SoFi stock falls after announcing $1.5B public offering of common stock

Introduction & Market Context

Geron Corporation (NASDAQ:GERN) presented its Q3 2025 earnings results on November 5, revealing mixed performance as the company continues commercializing its flagship drug RYTELO for lower-risk myelodysplastic syndrome (MDS). The biopharmaceutical company reported revenue that fell short of analyst expectations, contributing to a decline in its stock price, which dropped 4.17% to $1.11 in pre-market trading, approaching its 52-week low of $1.09.

The company's presentation highlighted both challenges in RYTELO's commercial execution and positive developments in its clinical pipeline, as management attempts to navigate the competitive hematology-oncology landscape while preserving its strong cash position.

Quarterly Performance Highlights

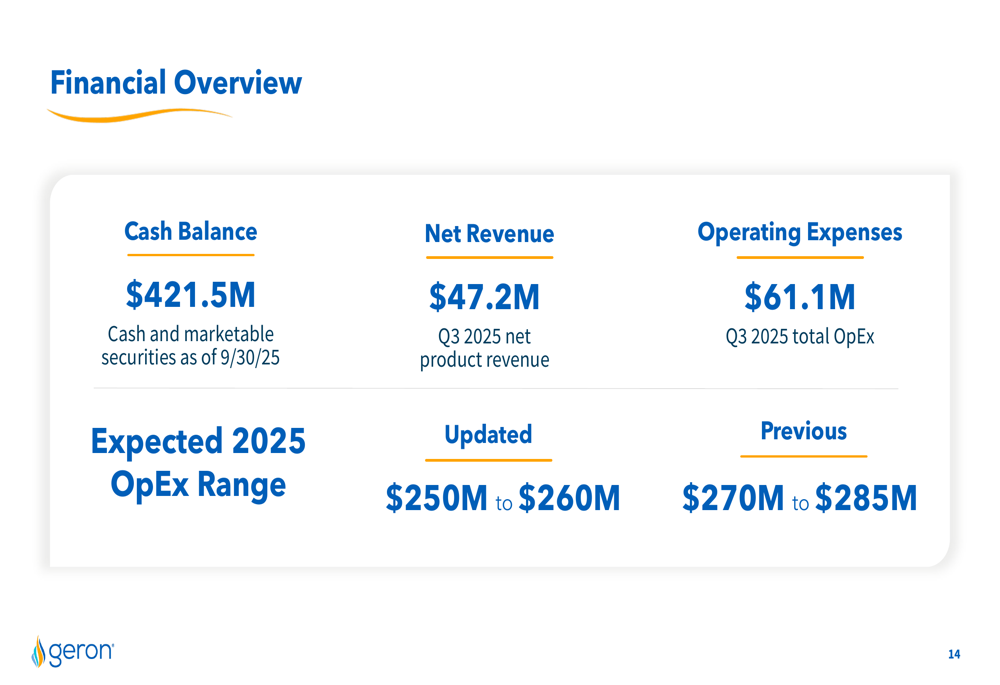

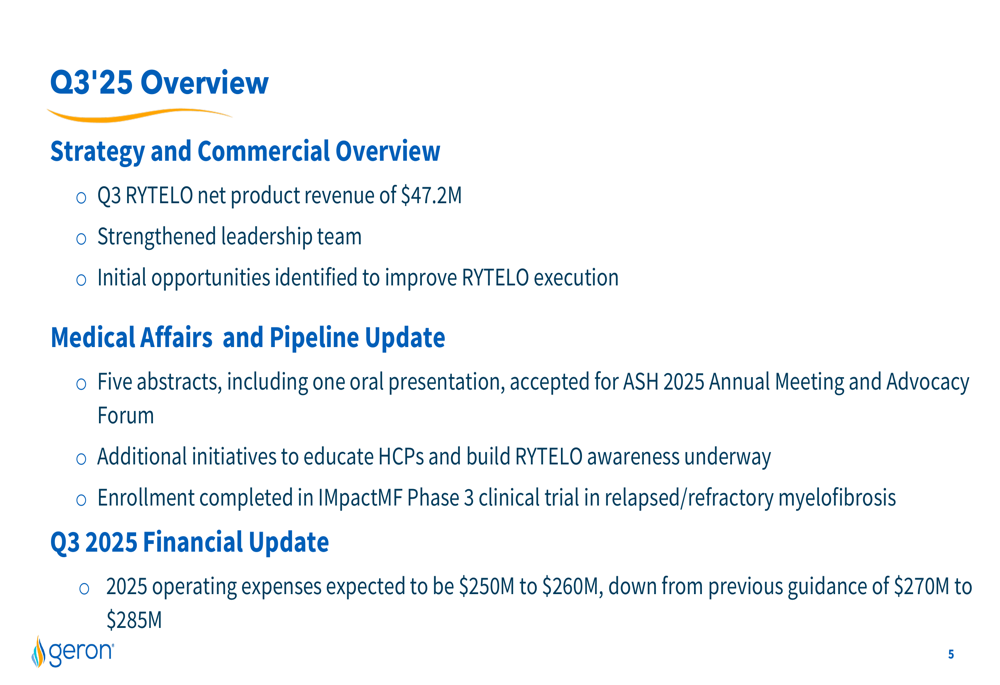

Geron reported Q3 2025 net product revenue of $47.2 million for RYTELO, representing significant year-over-year growth from $28 million in Q3 2024, but falling 13.38% below analyst expectations of $54.49 million. The company met earnings per share expectations at -$0.03.

As shown in the following financial overview:

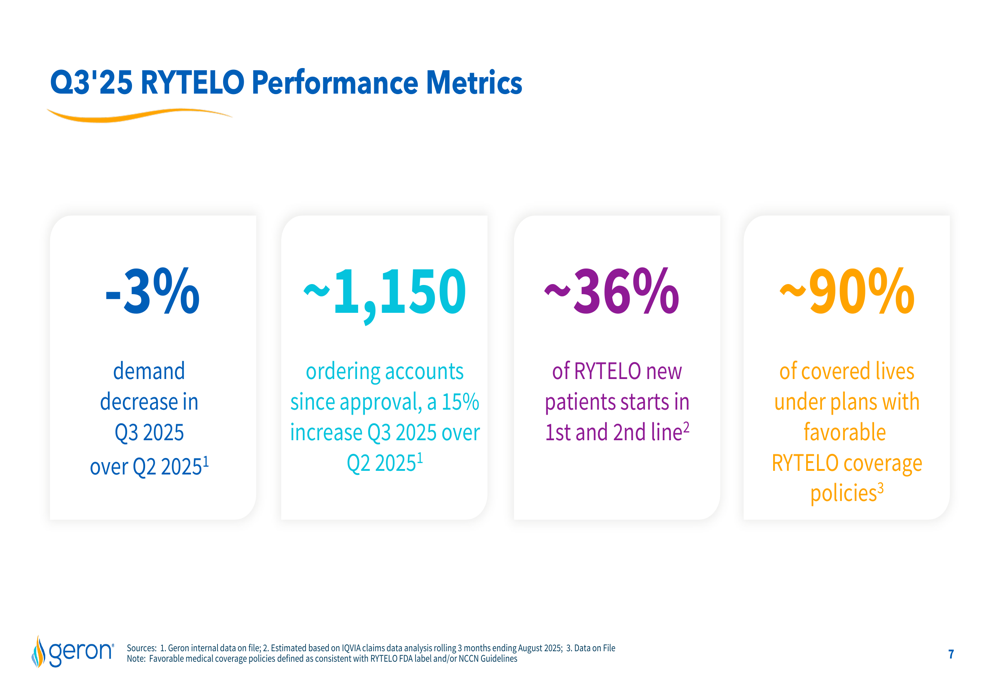

The quarterly results revealed concerning commercial trends for RYTELO, including a 3% demand decrease in Q3 2025 compared to Q2 2025. Despite this setback, the company highlighted some positive indicators, including a 15% quarter-over-quarter increase in ordering accounts to approximately 1,150 since approval, and favorable insurance coverage with about 90% of covered lives under plans with positive RYTELO coverage policies.

The following slide details these key performance metrics:

Strategic Initiatives & Commercial Challenges

Acknowledging execution challenges with RYTELO, Geron's management outlined several strategic initiatives aimed at improving commercial performance. CEO Harout Semerjian emphasized that "RYTELO is a drug that works" and that "with the right execution, we believe it can be positioned for long-term success," suggesting the company recognizes the need for improved implementation rather than issues with the product itself.

The company identified specific areas for commercial improvement, including enhanced healthcare provider education, increased presence at hematology forums, and expansion of investigator-sponsored trials to build broader clinical experience with RYTELO.

As illustrated in this strategic foundation slide:

The company is particularly focused on increasing RYTELO adoption in earlier treatment lines, noting that approximately 36% of new patient starts are currently in first and second line settings, representing a potential growth opportunity.

Pipeline & Medical Affairs Updates

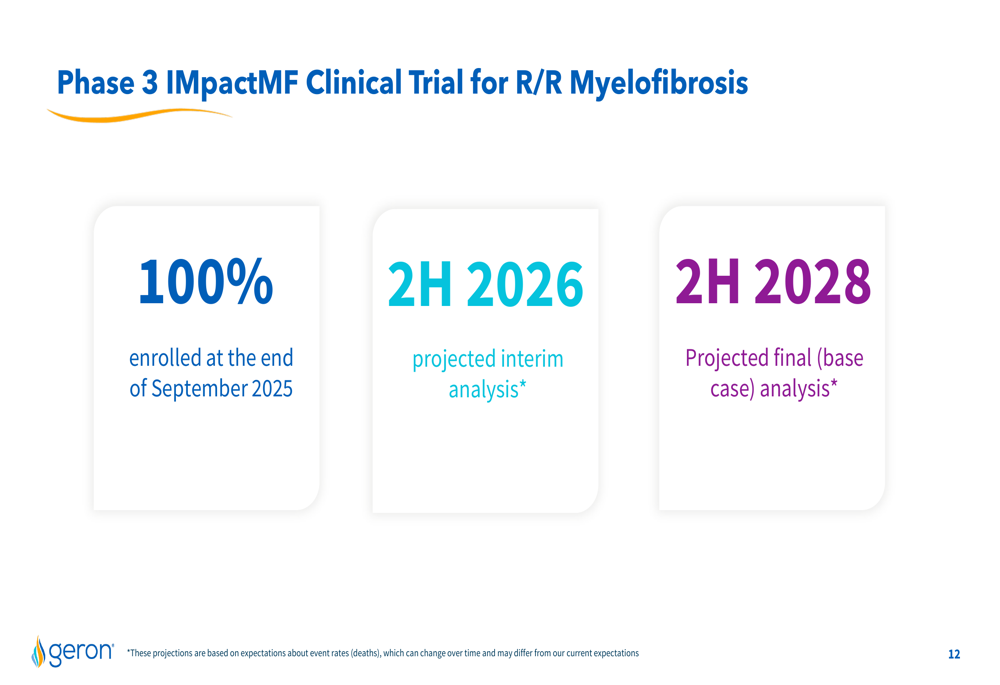

Geron reported significant progress with its clinical pipeline, most notably the completion of enrollment in its Phase 3 IMpactMF clinical trial for relapsed/refractory myelofibrosis. This milestone positions the company for potential data readouts in the coming years, with an interim analysis projected for the second half of 2026 and final analysis expected in the second half of 2028.

The timeline for this important trial is shown here:

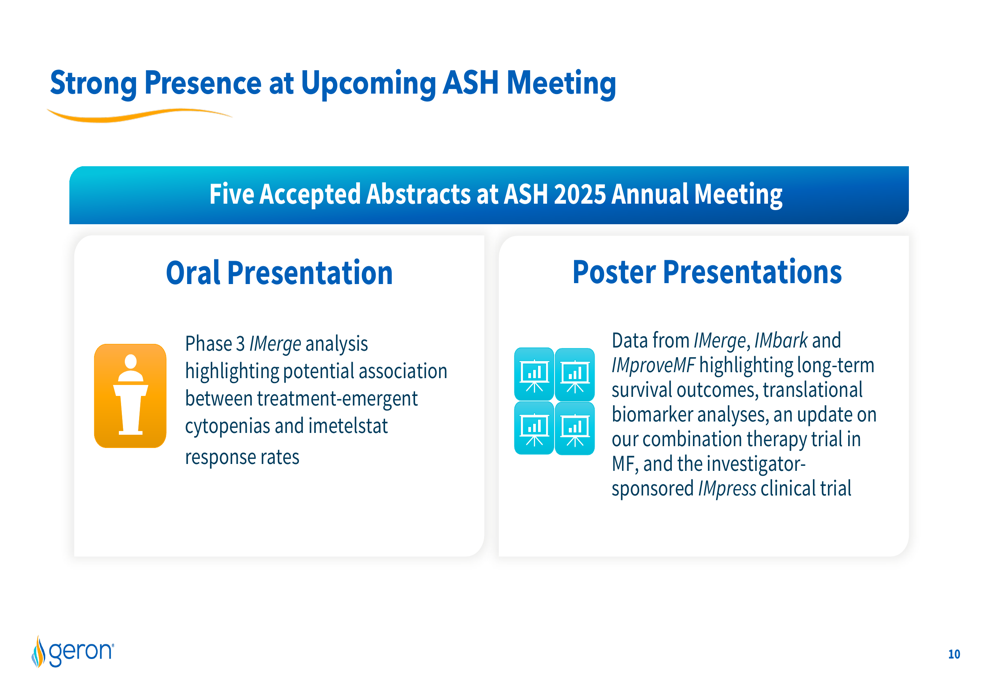

Additionally, the company announced a strong presence at the upcoming American Society of Hematology (ASH) 2025 Annual Meeting, with five abstracts accepted, including one oral presentation. These presentations will focus on analyses from the Phase 3 IMerge trial, highlighting potential associations between treatment-emergent cytopenias and imetelstat response rates, as well as long-term survival outcomes and biomarker analyses.

The following slide outlines Geron's upcoming ASH presentations:

To support RYTELO's growth, Geron is implementing several medical affairs initiatives focused on community site penetration, awareness and education, investigator-sponsored trials, and key opinion leader alignment. These efforts aim to address the commercial challenges by building stronger scientific support and clinical experience with the drug.

Financial Position & Outlook

Despite the revenue shortfall, Geron maintains a strong financial position with $421.5 million in cash and marketable securities as of September 30, 2025. This substantial cash reserve provides runway for continued commercial and clinical development activities.

In response to the commercial challenges, the company has revised its 2025 operating expense guidance downward to $250-260 million from the previous range of $270-285 million, indicating efforts to manage costs more efficiently while addressing execution issues.

The comprehensive quarterly overview provides context for these adjustments:

Conclusion

Geron's Q3 2025 results reveal a company at a critical juncture in its commercial journey with RYTELO. While the revenue miss and declining quarter-over-quarter demand raise concerns about market penetration and execution, the company's strong cash position, pipeline progress, and strategic adjustments suggest management is taking proactive steps to address these challenges.

Looking ahead to 2026, which management has positioned as a growth year, investors will be watching closely to see if the company's enhanced commercial execution and medical affairs initiatives can reverse the current trend and accelerate RYTELO adoption, particularly in earlier treatment lines. Meanwhile, progress in the IMpactMF trial represents a significant potential catalyst for the company's long-term prospects in the broader myelofibrosis market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.