrics:

Segment Analysis

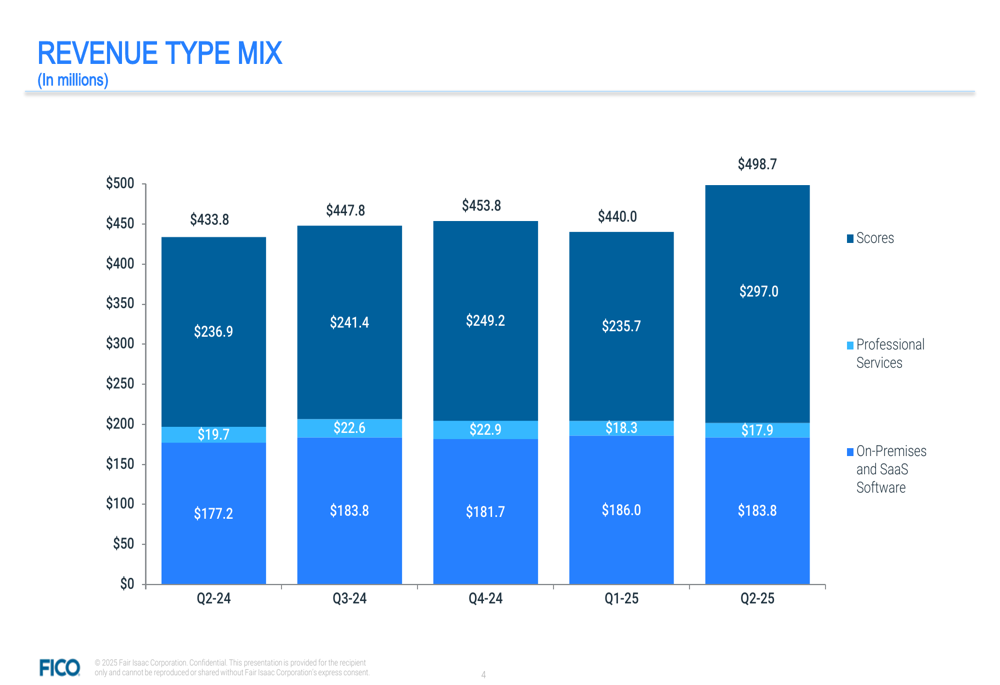

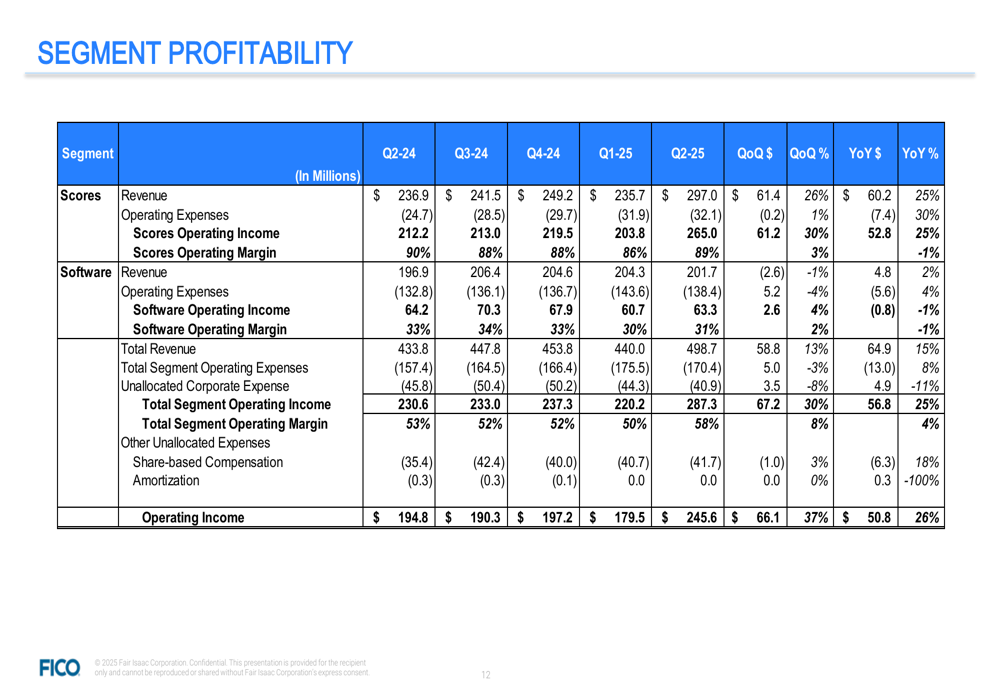

FICO’s performance reveals a stark contrast between its two main business segments. The Scores segment, which includes the company’s credit scoring products, delivered exceptional results with revenues of $297.0 million, up 25% year-over-year and 26% quarter-over-quarter. This segment maintained an impressive operating margin of 89%.

The revenue mix breakdown shows how the Scores segment has become an increasingly dominant contributor to overall performance:

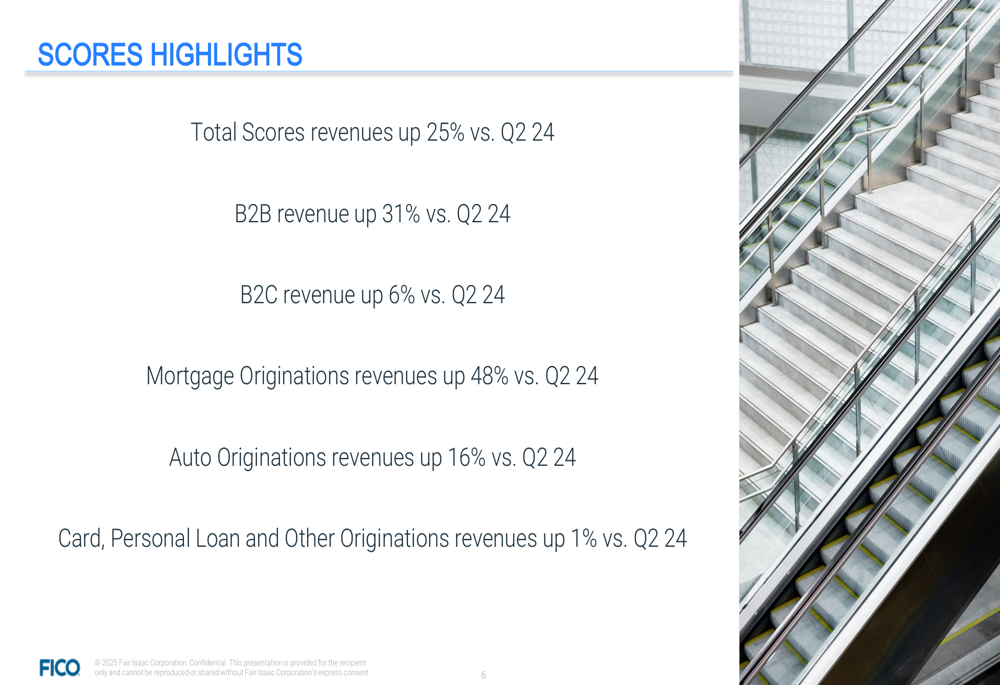

The Scores segment benefited significantly from increased mortgage activity, with mortgage originations revenues up 48% year-over-year. Auto originations revenues also performed strongly, increasing 16% compared to Q2 2024. The following highlights from the Scores segment illustrate these trends:

In contrast, the Software (ETR:SOWGn) segment showed more modest performance with revenues of $201.7 million, up just 2% year-over-year and down 1% quarter-over-quarter. The segment’s operating margin was 31%, significantly lower than the Scores segment.

The detailed segment profitability analysis reveals this divergence in performance:

Software Metrics and Trends

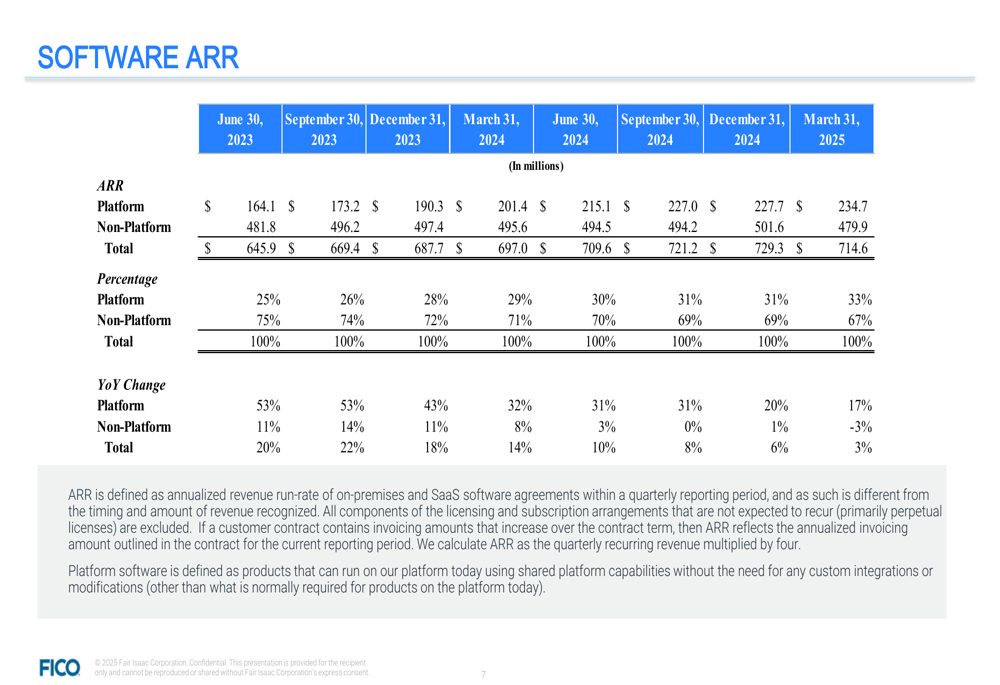

FICO’s software business shows mixed signals with Annual Recurring Revenue (ARR) reaching $714.6 million, up 3% year-over-year but down 2% quarter-over-quarter. The company’s strategic shift toward platform solutions continues, with Platform ARR growing 17% year-over-year to $234.7 million, while Non-Platform ARR declined 3% to $479.9 million.

The following table shows the evolution of Software ARR composition:

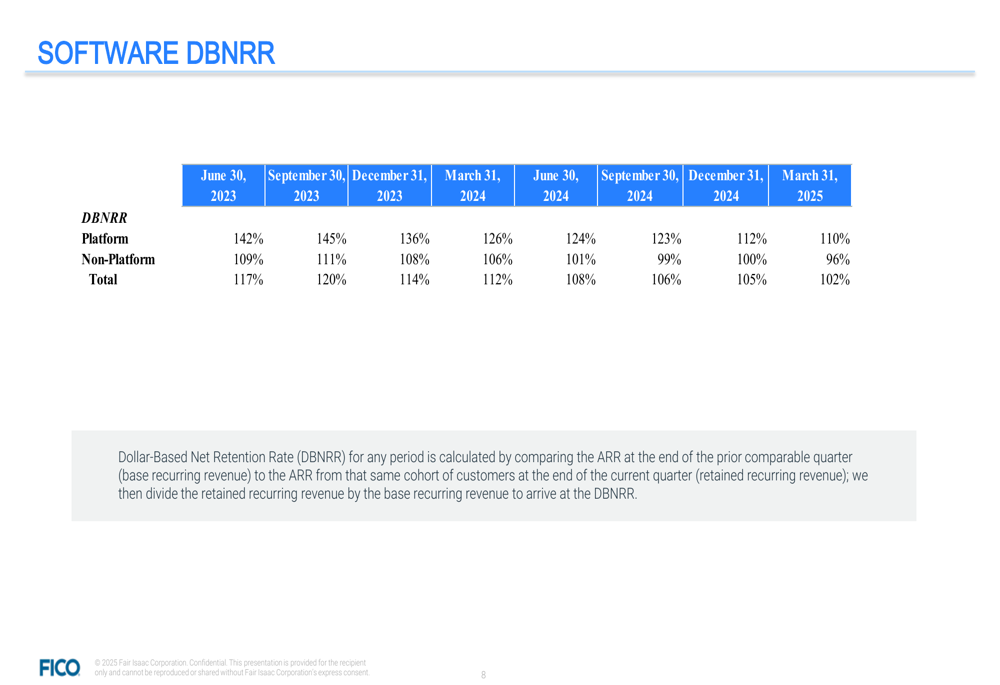

Dollar-Based Net Retention Rate (DBNRR), a key metric for subscription businesses, has been on a declining trend, reaching 102% overall compared to 112% a year ago. Platform DBNRR remains stronger at 110%, while Non-Platform DBNRR has fallen below 100% to 96%, indicating some challenges in retaining and expanding existing customer relationships.

As shown in the following DBNRR trend analysis:

Despite these challenges, Software ACV Bookings showed improvement at $21.8 million, up 30% year-over-year and 3% quarter-over-quarter, suggesting potential for future growth.

Financial Position

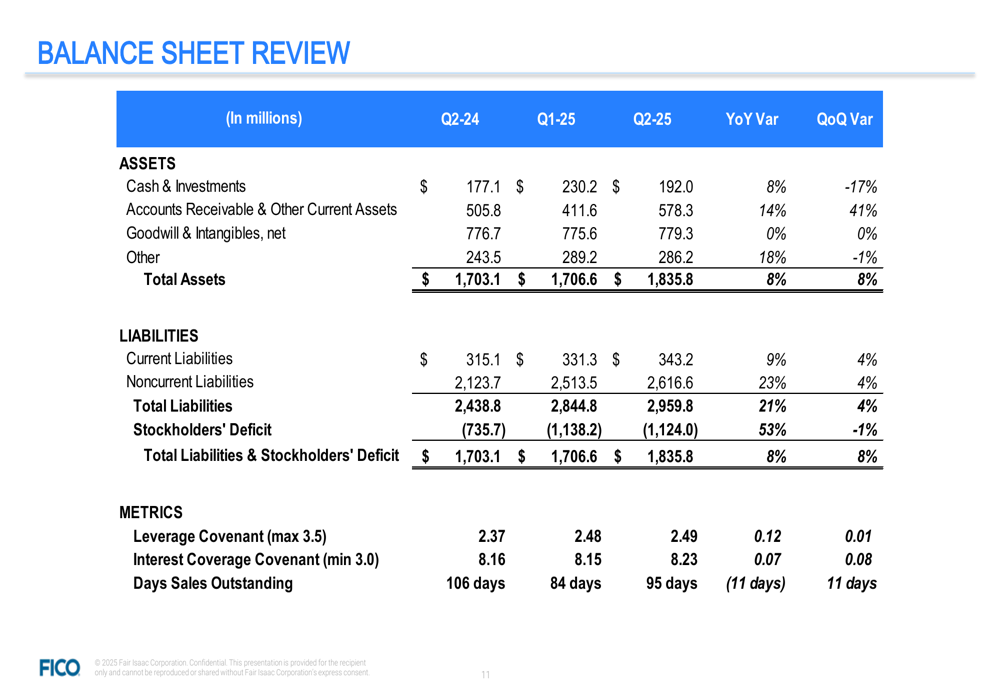

FICO’s balance sheet remains solid with cash and investments of $192.0 million as of Q2 2025, up 8% year-over-year but down 17% from the previous quarter. Total assets increased to $1,835.8 million, up 8% both year-over-year and quarter-over-quarter.

The company’s leverage covenant stands at 2.49, well below the maximum allowed 3.5, while interest coverage is strong at 8.23, comfortably above the minimum requirement of 3.0.

The following balance sheet summary provides a comprehensive view of FICO’s financial position:

Free cash flow for Q2 2025 was $65.5 million, slightly up from $61.6 million in Q2 2024 but significantly lower than the $186.8 million generated in Q1 2025. This quarterly fluctuation is illustrated in the following chart:

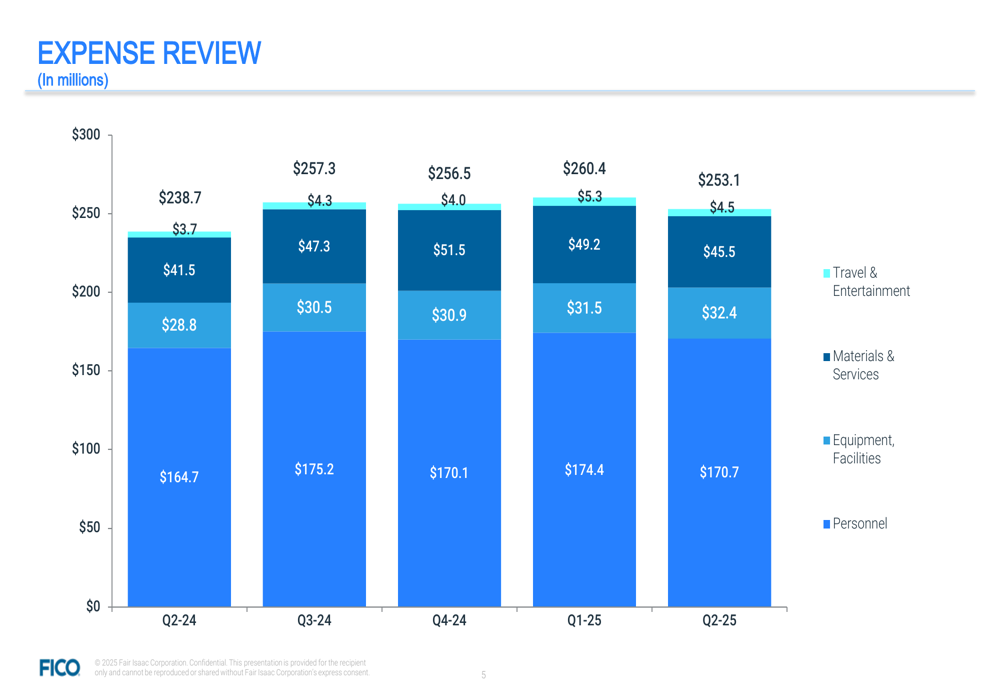

Expense Management

FICO has maintained disciplined expense management, with total expenses of $253.1 million in Q2 2025, down from $260.4 million in Q1 2025. Personnel costs, which represent the largest expense category, decreased to $170.7 million from $174.4 million in the previous quarter.

The expense breakdown over time is illustrated in the following chart:

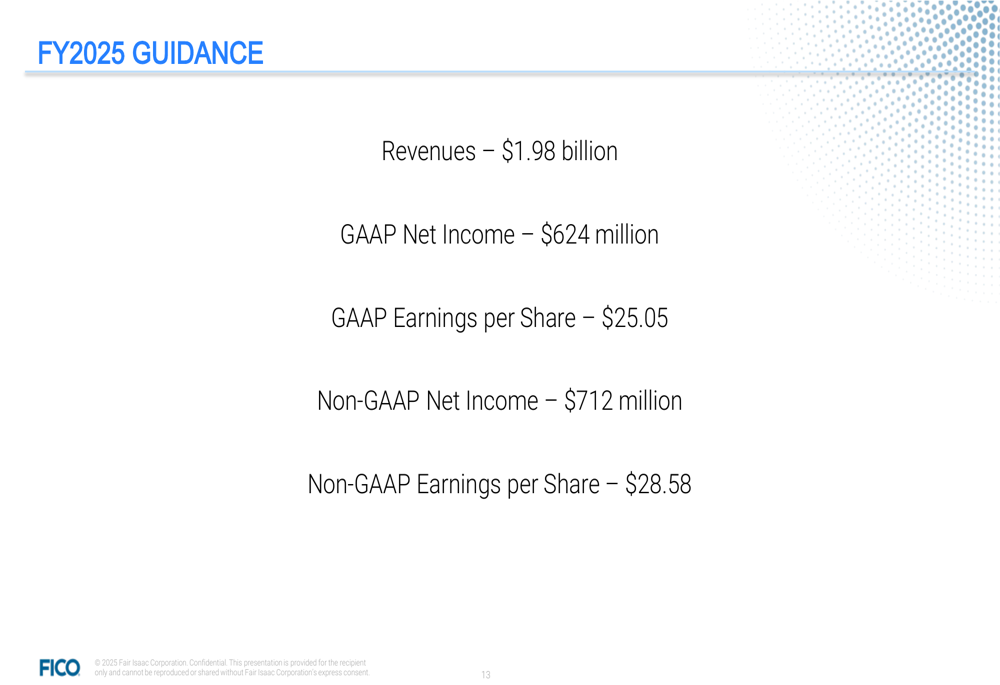

Forward Guidance

Despite the strong Q2 performance, FICO has maintained its fiscal year 2025 guidance rather than raising it. The company expects:

- Revenues of $1.98 billion

- GAAP Net Income of $624 million

- GAAP Earnings per Share of $25.05

- Non-GAAP Net Income of $712 million

- Non-GAAP Earnings per Share of $28.58

Conclusion

FICO’s Q2 2025 results demonstrate a strong recovery from its Q1 disappointment, primarily driven by exceptional performance in the Scores segment, particularly in mortgage and auto originations. The contrast between the booming Scores business and the more modest Software segment highlights the company’s current growth dynamics.

While the company maintains a solid financial position and has shown impressive profitability improvements, the declining trends in Software DBNRR and Non-Platform ARR suggest potential challenges in parts of the business. Nevertheless, the maintained full-year guidance indicates management’s confidence in sustaining overall performance through the remainder of fiscal year 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.