Gold prices suffer profit taking ahead of likely Fed cut; PCE inflation due

Introduction & Market Context

Flowserve Corporation (NYSE:FLS) presented its second quarter 2025 earnings results on July 30, highlighting continued operational improvements and margin expansion despite some moderation in bookings growth. The pump and flow control equipment manufacturer saw its stock rise 2.44% to close at $56.20 prior to the earnings release, trading well above its 52-week low of $37.34 but still below its high of $65.08.

Building on its strong first quarter performance, Flowserve demonstrated resilience in a complex global market environment characterized by tariff challenges and project timing uncertainties. The company’s strategic focus on aftermarket business and operational excellence continues to drive profitability improvements across its segments.

Quarterly Performance Highlights

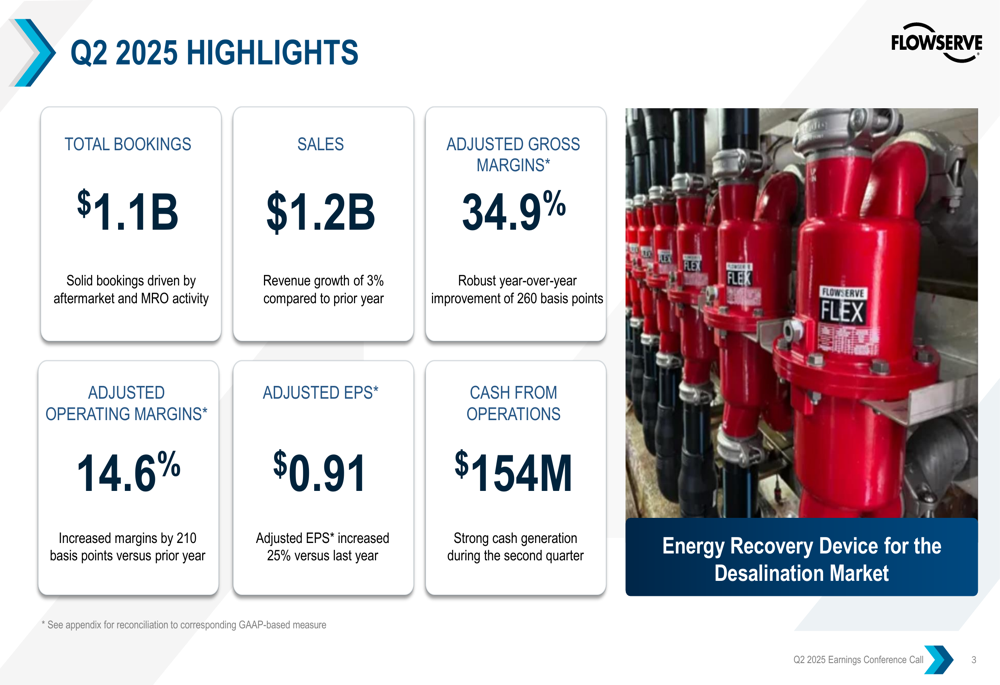

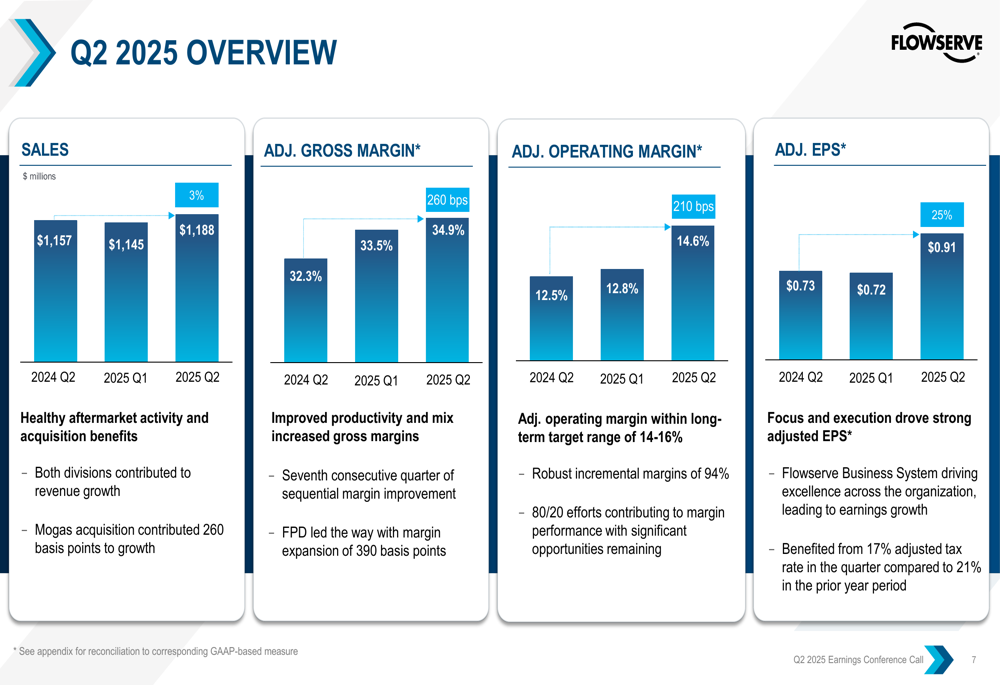

Flowserve reported sales of $1.2 billion for Q2 2025, representing a 3% increase compared to the prior year. More impressively, the company achieved significant margin expansion, with adjusted gross margin reaching 34.9%, up 260 basis points year-over-year, and adjusted operating margin improving to 14.6%, a 210 basis point increase.

As shown in the following comprehensive overview of Flowserve’s Q2 2025 performance:

This margin improvement translated into adjusted earnings per share of $0.91, marking a substantial 25% increase versus the same period last year. The strong earnings performance was supported by robust cash generation, with cash from operations totaling $154 million during the quarter.

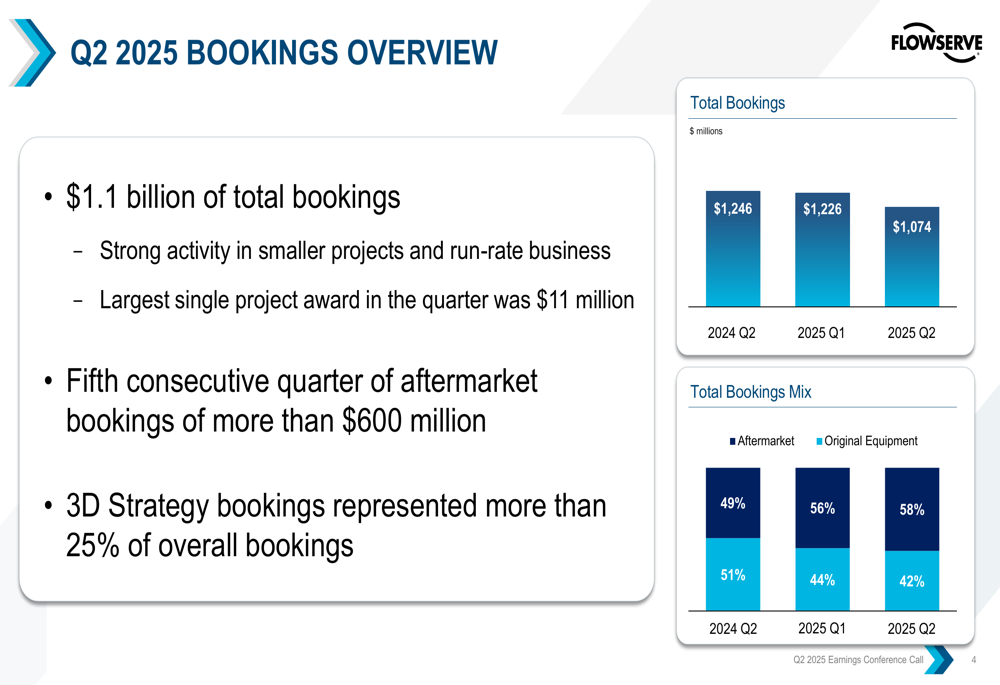

Total (EPA:TTEF) bookings came in at $1.1 billion, with aftermarket bookings representing 58% of the mix, up from 49% in Q2 2024. This shift toward higher-margin aftermarket business reflects the company’s strategic emphasis on service and maintenance activities.

The following chart illustrates Flowserve’s bookings trends and the increasing proportion of aftermarket business:

Segment Analysis

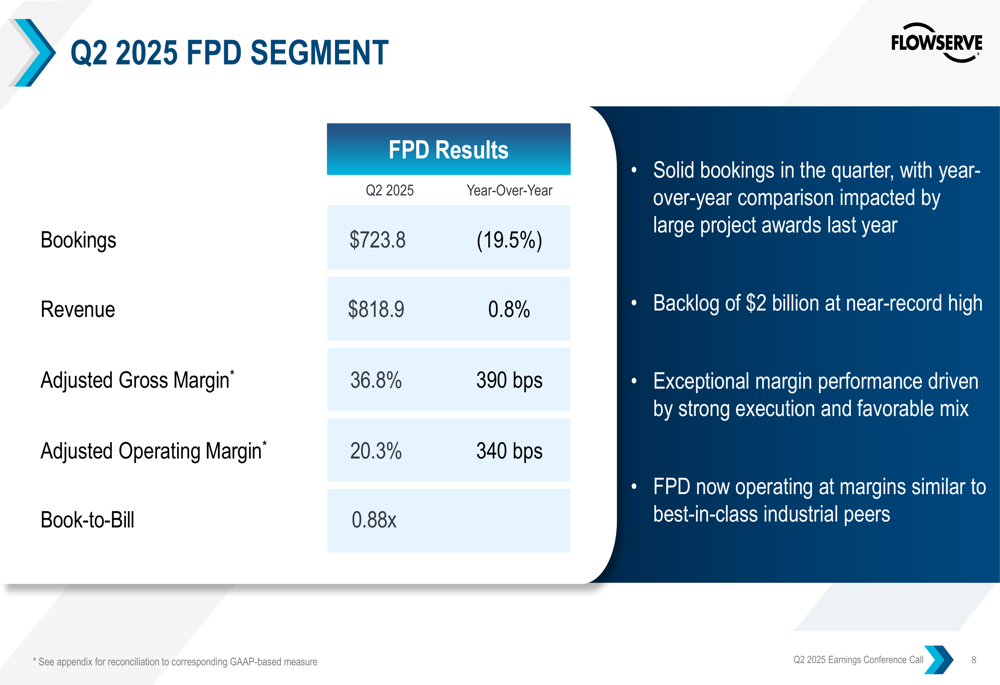

Flowserve’s performance showed significant divergence between its two main segments. The Flowserve Pumps Division (FPD) delivered exceptional margin performance despite lower bookings, while the Flow Control Division (FCD) faced challenges related to acquisition integration.

The FPD segment achieved an adjusted operating margin of 20.3%, a remarkable 340 basis point improvement year-over-year, reaching levels comparable to best-in-class industrial peers. However, bookings declined by 19.5% to $723.8 million, primarily due to tough comparisons with large project awards in the prior year. Revenue increased slightly by 0.8% to $818.9 million.

As shown in the FPD segment performance summary:

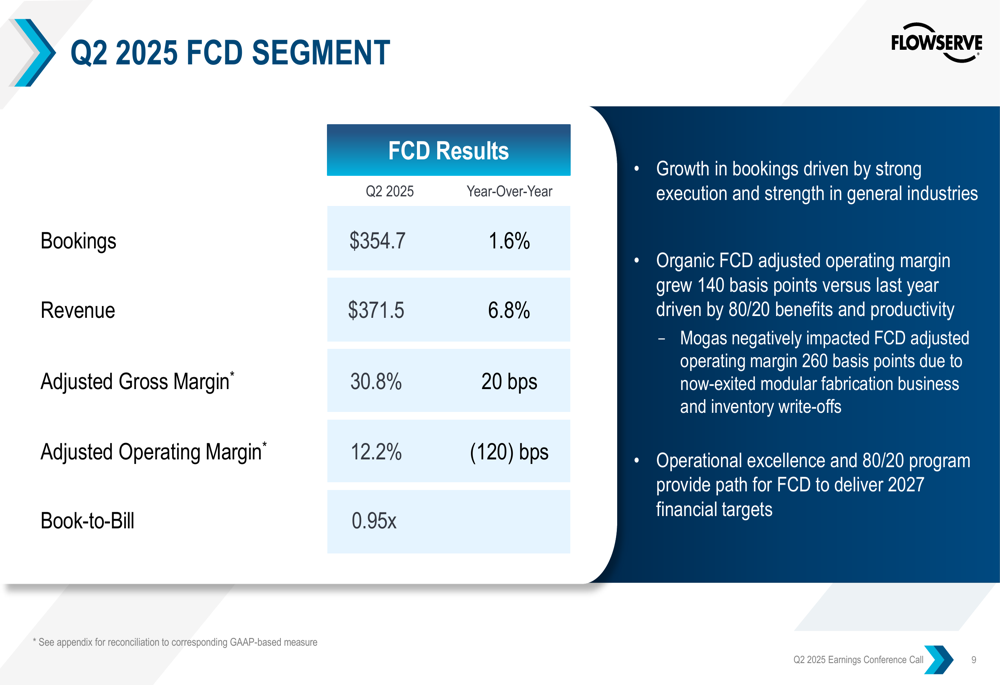

Meanwhile, the FCD segment reported a 1.6% increase in bookings to $354.7 million and a 6.8% rise in revenue to $371.5 million. However, adjusted operating margin declined by 120 basis points to 12.2%, primarily due to challenges with the Mogas acquisition, which negatively impacted FCD’s adjusted operating margin by 260 basis points. Management noted that these issues were related to the now-exited modular fabrication business and inventory write-offs.

The following chart details the FCD segment’s performance metrics:

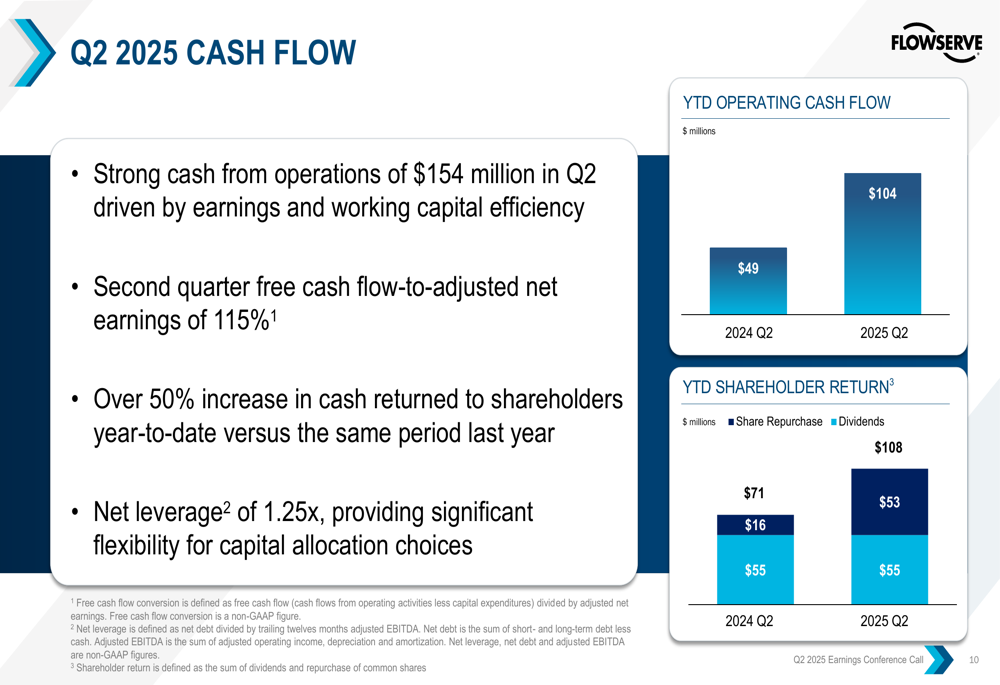

Cash Flow and Capital Allocation

Flowserve demonstrated strong cash generation in the second quarter, with operating cash flow of $154 million driven by earnings growth and working capital efficiency. The company achieved a free cash flow-to-adjusted net earnings ratio of 115% for the quarter, highlighting its ability to convert profits into cash.

This strong cash performance enabled Flowserve to increase shareholder returns, with year-to-date returns to shareholders up over 50% compared to the same period last year. The company maintained its quarterly dividend while significantly increasing share repurchases. With net leverage at a comfortable 1.25x, Flowserve maintains substantial financial flexibility for future capital allocation decisions.

As illustrated in the cash flow summary:

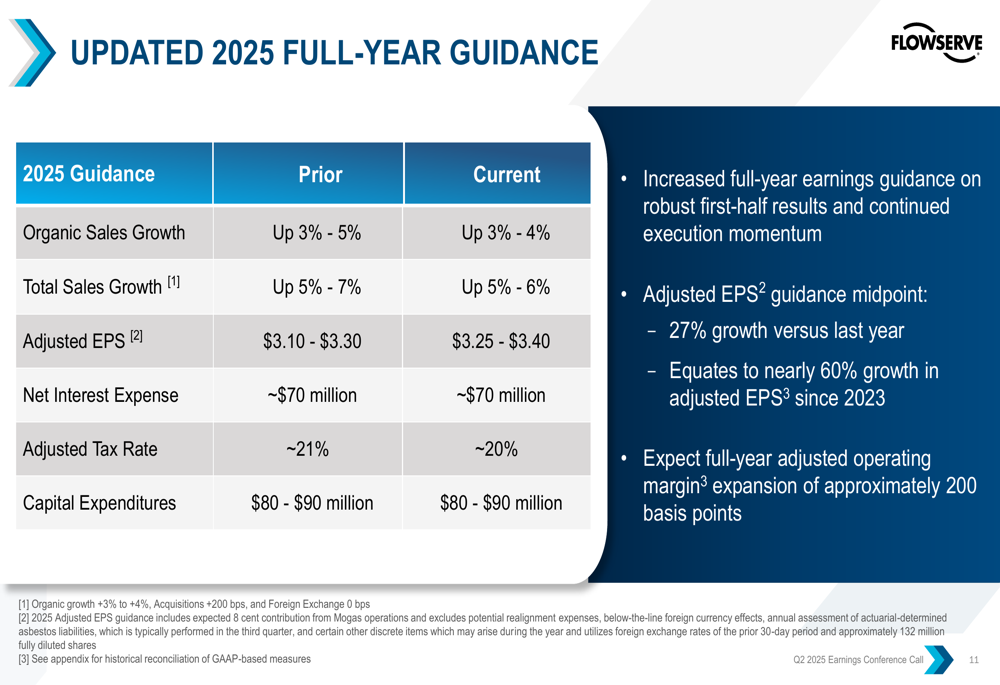

Updated Guidance and Outlook

Based on its strong first-half performance, Flowserve raised its full-year earnings guidance while slightly narrowing its revenue growth expectations. The company now forecasts adjusted EPS of $3.25-$3.40, up from the previous range of $3.10-$3.30, representing approximately 27% growth versus last year at the midpoint.

Organic sales growth is now expected to be 3%-4% (previously 3%-5%), with total sales growth of 5%-6% (previously 5%-7%). The company also lowered its expected adjusted tax rate to approximately 20% from 21% previously.

The following table details Flowserve’s updated 2025 guidance:

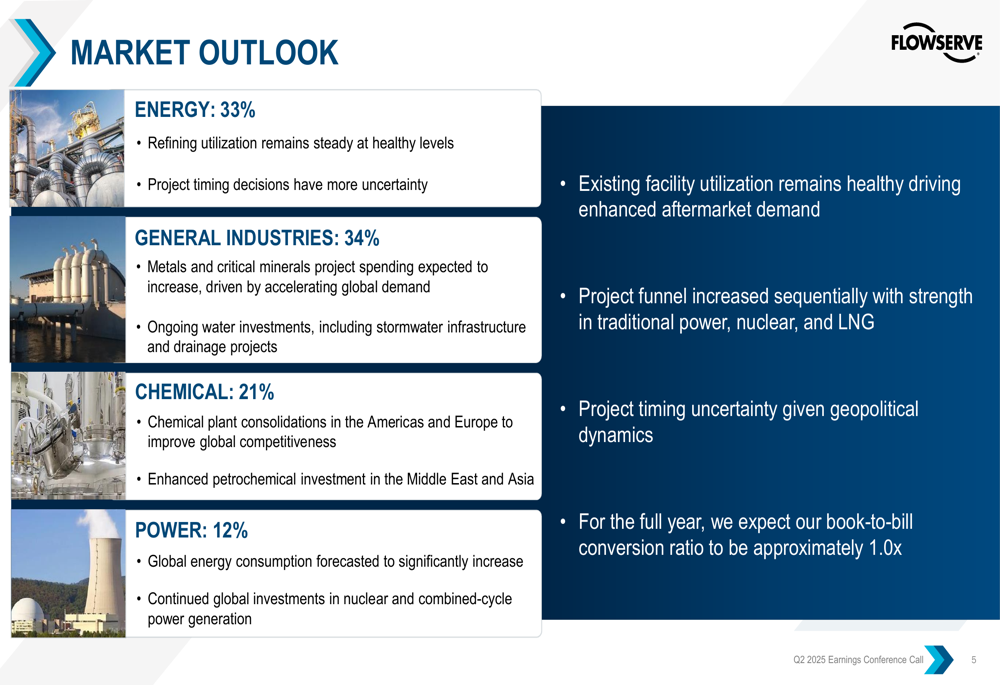

Flowserve’s market outlook remains generally positive across its key sectors, with energy (33% of business) seeing steady refining utilization, general industries (34%) benefiting from increased metals and critical minerals project spending, chemicals (21%) experiencing enhanced petrochemical investment in the Middle East and Asia, and power (12%) driven by growing global energy consumption.

However, management noted increased uncertainty around project timing due to geopolitical dynamics, while maintaining that existing facility utilization remains healthy, supporting continued strong aftermarket demand.

Strategic Initiatives

Flowserve continues to execute on its "3D Strategy" focused on diversification, decarbonization, and digitization. The company reported that bookings related to this strategy represented more than 25% of overall bookings in the quarter, highlighting progress in these strategic growth areas.

In response to tariff challenges, Flowserve has implemented two list price increases this year and introduced variable pricing as needed. The company estimates the annualized gross impact of tariffs to be between $50-$60 million but expects to fully offset this through mitigating actions, including shifting to alternative sourcing and leveraging its regional structure.

The company also launched a Commercial Excellence program in Q2 aimed at driving profitable growth, complementing its ongoing Flowserve Business System initiatives that have contributed to margin expansion.

As shown in the comprehensive Q2 2025 financial overview:

Flowserve’s second quarter results demonstrate the company’s ability to drive margin expansion and earnings growth despite a more challenging bookings environment. With raised earnings guidance, strong cash flow generation, and strategic initiatives gaining traction, the company appears well-positioned to continue its positive momentum through the second half of 2025, though investors should monitor project timing uncertainties and ongoing tariff impacts.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.