Asia FX steady as Fed, BOJ rate decisions loom; US-China talks in focus

Introduction & Market Context

Genuine Parts Company (NYSE:GPC) released its first quarter 2025 earnings presentation on April 22, showing modest sales growth but declining profitability metrics. The company reported global sales of $5.9 billion, up 1.4% year-over-year despite being negatively impacted by one less selling day in the quarter. GPC shares were up 1.95% in premarket trading following the release, with the stock trading at $114, after closing at $111.82 the previous day.

The results come as GPC navigates what management described as a "dynamic external environment," with the company focusing on controlling what it can while executing strategic initiatives. This follows a challenging fourth quarter 2024, when the company reported mixed results that saw its stock approaching 52-week lows.

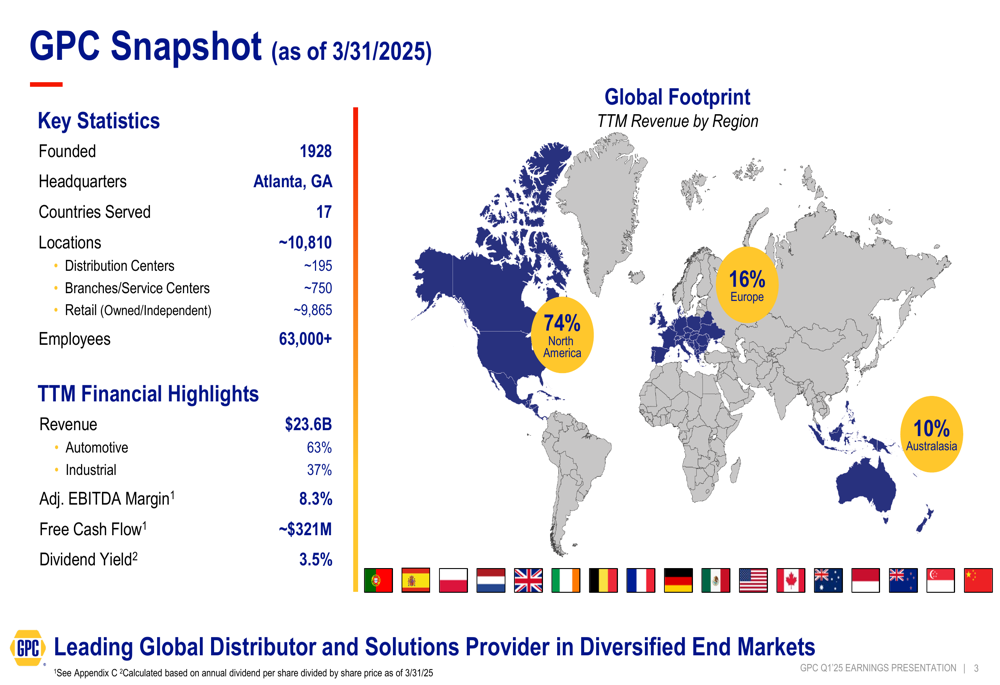

As shown in the company snapshot below, GPC operates as a leading global distributor in automotive and industrial markets across 17 countries, with approximately 10,810 locations and 63,000+ employees:

Quarterly Performance Highlights

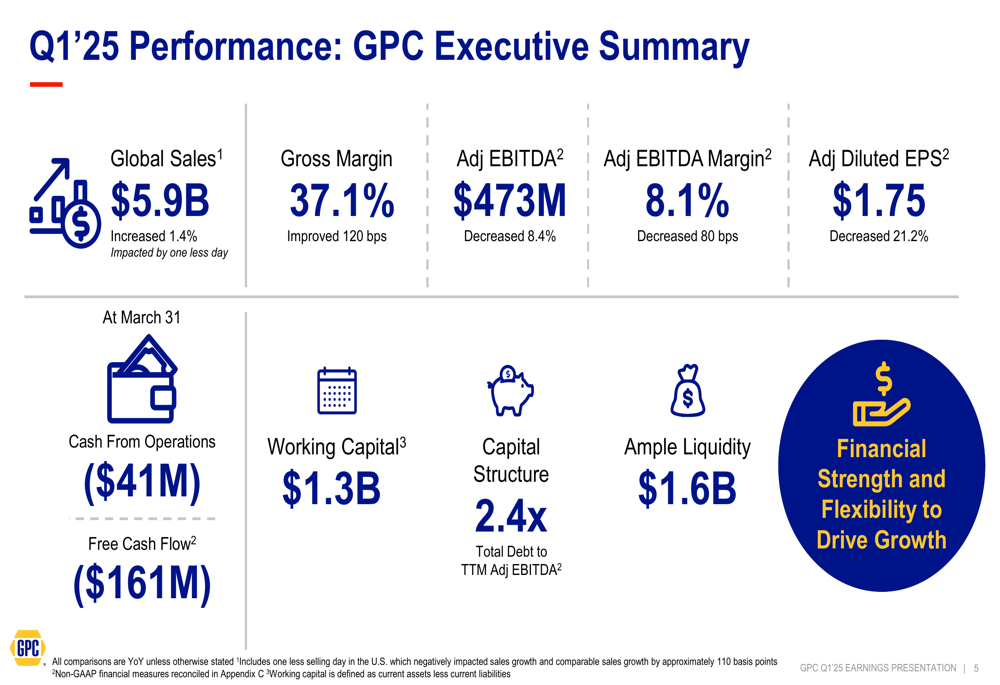

GPC’s first quarter results showed a divergence between top-line growth and bottom-line performance. While sales increased modestly, profitability metrics declined significantly year-over-year. The company reported gross margin improvement of 120 basis points to 37.1%, but adjusted EBITDA decreased 8.4% to $473 million, with adjusted EBITDA margin contracting 80 basis points to 8.1%. Adjusted diluted EPS fell 21.2% to $1.75.

The executive summary below highlights these key performance metrics:

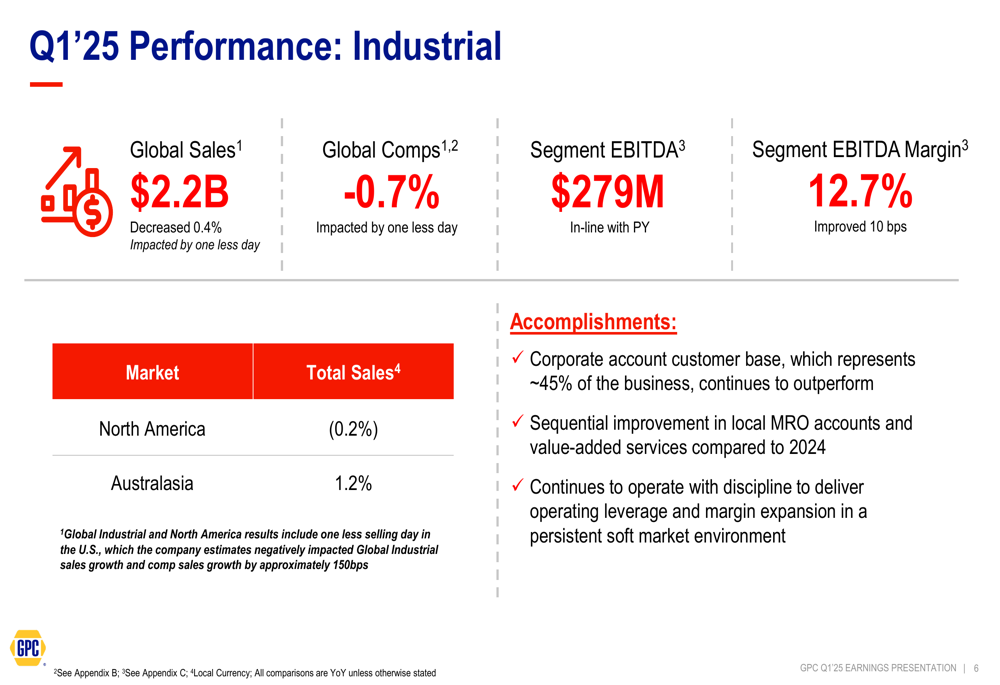

The company’s performance varied significantly between its two main segments. The Industrial segment showed resilience with global sales of $2.2 billion, down slightly by 0.4%, while segment EBITDA of $279 million was in-line with the prior year. Segment EBITDA margin actually improved by 10 basis points to 12.7%. Management noted that corporate account customers continued to outperform, with sequential improvement in local MRO accounts and value-added services.

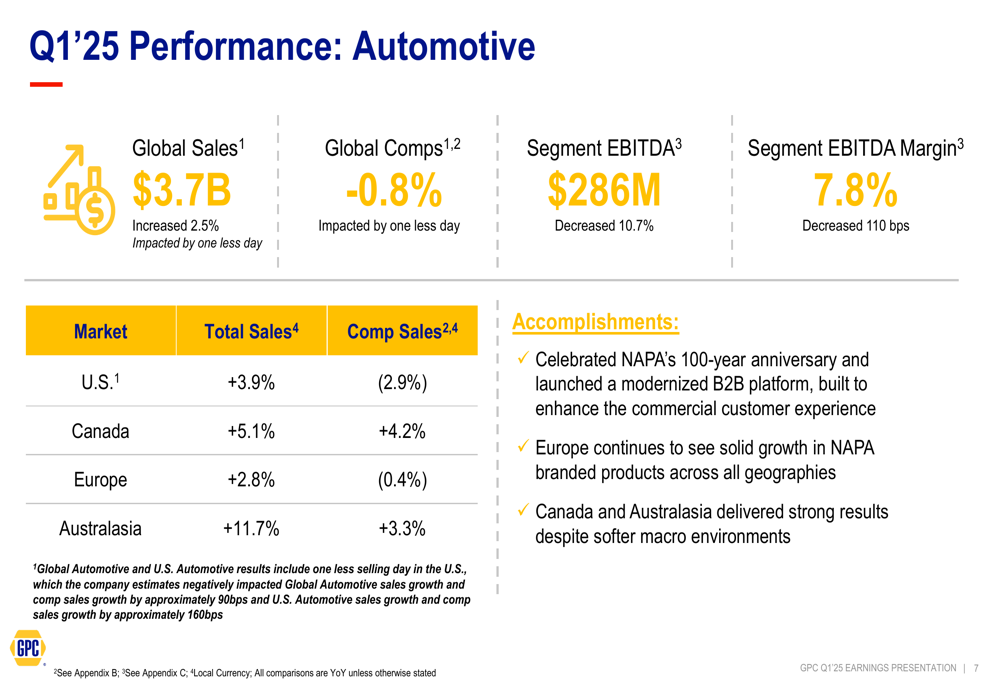

In contrast, the Automotive segment faced more significant challenges despite higher sales. Global Automotive sales increased 2.5% to $3.7 billion, but segment EBITDA decreased 10.7% to $286 million, with segment EBITDA margin declining 110 basis points to 7.8%. The company highlighted NAPA’s upcoming 100-year anniversary and the launch of a modernized B2B platform as positive developments, along with solid growth in Europe and strong results in Canada and Australasia.

Detailed Financial Analysis

A closer examination of GPC’s financial performance reveals both strengths and challenges. The company’s cash position deteriorated in the first quarter, with cash from operations at negative $41 million and free cash flow at negative $161 million. Working capital stood at $1.3 billion, while the company maintained a leverage ratio of 2.4x total debt to TTM adjusted EBITDA, with ample liquidity of $1.6 billion.

The decline in profitability metrics appears consistent with management’s previous guidance during the Q4 2024 earnings call, where they projected first-half 2025 earnings to decline by 15-20%. The 21.2% drop in adjusted EPS for Q1 is at the higher end of this range, suggesting continued pressure on margins despite sales growth.

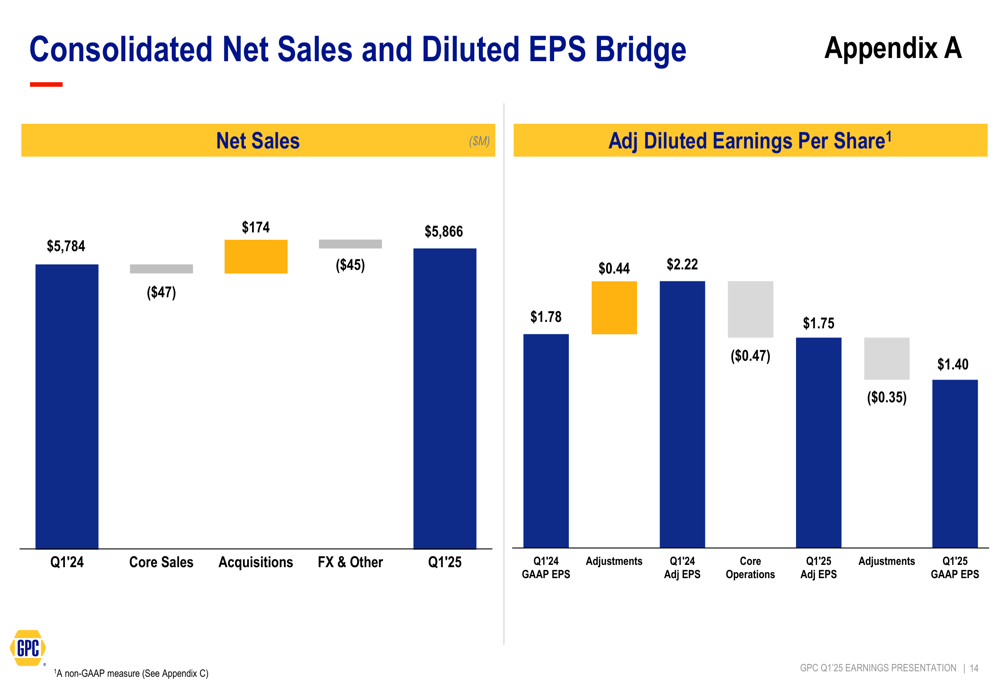

Looking at the consolidated net sales and diluted EPS bridge provides further insight into the factors affecting performance:

The bridge shows that core sales declined by $47 million compared to Q1 2024, but this was offset by acquisitions (+$174 million) and partially reduced by FX & Other (-$45 million). On the earnings side, core operations negatively impacted adjusted diluted EPS by $0.47, with additional adjustments of $0.35, resulting in a significant year-over-year decline.

Strategic Initiatives

Despite near-term challenges, GPC continues to invest in strategic priorities to drive long-term growth. The company outlined its investment focus areas, including talent & culture, sales effectiveness, supply chain modernization, and emerging technology:

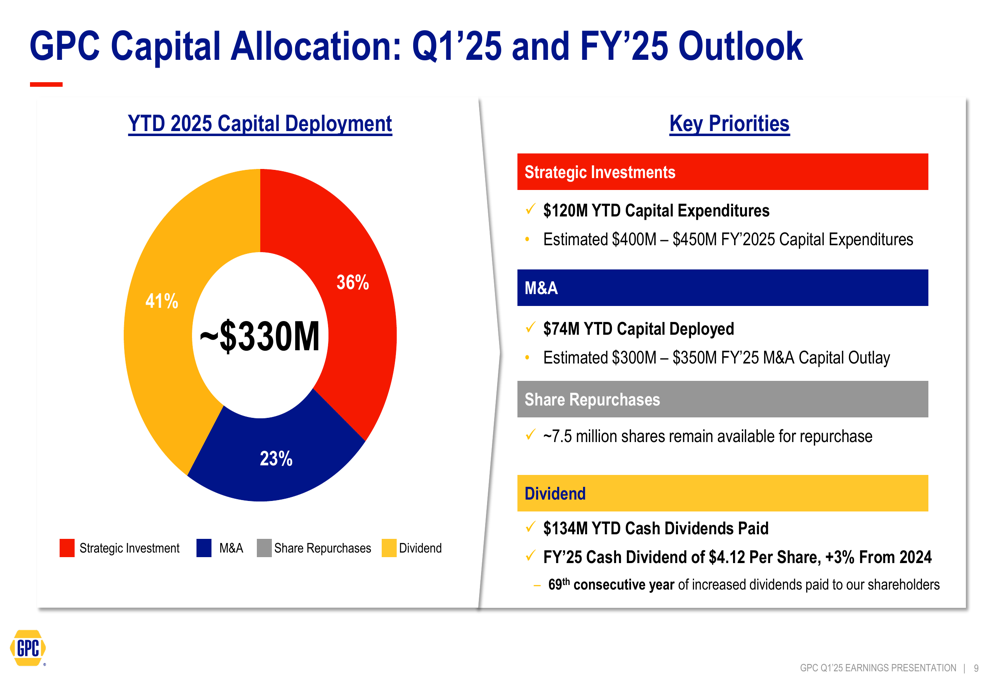

GPC’s capital allocation strategy for Q1 2025 balanced investments in the business with shareholder returns. The company deployed approximately $330 million, with 41% going to strategic investments, 36% to M&A, and 23% to share repurchases. Key priorities included $120 million in capital expenditures, $74 million for M&A, and $134 million in cash dividends paid.

The company’s M&A strategy appears to be continuing the momentum from 2024, when it completed the acquisition of more than 500 stores, mostly from independent owners. The current U.S. store footprint is approximately 35% company-owned, with management indicating a path toward a 50/50 mix over time.

Forward-Looking Statements

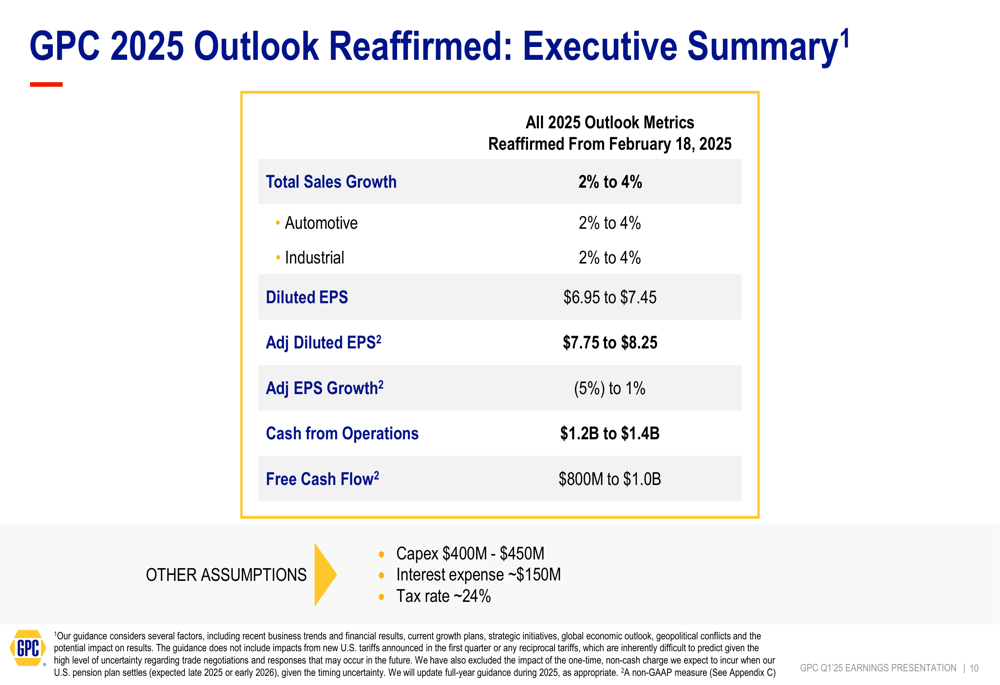

Despite the challenging first quarter, GPC reaffirmed its full-year 2025 outlook, projecting total sales growth of 2% to 4% across both Automotive and Industrial segments. The company expects adjusted diluted EPS of $7.75 to $8.25, representing adjusted EPS growth of -5% to 1%. Cash from operations is projected at $1.2 billion to $1.4 billion, with free cash flow of $800 million to $1.0 billion.

The detailed outlook is presented in the following slide:

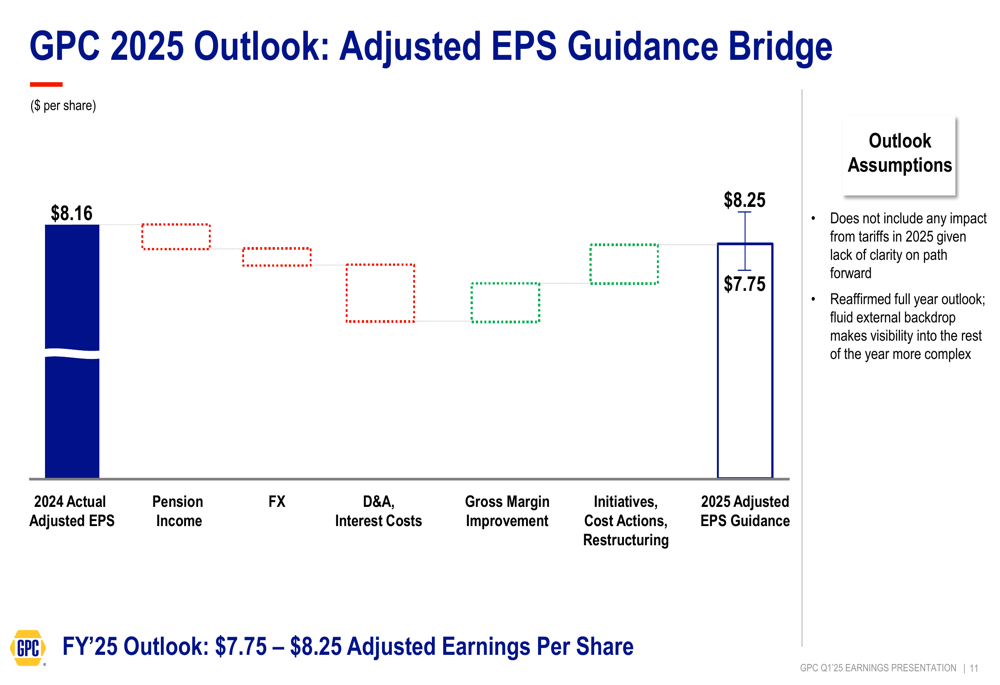

Management provided additional context for the adjusted EPS guidance through a bridge illustration, showing the impact of various factors on the year-over-year comparison:

The outlook assumes no impact from potential tariffs in 2025, though management acknowledged in the Q4 2024 earnings call that the company has exposure to China (7% of purchases), Mexico (less than 5%), and Canada (less than 5%). The reaffirmed guidance comes despite what management described as a "fluid external backdrop making visibility into the rest of the year more complex."

In conclusion, while GPC faces near-term profitability challenges, particularly in its Automotive segment, the company maintains a focus on strategic investments and operational discipline to navigate the current environment. The reaffirmed full-year outlook suggests management’s confidence in improved performance as 2025 progresses, consistent with their previous expectation for a stronger second half of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.