Crispr Therapeutics shares tumble after significant earnings miss

Gibson Energy Inc . (TSX:GEI) recently presented its Q2 2025 corporate strategy, emphasizing its "Focused, Disciplined Growth" approach while navigating recent performance challenges. The Canadian midstream energy company, which missed earnings expectations in Q4 2024, is doubling down on its infrastructure-first strategy to deliver long-term shareholder value despite marketing segment volatility.

Introduction & Market Context

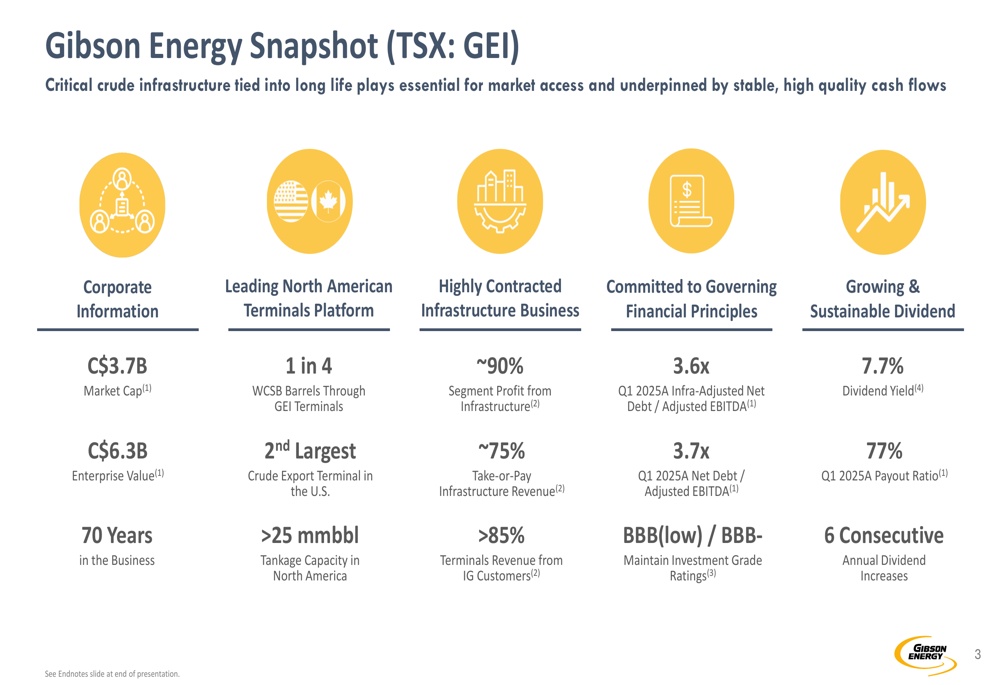

Gibson Energy, with a market capitalization of C$3.7 billion and enterprise value of C$6.3 billion, positions itself as a critical player in North American energy infrastructure. The company’s stock currently trades at C$21.54, down slightly from its previous close and significantly below its 52-week high of C$26.10, reflecting investor concerns following its Q4 2024 earnings miss.

The company’s presentation highlights its 70+ year history and strategic positioning in key energy hubs, including Hardisty and Edmonton in Canada and the Gateway Terminal on the U.S. Gulf Coast. Gibson emphasizes that global oil demand continues to grow at approximately 1.5% CAGR from 2023 to 2030, with Western Canadian production expected to increase from 5.7 million barrels per day in 2023 to 6.4 million barrels per day by 2030.

As shown in the following snapshot of Gibson Energy’s key metrics:

Strategic Initiatives

Gibson’s strategy centers on leveraging its strategically located infrastructure assets to generate stable, contracted cash flows. The company has deliberately shifted its business mix toward infrastructure, with approximately 90% of segment profit now coming from infrastructure assets and over 75% of infrastructure revenue derived from take-or-pay contracts.

The company’s key investment thesis is built around five pillars, including favorable macro environment, best-in-class liquids infrastructure, stable contracted cash flows, sustainable growing dividend, and customer focus:

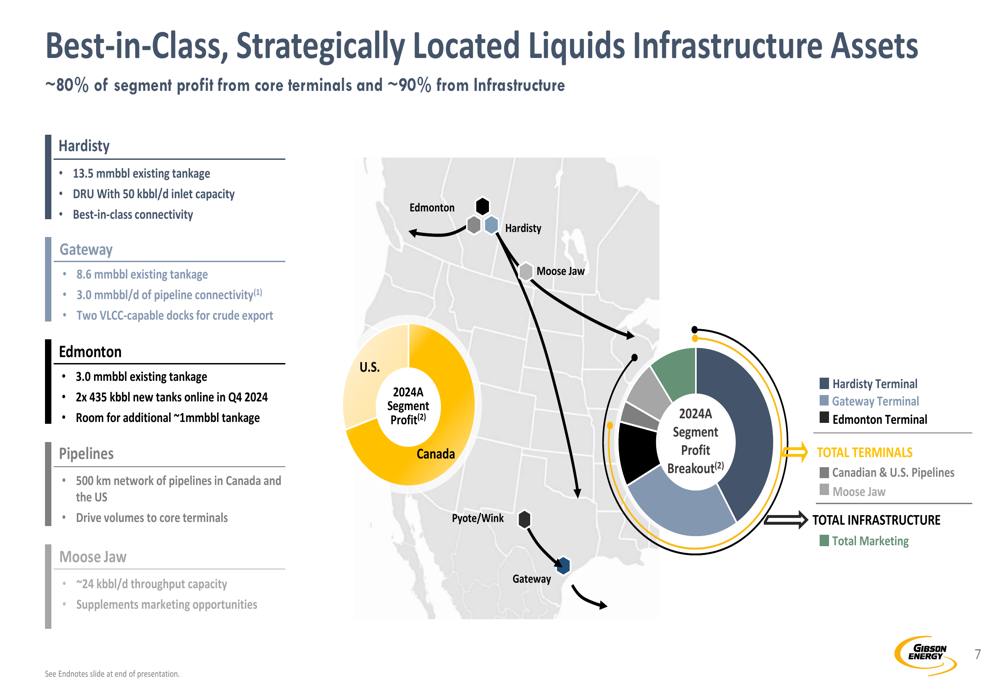

Gibson’s infrastructure network spans critical energy corridors in North America, with terminals strategically positioned to handle significant volumes of crude oil. The company’s Hardisty terminal touches approximately one in four barrels in the Western Canadian Sedimentary Basin, while its Gateway Terminal represents the second-largest crude export terminal in the U.S.

The following map illustrates Gibson’s strategically located liquids infrastructure assets across North America:

Financial Performance & Outlook

Despite Gibson’s optimistic long-term outlook, the company’s recent financial performance has been mixed. In Q4 2024, Gibson reported earnings per share of $0.24, missing analyst expectations of $0.3193, and revenue of $2.36 billion against forecasts of $3.39 billion. This disappointing performance led to a 7.29% drop in the stock price following the earnings announcement.

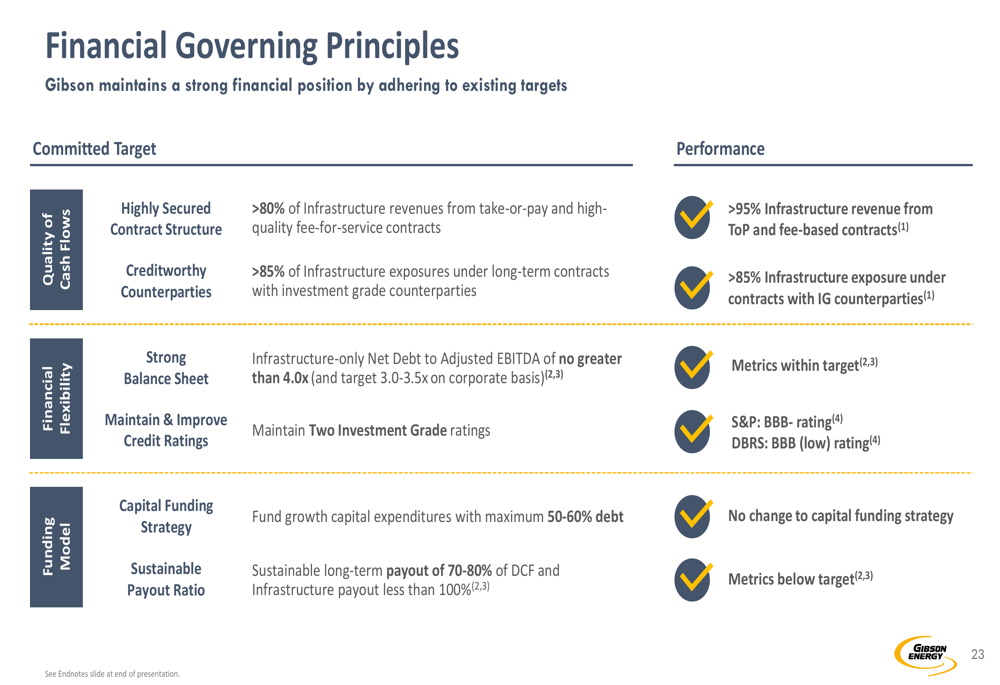

The company’s financial governing principles emphasize maintaining a strong balance sheet with investment grade credit ratings (currently BBB- from S&P and BBB (low) from DBRS). Gibson targets an infrastructure-adjusted net debt to EBITDA ratio of 3.0x-3.5x, with Q1 2025 actual levels at 3.6x.

As shown in the following slide detailing Gibson’s financial governing principles:

A key challenge for Gibson has been the volatility in its marketing segment, which saw adjusted EBITDA decline from $145 million in 2023 to $63 million in 2024. This decline was attributed to narrow differentials and market backwardation, which management described as "temporal" headwinds during the Q4 earnings call.

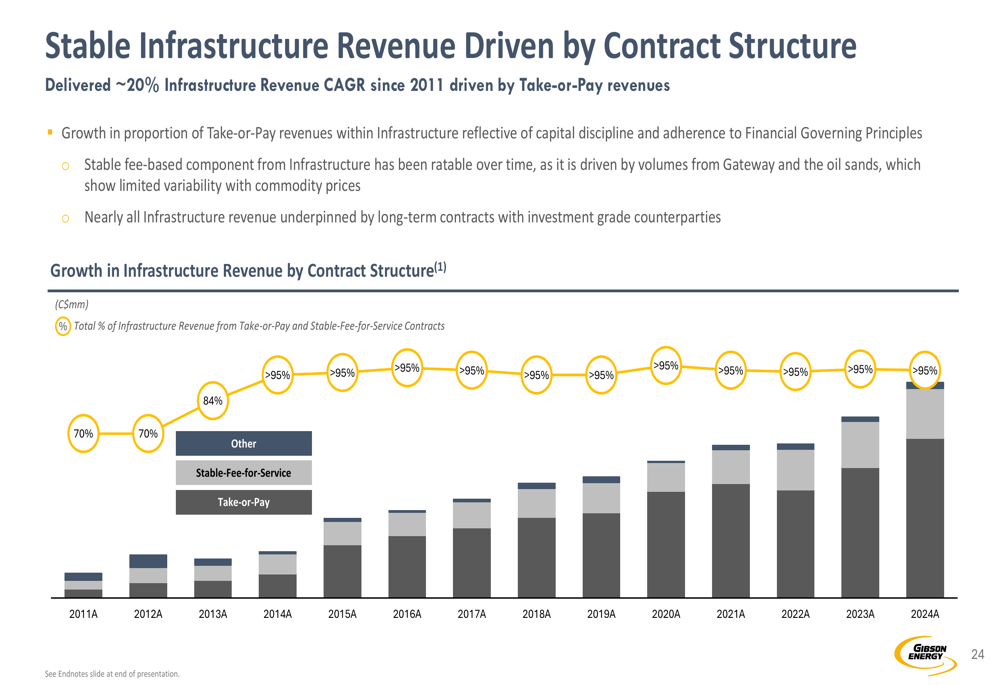

The company’s infrastructure segment, however, continues to show strength, with infrastructure revenue increasingly underpinned by long-term take-or-pay contracts:

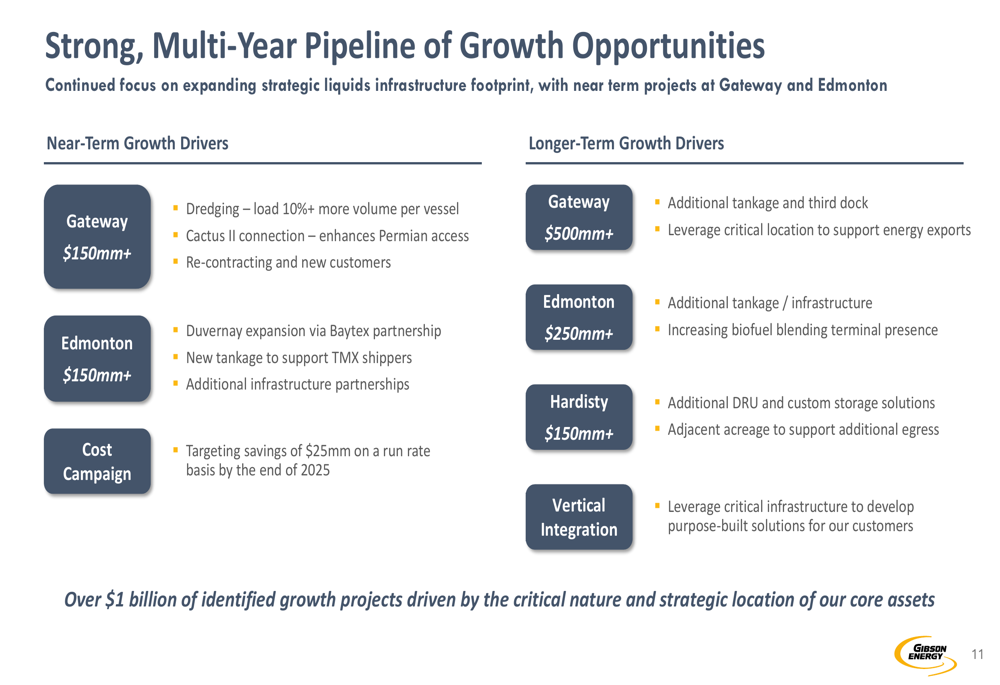

Growth Opportunities

Gibson has identified over $1 billion in potential growth projects across its asset base. Near-term growth drivers include expansion at the Gateway Terminal ($150 million+), Edmonton Terminal ($150 million+), and a cost campaign targeting $25 million in savings on a run-rate basis.

The following slide outlines Gibson’s multi-year pipeline of growth opportunities:

At the Gateway Terminal, which Gibson acquired in 2023, the company is pursuing several growth initiatives including dredging to increase loading depth, connecting to the Cactus (NYSE:WHD) II pipeline, and re-contracting opportunities. The company targets 15-20% EBITDA growth at Gateway by the end of 2025.

The Edmonton Terminal is also seeing expansion, with three new TMX-connected tanks recently brought into service and a strategic partnership with Baytex Energy (NYSE:BTE) involving approximately $50 million in investment supported by long-term return on investment agreements.

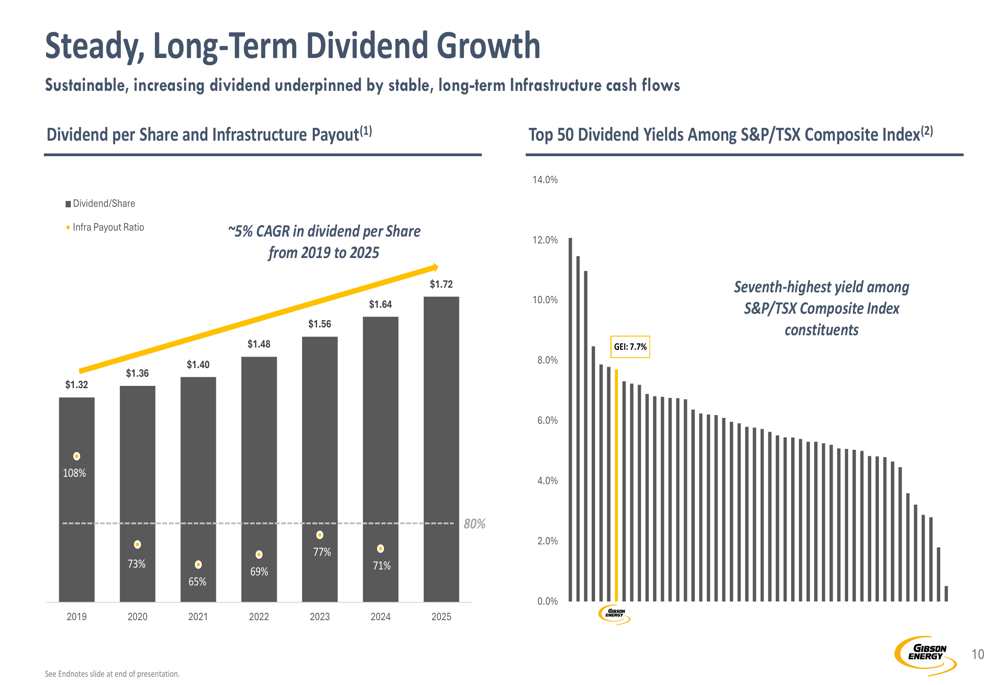

Dividend Strategy & Shareholder Returns

Gibson emphasizes its commitment to a sustainable and growing dividend as a key component of shareholder returns. The company has increased its dividend for six consecutive years, with planned growth from $1.56 per share in 2023 to $1.64 in 2024 and $1.72 in 2025, representing a compound annual growth rate of approximately 5% since 2019.

The presentation highlights Gibson’s 7.7% dividend yield, which it claims is among the top 50 dividend yields in the S&P/TSX Composite Index. However, the recent earnings article noted a current dividend yield of 4.72%, suggesting potential changes in the stock price or dividend expectations.

The following chart illustrates Gibson’s steady, long-term dividend growth:

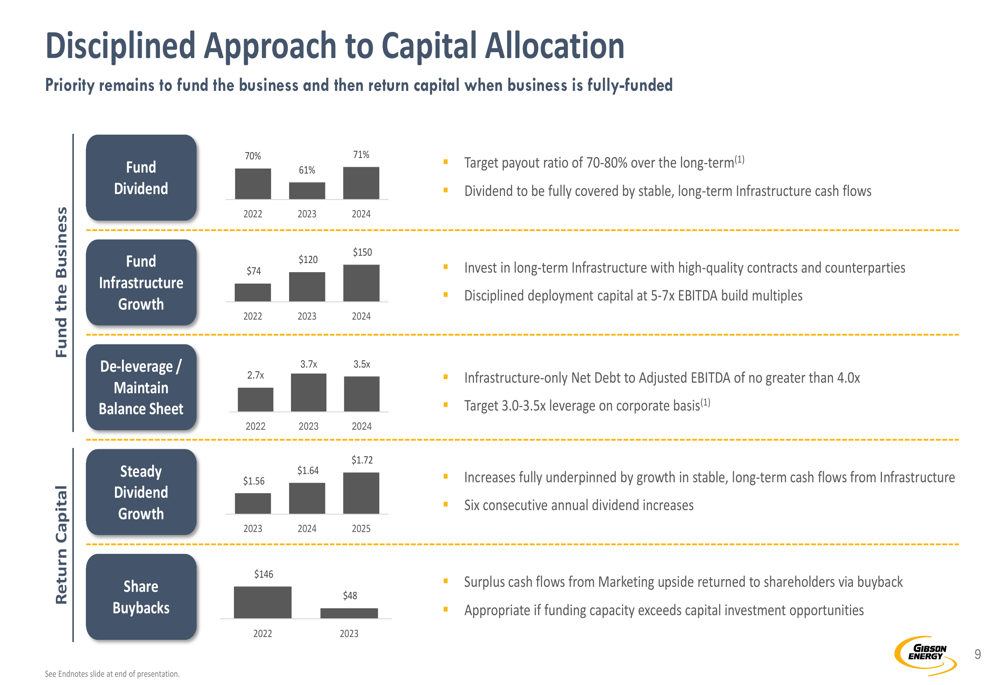

Gibson’s capital allocation strategy prioritizes funding its dividend (71% of available cash flow in 2024), followed by infrastructure growth ($150 million in 2024), and maintaining balance sheet strength. The company has also engaged in share buybacks when appropriate, though these were reduced from $146 million in 2022 to $48 million in 2023.

Looking ahead, Gibson plans to deploy up to $200 million in growth capital and share repurchases in 2025, with management expressing optimism that marketing opportunities will improve later in 2025 and into 2026. However, investors will be closely watching whether the company can overcome recent challenges and deliver on its growth and dividend commitments in the face of volatile energy markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.