Raymond James raises Fulgent Genetics stock price target to $36 on strong performance

Introduction & Market Context

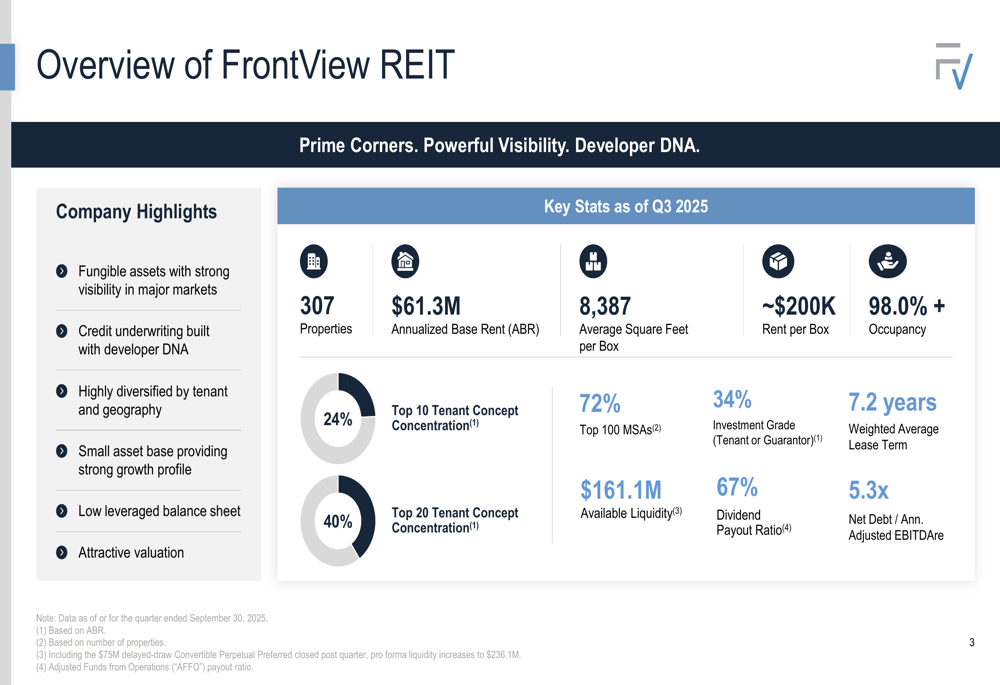

FrontView REIT Inc. (NYSE:FVR), an internally-managed net-lease REIT focused on high-traffic frontage properties, presented its Q3 2025 investor update on November 13, 2025. The company reported an impressive EPS of $0.19, significantly outperforming the forecasted -$0.01, while maintaining high occupancy levels above 98%. Despite this strong performance, FVR’s stock showed only a modest 0.81% increase, closing at $13.61.

The presentation highlighted FrontView’s strategic positioning in the net-lease REIT sector, emphasizing its focus on smaller, more productive assets with frontage on high-traffic roads. The company maintains a portfolio of 307 properties generating $61.3 million in annualized base rent, down slightly from $63.2 million in the previous quarter due to strategic dispositions.

Quarterly Performance Highlights

FrontView reported solid operating metrics for Q3 2025, including 98% occupancy (a 20 basis point increase), a weighted average lease term of 7.2 years, and a net debt to adjusted annual EBITDAre ratio of 5.3x. The company’s dividend payout ratio stands at a conservative 67%, providing room for future increases.

As shown in the following overview of FrontView REIT’s key metrics:

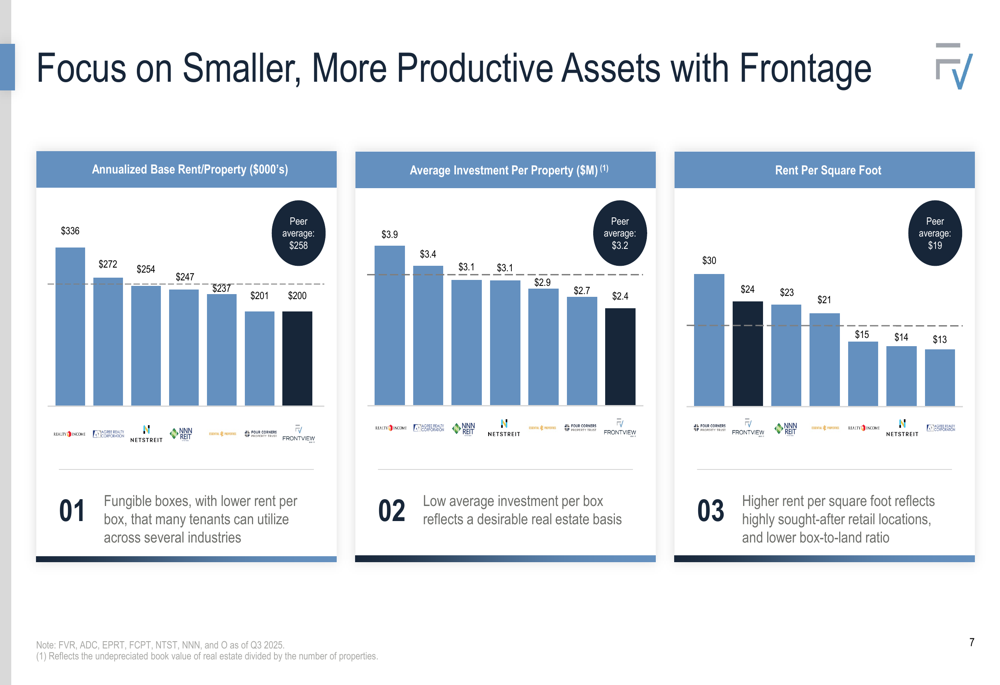

The company’s portfolio consists primarily of smaller properties averaging 8,387 square feet, with an average rent of approximately $200,000 per property. This strategy allows FrontView to maintain higher rent per square foot compared to its peers, reflecting the premium nature of its high-visibility locations.

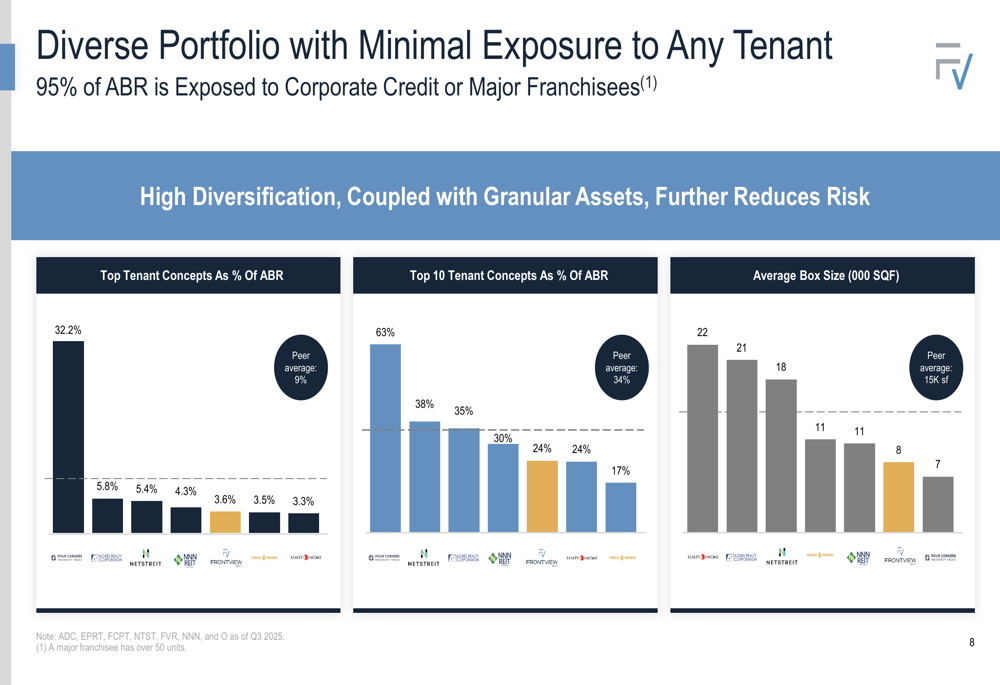

FrontView’s tenant base is well-diversified across industries, with medical and dental providers (15.1%), casual dining (13.0%), and quick service restaurants (12.1%) representing the largest segments. The top 10 tenant concepts account for only 24% of annualized base rent, demonstrating the company’s focus on minimizing tenant concentration risk.

Strategic Capital Partnership

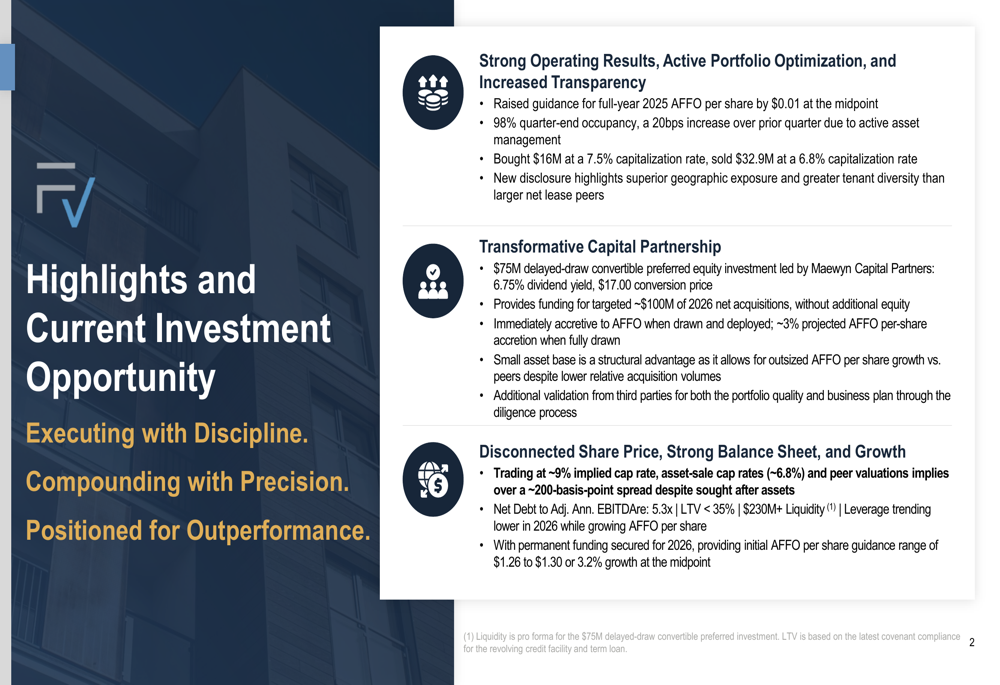

The most significant announcement in the presentation was a $75 million delayed-draw convertible perpetual preferred equity investment led by Maewyn Capital Partners. This strategic capital partnership features a 6.75% dividend yield and a $17.00 conversion price, representing approximately a 30% premium to recent trading prices.

The following slide details the highlights and current investment opportunity:

This capital infusion is expected to fund approximately $100 million of acquisitions in 2026 without requiring additional equity issuance. Management projects this will be immediately accretive to AFFO when drawn and deployed, with approximately 3% projected AFFO per-share accretion when fully drawn.

CEO Pierre Revol emphasized during the earnings call that "having a small size allows us to deliver faster growth than all of our peers," highlighting how this capital partnership enhances the company’s ability to execute its growth strategy while maintaining a conservative balance sheet.

The transaction provides FrontView with increased financial flexibility, bringing total liquidity to $236.1 million while maintaining a loan-to-value ratio below 35%. This strengthened balance sheet positions the company well for continued growth in a competitive market environment.

Portfolio Optimization Strategy

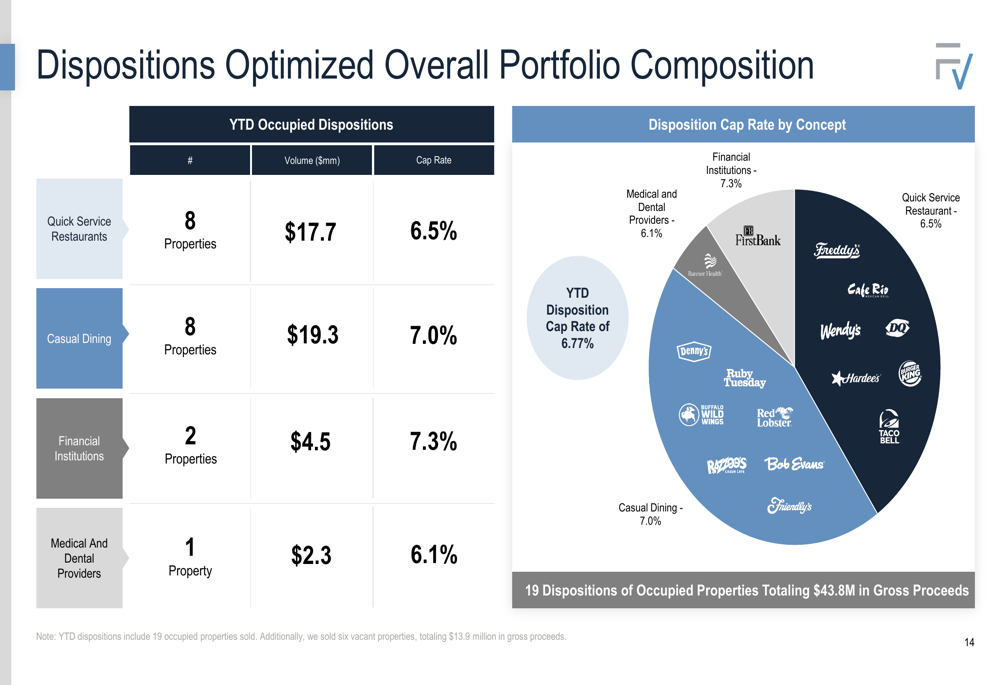

FrontView has been actively optimizing its portfolio through strategic acquisitions and dispositions. Year-to-date, the company has acquired 25 properties at an average economic yield of 8.31%, while selling 19 occupied properties for $43.8 million at an average cap rate of 6.8%.

The following chart illustrates how these dispositions have optimized the overall portfolio composition:

This capital recycling strategy has allowed FrontView to exit less desirable assets while acquiring properties with better long-term growth potential. During Q3 specifically, the company acquired three new properties enhancing its presence in financial, fitness, and discount retail sectors, while selling 15 properties for $32.9 million to eliminate exposure to less profitable restaurant concepts.

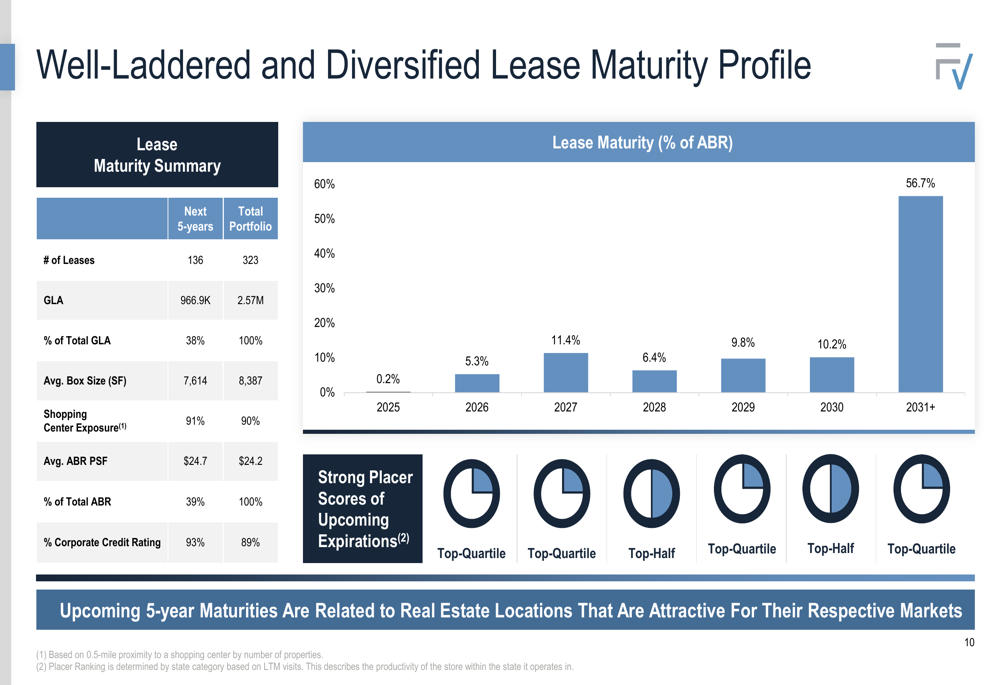

FrontView’s asset management approach is supported by its strong track record on lease renewals, with a 105% recapture rate since 2016. The company’s lease maturity profile is well-laddered, with 56.7% of leases expiring after 2031, providing stable cash flow visibility.

As shown in the following lease maturity profile:

Competitive Positioning

FrontView differentiates itself from peers through its focus on smaller, more productive assets with frontage on high-traffic roads. The company’s properties average 8,387 square feet, significantly smaller than the peer average of approximately 15,000 square feet, but generate higher rent per square foot.

The following chart highlights FrontView’s focus on smaller, more productive assets with frontage:

Another competitive advantage is FrontView’s geographic concentration, with 72% of its properties located in the top 100 Metropolitan Statistical Areas (MSAs), compared to 56% for FCPT and 54% for Agree Realty Corporation. This strategic positioning in higher-growth markets supports stronger long-term rent growth and property values.

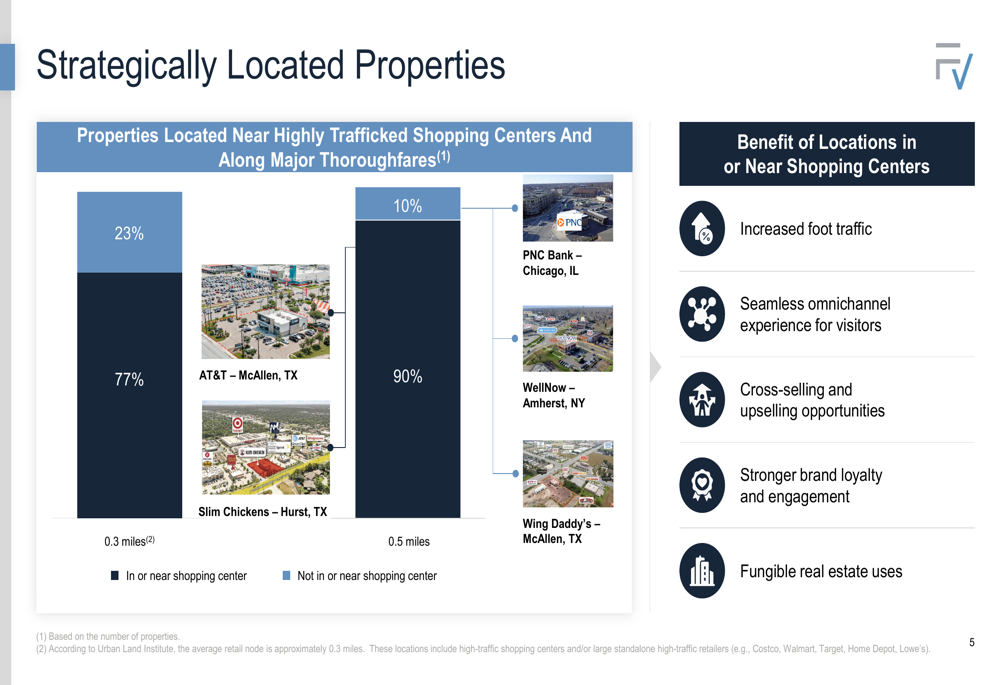

Additionally, 77% of FrontView’s properties are located in or near shopping centers, and 90% are situated along major thoroughfares, providing tenants with high visibility and customer convenience. This positioning is particularly attractive to tenants in essential and experiential retail segments that demand high-profile physical locations.

As illustrated in the following slide on strategically located properties:

The company’s portfolio is also well-diversified, with minimal exposure to any single tenant. This diversification strategy reduces risk and provides multiple growth avenues across different retail sectors.

The following chart demonstrates FrontView’s diverse portfolio with minimal tenant exposure:

Forward-Looking Statements

FrontView has raised its guidance for full-year 2025 AFFO per share by $0.01 at the midpoint, now projecting $1.23-$1.25. Looking ahead to 2026, the company has provided initial AFFO per share guidance of $1.26-$1.30, representing 3.2% growth at the midpoint.

Management expects the $75 million convertible preferred equity investment to enable approximately $100 million of net acquisitions in 2026, representing a roughly 10% increase in the company’s asset base. These acquisitions are projected to be made at an average capitalization rate of approximately 7.5%.

Despite these positive developments, FrontView’s stock continues to trade at an implied cap rate of approximately 9%, representing a significant discount to both its asset-sale cap rates (~6.8%) and peer valuations. Management views this as a compelling opportunity for investors, given the company’s strong balance sheet, improving operational metrics, and clear growth strategy.

CFO Steve Preston highlighted during the earnings call the strategic advantage of the company’s asset portfolio, noting its ability to quickly reposition in response to market dynamics. With its strengthened balance sheet and secured funding for 2026 growth, FrontView appears well-positioned to continue executing its strategy of acquiring high-quality, high-visibility properties while maintaining conservative leverage.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.