S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Five9 Inc (NASDAQ:FIVN) released its Q2 2025 investor presentation on July 31, 2025, highlighting 12% year-over-year revenue growth and significant traction in its artificial intelligence offerings. Despite posting solid operational results, including an all-time high adjusted EBITDA margin of 24%, the company’s stock declined 5.28% in regular trading to $27.27, with minimal movement in after-hours trading.

The cloud contact center provider continues to execute on its enterprise-focused strategy while positioning AI capabilities as a key growth driver. Five9’s presentation comes amid increasing competition in the Contact Center as a Service (CCaaS) market, where cloud migration and AI integration have become critical differentiators.

Quarterly Performance Highlights

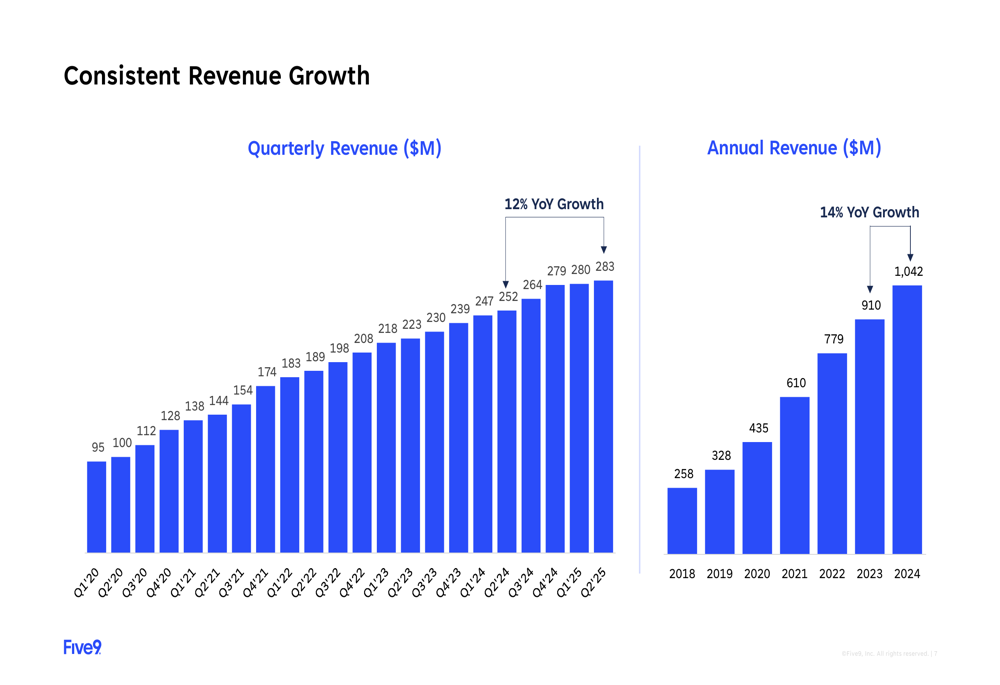

Five9 reported Q2 2025 revenue of $283 million, representing 12% year-over-year growth. Subscription revenue, which constitutes 81% of total revenue, grew at a faster 16% rate, demonstrating the company’s success in building a recurring revenue base.

As shown in the following chart of quarterly and annual revenue growth, Five9 has maintained consistent expansion over the past five years:

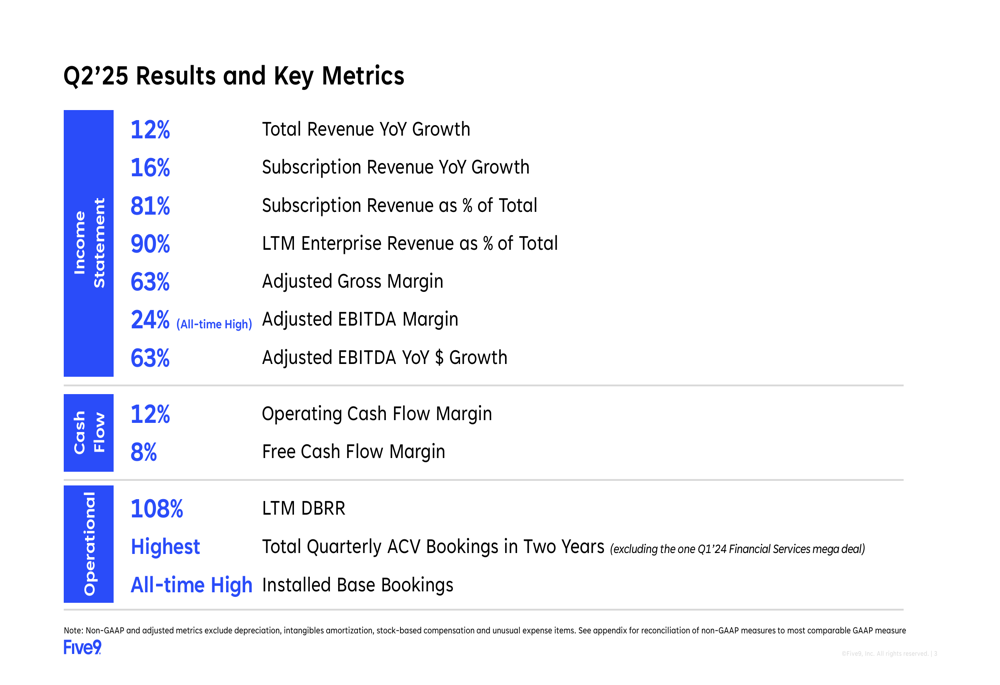

The company achieved an adjusted EBITDA margin of 24% in Q2 2025, an all-time high, with adjusted EBITDA dollar growth of 63% year-over-year. This substantial improvement in profitability reflects Five9’s increasing operational efficiency and scale. Other key financial metrics included:

- Adjusted gross margin of 63%

- Operating cash flow margin of 12%

- Free cash flow margin of 8%

- LTM dollar-based retention rate (DBRR) of 108%

The following slide summarizes these key financial and operational metrics:

AI Strategy and Customer Success

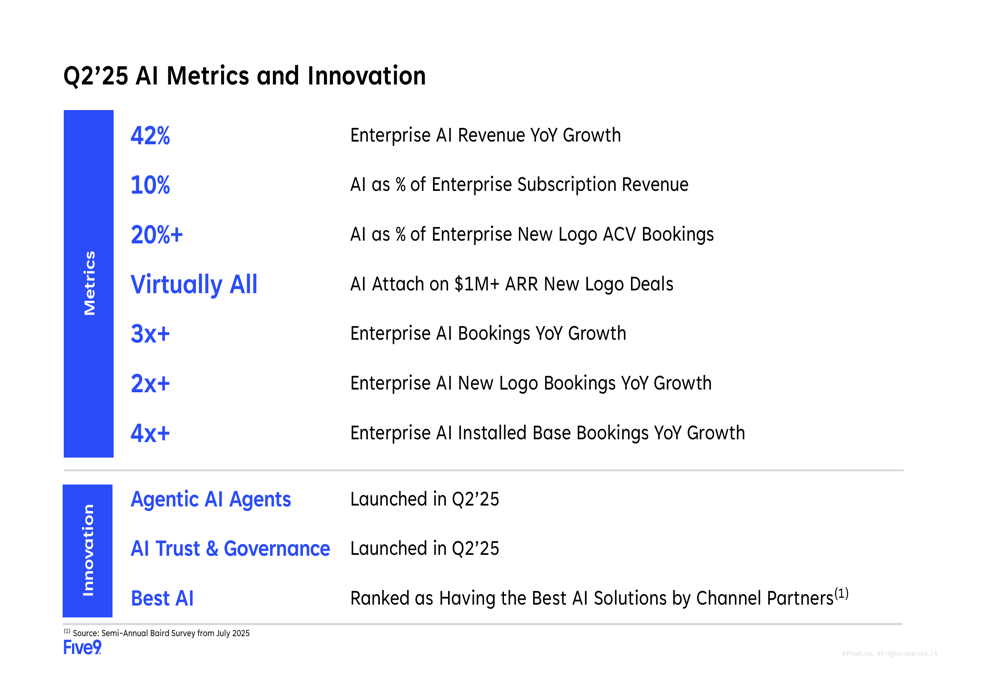

Five9’s AI business showed remarkable momentum in Q2 2025, with enterprise AI revenue growing 42% year-over-year. AI now represents 10% of enterprise subscription revenue and over 20% of enterprise new logo annual contract value (ACV) bookings. The company reported that virtually all new deals exceeding $1 million in annual recurring revenue (ARR) included AI components.

The following slide details Five9’s AI metrics and recent innovations:

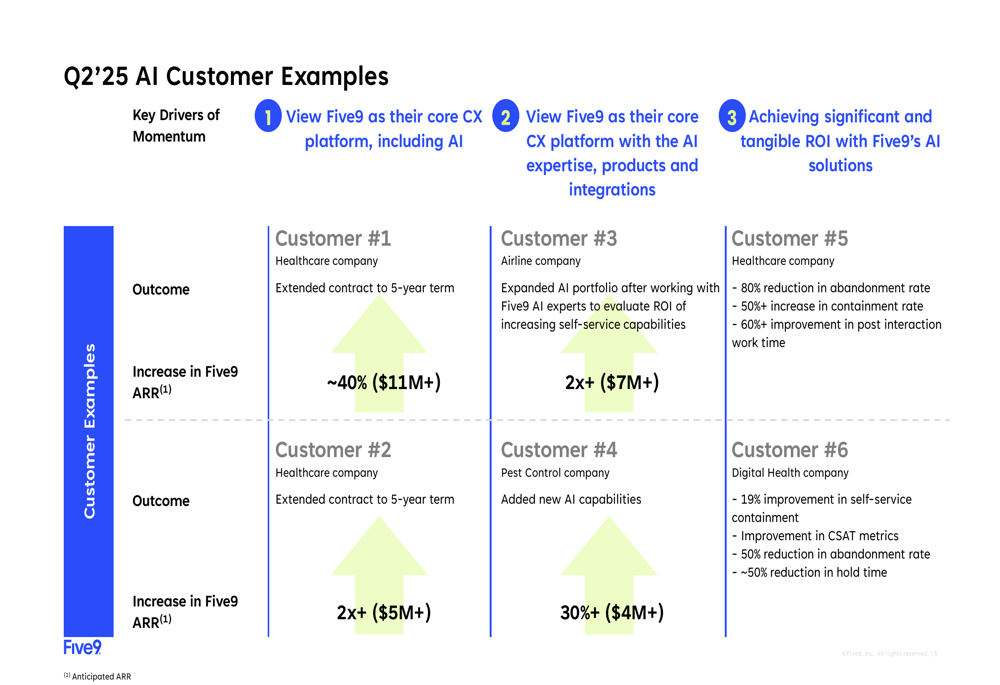

The company highlighted several customer success stories demonstrating the impact of its AI solutions. For example, a healthcare company extended its contract to a 5-year term with a 40% increase in ARR to over $11 million, while an airline company expanded its AI portfolio resulting in more than doubling its ARR to over $7 million.

These customer examples illustrate tangible ROI metrics, including an 80% reduction in abandonment rate for one healthcare company and a 50% improvement in containment rate for another:

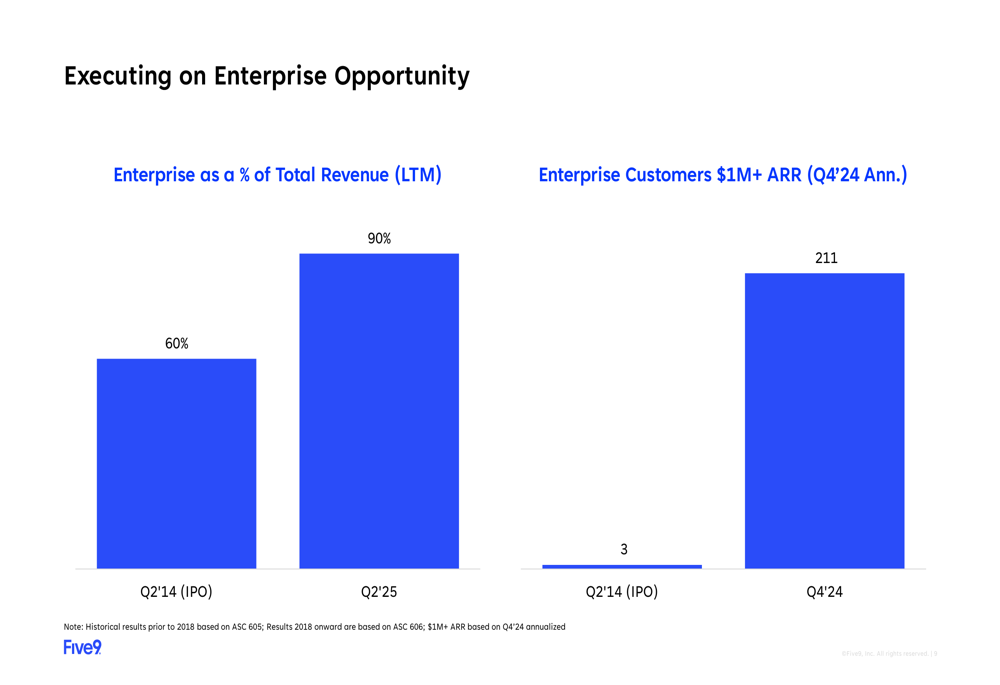

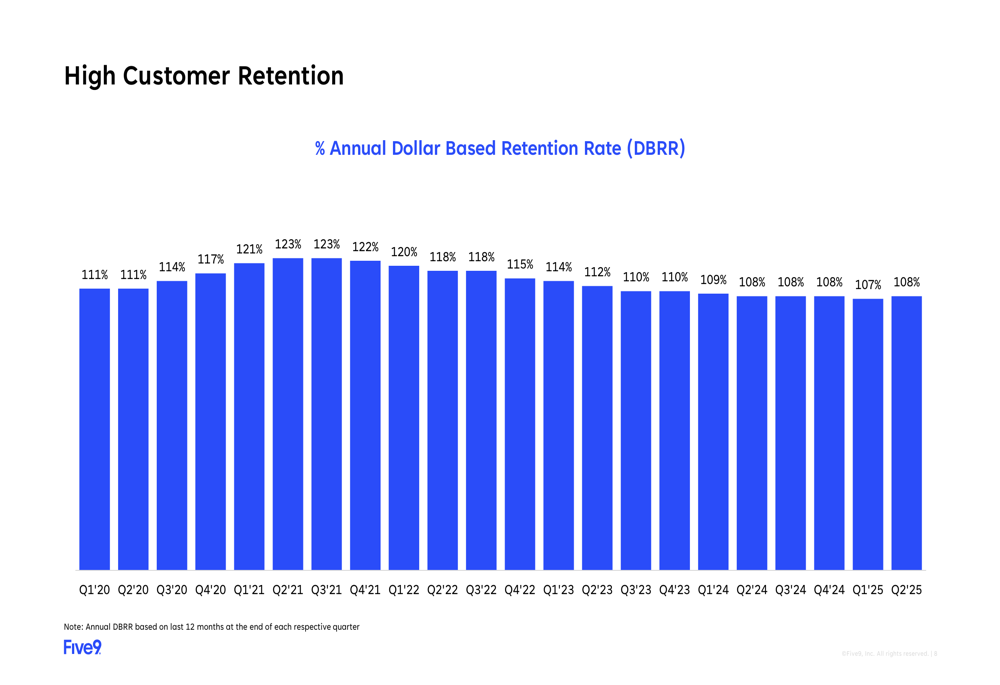

Enterprise Focus and Customer Retention

Five9 continues to successfully execute its enterprise-focused strategy, with large enterprise customers now representing 90% of total revenue, up from 60% at the time of the company’s IPO. The number of customers with over $1 million in ARR has grown dramatically from just 3 at IPO to 211 as of Q4 2024.

The following chart illustrates this strategic shift toward enterprise customers:

Customer retention remains strong, with a dollar-based retention rate of 108% for the trailing twelve months ending Q2 2025. This metric indicates that existing customers are not only staying with Five9 but also expanding their usage over time:

The company highlighted several significant customer wins and expansions in Q2, including a global data and analytics company with anticipated ARR of $3.3 million, a business unit of a Fortune 50 financial services company with anticipated ARR of $2.8 million, and a leading academic health system that expanded its partnership with a new five-year agreement adding $3.0 million in ARR.

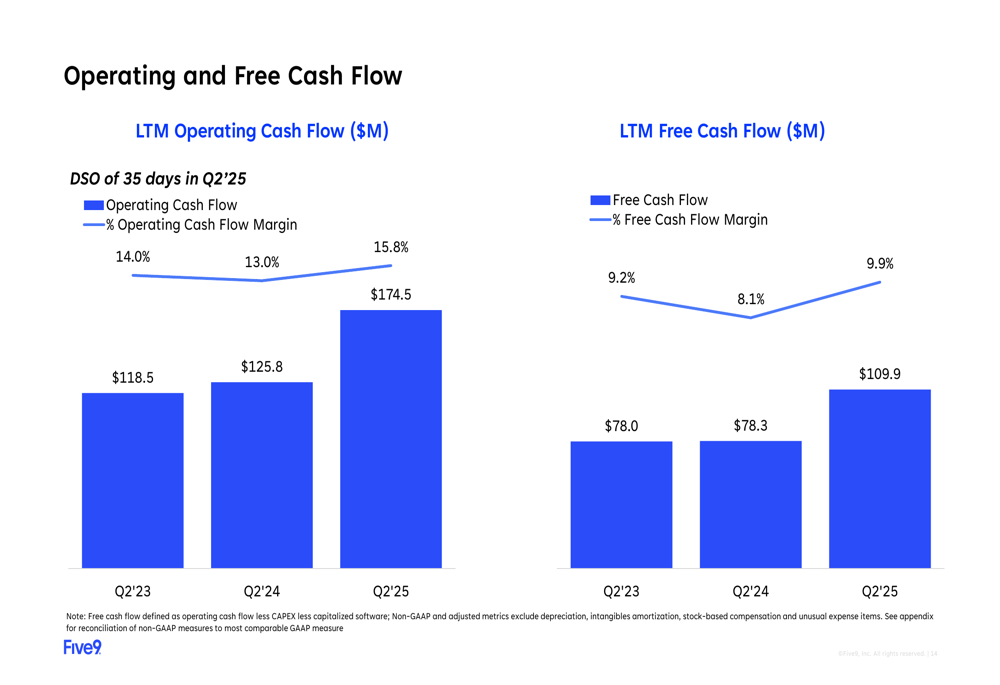

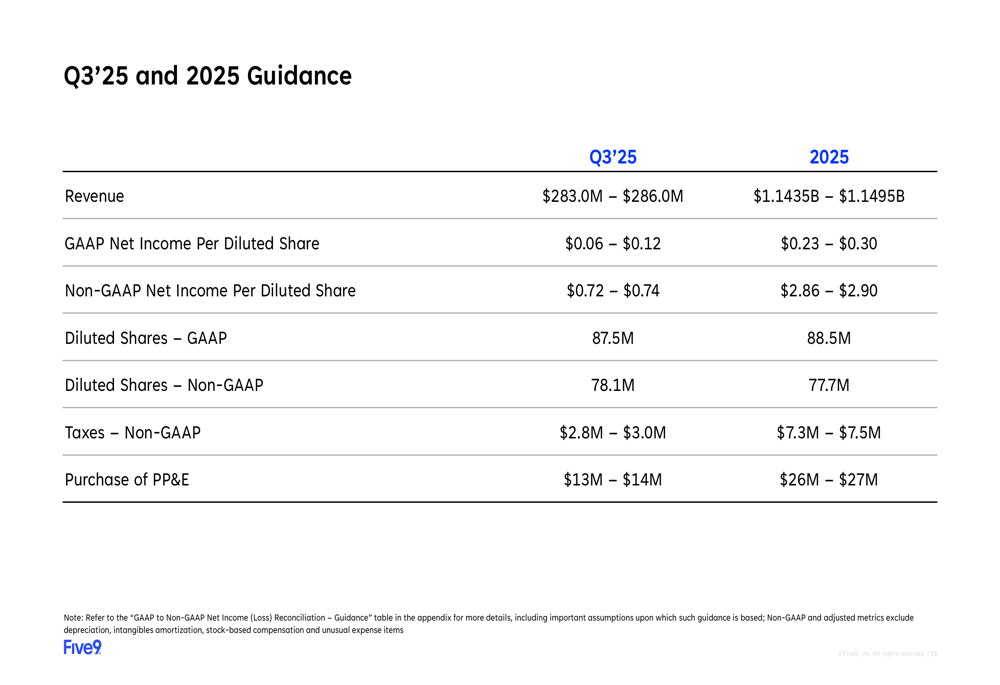

Financial Position and Guidance

Five9’s balance sheet as of June 30, 2025, showed $635.9 million in cash, cash equivalents, and marketable investments, down from $1,006.0 million at the end of 2024. Total (EPA:TTEF) debt decreased to $733.6 million from $1,165.3 million during the same period. The company noted that it has fulfilled notes worth $434.4 million in cash, with the remaining principal amount of $747.5 million due in March 2029.

The company’s operating cash flow and free cash flow continue to improve, as illustrated in the following chart:

For Q3 2025, Five9 provided revenue guidance of $283.0-286.0 million and non-GAAP net income per diluted share of $0.72-0.74. For the full year 2025, the company expects revenue of $1.1435-1.1495 billion and non-GAAP net income per diluted share of $2.86-2.90.

The following slide details the company’s guidance for Q3 and full-year 2025:

Forward-Looking Statements

Five9 outlined its medium-term operating model, projecting revenue growth of 10-15% by 2027, up from the current 12%. The company expects adjusted gross margins to improve from the current 63% to 66-68%+ and adjusted EBITDA margins to increase from 24% to 25-30%+ by 2027.

The company sees significant market opportunity, estimating its total addressable market at $234 billion, including $24 billion for cloud contact center software and $210 billion for contact center labor spend. Five9 believes AI will be a key driver of TAM expansion.

Five9 continues to focus on balancing growth and profitability, with a target of achieving "Rule of 40+" (the sum of revenue growth rate and profit margin exceeding 40%) by 2027. The company also expects ongoing decline in stock-based compensation as a percentage of revenue, which has already decreased from 18% in Q1 2024 to 15% in Q2 2025.

As Five9 navigates a competitive landscape and macroeconomic uncertainties, its strong enterprise customer base, high retention rates, and growing AI capabilities position the company to capitalize on the ongoing digital transformation in the contact center industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.