German construction sector still in recession, civil engineering only bright spot

Global Payments Inc (NYSE:GPN) reported second-quarter results that modestly exceeded expectations, with adjusted earnings per share growing 11% year-over-year. The company’s stock rose 4.58% in premarket trading to $82.00, reflecting positive investor sentiment following the earnings release on August 6, 2025.

Quarterly Performance Highlights

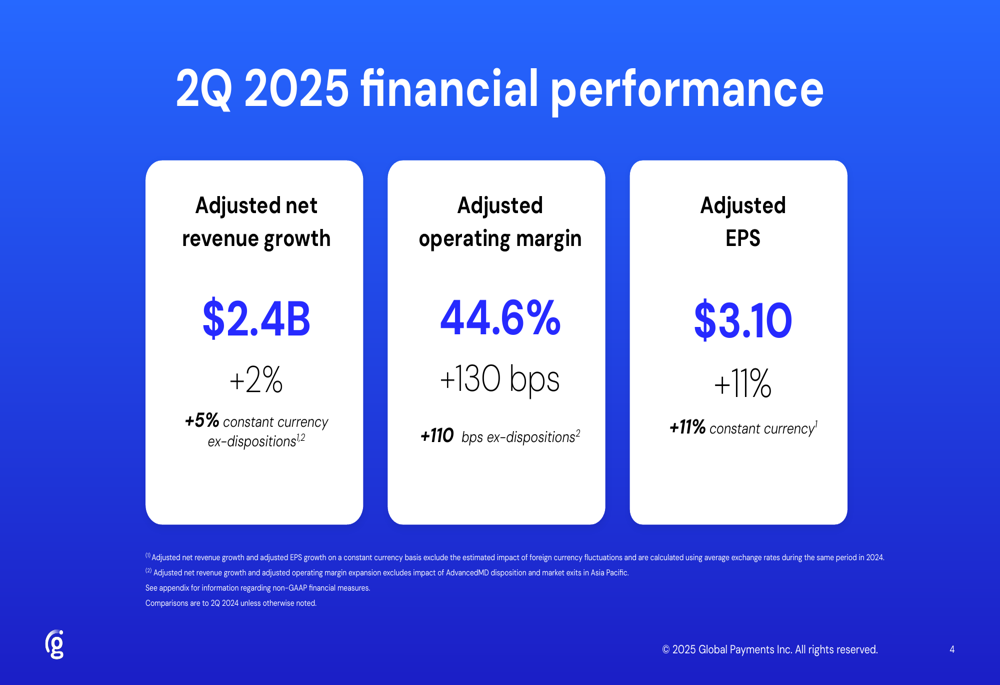

Global Payments delivered adjusted net revenue of $2.4 billion in the second quarter, representing 2% growth on a reported basis and 5% growth on a constant currency basis excluding dispositions. The company achieved an adjusted operating margin of 44.6%, expanding 130 basis points (110 basis points excluding dispositions), while adjusted earnings per share reached $3.10, an 11% increase in both reported and constant currency terms.

As shown in the following financial performance summary:

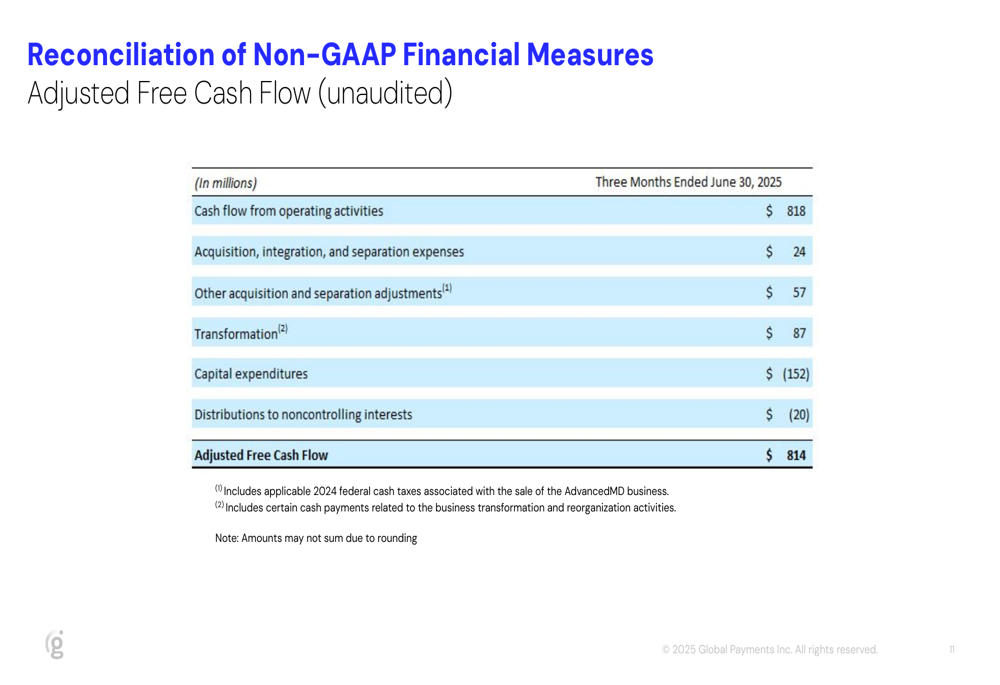

The company generated strong adjusted free cash flow with a 108% conversion rate, demonstrating efficient capital management. This performance builds on the momentum from Q1 2025, when the company reported a 77% conversion rate.

"We delivered Q2 results modestly ahead of expectations while producing strong adjusted free cash flow with a 108% conversion rate," noted the company in its presentation highlights, which also revealed plans for a $500 million accelerated share repurchase program connected to the Payroll divestiture.

The company’s key achievements for the quarter included:

Segment Performance Analysis

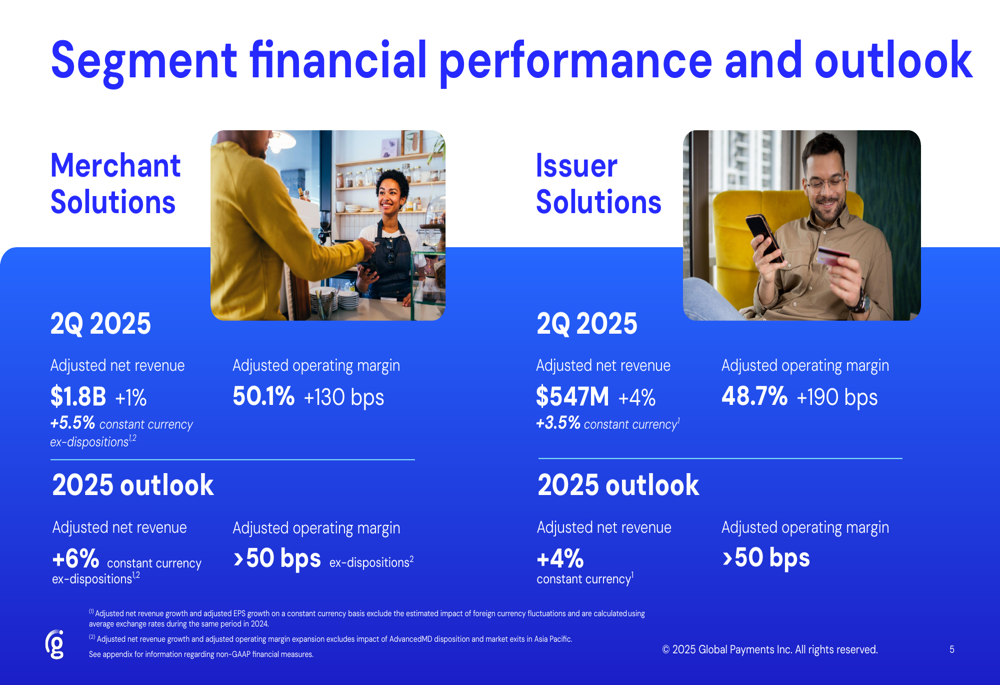

Global Payments’ performance varied across its two main segments. The Merchant Solutions segment, which accounts for approximately three-quarters of total revenue, generated $1.8 billion in adjusted net revenue, up 1% on a reported basis and 5.5% on a constant currency basis excluding dispositions. The segment’s adjusted operating margin expanded 130 basis points to 50.1%.

Meanwhile, the Issuer Solutions segment delivered stronger reported growth, with adjusted net revenue increasing 4% to $547 million (3.5% in constant currency). This segment achieved significant margin improvement, with adjusted operating margin expanding 190 basis points to 48.7%.

The segment breakdown illustrates these performance metrics:

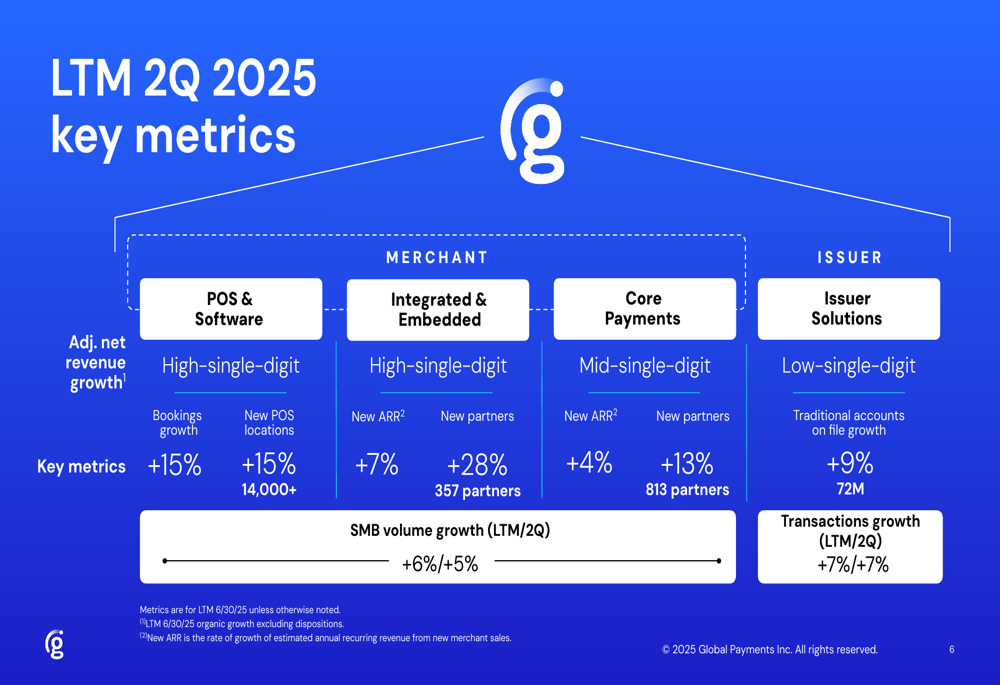

Looking at longer-term performance metrics across business areas, Global Payments showed consistent growth across its portfolio. The company’s POS & Software (ETR:SOWGn) and Integrated & Embedded solutions both achieved high-single-digit adjusted net revenue growth over the last twelve months, while Core Payments delivered mid-single-digit growth. The Issuer Solutions business, which is slated for divestiture, showed low-single-digit growth.

The following chart details key metrics across business lines:

Small and medium-sized business (SMB) volume growth reached 6% over the last twelve months and 5% in Q2, while transactions growth maintained a steady 7% pace both for the quarter and the trailing twelve months.

Strategic Initiatives & Transformation

Global Payments continues to make progress on its strategic transformation, with several significant developments announced during the quarter. The company received Hart-Scott-Rodino (HSR) clearances for both the acquisition of Worldpay and the divestiture of its Issuer Solutions business, keeping these transactions on track to close in the first half of 2026.

The company also expanded its product portfolio with the launch of Genius for Restaurants and Genius for Retail, enhancing its vertical-specific offerings. These launches align with the company’s strategy to deepen its technology integration in key merchant segments.

In a significant update to its operational transformation initiatives, Global Payments increased its expected annual run-rate operating income benefit to $650 million, reflecting greater efficiency gains than previously anticipated.

The company also raised its capital return expectations for 2025-2027 to $7.5 billion, excluding returns associated with asset dispositions, signaling confidence in its long-term cash generation capabilities.

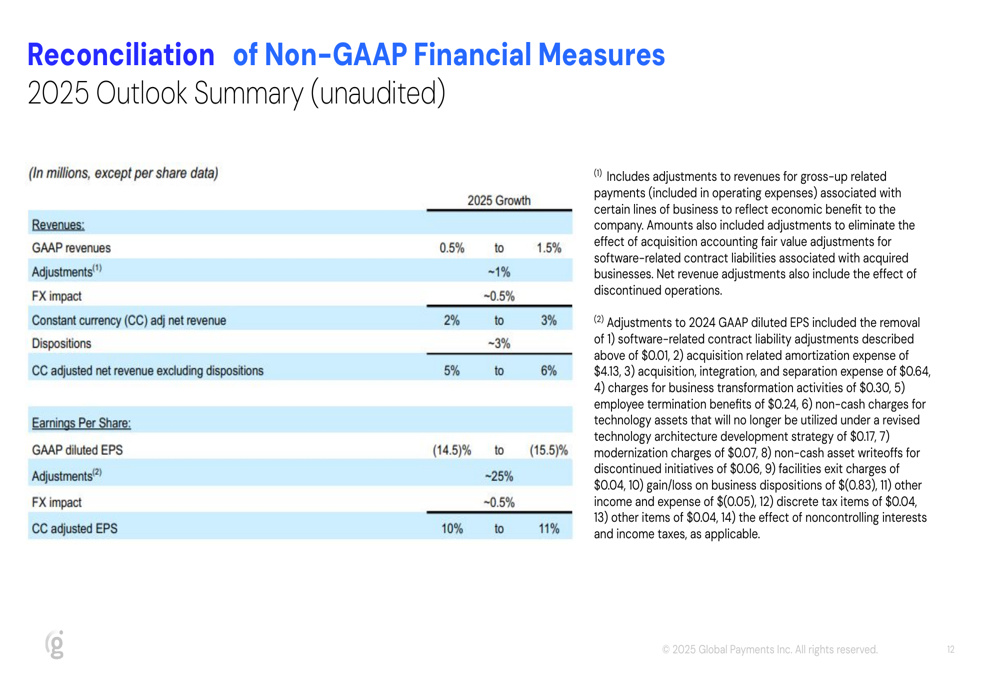

2025 Outlook & Forward Guidance

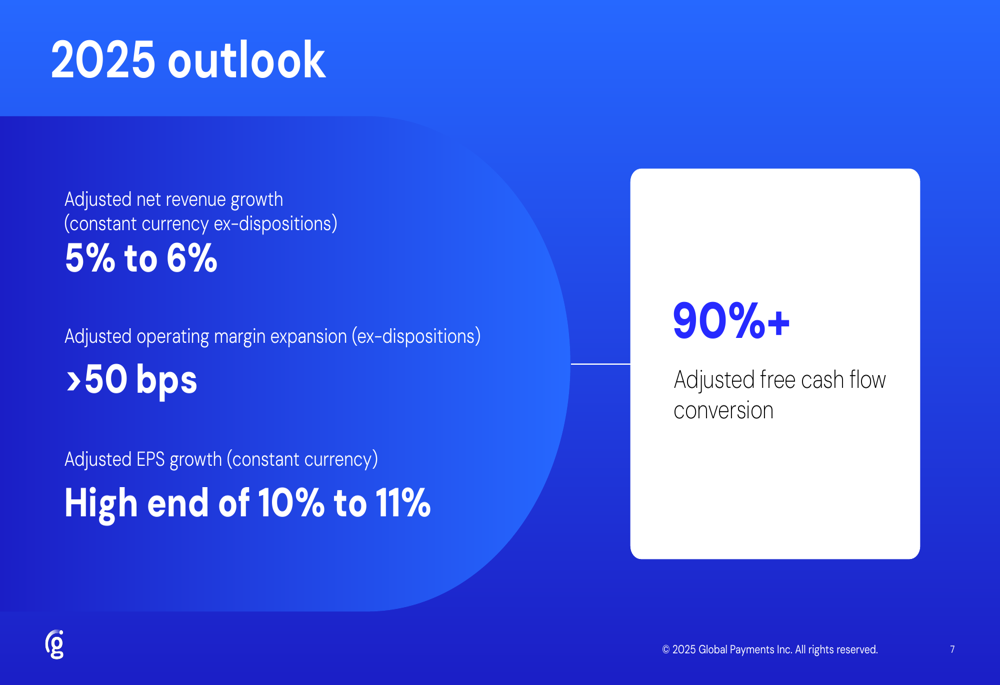

Global Payments updated its outlook for 2025, projecting adjusted net revenue growth of 5% to 6% on a constant currency basis excluding dispositions. The company expects adjusted operating margin expansion of more than 50 basis points excluding dispositions and adjusted EPS growth at the high end of the 10% to 11% range on a constant currency basis.

The company’s forward guidance is summarized in the following slide:

A more detailed breakdown of the 2025 outlook shows how various adjustments and currency effects impact the company’s growth projections:

The adjusted free cash flow calculation provides additional insight into the company’s financial health and operational efficiency:

Global Payments’ Q2 results and updated outlook suggest the company is successfully navigating its strategic transformation while delivering consistent financial performance. With the Worldpay acquisition and Issuer Solutions divestiture progressing as planned, and operational improvements exceeding initial expectations, the company appears well-positioned to meet its financial targets for 2025 and beyond.

The market’s positive reaction, with the stock trading up 4.58% in premarket trading, indicates investor confidence in the company’s strategic direction and financial performance. This represents a potential recovery from the stock’s significant decline over the past six months, during which it fell 31% according to previous earnings reports.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.