Gold prices suffer profit taking ahead of likely Fed cut; PCE inflation due

Introduction & Market Context

Flowserve Corporation (NYSE:FLS) reported strong first quarter 2025 results on April 30, showcasing robust performance across key metrics despite emerging tariff challenges. The pump and flow control equipment manufacturer delivered solid revenue growth and significant margin expansion, while maintaining its full-year guidance despite an increasingly complex global trade environment.

The company is navigating a mixed market landscape, with healthy demand in energy and power sectors offsetting some softness in chemicals. Notably, Flowserve is confronting substantial tariff headwinds, particularly from China (145% tariffs), Canada and Mexico (25%), and the European Union (10%), which the company estimates could have a $90-100 million annualized gross impact before mitigating actions.

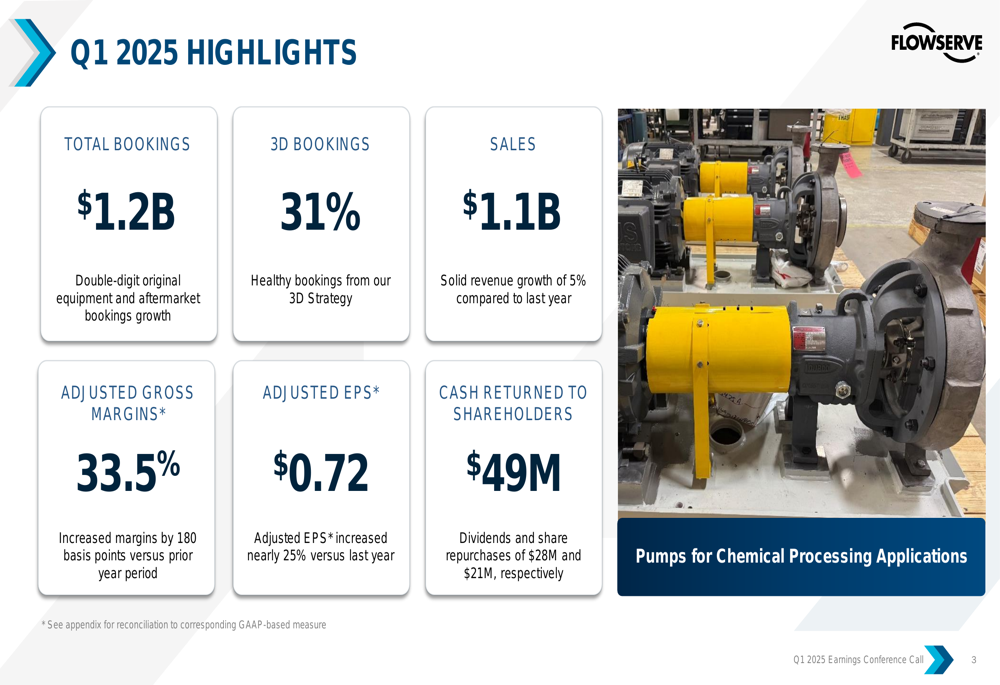

As shown in the following quarterly highlights slide, Flowserve delivered impressive financial results across key metrics:

Quarterly Performance Highlights

Flowserve reported total bookings of $1.2 billion in Q1 2025, representing double-digit growth in both original equipment and aftermarket segments. The company achieved sales of $1.1 billion, reflecting a 5% increase compared to the prior year period. Adjusted gross margins expanded to 33.5%, up 180 basis points year-over-year, while adjusted EPS reached $0.72, nearly 25% higher than Q1 2024.

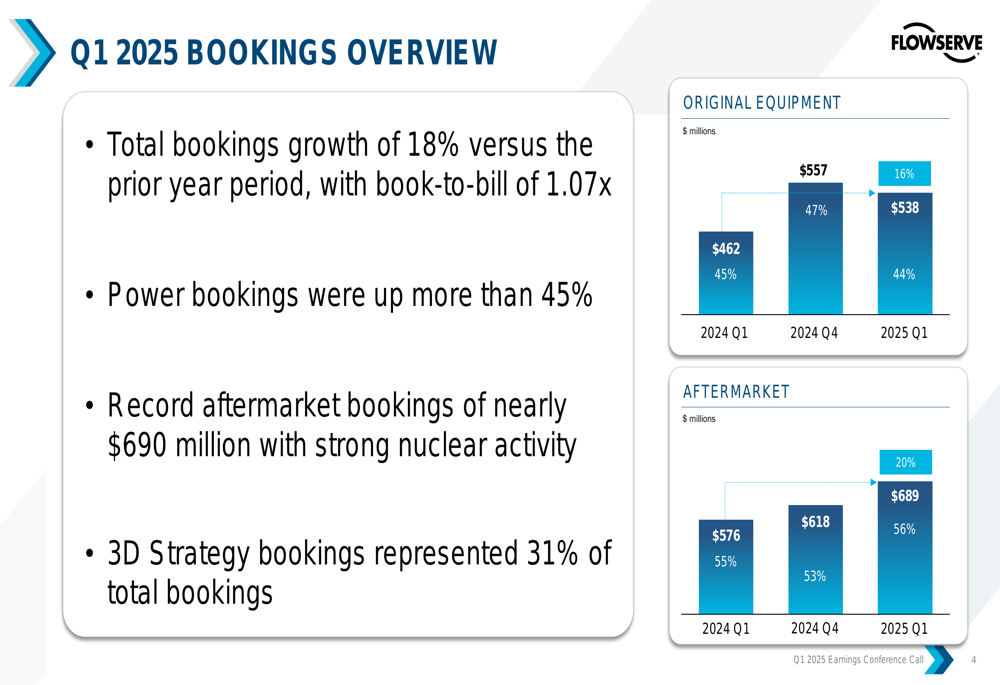

The company’s bookings performance was particularly strong, with 18% overall growth versus the prior year and a book-to-bill ratio of 1.07x. Power sector bookings increased by more than 45%, while aftermarket bookings reached a record level of nearly $690 million, supported by strong nuclear activity. The company’s strategic 3D initiatives represented 31% of total bookings.

The following slide illustrates Flowserve’s bookings performance across original equipment and aftermarket segments:

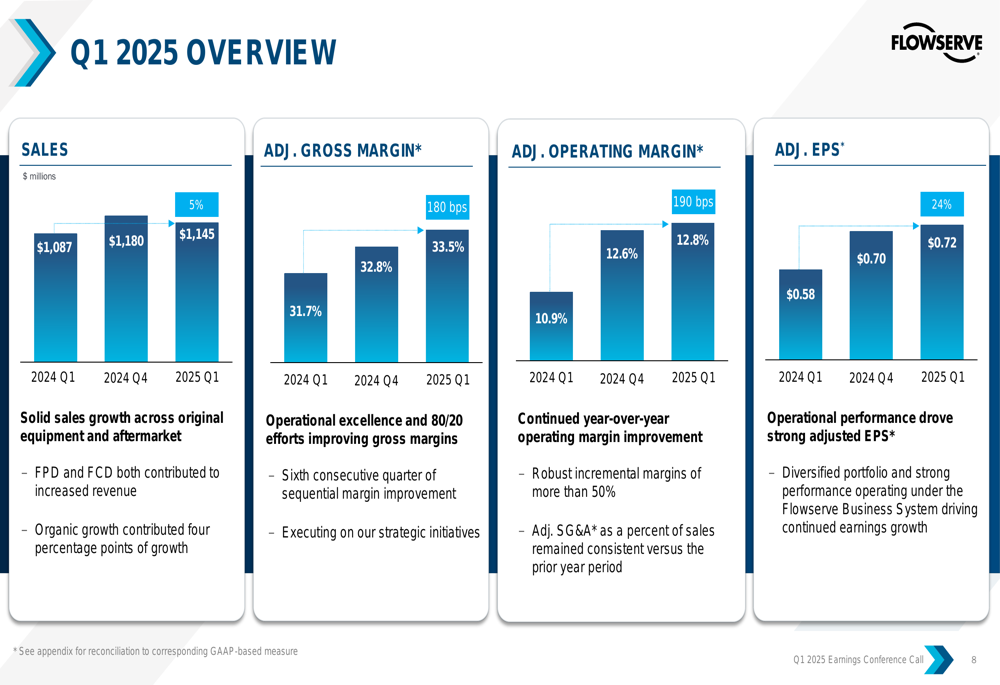

Flowserve’s financial overview demonstrates consistent improvement across key metrics, with the first quarter marking the sixth consecutive quarter of sequential margin improvement. The company achieved robust incremental margins exceeding 50%, driving strong earnings growth.

Segment Performance

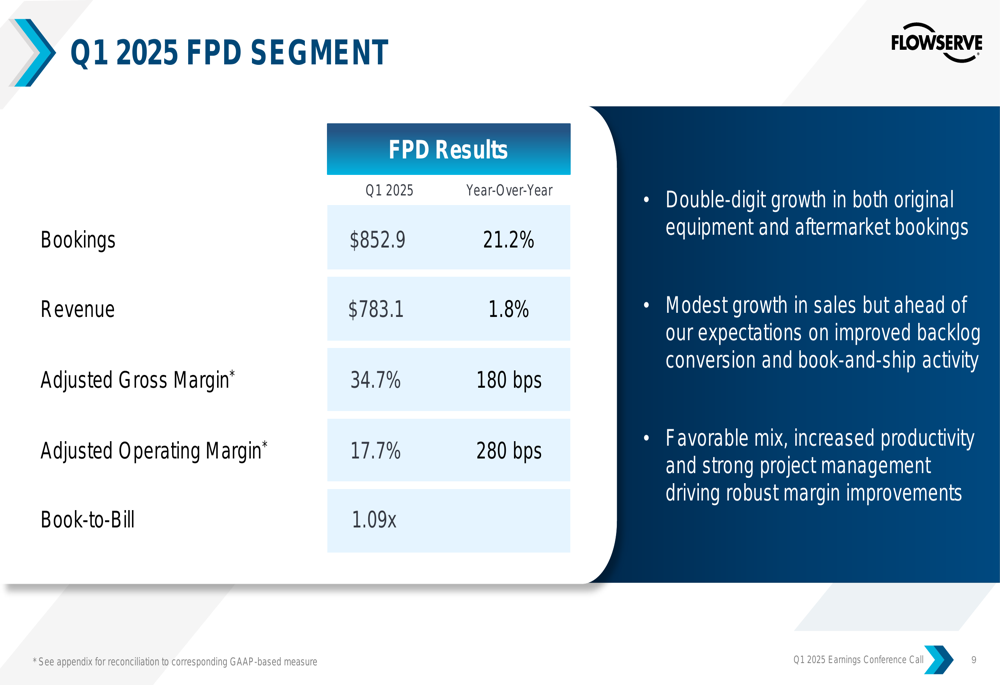

Flowserve’s Pumps Division (FPD) delivered exceptional results in Q1 2025, with bookings of $852.9 million representing a 21.2% increase year-over-year. While revenue growth was more modest at 1.8%, reaching $783.1 million, the segment achieved significant margin expansion with adjusted gross margin improving 180 basis points to 34.7% and adjusted operating margin increasing 280 basis points to 17.7%.

The following slide details the FPD segment’s performance metrics:

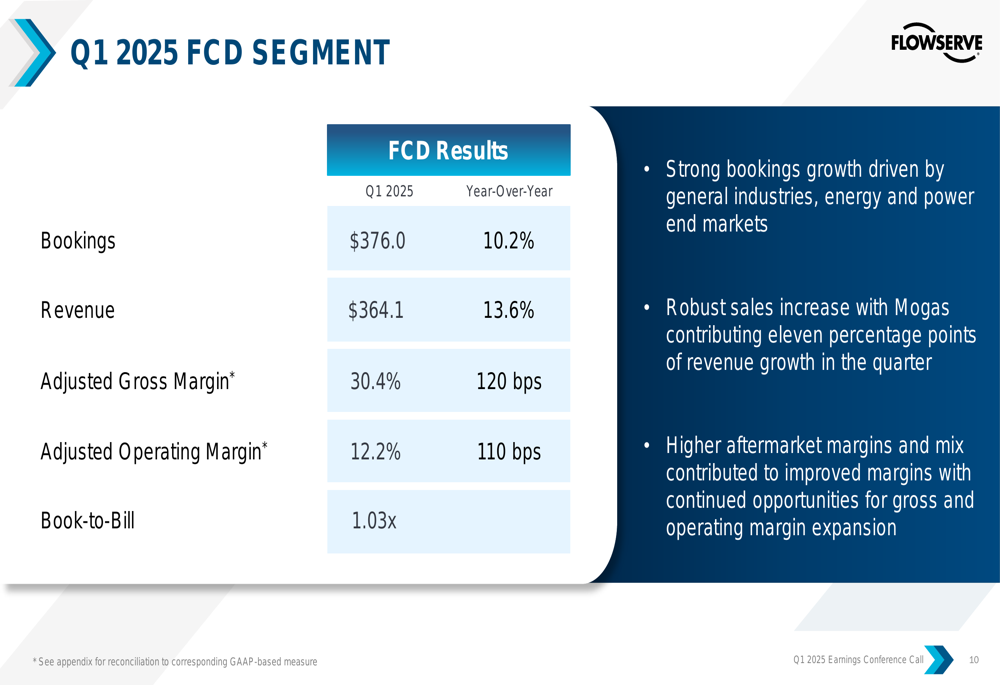

The Flow Control Division (FCD) also performed well, with bookings of $376.0 million, up 10.2% compared to Q1 2024. Revenue increased by 13.6% to $364.1 million, with Mogas contributing eleven percentage points of growth. Adjusted gross margin improved 120 basis points to 30.4%, while adjusted operating margin expanded 110 basis points to 12.2%.

Strategic Initiatives

Flowserve is leveraging its Business System framework to drive operational improvements and navigate market volatility. The company’s Portfolio Excellence program, based on the 80/20 principle, is showing early success with approximately 80% SKU reduction at one of its pump division sites. Management expects all product revenue to utilize the 80/20 framework by mid-year, with minimal revenue impact but gross margin benefits of at least 50 basis points for the full year.

The company is implementing several strategies to mitigate tariff impacts, including pricing actions, shifting to alternative sourcing, leveraging its regional structure, and accelerating its CORE framework. Flowserve’s global manufacturing footprint, with only about one-third of facilities in North America, provides some natural hedging against tariff pressures.

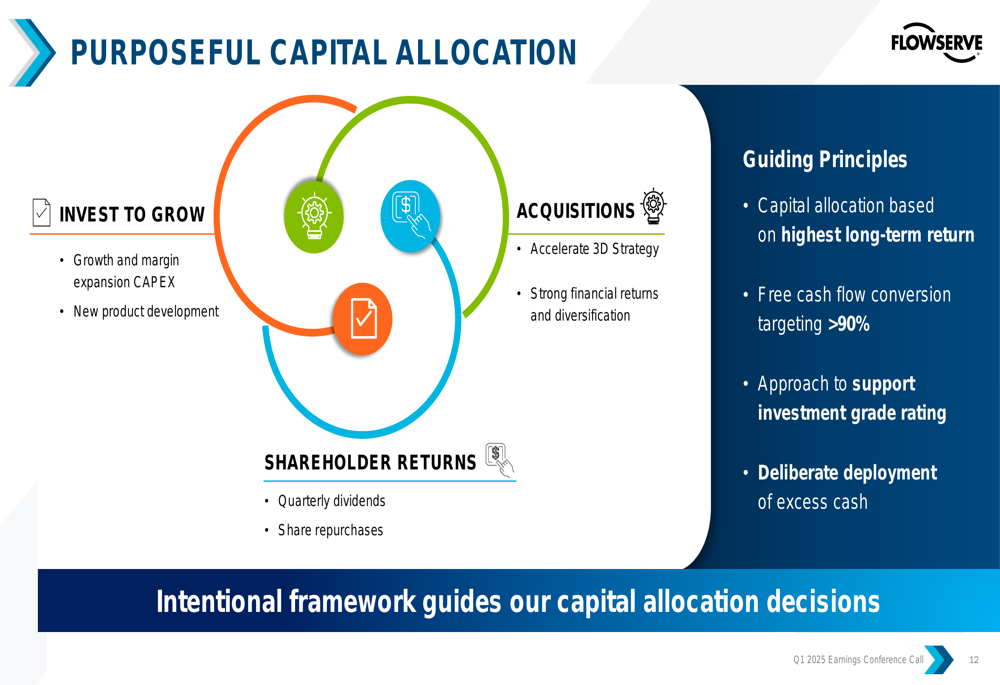

Flowserve’s capital allocation strategy remains focused on balancing growth investments, shareholder returns, and strategic acquisitions:

The company returned $49 million to shareholders in Q1 2025 through dividends ($28 million) and share repurchases ($21 million), representing an increase from the prior year period.

Market Outlook & Forward Guidance

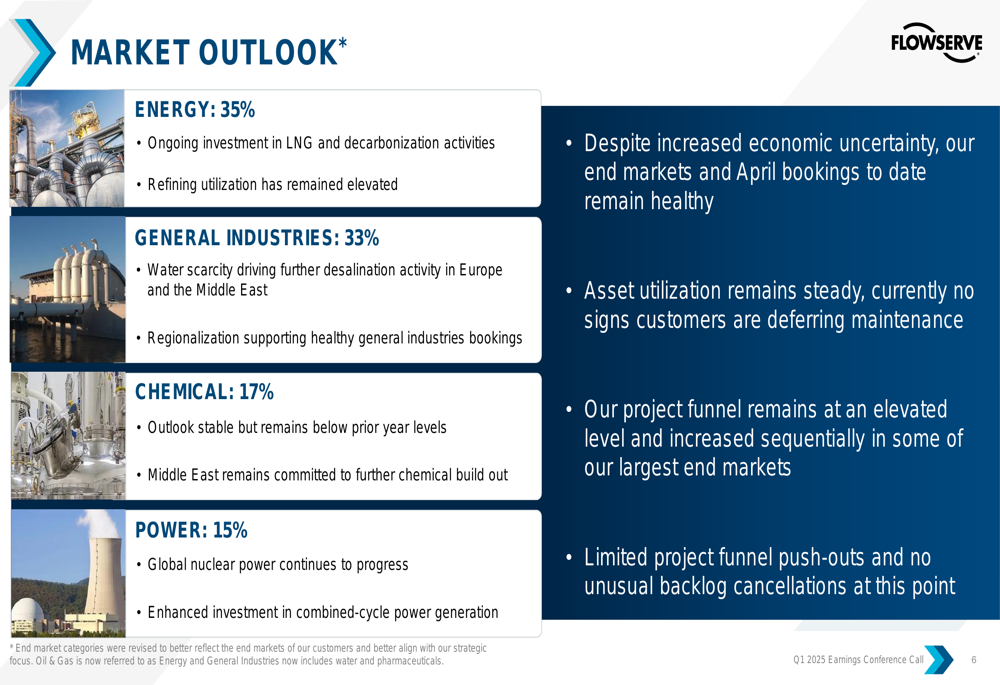

Flowserve provided a detailed market outlook across its key industry segments. The energy sector (35% of business) continues to see investment in LNG and decarbonization activities, while general industries (33%) are driven by water scarcity and regionalization trends. The chemical sector (17%) remains stable but below prior year levels, and the power sector (15%) is benefiting from nuclear power development and investment in combined-cycle generation.

Despite first quarter cash flow challenges, with operations using $50 million due to higher temporary working capital requirements, management expects significant improvements throughout the remainder of the year, targeting full-year cash flow to adjusted net earnings of 90% or more.

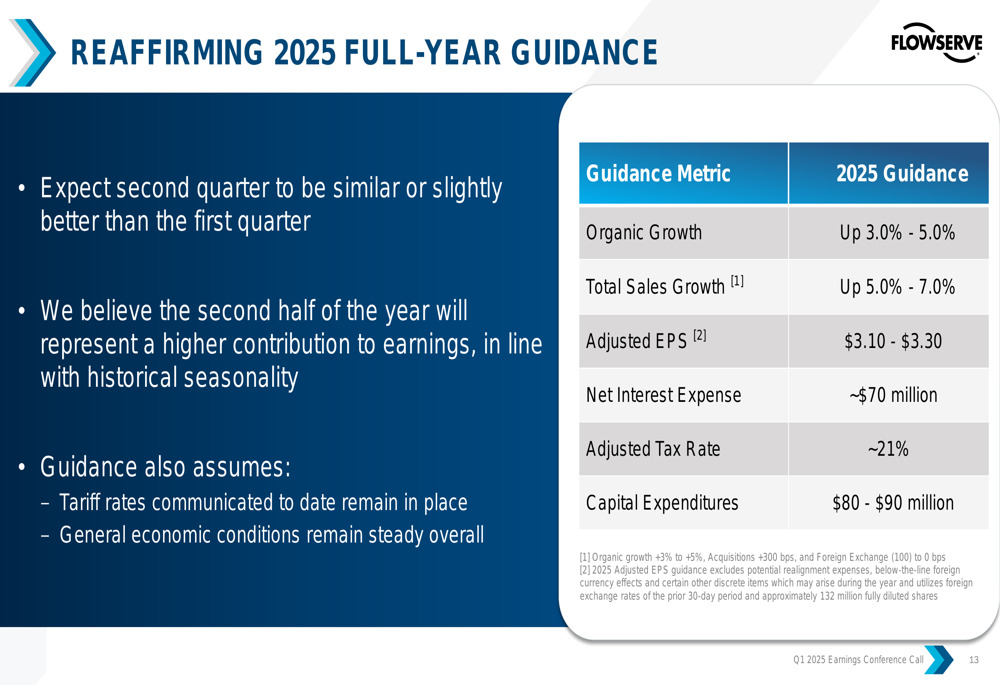

Flowserve reaffirmed its full-year 2025 guidance, expecting the second quarter to be similar or slightly better than the first quarter, with a stronger second half in line with historical seasonality. The guidance assumes that current tariff rates remain in place and general economic conditions stay relatively steady.

Conclusion

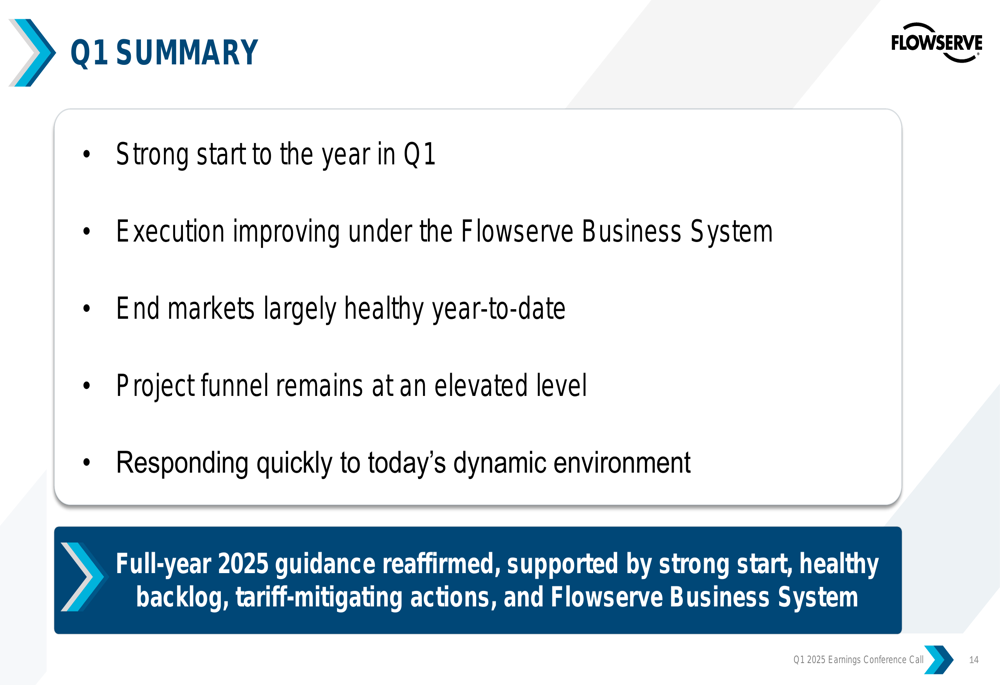

Flowserve delivered a strong start to 2025, with impressive bookings growth, margin expansion, and earnings improvement. The company’s execution under the Flowserve Business System is yielding tangible results, enabling it to navigate tariff headwinds while maintaining its full-year outlook.

Management expressed confidence in the health of its end markets, noting that the project funnel remains at an elevated level with limited push-outs and no unusual backlog cancellations. With a book-to-bill ratio above 1.0 and record aftermarket bookings, Flowserve appears well-positioned to deliver on its 2025 financial targets despite the challenging global trade environment.

The company’s stock closed at $44.66 on April 29, 2025, but jumped 6.51% to $47.80 in after-hours trading following the earnings release, reflecting positive investor reaction to the strong quarterly results and reaffirmed guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.