S&P 500 struggles for direction as investor await inflation data

Introduction & Market Context

Four Corners Property Trust (NYSE:FCPT) released its Q2 2025 investor presentation highlighting the company's consistent growth trajectory and resilient portfolio performance. The net lease REIT reported AFFO per share of $0.44 for the quarter, representing a 2.8% year-over-year increase, while rental income grew by 11% to $64.5 million.

FCPT's stock closed at $23.84 following the release, up 1.09% in regular trading, with a slight decline of 0.17% in aftermarket trading. The company positions itself as a "calm port in the volatility storm," emphasizing its conservative financial policies and selective acquisition approach in the current market environment.

10-Year Growth and Portfolio Diversification

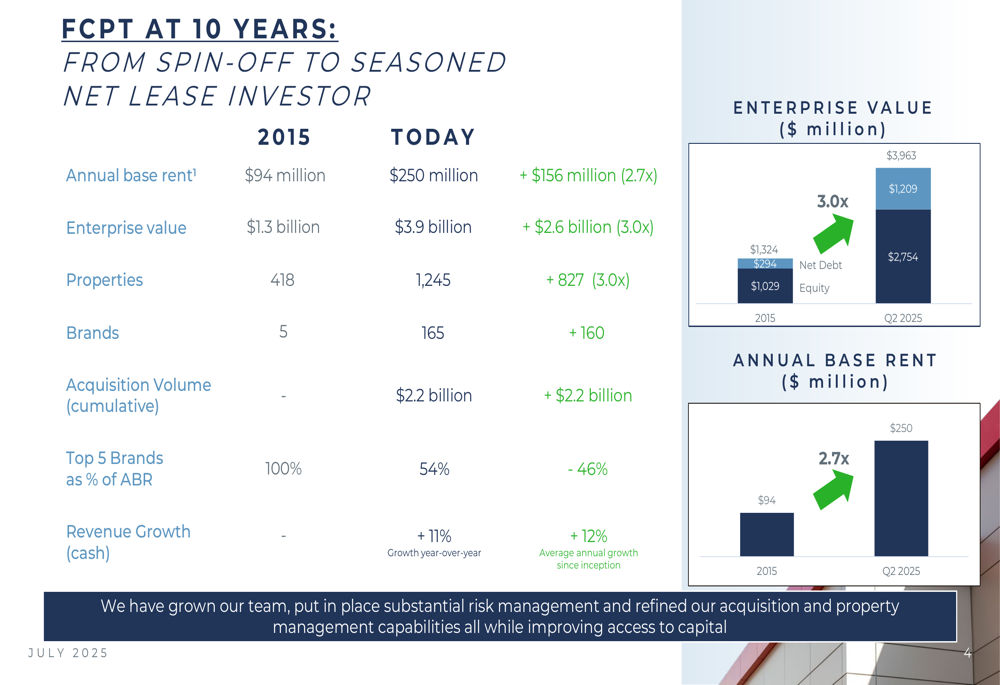

The presentation showcased FCPT's impressive growth since its 2015 inception as a spin-off from Darden Restaurants. Over the past decade, the company has expanded its property count from 418 to 1,245 (a 3.0x increase), while growing its enterprise value from $1.3 billion to $3.9 billion and annual base rent from $94 million to $250 million.

As shown in the following chart detailing FCPT's 10-year growth metrics:

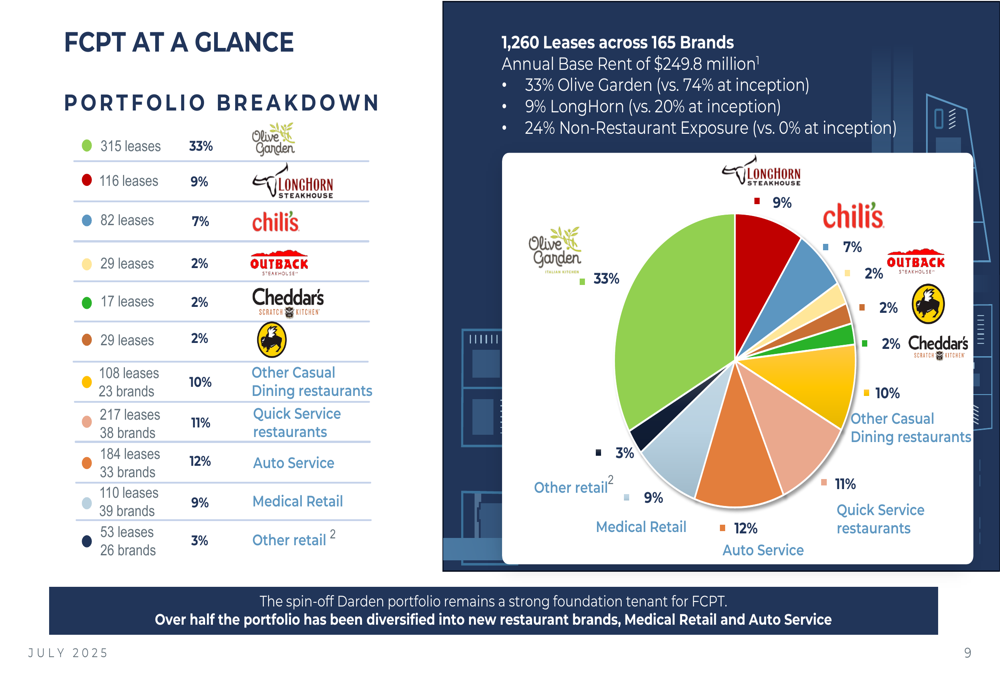

A key component of FCPT's strategy has been diversifying beyond its original Darden-heavy portfolio. While Olive Garden and LongHorn Steakhouse properties initially represented 94% of annual base rent, they now account for 42%, with Olive Garden at 33% (down from 74% at inception) and LongHorn at 9% (down from 20%). The company has expanded to include 1,260 leases across 165 brands, with 24% non-restaurant exposure compared to 0% at inception.

The following portfolio breakdown illustrates this diversification:

During the earnings call, CEO Bill Lannahan emphasized this strategic diversification, stating: "Our portfolio remains resilient. Small and fungible buildings leased to large national operators, which are resilient in uncertain times."

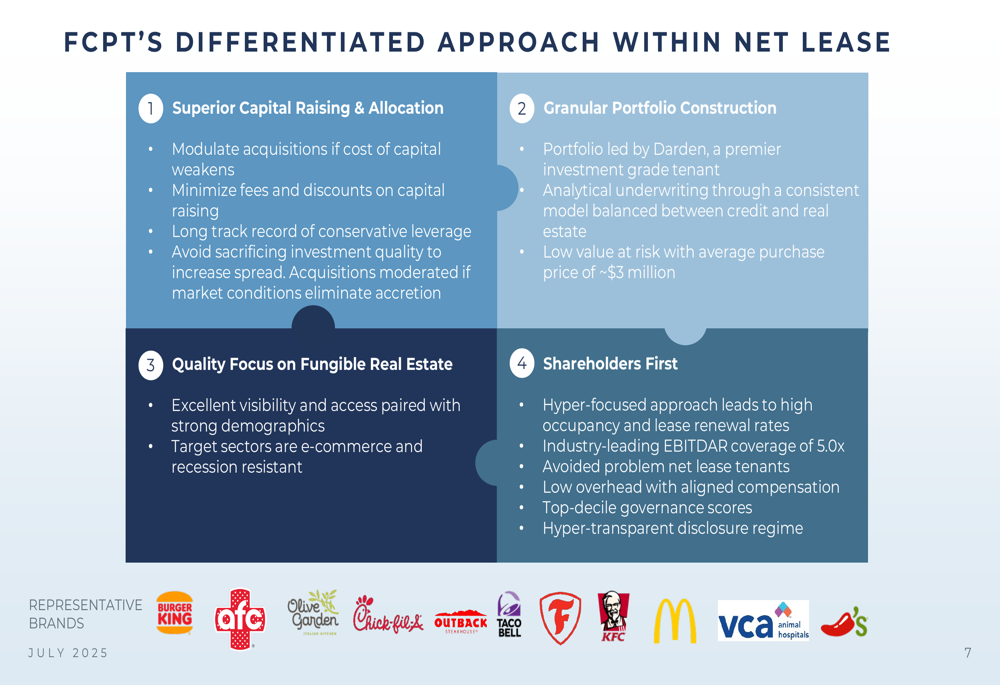

Differentiated Investment Strategy

FCPT's presentation highlighted its differentiated approach within the net lease sector, focusing on four key areas: superior capital allocation, granular portfolio construction, quality focus on fungible real estate, and shareholder-first policies.

The company's strategy emphasizes:

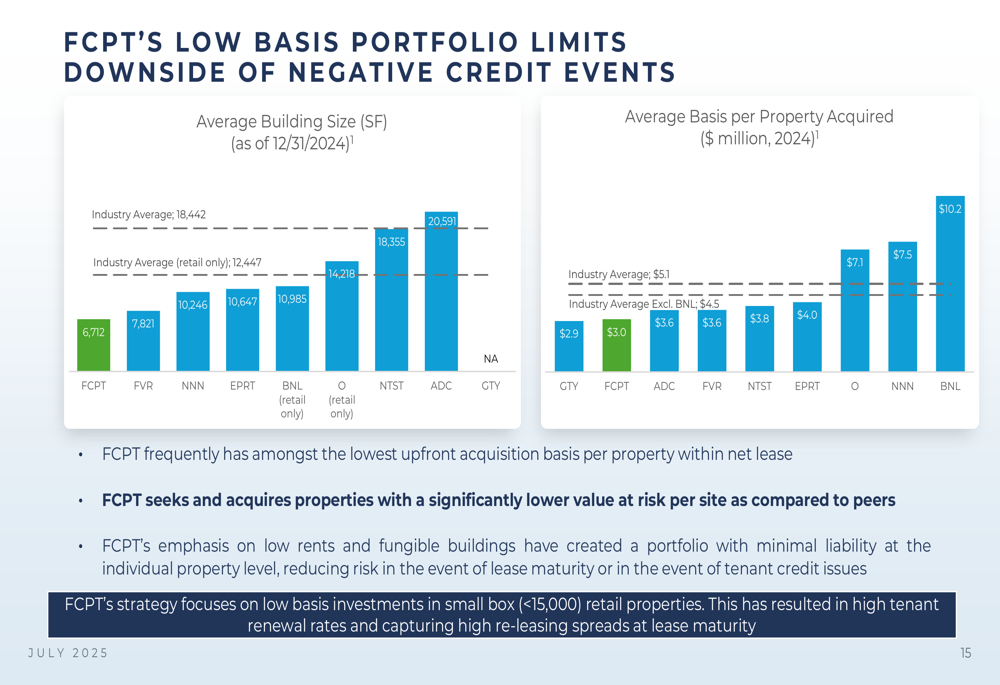

A cornerstone of FCPT's approach is its focus on low-basis investments, which limits downside risk. With an average building size of 6,712 square feet (compared to the industry average of 18,442) and an average property acquisition basis of $3.0 million (versus the industry average of $5.1 million), FCPT maintains a significantly lower value at risk per site compared to peers.

The following chart illustrates this competitive advantage:

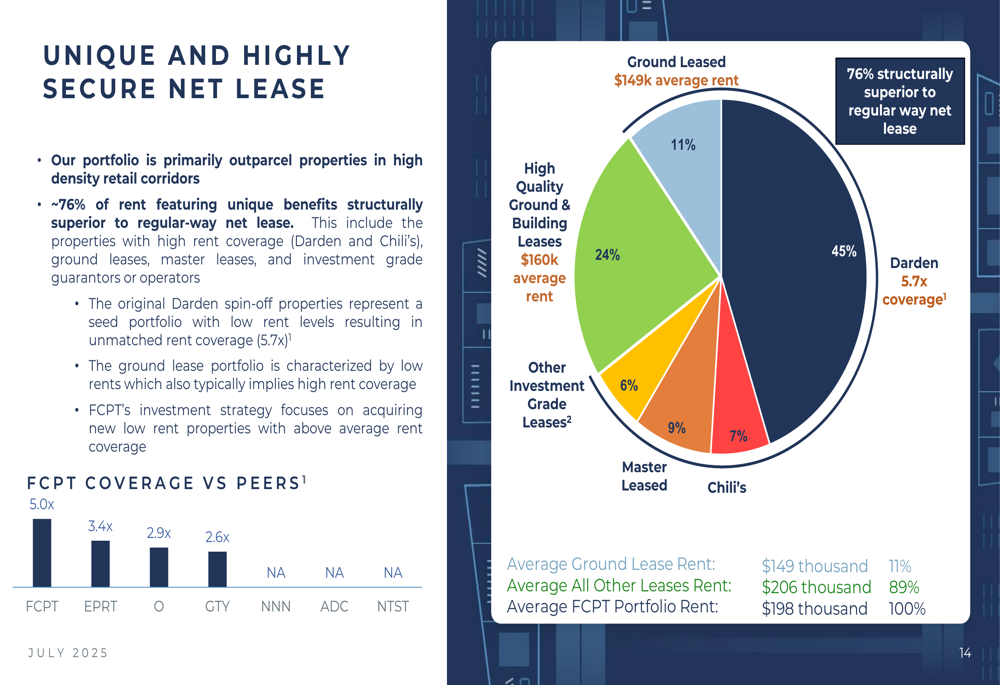

FCPT also emphasizes the security of its portfolio, with approximately 76% of rent featuring structural advantages superior to typical net lease arrangements. This includes properties with high rent coverage (Darden and Chili's), ground leases, master leases, and investment grade guarantors or operators.

As shown in the following breakdown of FCPT's secure net lease portfolio:

The company has maintained a highly selective approach to tenant selection, deliberately avoiding exposure to sectors it considers higher risk, including pharmacies, entertainment venues, gyms, furniture retailers, and EV-only auto service. This strategy has contributed to FCPT's strong rent collection rate of 99.8% and portfolio occupancy of 99.4%.

Financial Position and Outlook

FCPT's presentation emphasized its conservative financial policies, including a well-laddered debt maturity profile, conservative leverage (4.5x net debt to adjusted EBITDAre), strong liquidity ($500 million available), minimal floating rate exposure (97% fixed-rate debt), and investment grade ratings (BBB by Fitch and Baa3 by Moody's).

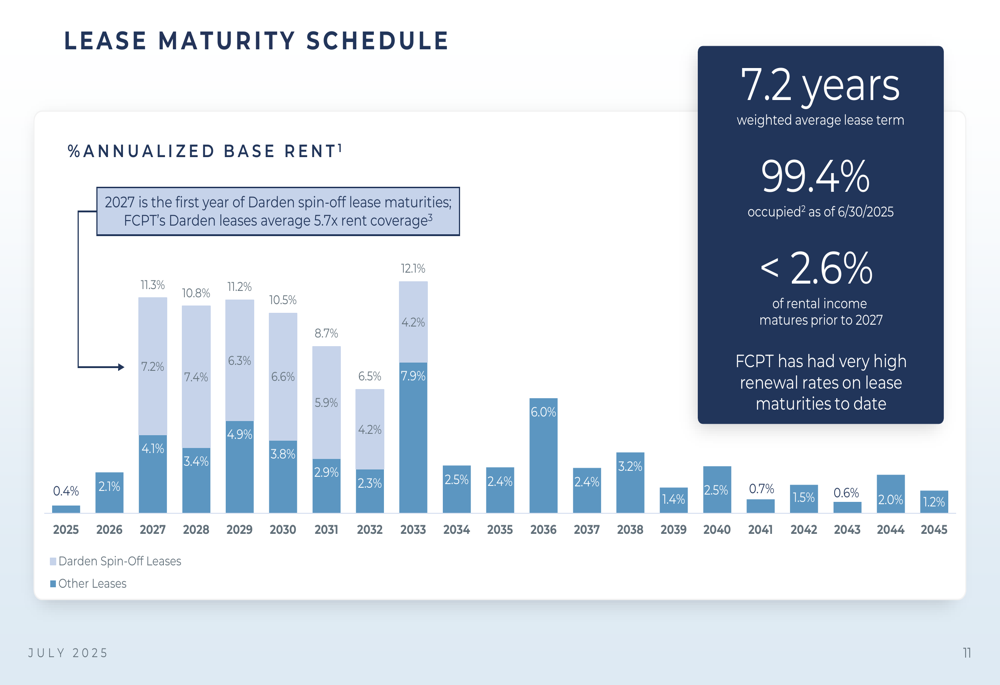

The company's lease maturity schedule demonstrates long-term stability, with a weighted average lease term of 7.2 years and less than 2.6% of rental income maturing prior to 2027:

For 2025, FCPT has completed $84 million of acquisitions in Q2 at a 6.7% cap rate, bringing the last twelve months' acquisition volume to $344 million at a 6.9% cap rate. The company has maintained its disciplined approach to acquisitions, focusing on properties with strong demographics, visibility, and access, while avoiding compromises on quality to increase spread.

Looking ahead, FCPT is well-positioned for continued growth with $500 million in available capital for acquisitions and a $470 million capacity before reaching a 6x leverage ratio. The company expects cash general and administrative expenses to range between $18 million and $18.5 million for the full year 2025.

Conclusion

FCPT's Q2 2025 presentation portrays a company that has successfully executed its growth and diversification strategy over the past decade while maintaining a conservative financial position. The company's focus on small, fungible properties with strong tenant coverage has resulted in consistent performance, even during periods of economic uncertainty.

As CEO Bill Lannahan noted during the earnings call, "We have a ten-year track record of being extra sensitive to our cost of capital by modulating capital raising and investment when necessary." This disciplined approach to capital management, combined with FCPT's selective acquisition strategy, positions the company to continue delivering stable returns to shareholders despite potential economic headwinds.

While the company faces challenges including potential economic downturns, rising interest rates, and competition for acquisitions, FCPT's conservative leverage, high occupancy rates, and diversified tenant base provide a solid foundation for navigating market volatility.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.