Asia FX moves little with focus on US-China trade, dollar steadies ahead of CPI

Introduction & Market Context

Gilead Sciences (NASDAQ:GILD) presented its Q2 2025 financial results on August 7, 2025, showcasing strong performance in its core HIV business and progress across its oncology pipeline. The biotech company’s shares responded positively, rising 2.9% in premarket trading to $113.48 following the presentation, reflecting investor confidence in the company’s improved outlook and strategic direction.

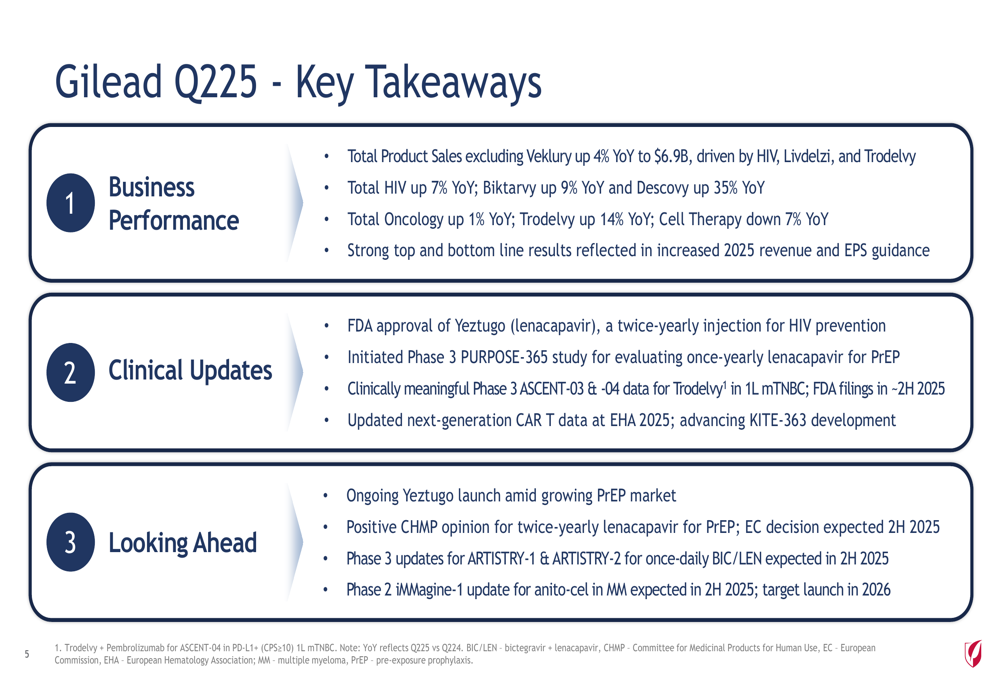

The quarterly results demonstrated resilience in Gilead’s base business, with total product sales excluding Veklury growing 4% year-over-year to $6.9 billion, driven primarily by the HIV portfolio, Trodelvy, and emerging contributions from Livdelzi. This performance prompted management to raise its full-year 2025 guidance for both revenue and earnings per share.

Quarterly Performance Highlights

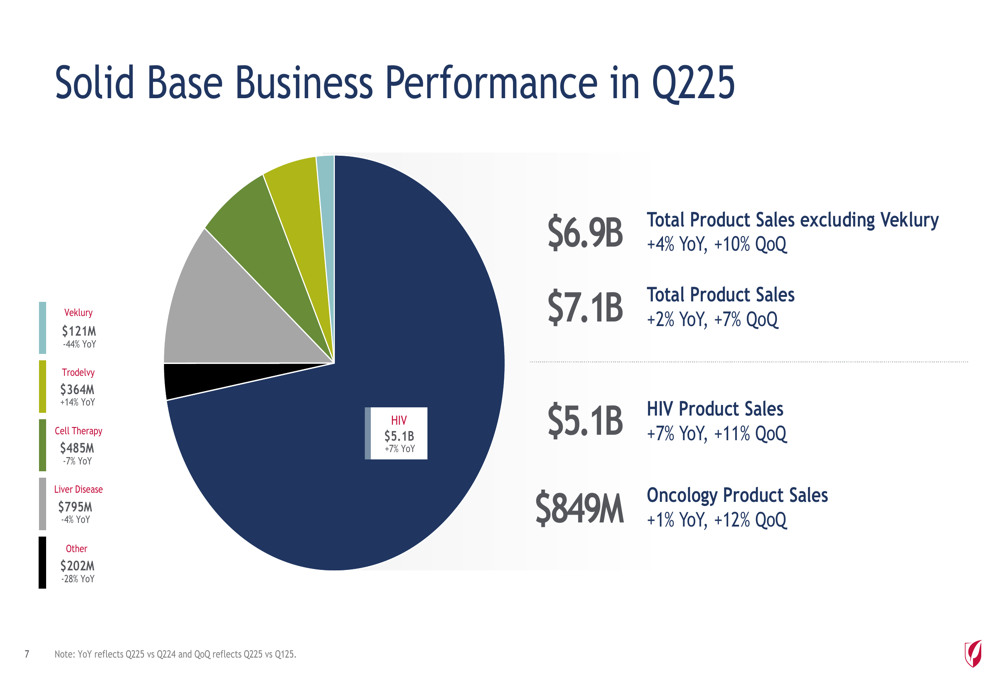

Gilead reported total product sales of $7.1 billion for Q2 2025, representing a 2% year-over-year increase and a 7% sequential improvement from Q1. Excluding Veklury, which continues to decline as COVID-19 hospitalizations decrease, the base business grew 4% year-over-year and 10% quarter-over-quarter.

As shown in the following breakdown of product sales by category:

HIV remains Gilead’s dominant revenue driver at $5.1 billion (72% of total sales), followed by oncology at $849 million (12%) and liver disease at $795 million (11%). Veklury sales declined 44% year-over-year to $121 million, reflecting fewer COVID-19 related hospitalizations.

The company highlighted several key achievements during the quarter, including FDA approval of Yeztugo (lenacapavir) for HIV prevention in June 2025, continued momentum in the HIV treatment portfolio, and meaningful clinical data for Trodelvy in first-line metastatic triple-negative breast cancer.

HIV Portfolio Strength

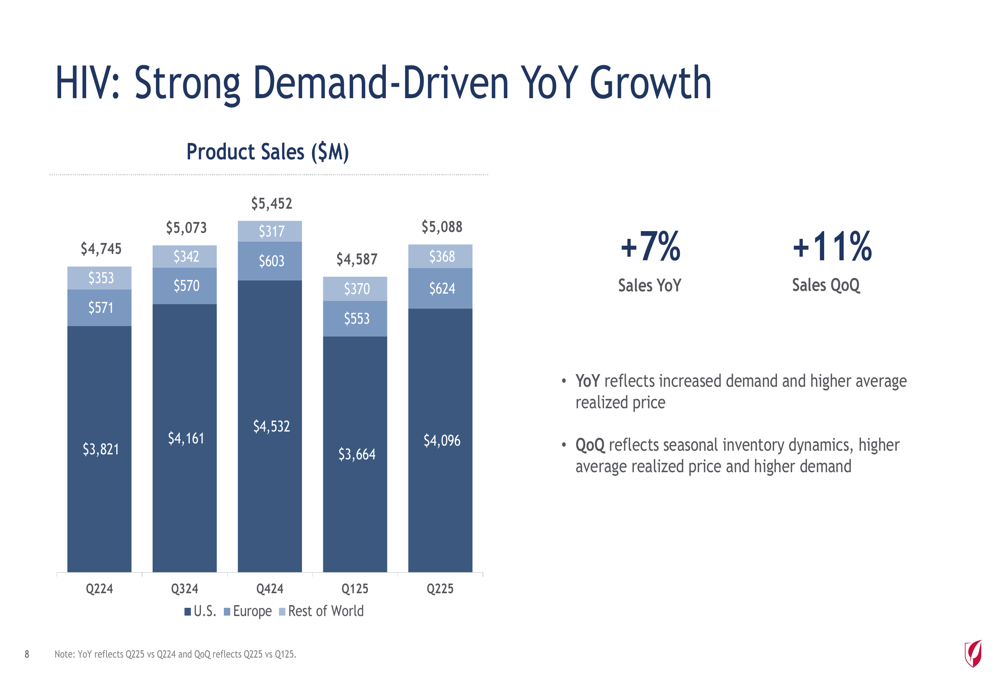

Gilead’s HIV franchise delivered impressive results, with total sales increasing 7% year-over-year to $5.1 billion. This growth was driven by increased demand and higher average realized prices. The sequential growth of 11% from Q1 reflected seasonal inventory dynamics and continued strong demand.

The following chart illustrates the regional breakdown of HIV sales:

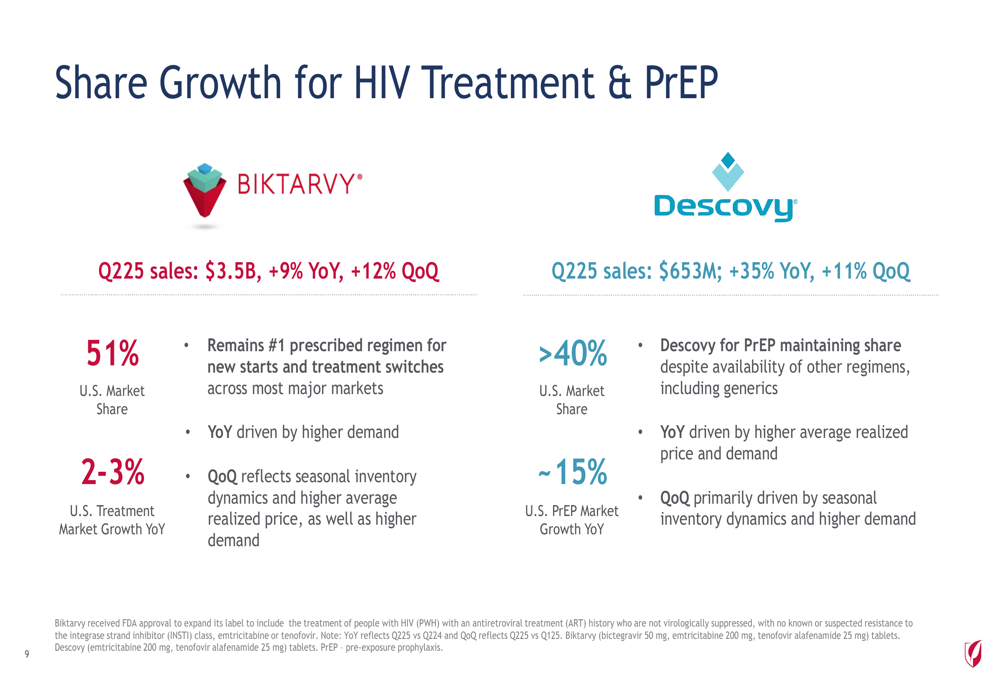

Biktarvy maintained its position as the market leader with 51% U.S. market share and sales growth of 9% year-over-year to $3.5 billion. Descovy demonstrated exceptional performance with 35% year-over-year growth to $653 million, maintaining over 40% U.S. market share despite generic competition in the PrEP market.

A significant milestone for Gilead’s HIV business was the FDA approval of Yeztugo (lenacapavir) for HIV prevention. The company reported rapid execution of its launch strategy, with the first prescription written within hours of approval and the first product shipped within 24 hours.

Based on the strong performance year-to-date, Gilead updated its full-year 2025 HIV revenue guidance to approximately 3% year-over-year growth, an improvement from the previous expectation of flat sales. This guidance accounts for Medicare Part D redesign impacts, the recent Yeztugo launch, and the current policy environment.

Oncology and Liver Disease Performance

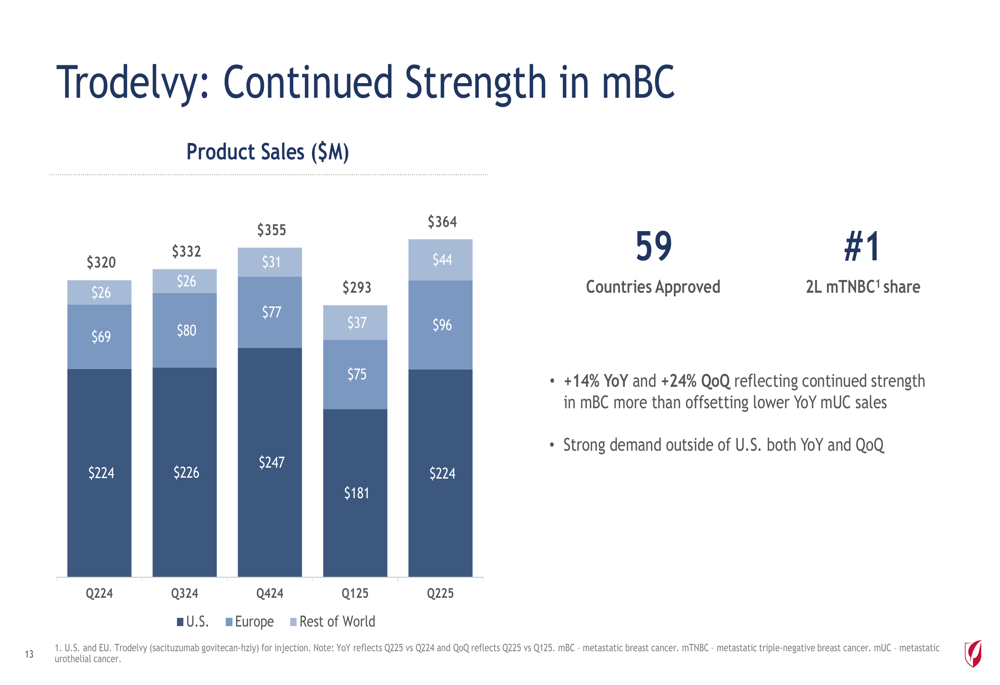

Gilead’s oncology portfolio grew 1% year-over-year to $849 million, driven by Trodelvy’s 14% growth to $364 million. Trodelvy continues to hold the #1 market share position in second-line metastatic triple-negative breast cancer (mTNBC) in both the U.S. and EU.

The following chart shows Trodelvy’s continued growth trajectory:

Cell therapy sales declined 7% year-over-year to $485 million, reflecting lower demand in an increasingly competitive landscape, partially offset by higher average realized prices. The company noted that more than 31,000 patients have been treated with its cell therapy products to date across over 570 authorized treatment centers globally.

In liver disease, total sales declined 4% year-over-year but increased 5% sequentially. A bright spot was Livdelzi, which saw sales almost double quarter-over-quarter to $78 million. Gilead maintains over 60% market share in the U.S. HCV market.

Financial Results and Guidance Update

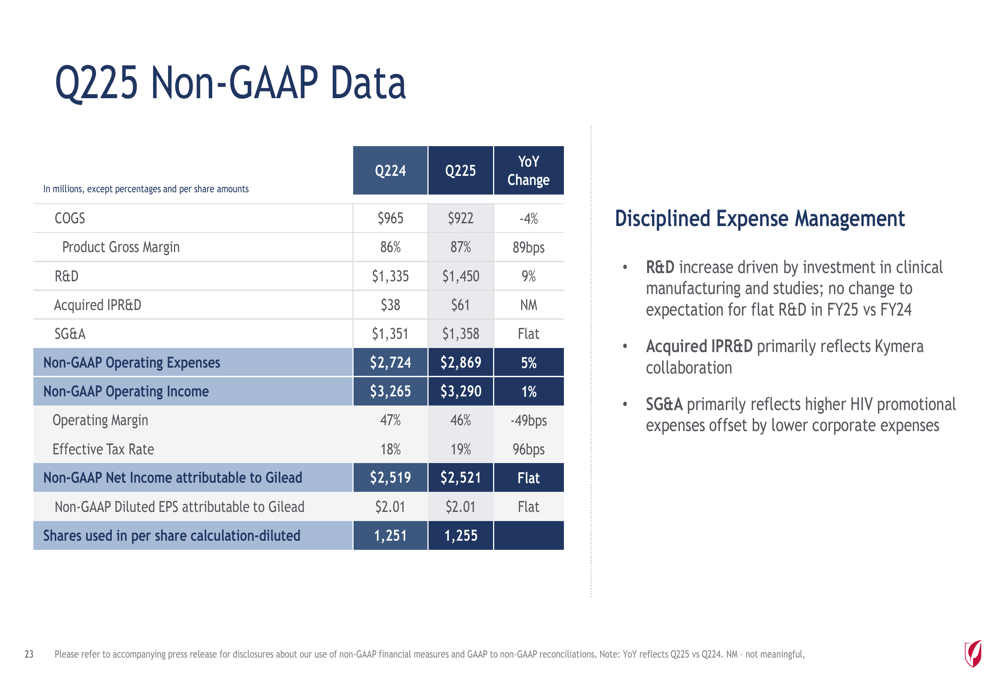

Gilead’s disciplined expense management helped drive solid financial performance in Q2 2025. Product gross margin improved by 89 basis points compared to Q2 2024, while non-GAAP operating income increased 1% despite higher R&D investments.

The following table provides a detailed breakdown of Gilead’s Q2 2025 non-GAAP financial results:

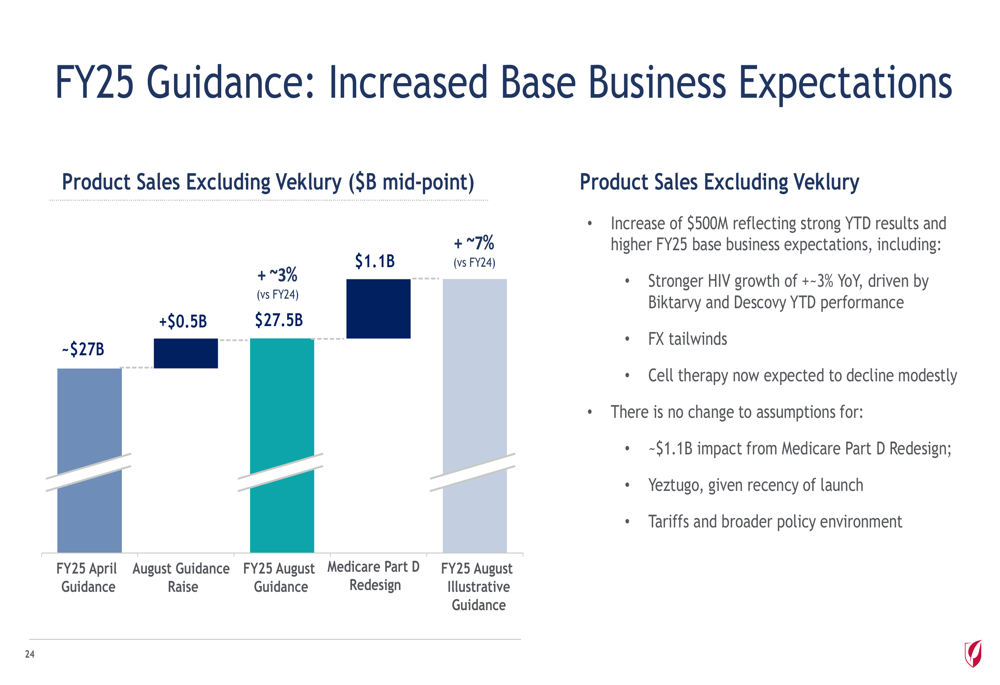

Based on the strong performance in the first half of 2025, Gilead increased its full-year guidance by $500 million, reflecting higher base business expectations. The company now projects total product sales of approximately $27 billion, representing about 7% growth when excluding the impact of the Medicare Part D redesign.

The company also raised its earnings per share guidance by $0.20 at the midpoint, reflecting the stronger sales outlook and effective expense management.

Strategic Initiatives and Pipeline Progress

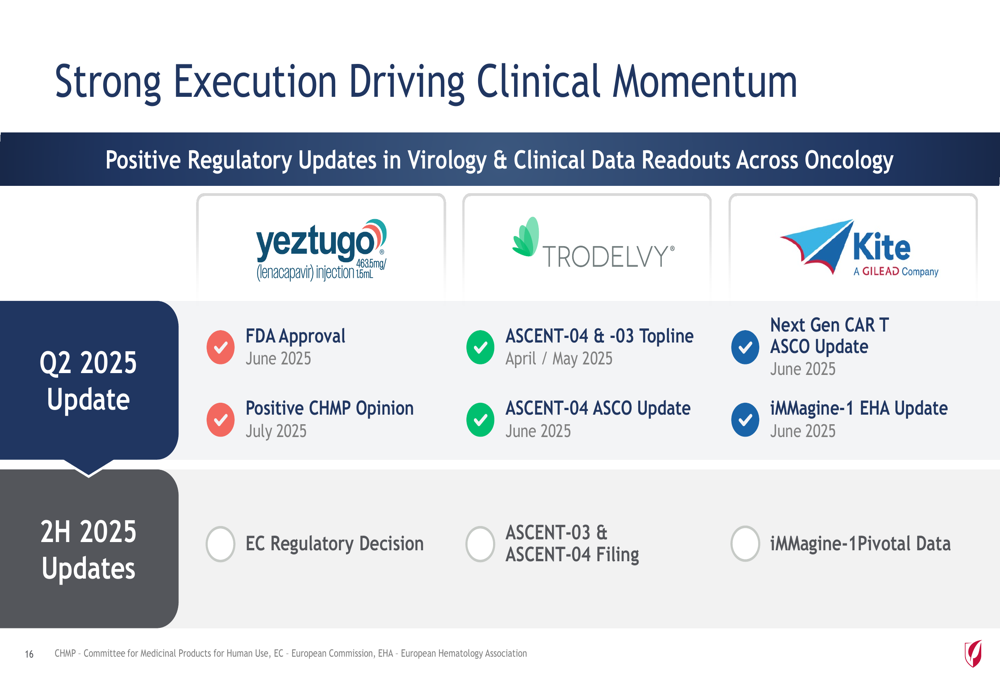

Gilead continues to advance its robust pipeline across virology, oncology, and inflammatory diseases. The company highlighted several key milestones achieved in the first half of 2025 and upcoming catalysts for the remainder of the year.

In HIV, Gilead is building on the recent approval of Yeztugo with the initiation of the Phase 3 PURPOSE-365 study evaluating once-yearly lenacapavir for PrEP. The company also received a positive CHMP opinion for twice-yearly lenacapavir for PrEP in Europe, with an EC decision expected in the second half of 2025.

In oncology, Gilead reported meaningful Phase 3 data from the ASCENT-03 and ASCENT-04 trials for Trodelvy in first-line mTNBC, with FDA filings expected in the second half of 2025. The company is also advancing its next-generation CAR T therapies, including KITE-363.

Capital Allocation and Shareholder Returns

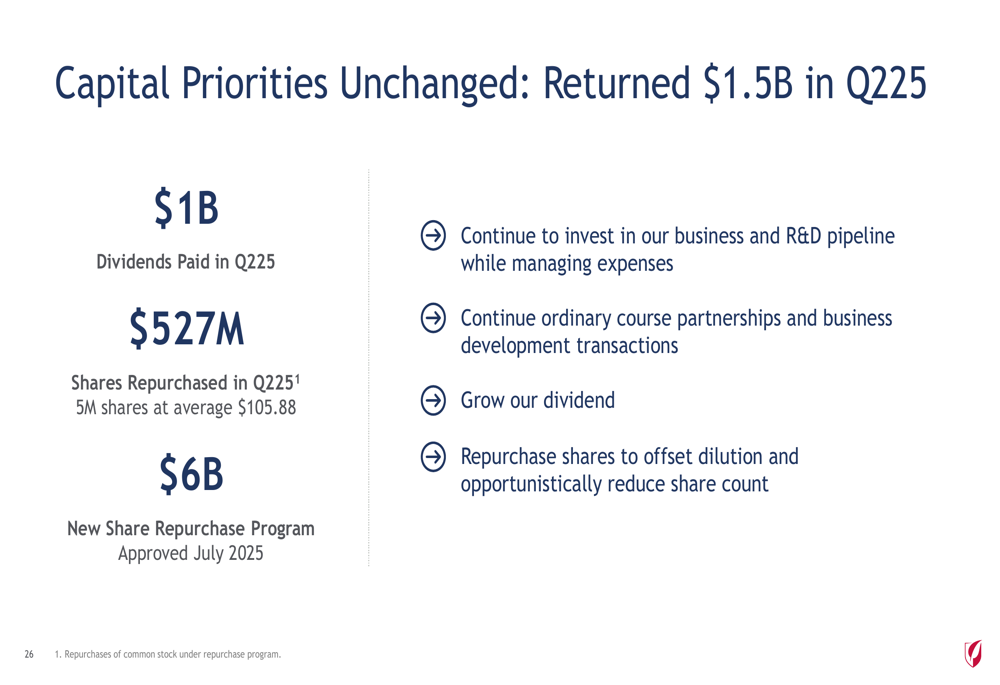

Gilead maintained its commitment to returning capital to shareholders, distributing $1.5 billion in Q2 2025 through dividends and share repurchases. The company paid $1 billion in dividends and repurchased 5 million shares for $527 million at an average price of $105.88 per share.

In July 2025, Gilead’s board approved a new $6 billion share repurchase program, underscoring the company’s confidence in its long-term prospects and commitment to shareholder returns.

The company reiterated its capital allocation priorities: investing in its business and R&D pipeline, pursuing strategic partnerships, growing its dividend, and repurchasing shares to offset dilution.

Forward-Looking Statements

Looking ahead, Gilead is focused on executing the Yeztugo launch, advancing its HIV and oncology pipelines, and delivering on its increased financial guidance for 2025. Key upcoming catalysts include the European Commission decision on twice-yearly lenacapavir for PrEP, Phase 3 updates for once-daily BIC/LEN, and Phase 2 data for anito-cel in multiple myeloma.

The company’s robust pipeline, with 52 clinical-stage programs and 8 potential opt-in assets, positions it well for sustained growth beyond 2025. Management expressed confidence in navigating challenges such as the Medicare Part D redesign and competitive pressures in the cell therapy market through continued innovation and commercial execution.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.