DoD tests AI models that make it easy to switch from vendors like Palantir

Gibraltar Industries (NASDAQ:ROCK) reported solid first-quarter 2025 results, with significant earnings growth despite essentially flat sales, according to the company’s earnings presentation released on April 30. The building products manufacturer achieved 19% growth in adjusted earnings per share while continuing to execute on strategic acquisitions and share repurchases.

Quarterly Performance Highlights

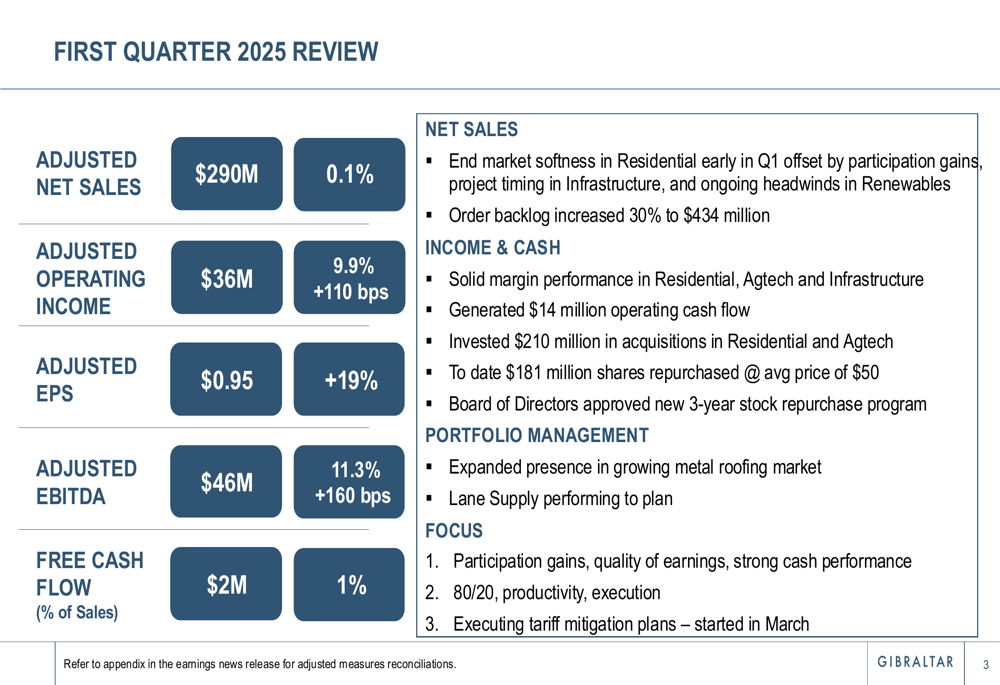

Gibraltar reported Q1 2025 adjusted net sales of $290 million, a marginal increase of 0.1% compared to the prior year. Despite the flat top-line performance, the company delivered impressive bottom-line growth with adjusted operating income of $36 million (up 9.9%), adjusted EBITDA of $46 million (up 11.3%), and adjusted earnings per share of $0.95 (up 19%).

As shown in the following quarterly performance summary:

The company’s order backlog increased 30% to $434 million, suggesting potential revenue acceleration in future quarters. Free cash flow was $2 million, representing 1% of sales, while operating cash flow reached $14 million.

Performance varied significantly across Gibraltar’s four business segments, with Agtech showing the strongest growth while Renewables faced the most significant challenges.

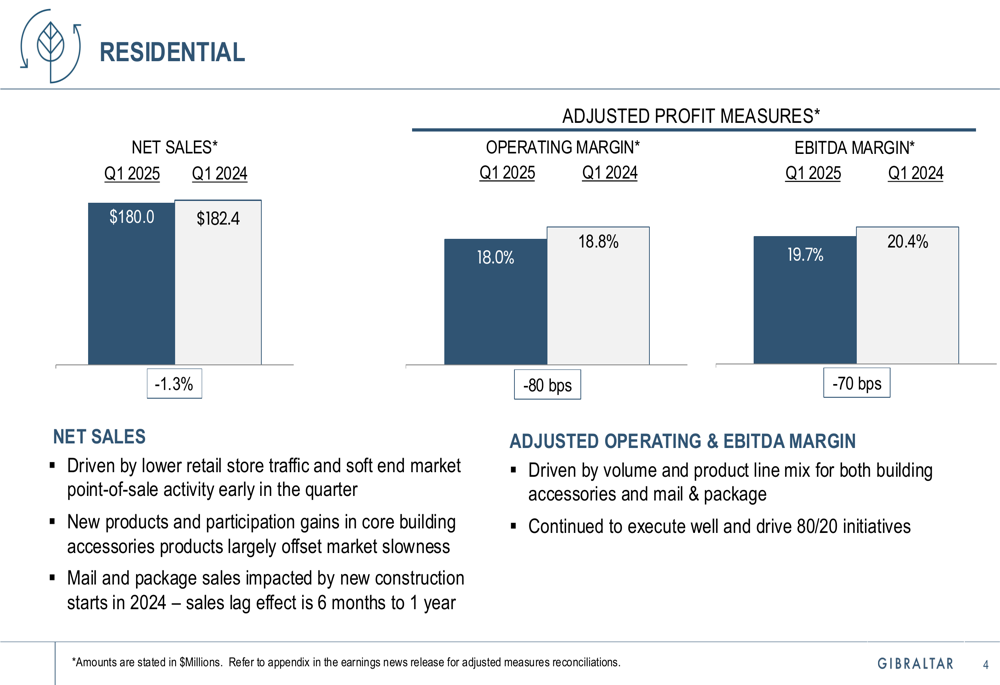

The Residential segment, Gibraltar’s largest business unit, reported sales of $180 million, down 1.3% year-over-year, with adjusted operating margin contracting to 18.0% from 18.8% in Q1 2024. The company attributed this performance to lower retail store traffic and soft end market activity, noting that store foot traffic was down 6-8% in February with some recovery in March.

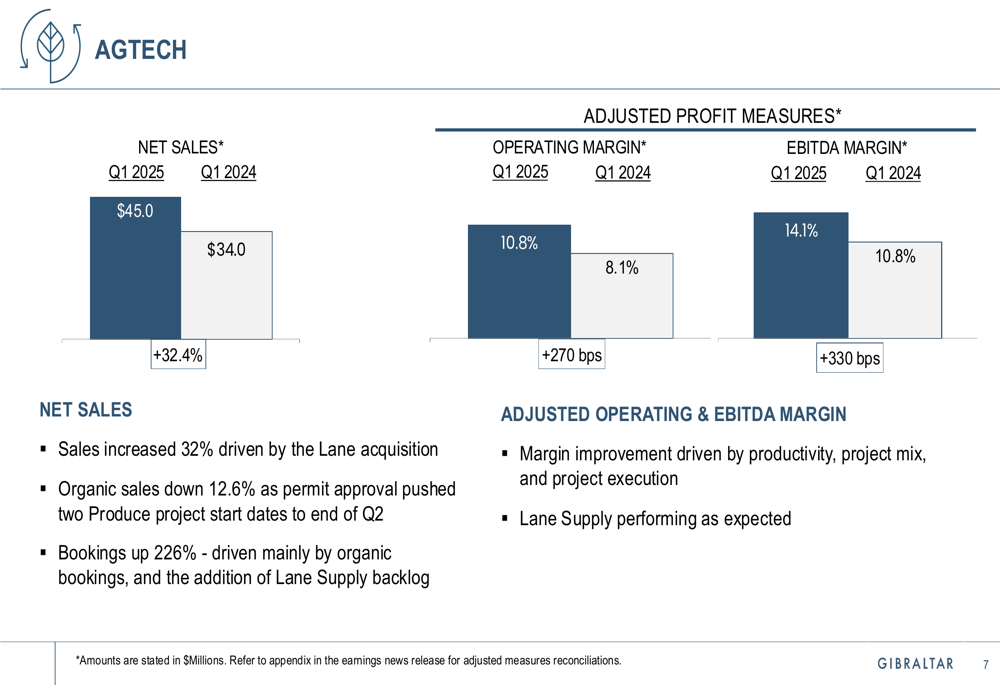

The Agtech segment delivered the strongest performance with sales of $45 million, up 32.4% year-over-year, driven primarily by the Lane acquisition. Organic sales declined 12.6% due to permit approvals pushing two produce projects to the end of Q2. Operating margin improved significantly to 10.8% from 8.1% in the prior year.

The Renewables segment faced the most significant challenges, with sales declining 15.1% to $43.7 million and operating margin contracting to 3.4% from 3.9%. The company cited lower bookings and backlog in the second half of 2024 as the primary cause, though noted that bookings accelerated in Q1, up 90% sequentially.

The Infrastructure segment reported a 2.7% sales decline to $21.3 million due to project delays, but delivered strong margin improvement with operating margin expanding to 24.7% from 22.4% in the prior year.

Strategic Initiatives

Gibraltar completed two strategic acquisitions on March 31 to expand its metal roofing business, investing $90 million in companies specializing in metal roofing systems, wall panels, and trim products. These acquisitions, with combined annual sales of $73 million and adjusted EBITDA margin of 17.8%, support the company’s building product localization strategy in the Southeast and Rocky Mountain regions.

The company highlighted the attractiveness of the metal roofing market, noting growth driven by the substitution effect, attractive margins, and increasing mainstream adoption:

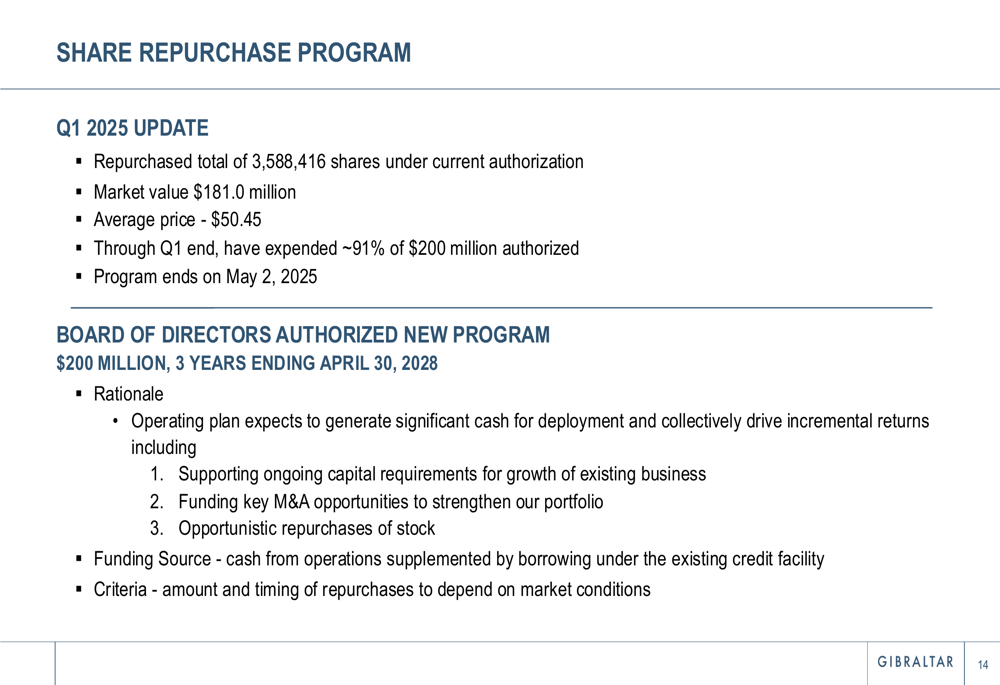

Gibraltar also continued its aggressive share repurchase program, buying back 915,000 shares in Q1 at an average price of $50.45. Through the end of Q1, the company had repurchased approximately 3.59 million shares for $181 million, representing about 91% of its authorized $200 million program. The Board of Directors has authorized a new $200 million share repurchase program for the next three years ending April 30, 2028.

Forward-Looking Statements

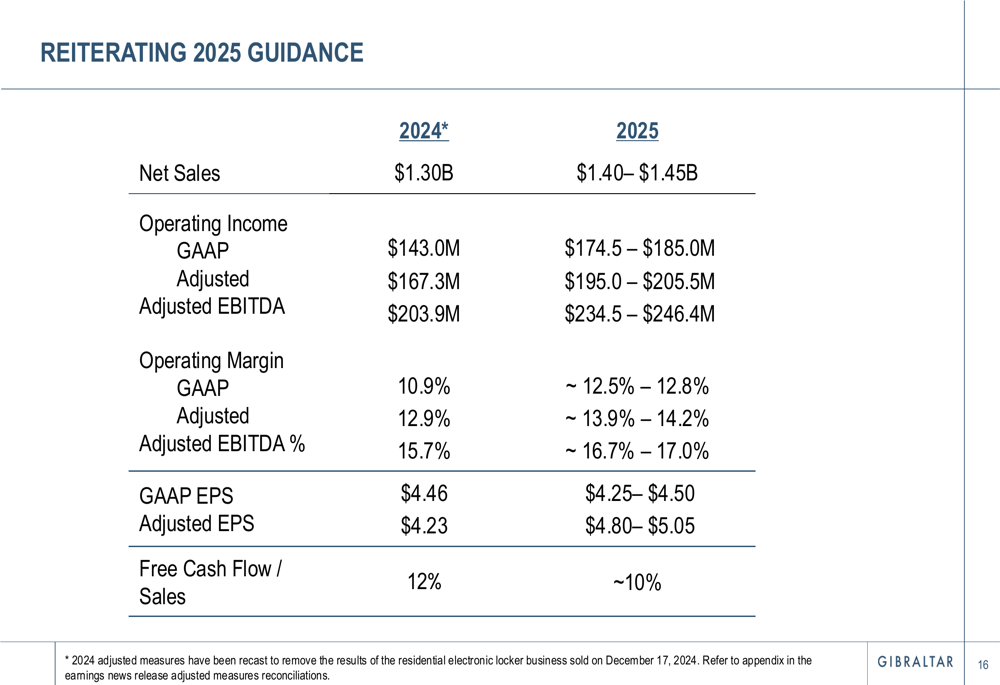

Gibraltar reiterated its full-year 2025 guidance, projecting net sales of $1.40-$1.45 billion (compared to $1.30 billion in 2024), adjusted operating income of $195.0-$205.5 million, and adjusted earnings per share of $4.80-$5.05. The company expects free cash flow to be approximately 10% of sales, slightly below the 12% achieved in 2024.

The following slide details the company’s 2025 guidance:

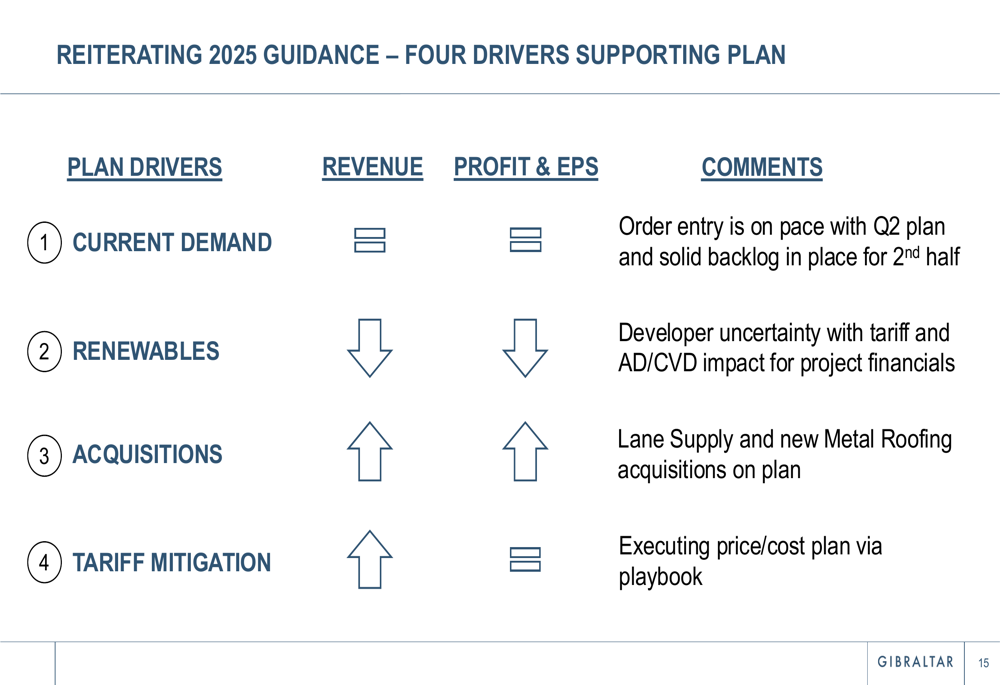

Gibraltar identified four key drivers supporting its 2025 plan: current demand tracking on target, renewables expected to decrease due to developer uncertainty related to tariffs, acquisitions projected to increase revenue, and tariff mitigation strategies expected to have a positive impact.

Market Context and Outlook

Gibraltar’s Q1 2025 performance builds on its strong Q4 2024 results, when the company reported EPS of $1.01, exceeding analysts’ forecasts of $0.91. The stock has shown positive momentum, with premarket trading on April 30 indicating a 1.74% increase to $53.75, according to available market data.

The company faces mixed market conditions across its segments. The residential market started slowly in January and February but showed improvement in late March. The renewables segment continues to navigate regulatory uncertainties and tariff impacts, while infrastructure demand remains robust with an 11% increase in backlog.

Despite these challenges, Gibraltar’s focus on margin expansion, strategic acquisitions, and operational efficiency positions the company to deliver on its full-year guidance. The significant growth in adjusted earnings per share despite flat sales demonstrates management’s ability to improve profitability even in challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.