Ukraine proposes $100 bln US weapons deal for security guarantees - FT

Introduction & Market Context

Flowers Foods, Inc. (NYSE:FLO) released its second quarter 2025 financial results on August 15, 2025, showing modest sales growth driven primarily by acquisition while facing profitability challenges in a difficult consumer environment. The stock reacted negatively in pre-market trading, declining 3.44% to $16.01, continuing a downward trend that has seen the share price approach its 52-week low of $15.27.

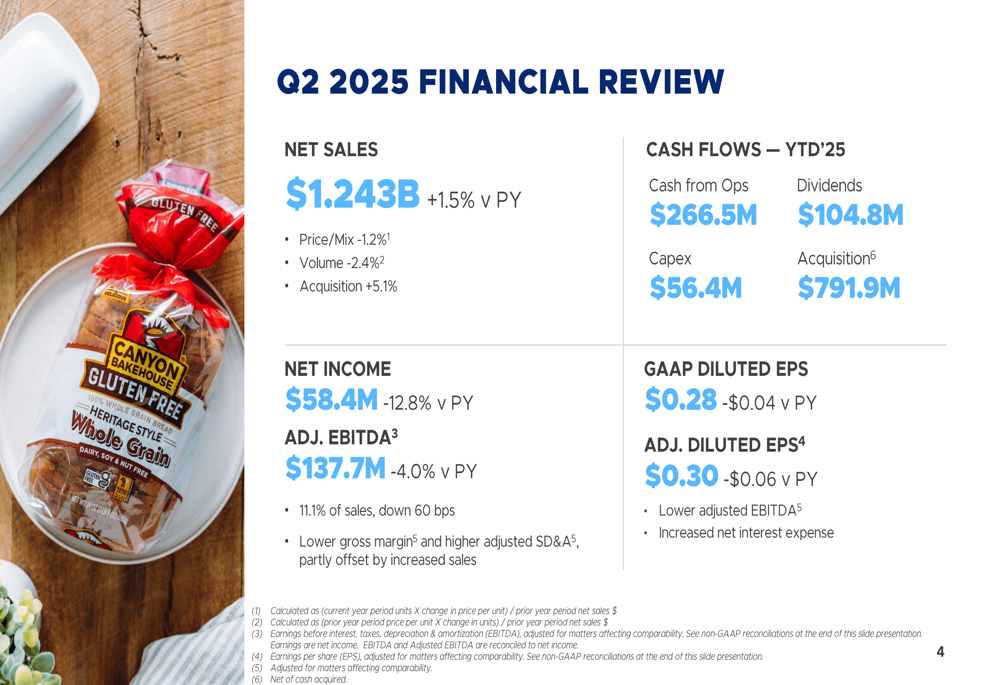

The bakery products company reported net sales growth of 1.5% to $1.243 billion, but saw net income decline by 12.8% to $58.4 million compared to the same period last year. The results reflect ongoing challenges in the bread category and shifting consumer preferences that have pressured traditional segments.

Quarterly Performance Highlights

Flowers Foods’ second quarter results showed mixed performance across key metrics. While the Simple Mills acquisition contributed 5.1% to sales growth, this was largely offset by a 2.4% volume decline and a 1.2% negative price/mix impact.

As shown in the following financial overview slide, adjusted EBITDA decreased 4.0% to $137.7 million, representing 11.1% of sales, a 60 basis point decline from the prior year:

The company’s adjusted diluted earnings per share fell to $0.30, down from $0.36 in the prior-year period, primarily due to lower adjusted EBITDA and increased net interest expense related to the Simple Mills acquisition. GAAP diluted EPS was $0.28, compared to $0.32 in Q2 2024.

Detailed Financial Analysis

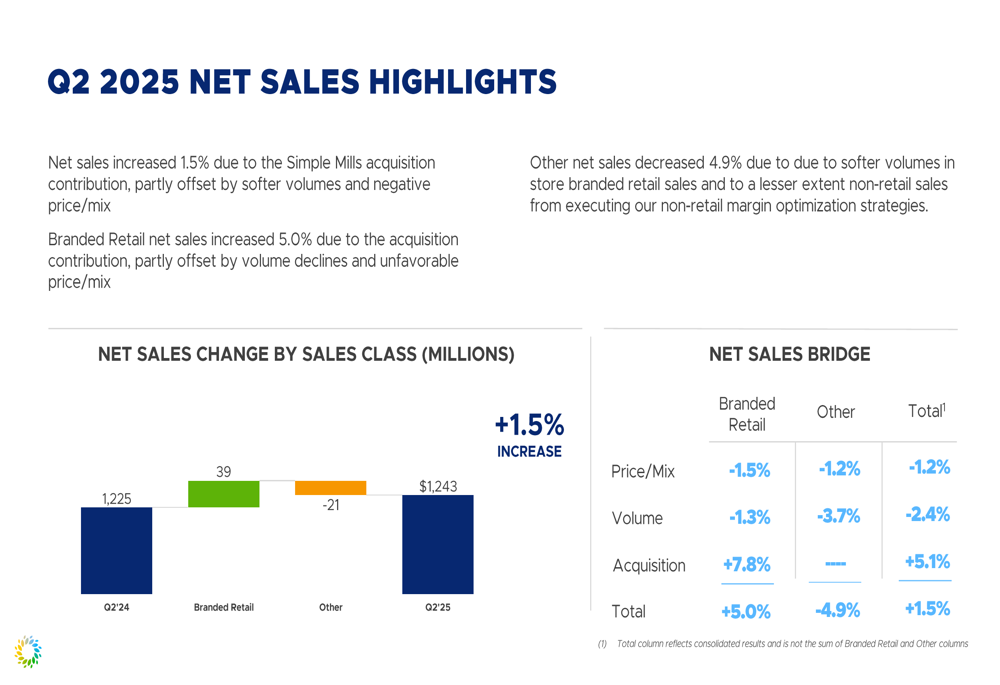

Breaking down the sales performance, Flowers Foods’ branded retail segment showed 5.0% growth, driven by the Simple Mills acquisition contribution of 7.8%, which helped offset a 1.3% volume decline and 1.5% negative price/mix impact. The "Other" segment, which includes store-branded retail and foodservice products, decreased 4.9%, with volume down 3.7% and price/mix down 1.2%.

The following chart illustrates the components of the company’s net sales change:

Profitability metrics showed pressure across the board, with gross margin excluding depreciation and amortization declining due to greater outside purchases of product, higher workforce-related and rent costs, and lower production volumes. The following slide highlights the adjusted EBITDA performance:

Strategic Initiatives

Flowers Foods emphasized several strategic priorities aimed at navigating the challenging environment. The company highlighted its portfolio strategy, which has driven solid relative performance led by unit share gains for Dave’s Killer Bread, Wonder, and Canyon Bakehouse brands.

As shown in the key messages slide, the company is focusing on a deep innovation pipeline targeting significant opportunities in faster-growing categories and adjacencies to mitigate category weakness:

The acquisition of Simple Mills represents a significant strategic move to expand into premium, health-focused categories with stronger growth potential. This aligns with the company’s efforts to offset weakness in traditional bread segments by building presence in higher-margin specialty categories.

Competitive Industry Position

Despite category headwinds, Flowers Foods has maintained or improved its position in key growth segments. The company’s share of the organic bread category stands at 73.9%, though slightly down from its peak of 74.2% in FY 2023. Meanwhile, its share of the gluten-free category has continued to improve, reaching 38.2% in the latest 52-week period.

The overall branded versus store brand market share trends show the impact of inflationary pressures on consumers, with branded dollar share declining from 76.2% in FY 2020 to 73.9% in the latest period, while store branded share has increased from 23.8% to 26.1% during the same timeframe.

Flowers’ bread dollar share has remained relatively stable at 16.6% in Q2 2025, while its cake dollar share improved to 6.3%, showing a recovery in the cake segment after several challenging quarters. The company’s commercial cake business showed positive growth in Q2 2025, with dollar sales up 3.6% and unit sales up 4.2%, a significant improvement after several quarters of decline.

Forward-Looking Statements

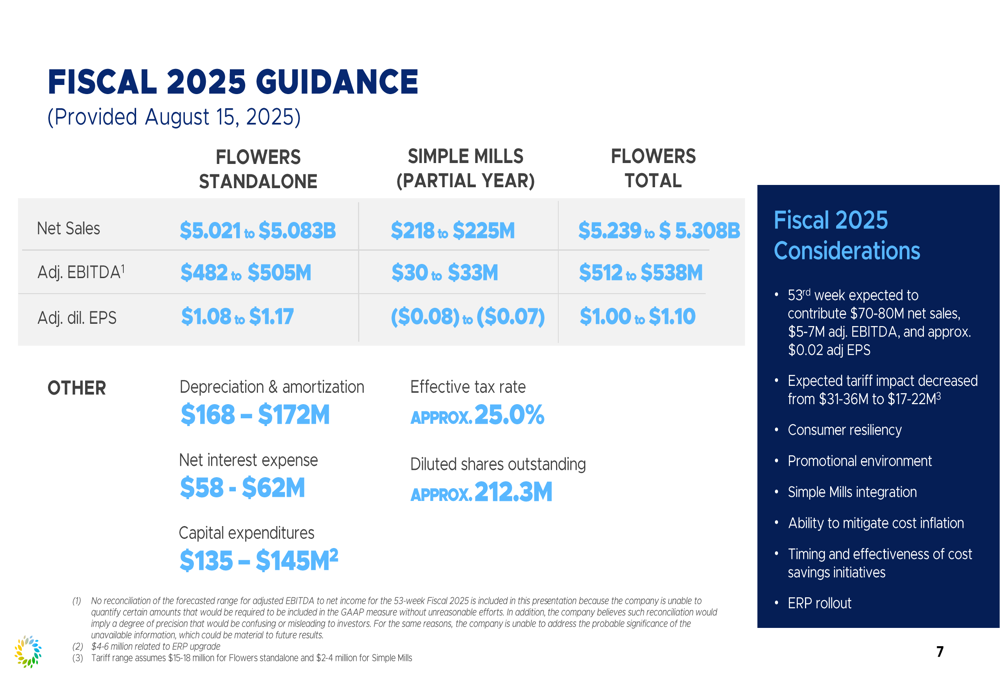

Flowers Foods adjusted its fiscal 2025 guidance to reflect the challenging operating environment. The updated outlook incorporates both the standalone business and the partial-year contribution from Simple Mills:

The revised guidance reflects softness in traditional loaf sales and a more intense competitive environment. For the total company, Flowers now expects net sales of $5.239 to $5.308 billion, adjusted EBITDA of $512 to $538 million, and adjusted diluted EPS of $1.00 to $1.10.

The company’s long-term growth targets continue to face pressure, with the FY 2025 CAGR for net sales (3.4%), adjusted EBITDA (2.6%), and adjusted diluted EPS (2.7%) all falling below the long-term targets of 1-2%, 4-6%, and 7-9%, respectively.

Executive Summary

Flowers Foods’ Q2 2025 results reflect the ongoing challenges in the bread category, with growth primarily driven by acquisition rather than organic performance. While the company has successfully maintained or improved its position in premium segments like organic and gluten-free, traditional categories continue to face pressure from changing consumer preferences and economic headwinds.

The acquisition of Simple Mills represents a strategic pivot toward faster-growing, premium categories, but integration costs and increased interest expense have pressured near-term profitability. Management’s adjusted guidance acknowledges the difficult operating environment, with a focus on innovation and portfolio optimization to drive future growth.

With the stock trading near its 52-week low, investors appear concerned about the company’s ability to navigate these challenges and return to stronger organic growth. However, Flowers Foods’ strong position in specialty categories and ongoing portfolio transformation provide potential pathways to improved performance as consumer trends evolve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.