5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Flowserve Corporation (NYSE:FLS) reported strong second-quarter 2025 results during its July 30 earnings presentation, highlighted by significant margin expansion and earnings growth despite ongoing tariff challenges and project timing uncertainties. The pump and flow control equipment manufacturer achieved a 25% year-over-year increase in adjusted earnings per share, reaching $0.91, while revenue grew 3% to $1.2 billion.

Despite these positive results, Flowserve’s stock declined 1.77% in aftermarket trading following the presentation, suggesting some investor caution amid broader market uncertainties. The company’s current share price of $49.31 in aftermarket trading represents a pullback from its 52-week high of $65.08.

Quarterly Performance Highlights

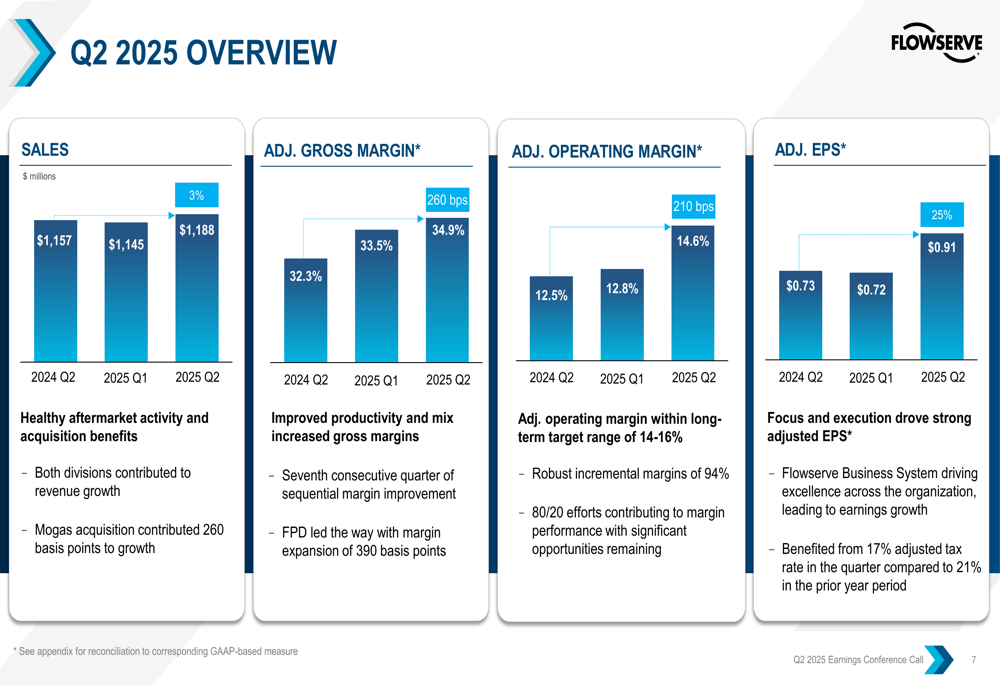

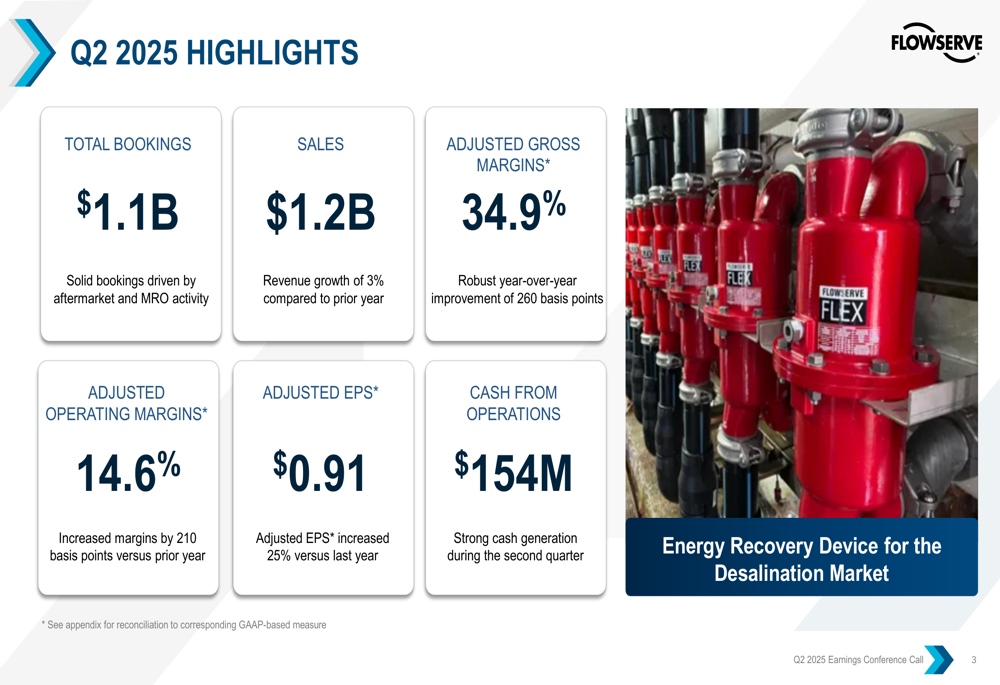

Flowserve’s second quarter demonstrated robust financial performance across key metrics, with particularly strong improvements in profitability measures. The company achieved revenue growth of 3% year-over-year to $1.2 billion, while adjusted gross margins expanded by 260 basis points to 34.9%.

As shown in the following chart of quarterly financial performance:

Adjusted operating margin reached 14.6%, an improvement of 210 basis points compared to the prior year, bringing this metric within the company’s long-term target range of 14-16%. The 25% year-over-year increase in adjusted EPS to $0.91 was driven by improved productivity and favorable mix.

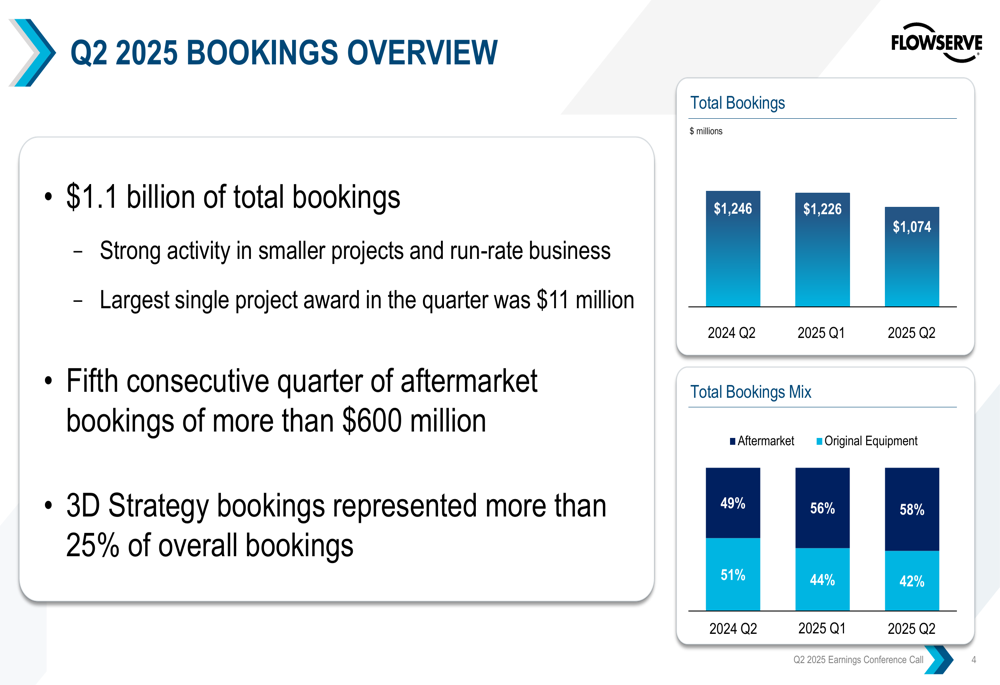

Total bookings for the quarter reached $1.1 billion, with the company noting strong activity in smaller projects and run-rate business. Notably, aftermarket bookings exceeded $600 million for the fifth consecutive quarter, representing 58% of total bookings compared to 49% in Q2 2024.

The following chart illustrates the evolution of bookings mix:

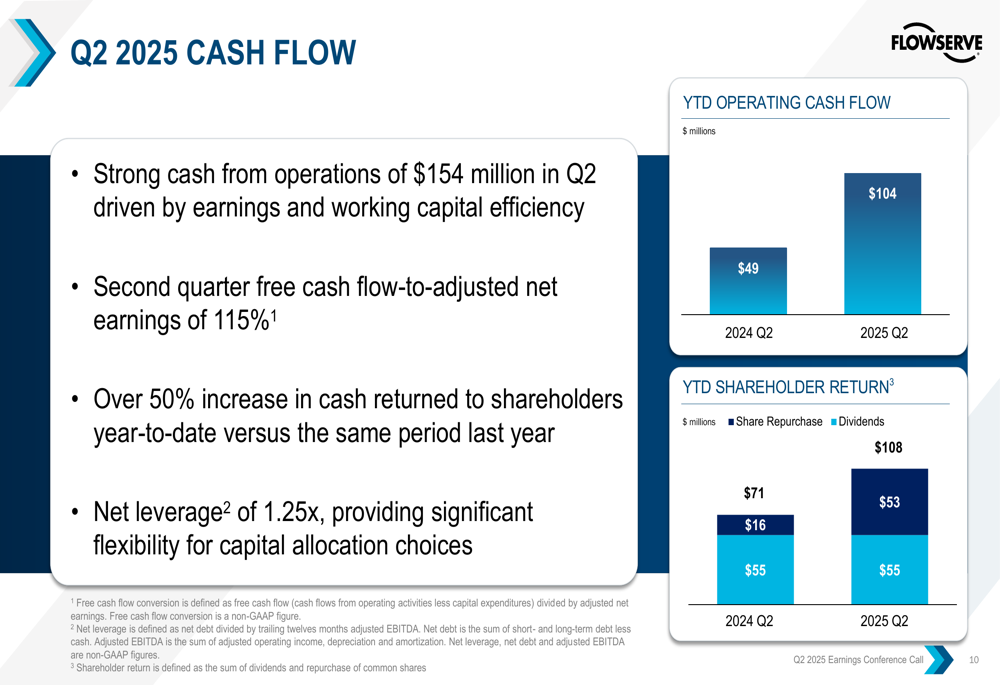

Cash generation remained strong, with cash from operations reaching $154 million in the second quarter. This performance translated to a free cash flow-to-adjusted net earnings ratio of 115%, demonstrating the company’s ability to convert earnings into cash.

The company’s cash flow and shareholder returns are illustrated in the following chart:

Segment Analysis

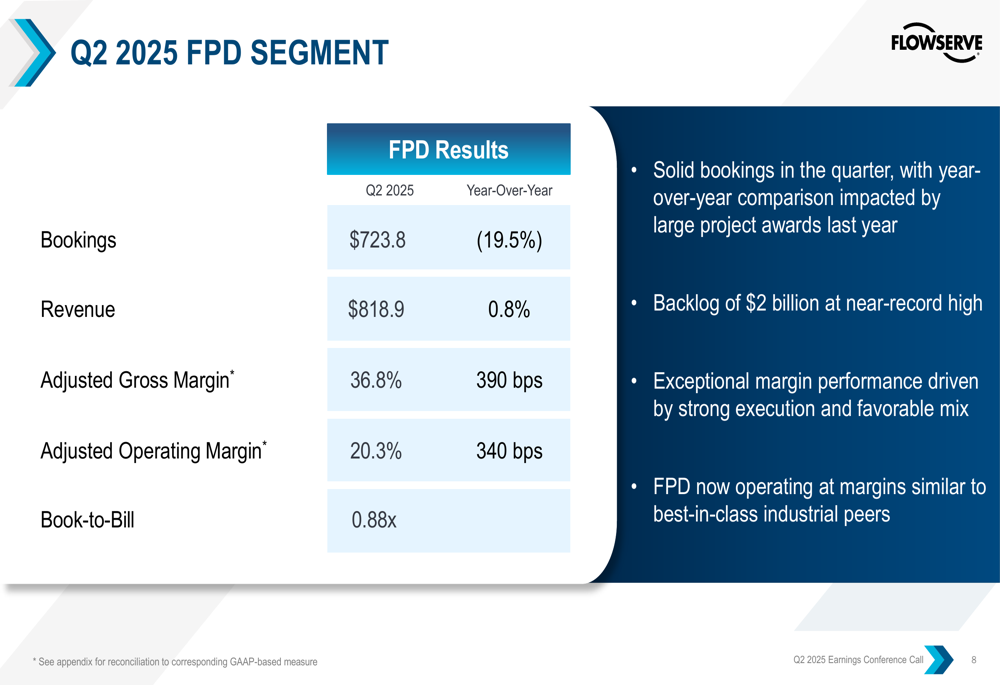

Flowserve’s Pumps Division (FPD) segment delivered exceptional margin performance in Q2 2025, achieving an adjusted operating margin of 20.3%, a 340 basis point improvement year-over-year. This places the segment’s profitability on par with best-in-class industrial peers, according to the company.

The segment’s performance is detailed in the following chart:

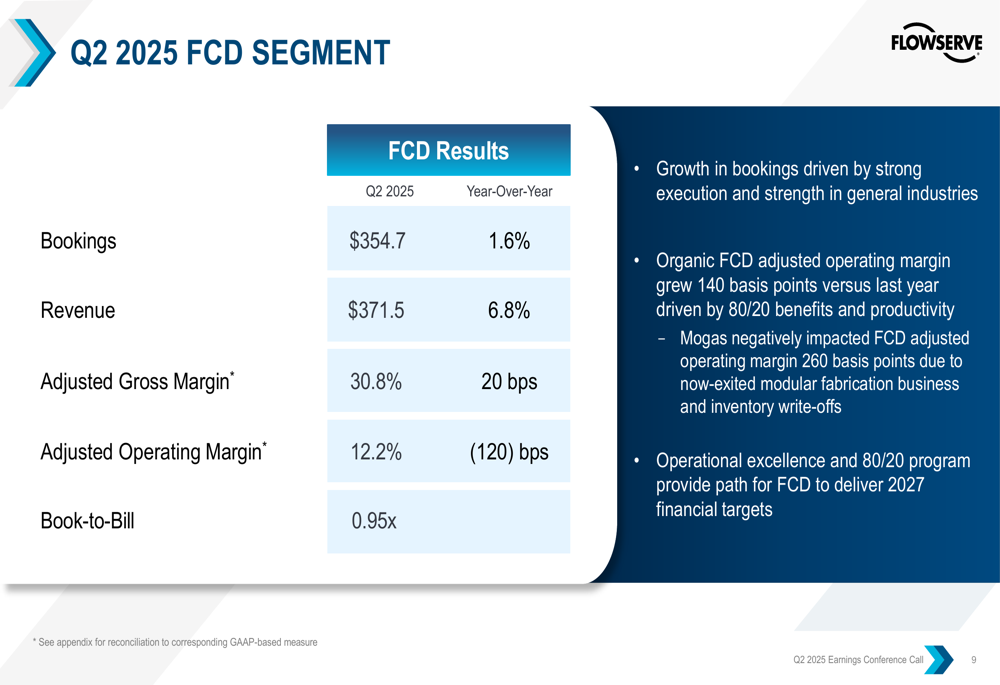

Meanwhile, the Flow Control Division (FCD) segment reported mixed results. While revenue grew 6.8% year-over-year to $371.5 million, adjusted operating margin declined by 120 basis points to 12.2%. The company attributed this decline to its Mogas acquisition, which negatively impacted FCD adjusted operating margin by 260 basis points due to a now-exited modular fabrication business and inventory write-offs.

The following chart details the FCD segment’s performance:

Strategic Initiatives

Flowserve highlighted its ongoing "3D Strategy" focused on diversification, decarbonization, and digitization. The company reported that bookings related to this strategy represented more than 25% of overall bookings in Q2 2025, indicating progress in its strategic transformation.

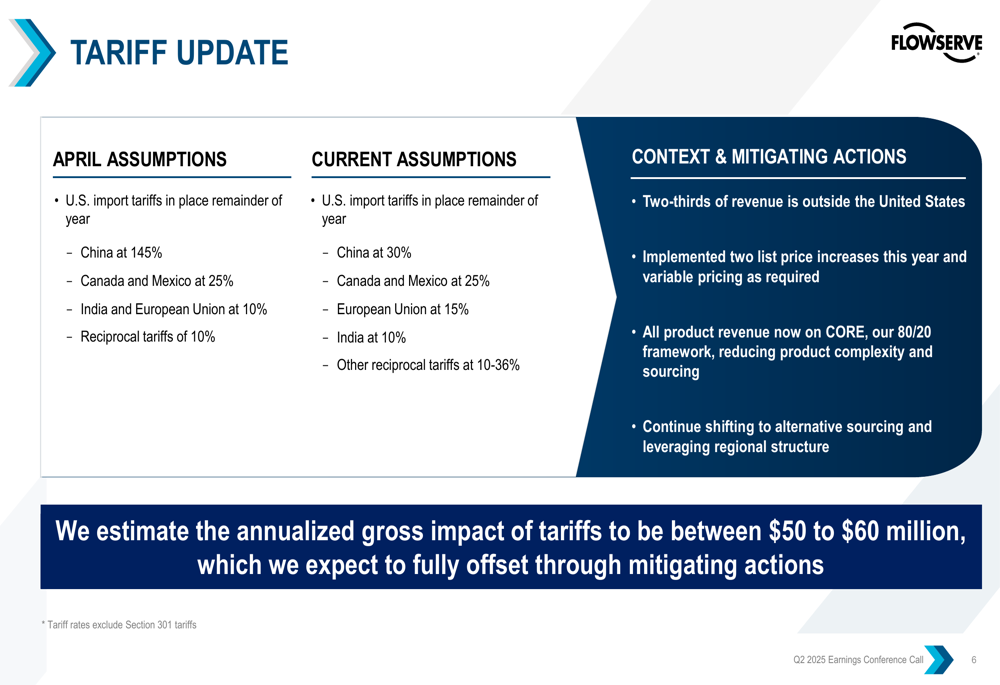

The company is also actively managing the impact of tariffs, which have evolved since its previous guidance. Flowserve estimates the annualized gross impact of tariffs to be between $50-60 million but expects to fully offset this through mitigating actions including price increases, product simplification, and alternative sourcing.

The tariff situation and mitigation strategies are outlined in the following slide:

Additionally, Flowserve launched a Commercial Excellence program in Q2 aimed at driving profitable growth. This initiative, combined with the company’s 80/20 program (focusing on the most profitable products and customers), is expected to improve operational efficiency and margin expansion, particularly in the FCD segment.

Forward-Looking Statements

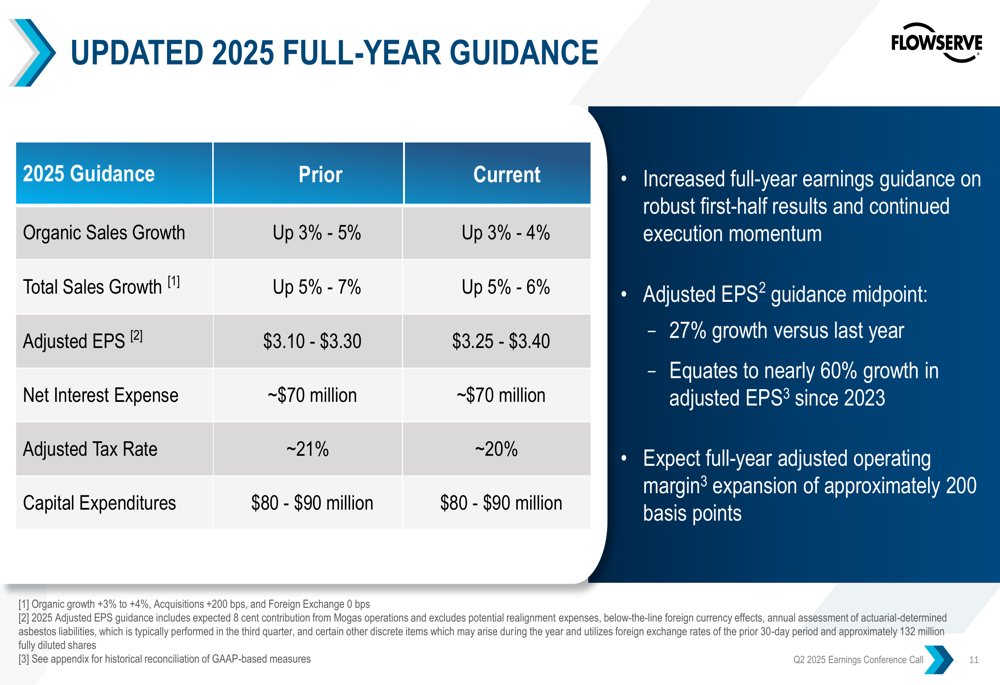

Based on strong first-half performance, Flowserve raised its full-year 2025 earnings guidance. The company now expects adjusted EPS of $3.25-$3.40, up from the previous guidance of $3.10-$3.30. This represents approximately 27% growth versus the prior year and nearly 60% growth since 2023.

The updated guidance is detailed in the following chart:

Organic sales growth is now projected at 3-4% (narrowed from 3-5% previously), while total sales growth is expected to be 5-6% (narrowed from 5-7%). The company anticipates full-year adjusted operating margin expansion of approximately 200 basis points and expects its book-to-bill conversion ratio to be approximately 1.0x for the full year.

Regarding market outlook, Flowserve noted healthy refining utilization levels driving enhanced aftermarket demand in the energy sector (33% of business). The company sees growth opportunities in metals and critical minerals projects, water investments, and nuclear and combined-cycle power generation, though it acknowledged increased uncertainty in project timing decisions due to geopolitical dynamics.

Conclusion

Flowserve’s Q2 2025 presentation painted a picture of a company successfully navigating challenging market conditions through operational excellence and strategic focus on higher-margin business. The significant margin expansion and strong cash generation enabled the company to increase shareholder returns while maintaining a healthy balance sheet with net leverage of 1.25x.

While the stock’s aftermarket decline suggests some investor caution, the raised full-year guidance reflects management’s confidence in continued execution. The company’s ability to offset tariff impacts and drive margin improvements will be key factors to watch in the coming quarters as Flowserve continues to implement its strategic initiatives.

As summarized in the company’s Q2 highlights:

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.