Sun Valley Gold sells Vista Gold (VGZ) shares worth $2.16 million

Introduction & Market Context

Fuji Electric Co., Ltd. (TYO:6504) released its consolidated financial results for the first half of fiscal year 2025 on October 30, revealing record-high net sales and operating profit despite challenges in its semiconductor business. The Japanese electrical equipment manufacturer reported strong performance in its Energy and Industry segments, leading to an upward revision of its full-year forecasts.

Despite beating analyst expectations with earnings per share of ¥106.46 against forecasts of ¥102.48, Fuji Electric’s stock declined 3.41% following the announcement, closing at ¥11,450. This suggests investor concerns about rising fixed costs and segment-specific headwinds, particularly in the semiconductor division.

Quarterly Performance Highlights

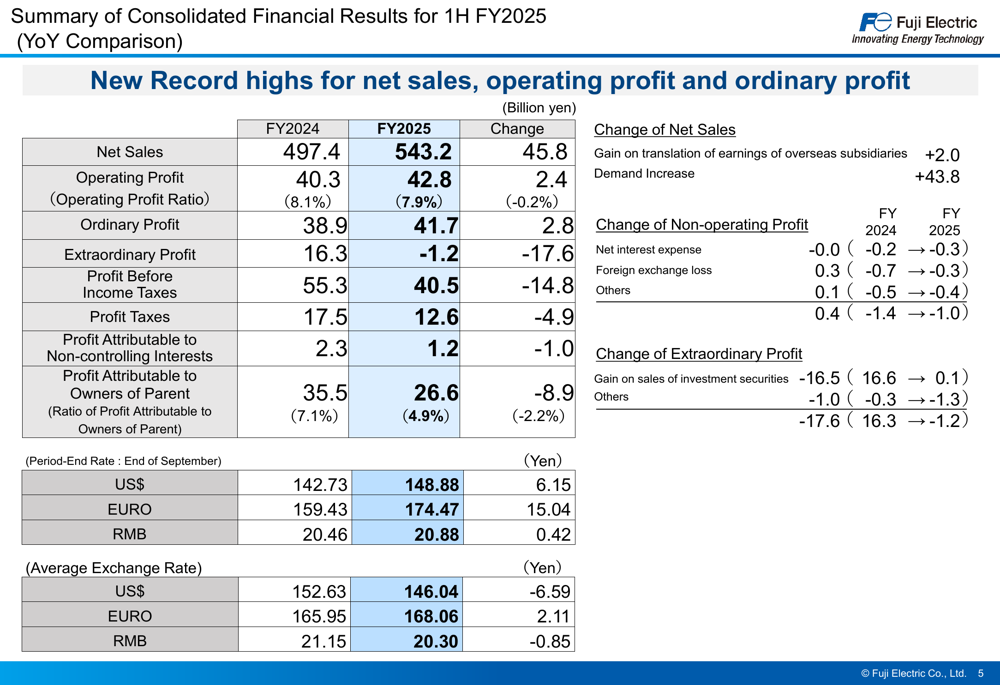

Fuji Electric reported net sales of ¥543.2 billion for the first half of FY2025, representing an increase of ¥45.8 billion (9.2%) year-over-year. Operating profit rose by ¥2.4 billion to ¥42.8 billion, though the operating profit ratio slightly decreased by 0.2 percentage points to 7.9%.

As shown in the following summary of consolidated financial results, profit attributable to owners of parent declined significantly by ¥8.9 billion to ¥26.6 billion, largely due to a ¥17.6 billion decrease in extraordinary profit compared to the previous year:

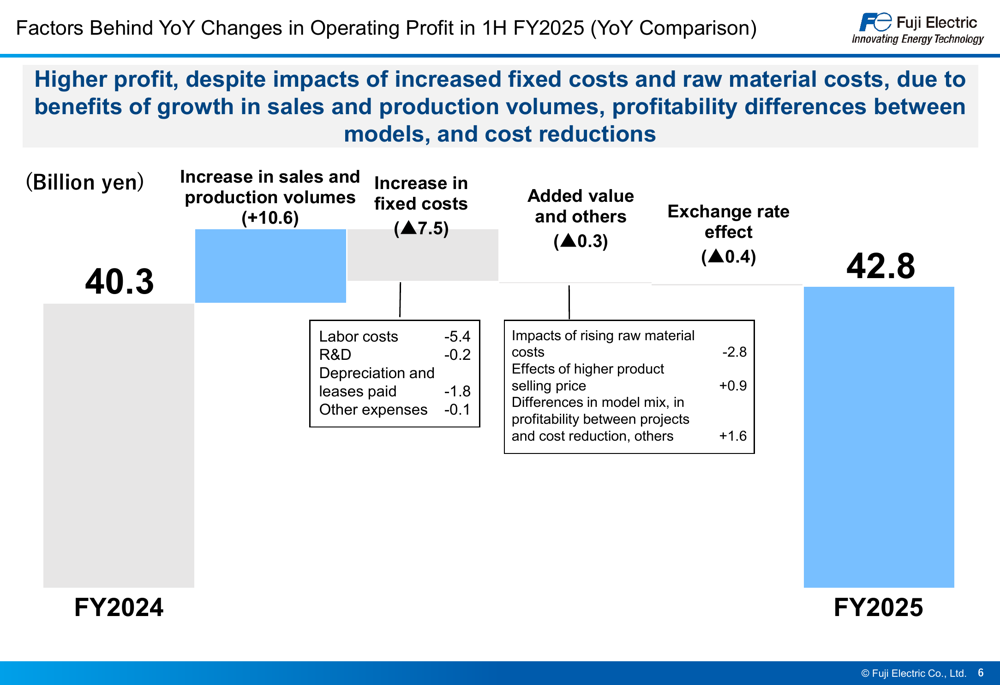

The company’s operating profit growth was driven by increased sales and production volumes (+¥10.6 billion), partially offset by higher fixed costs (-¥7.5 billion) and rising raw material costs. The following chart illustrates these factors:

Orders showed remarkable growth, reaching ¥684.9 billion, an increase of ¥113.2 billion year-over-year. This was primarily driven by strong performance in plant and system operations of the Energy and Industry segments, with particularly strong demand for thermal and geothermal power plants, data centers, transportation systems, and academic sector projects.

Segment Analysis

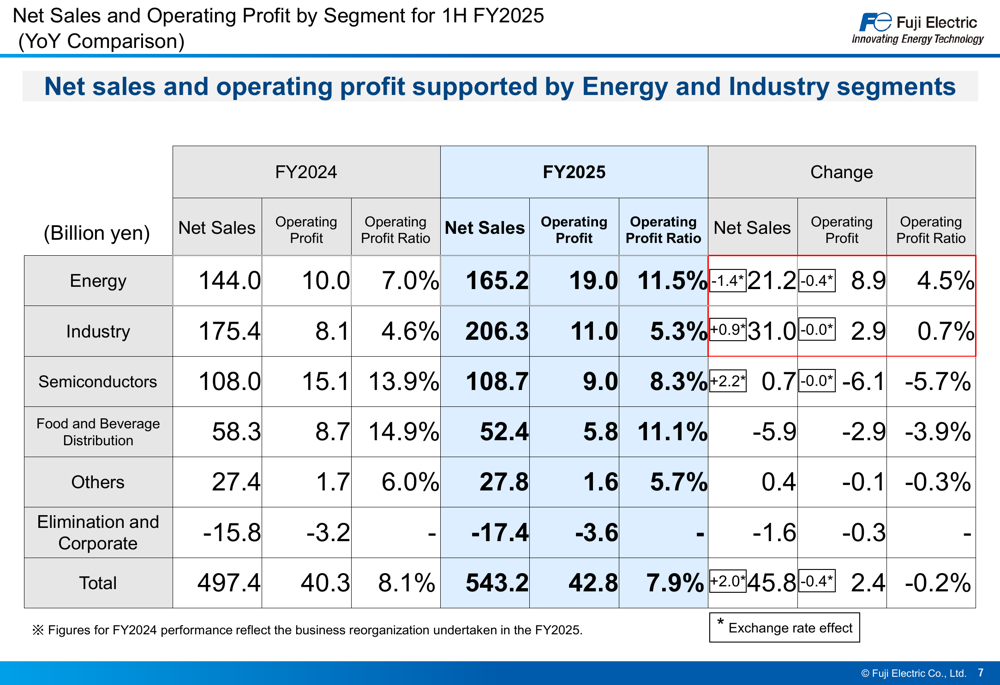

Fuji Electric’s performance varied significantly across its business segments, with Energy and Industry driving growth while Semiconductors and Food & Beverage Distribution faced challenges.

The Energy segment saw substantial growth with net sales increasing by ¥21.2 billion to ¥165.2 billion and operating profit surging by ¥8.9 billion to ¥19.0 billion. The Industry segment also performed well, with net sales rising by ¥31.0 billion to ¥206.3 billion and operating profit increasing by ¥2.9 billion to ¥11.0 billion.

The following breakdown illustrates the performance across all segments:

However, the Semiconductors segment faced significant challenges despite a slight increase in net sales to ¥108.7 billion (+¥0.7 billion). Operating profit in this segment fell sharply by ¥6.1 billion to ¥9.0 billion, with the operating profit ratio declining by 5.7 percentage points to 8.3%. This decline was primarily attributed to reduced demand in the automotive sector.

The Food and Beverage Distribution segment also experienced a decline, with net sales decreasing by ¥5.9 billion to ¥52.4 billion and operating profit falling by ¥2.9 billion to ¥5.8 billion. The company attributed this to a reactionary decline from last year’s special demand in vending machines and store distribution.

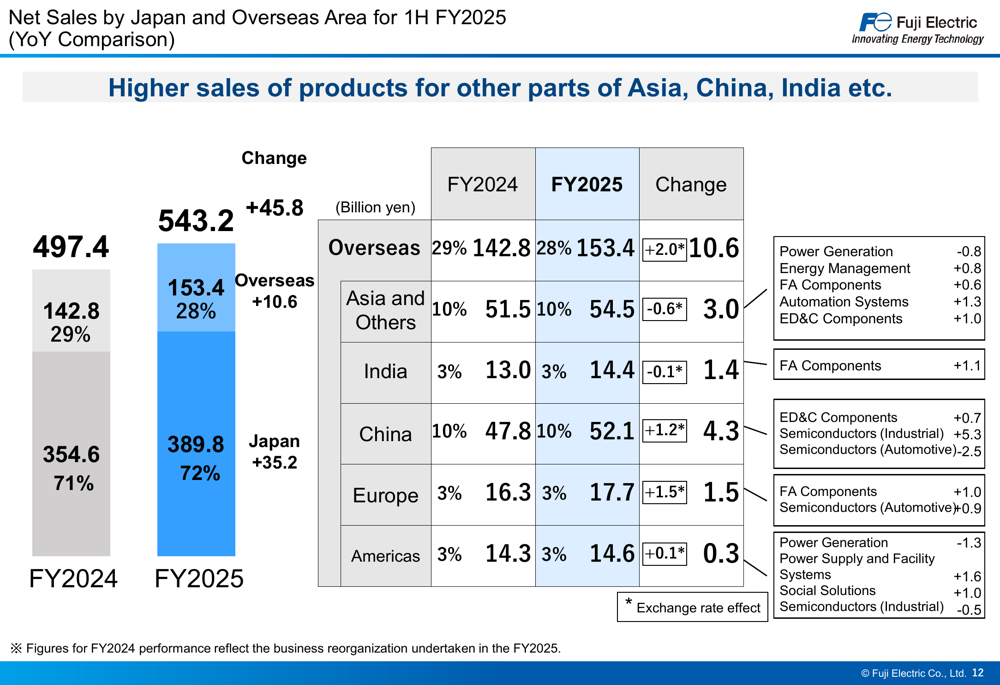

In terms of geographic distribution, domestic sales in Japan accounted for 72% of total sales at ¥389.8 billion (+¥35.2 billion YoY), while overseas sales represented 28% at ¥153.4 billion (+¥10.6 billion YoY):

Revised Forecasts

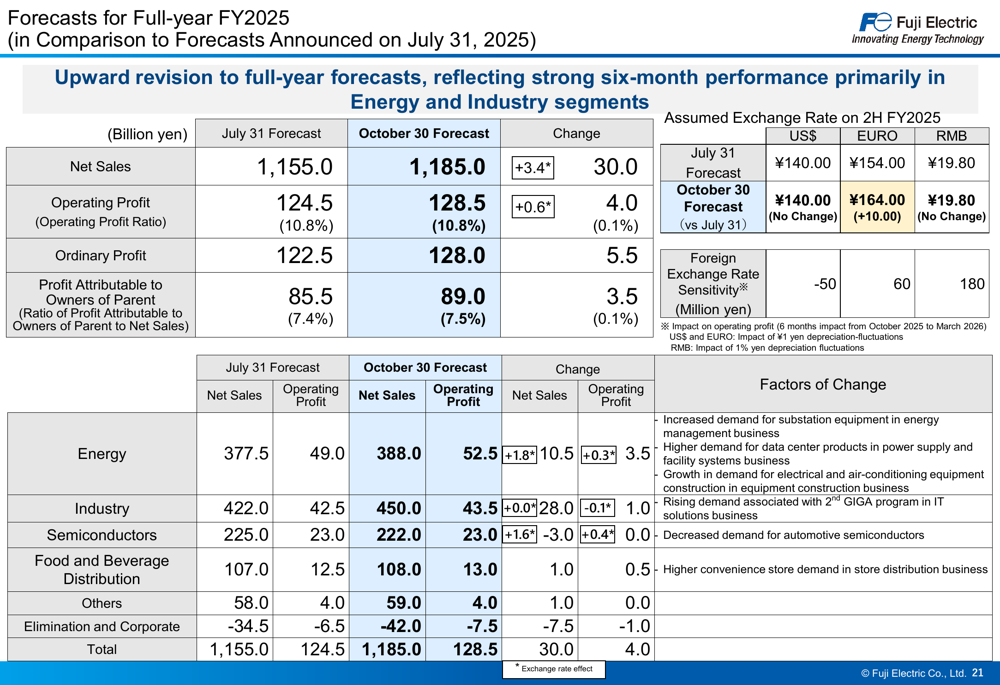

Based on the strong first-half performance, Fuji Electric revised its full-year FY2025 forecasts upward compared to projections announced on July 31. The company now expects net sales of ¥1,185.0 billion (up ¥30.0 billion from previous forecast) and operating profit of ¥128.5 billion (up ¥4.0 billion):

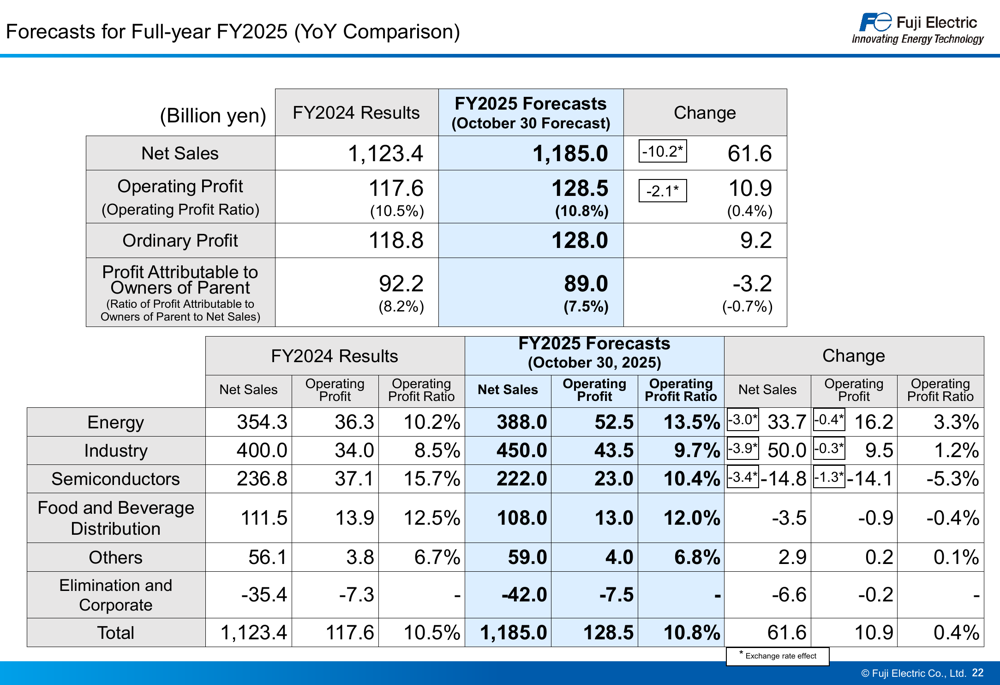

Year-over-year, the revised forecasts represent an increase of ¥61.6 billion in net sales and ¥10.9 billion in operating profit compared to FY2024 results:

The company also announced an interim dividend payment of ¥91 per share, up ¥16 from the previous year, as it pursues a full-year dividend payout ratio target of 30%.

Financial Position and Outlook

Fuji Electric’s balance sheet showed total assets of ¥1,304.9 billion as of September 30, 2025, a decrease of ¥7.3 billion from March 31. Total liabilities decreased by ¥32.2 billion to ¥549.4 billion, while net assets increased by ¥24.9 billion to ¥755.6 billion. The equity ratio improved by 2.2 percentage points to 54.9%.

The company’s cash flow position weakened compared to the previous year, with operating cash flow decreasing to ¥35.9 billion from ¥87.5 billion in FY2024. Cash flows from investing activities were -¥44.6 billion, resulting in a negative free cash flow of -¥8.7 billion, compared to a positive ¥61.8 billion in the previous year.

Despite the overall positive results and upward revision of forecasts, investors appear concerned about rising fixed costs, challenges in the semiconductor segment, and the negative free cash flow. As noted in the earnings call transcript, while Fuji Electric surpassed both EPS and revenue forecasts for Q2 2025, the stock’s decline suggests the market is focusing on these underlying challenges rather than the headline growth figures.

Looking ahead, Fuji Electric’s management remains optimistic about continued strong performance in the Energy and Industry segments, while acknowledging the need to address issues in the Semiconductors business, particularly related to automotive demand. The company’s strong order book of ¥684.9 billion provides a solid foundation for future growth, especially in plant and system operations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.