Street Calls of the Week

Introduction & Market Context

Frontier Communications (OTC:FTRCQ) Parent Inc (NASDAQ:FYBR) presented its second quarter 2025 results on July 29, 2025, showcasing accelerated growth across all key performance metrics. The company’s shares closed at $36.60 and rose 1.01% in after-hours trading following the presentation, reflecting positive investor sentiment toward the results.

The telecommunications provider continues to execute its fiber-first strategy, with significant progress in expanding its fiber network footprint and attracting new customers. This quarter’s results demonstrate Frontier’s continued momentum in transitioning from a legacy copper network provider to a modern fiber broadband company.

Quarterly Performance Highlights

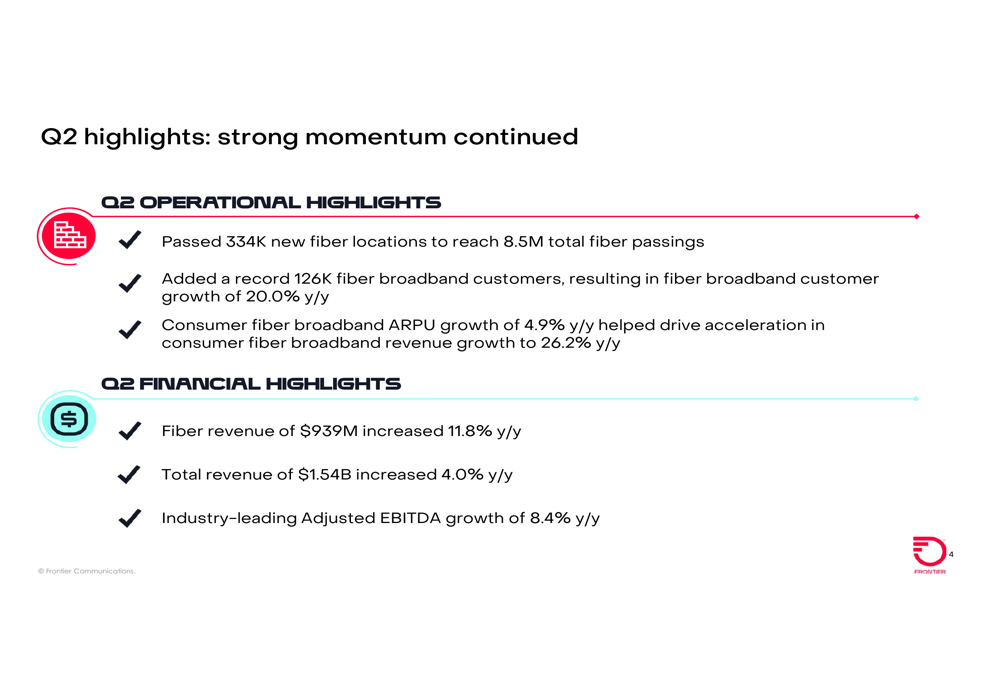

Frontier reported robust operational and financial results for Q2 2025, with notable acceleration compared to the same period last year. The company passed 334,000 new fiber locations during the quarter, bringing its total fiber passings to 8.5 million. Most impressively, Frontier added a record 126,000 fiber broadband customers, representing 20.0% year-over-year growth.

As shown in the following quarterly highlights slide, the company achieved strong growth across multiple metrics:

The consumer fiber broadband average revenue per user (ARPU) increased by 4.9% year-over-year, helping drive consumer fiber broadband revenue growth of 26.2%. Total (EPA:TTEF) revenue reached $1.54 billion, up 4.0% compared to Q2 2024, while Adjusted EBITDA grew by 8.4% year-over-year, which the company describes as "industry-leading."

These results represent significant acceleration compared to Q2 2024, when Frontier reported 2% revenue growth, 5% EBITDA growth, and added 92,000 fiber broadband customers with 3.5% ARPU growth.

Fiber Customer and ARPU Growth

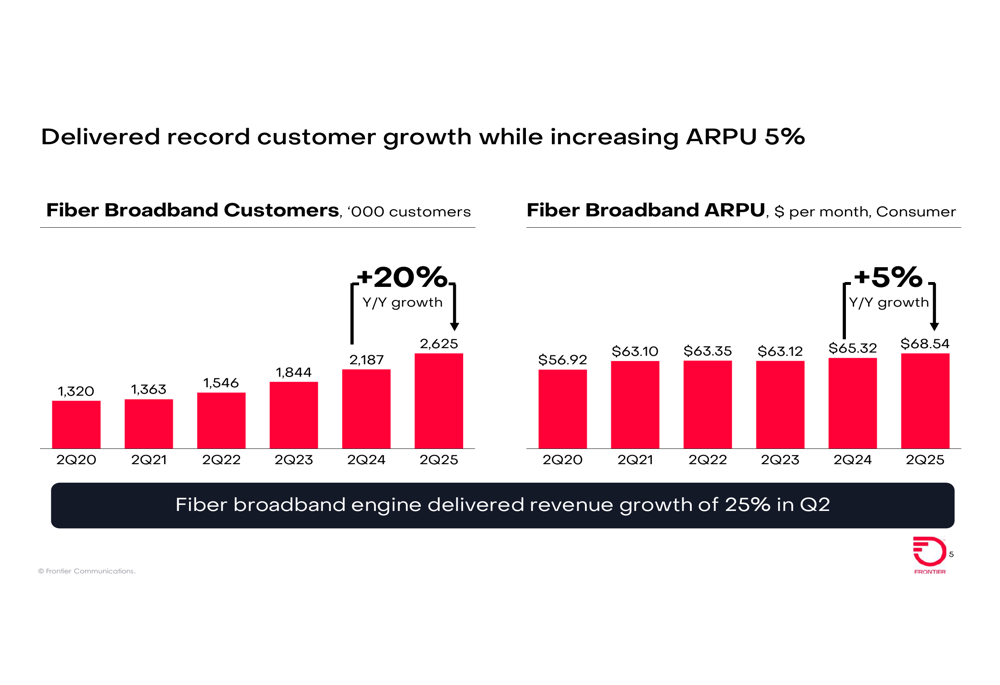

Frontier’s fiber broadband customer base has shown consistent growth over the past five years, nearly doubling from 1,320,000 in Q2 2020 to 2,625,000 in Q2 2025. Simultaneously, the company has successfully increased its ARPU from $56.92 to $68.54 over the same period, representing a 20.4% increase over five years.

The following chart illustrates this impressive growth trajectory in both customers and ARPU:

The combination of expanding customer base and rising ARPU has created a powerful growth engine for Frontier, with fiber broadband revenue increasing by 25% in Q2 2025. This growth rate significantly outpaces the overall company revenue growth of 4%, highlighting the importance of fiber to Frontier’s future.

Financial Results Analysis

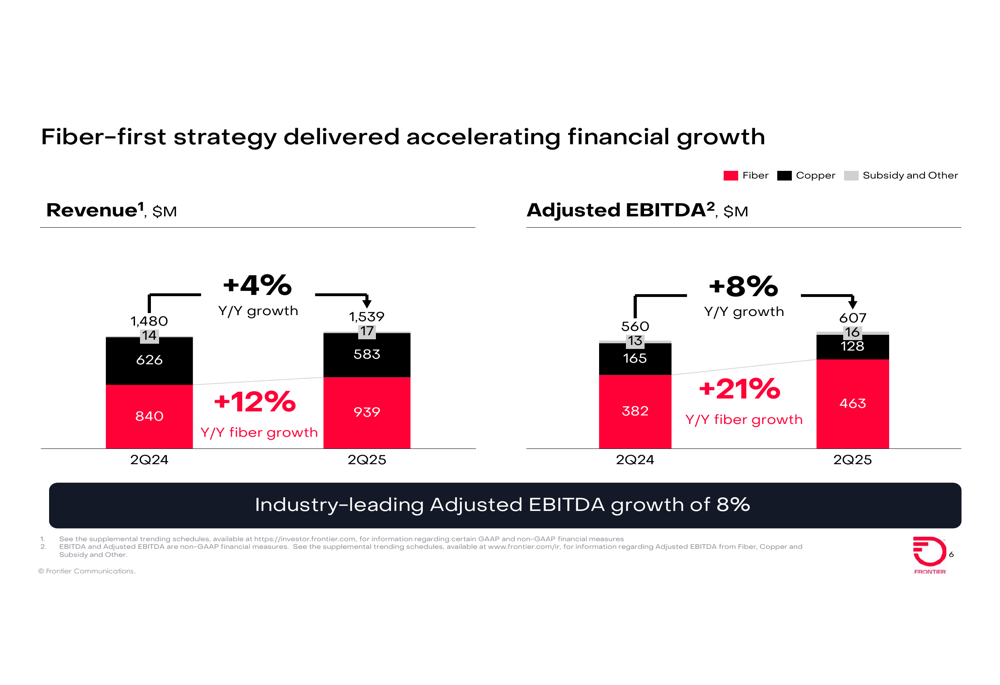

Frontier’s financial performance demonstrates the success of its fiber-first strategy, with fiber revenue now comprising a larger portion of total revenue. As shown in the following financial breakdown, fiber revenue grew by 12% year-over-year to $939 million in Q2 2025, while total revenue increased by 4% to $1.54 billion:

Even more impressive is the company’s Adjusted EBITDA growth of 8%, reaching $607 million in Q2 2025 compared to $560 million in Q2 2024. The fiber segment’s contribution to Adjusted EBITDA grew by 21% year-over-year, from $382 million to $463 million, demonstrating the higher profitability of fiber services compared to legacy copper offerings.

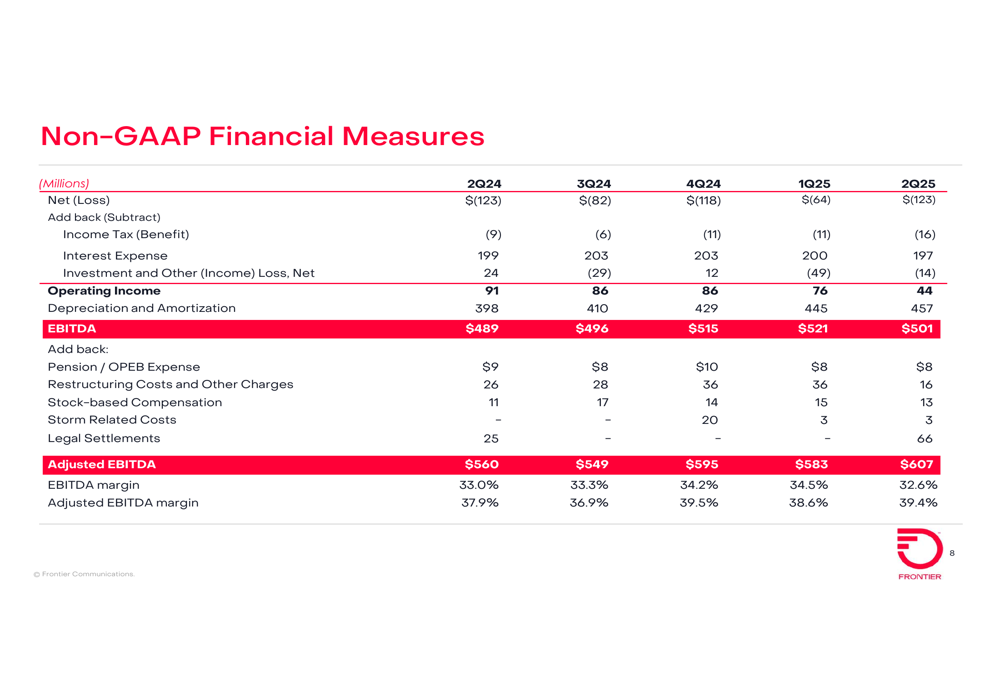

The company’s detailed Non-GAAP financial measures table provides additional context for its performance:

This financial data reveals that Frontier’s operating income and EBITDA have been consistently improving over the past five quarters, with Q2 2025 showing the strongest results. The company’s EBITDA margin and Adjusted EBITDA margin have also shown steady improvement, indicating increased operational efficiency.

Strategic Initiatives

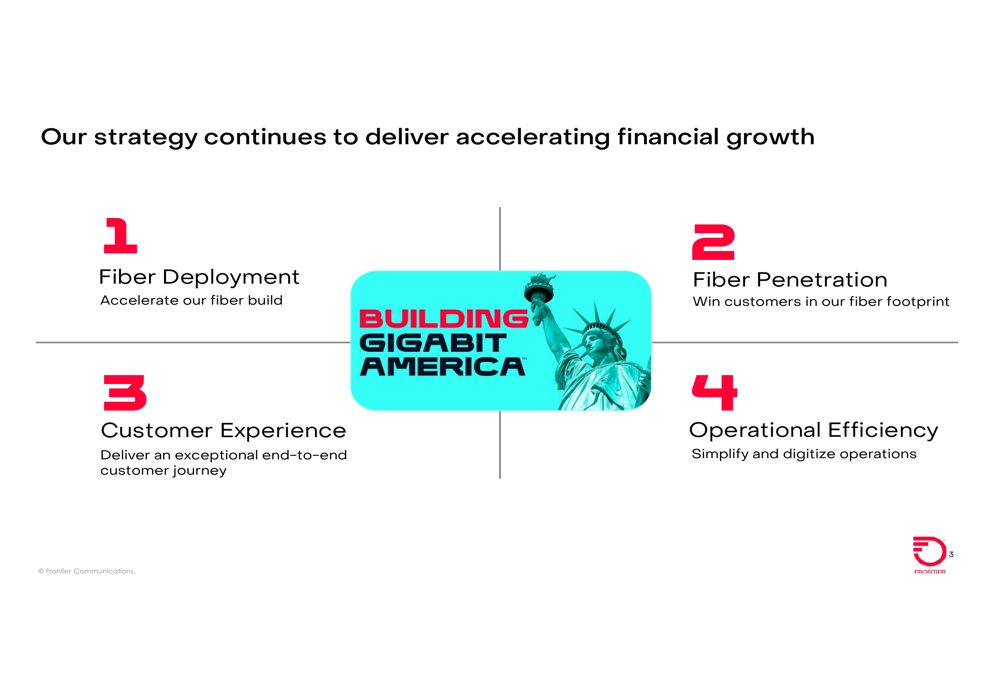

Frontier’s presentation outlined its four-pillar strategy for accelerating financial growth, focusing on fiber deployment, fiber penetration, customer experience, and operational efficiency. This comprehensive approach has been driving the company’s transformation and financial performance.

The following strategic framework illustrates Frontier’s approach to "Building Gigabit America":

The first pillar, accelerating fiber build, is evident in the addition of 334,000 new fiber locations during Q2. The second pillar, winning customers in the fiber footprint, is demonstrated by the record 126,000 fiber customer additions. The third and fourth pillars focus on delivering exceptional customer experiences and simplifying operations, which likely contribute to the improving ARPU and EBITDA margins.

Notably, the company’s Safe Harbor statement mentioned a proposed merger with Verizon (NYSE:VZ), though no additional details were provided in the presentation slides.

Forward Outlook

While Frontier did not provide specific forward guidance in the presentation slides, the company’s strong Q2 2025 performance suggests continued momentum in its fiber-first strategy. The accelerating growth in fiber customers, ARPU, revenue, and EBITDA indicates that Frontier’s strategic initiatives are yielding increasingly positive results.

The company’s focus on expanding its fiber network footprint while simultaneously increasing penetration rates in existing markets positions it well for continued growth. As Frontier continues to transition from legacy copper services to fiber broadband, investors can expect the higher-margin fiber business to drive further improvements in overall financial performance.

With fiber broadband revenue growing at 25% and fiber EBITDA increasing by 21% year-over-year, Frontier appears well-positioned to maintain its growth trajectory in the competitive telecommunications market. The after-hours stock price increase of 1.01% suggests that investors are optimistic about the company’s direction and execution of its fiber-first strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.