US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

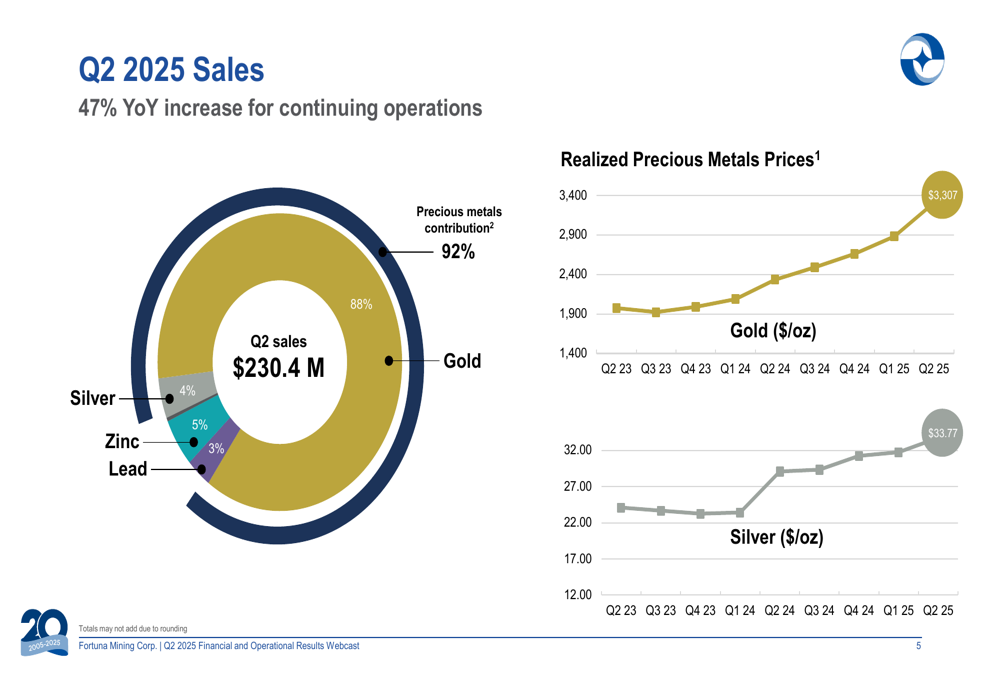

Fortuna Mining (NYSE:FSM | TSX:FVI) presented its Q2 2025 financial and operational results on August 7, 2025, highlighting significant year-over-year growth across key metrics. The company has benefited substantially from rising precious metals prices, with gold reaching $3,307 per ounce and silver at $33.77 per ounce during the quarter, while simultaneously executing strategic portfolio optimization initiatives.

The mining company’s presentation emphasized its transition to a stronger balance sheet position and focus on higher-margin operations, having divested shorter-life mines to concentrate resources on core assets with greater growth potential.

Quarterly Performance Highlights

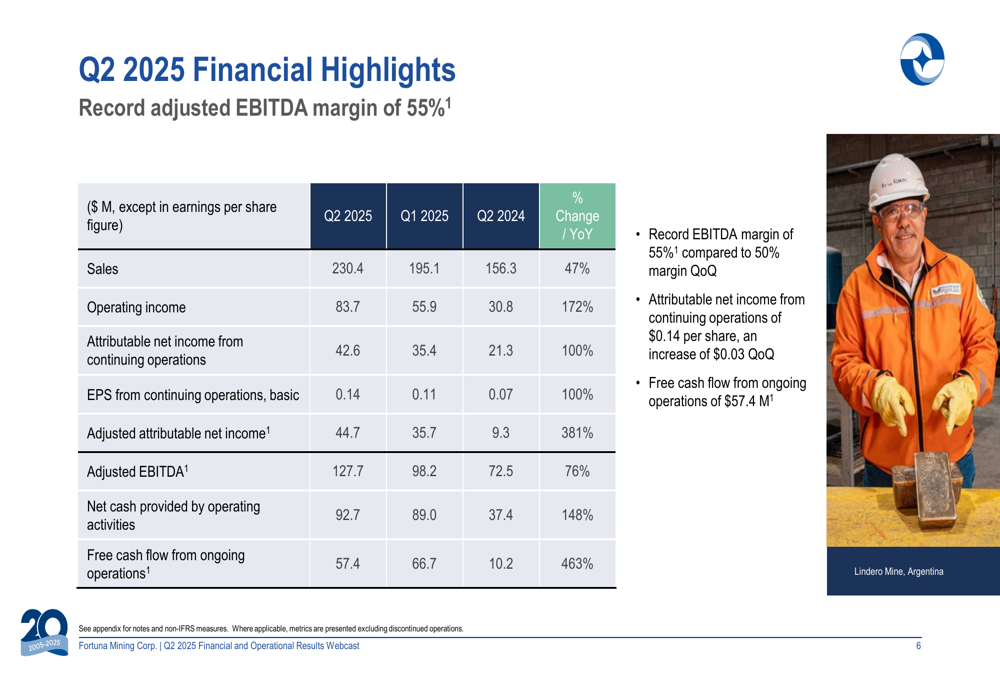

Fortuna reported impressive financial results for Q2 2025, with sales reaching $230.4 million, representing a 47% increase year-over-year for continuing operations. The company achieved a record EBITDA margin of 55%, up from 50% in the previous quarter, reflecting both higher metal prices and operational efficiencies.

As shown in the following financial highlights slide, operating income surged 172% year-over-year to $83.7 million, while attributable net income from continuing operations doubled to $42.6 million, translating to basic EPS of $0.14 per share:

Free cash flow from ongoing operations reached $57.4 million, a substantial 463% increase compared to the same period last year, though slightly lower than the $66.7 million generated in Q1 2025. The company’s adjusted EBITDA climbed to $127.7 million, representing a 76% year-over-year improvement.

Operational Results

Fortuna produced 71,229 gold equivalent ounces (GEO) during Q2 2025, keeping the company on track to meet its annual production guidance. Production was distributed across three continuing operations, with the Séguéla Mine in Côte d’Ivoire contributing the largest portion at 38,186 ounces of gold.

The breakdown of production by mine site shows relatively stable output compared to the previous quarter:

Cost metrics showed some increases compared to Q1 2025, with consolidated cash cost per GEO rising to $929 from $866, and all-in sustaining cost (AISC) increasing to $1,932 per GEO from $1,752. These increases were attributed to planned higher stripping activities at Séguéla, where AISC rose to $1,634 per ounce from $1,290 in the previous quarter.

The company’s sales composition remains heavily weighted toward gold, which accounted for 88% of total sales, followed by silver (4%), zinc (5%), and lead (3%). This metals mix, combined with rising precious metals prices, has driven the substantial revenue growth:

Strategic Initiatives

A key component of Fortuna’s strategy has been the optimization of its asset portfolio. During the quarter, the company completed the divestiture of its San Jose and Yaramoko mines, generating gross proceeds of $83.8 million while avoiding approximately $50 million in future closure costs.

This strategic repositioning allows management to focus resources on higher-margin, longer-life assets while strengthening the balance sheet. The company is also advancing its growth projects, notably at Diamba Sud, where gold resources increased significantly:

The Diamba Sud project saw a 53% increase in Indicated resources to 724,000 ounces of gold and a 93% increase in Inferred resources to 285,000 ounces. Fortuna is targeting completion of a Preliminary Economic Assessment (PEA) for the project in Q4 2025, potentially adding another growth avenue to its portfolio.

Balance Sheet and Liquidity

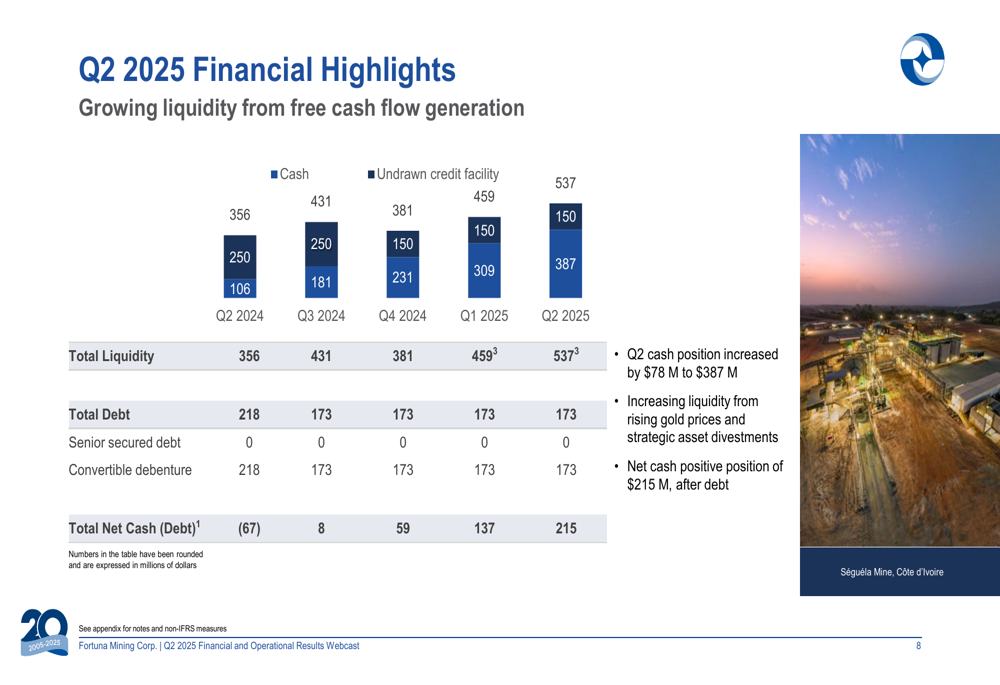

Fortuna’s financial position strengthened considerably during the quarter, with total liquidity reaching $537 million and a net cash position of $215 million. This represents a substantial improvement from the net debt position reported a year earlier.

The following chart illustrates the company’s growing liquidity position over recent quarters:

Cash increased by $78 million to $387 million in Q2, driven by strong operational cash flow, proceeds from asset divestments, and rising gold prices. The company maintained its total debt at $173 million, unchanged from previous quarters, resulting in the positive net cash position.

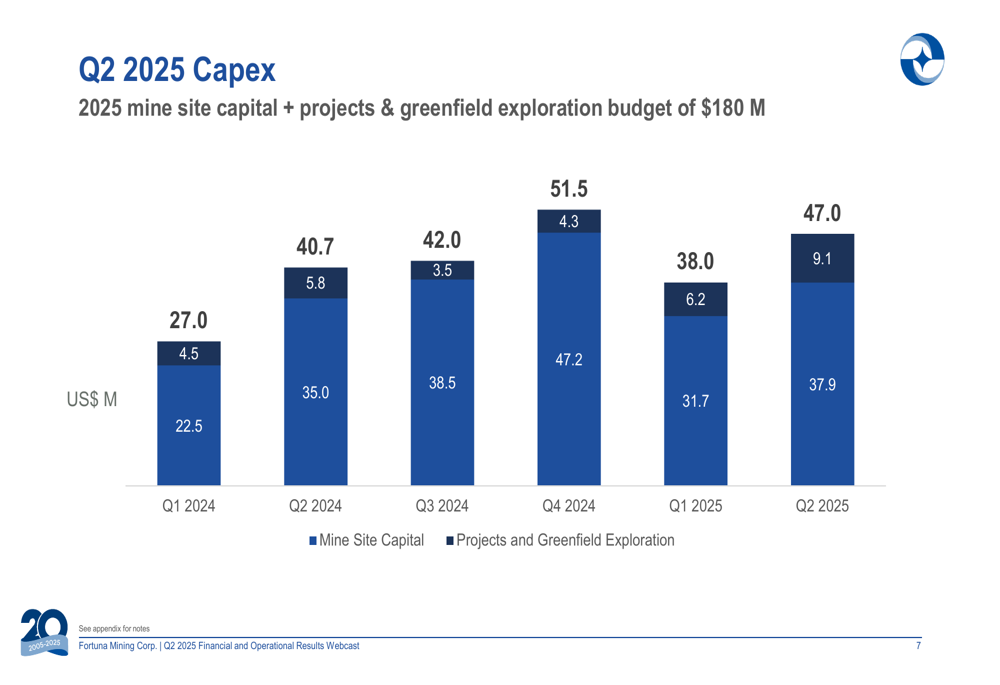

Capital expenditures for the quarter totaled $47 million, comprising $37.9 million in mine site capital and $9.1 million in projects and greenfield exploration. This represents an increase from the $38 million spent in Q1 2025, reflecting the company’s continued investment in growth initiatives:

Forward Guidance

Fortuna maintained its 2025 production guidance of 309,000 to 339,000 gold equivalent ounces at an all-in sustaining cost of $1,670 to $1,765 per GEO. The guidance includes expected gold production of 265,000 to 290,000 ounces, with the Séguéla mine in Côte d’Ivoire projected to be the lowest-cost producer at an AISC of $1,500 to $1,600 per ounce.

Looking ahead, the company highlighted that its Séguéla operation is on track for increased gold production in 2026, with guidance of 160,000 to 180,000 ounces from that mine alone. The upcoming PEA for Diamba Sud in Q4 2025 will provide further visibility on the company’s growth pipeline.

With its strengthened balance sheet, optimized portfolio, and exposure to strong precious metals prices, Fortuna appears well-positioned to continue delivering robust financial results while advancing its growth initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.