S&P 500 rises as health care, tech gain to overshadow Fed independence concerns

GoHealth (NASDAQ:GOCO) shares jumped 5.78% in premarket trading to $8.60 following the release of its first quarter 2025 results on May 13, extending the momentum from its strong fourth quarter performance. The health insurance marketplace provider reported double-digit growth in both revenue and adjusted EBITDA, though operational challenges emerged in cash flow metrics.

Quarterly Performance Highlights

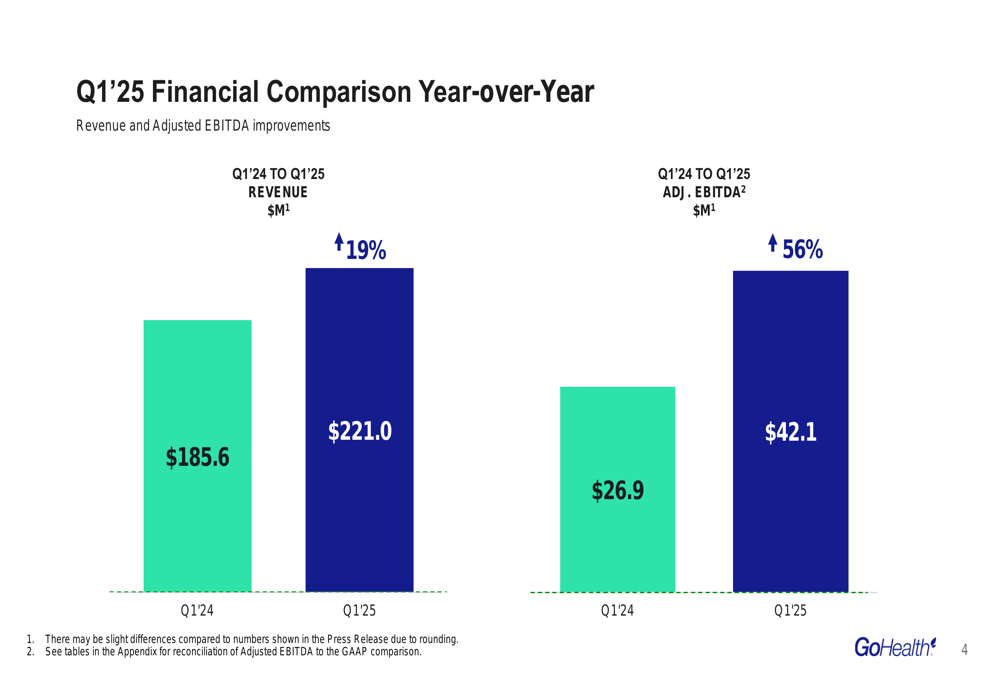

GoHealth reported Q1 2025 revenue of $221.0 million, representing a 19% increase from the $185.6 million recorded in the same period last year. This growth continues the positive trajectory seen in Q4 2024, when the company posted a 41% year-over-year revenue increase.

Adjusted EBITDA showed even stronger improvement, rising 56% year-over-year to $42.1 million from $26.9 million in Q1 2024. The adjusted EBITDA margin expanded to 19.0%, up from 14.5% in the prior-year period, demonstrating enhanced operational efficiency.

As shown in the following chart of quarterly financial performance:

Despite these positive top-line results, GoHealth reported a net loss of $9.8 million for the quarter. While still in negative territory, this represents a significant improvement from the $21.3 million loss recorded in Q1 2024. The company’s net loss margin improved to -4.4% from -11.5% in the prior-year period.

Detailed Financial Analysis

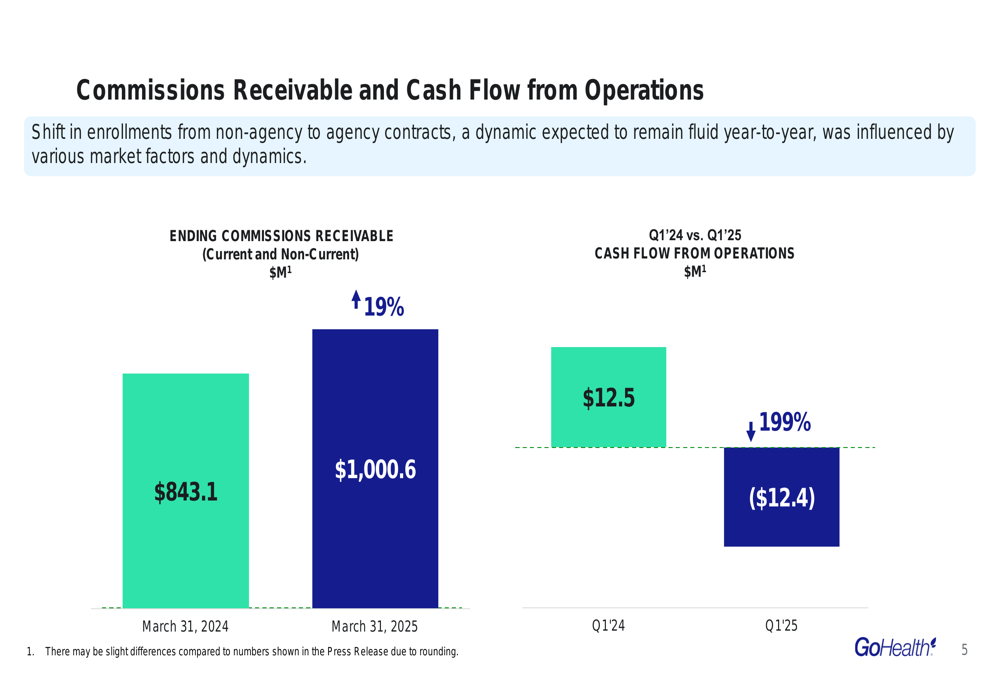

The company’s commissions receivable grew substantially, reaching $1,000.6 million as of March 31, 2025, a 19% increase from $843.1 million a year earlier. This growth aligns with the revenue expansion but also indicates a larger amount of future expected revenue that has not yet been collected.

A concerning development emerged in cash flow metrics, with cash flow from operations turning negative at -$12.4 million in Q1 2025, compared to a positive $12.5 million in Q1 2024—a 199% decline. This shift could potentially create liquidity challenges if the trend continues, despite the positive revenue and EBITDA growth.

The following chart illustrates these contrasting trends:

Interest expense decreased slightly to $16.0 million from $18.0 million in the prior-year period, suggesting some improvement in the company’s debt management. However, with a negative operating cash flow, debt service could become more challenging if operational trends don’t improve.

Strategic Initiatives & Operational Metrics

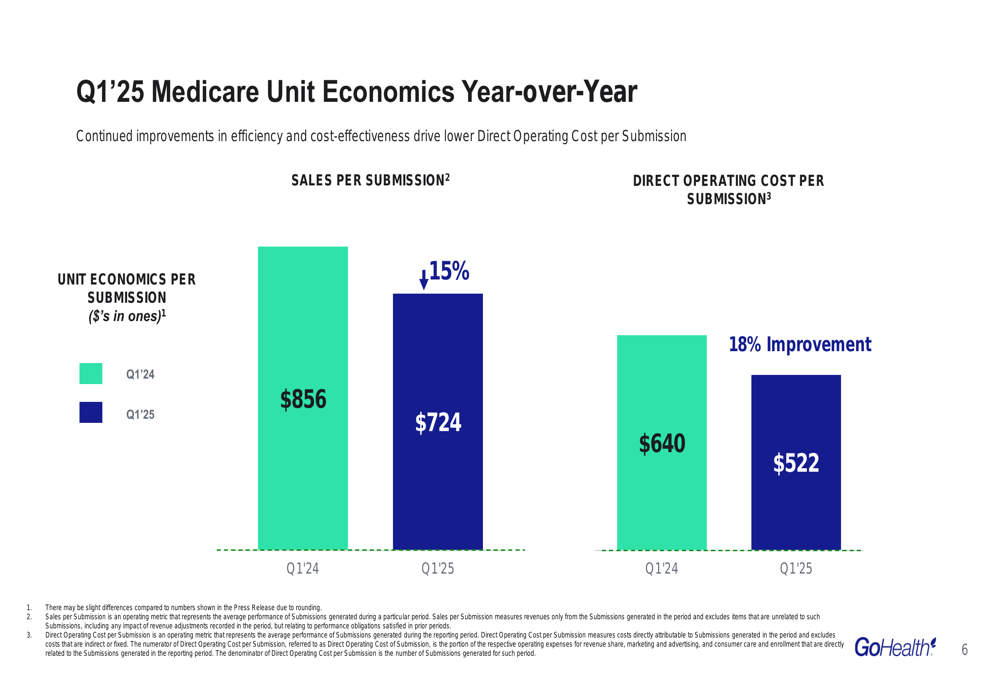

GoHealth’s operational efficiency showed marked improvement, with direct operating cost per submission decreasing by 18% to $522 in Q1 2025 from $640 in Q1 2024. This cost reduction appears to be a key driver behind the improved EBITDA margin, reflecting the company’s focus on operational efficiency.

However, sales per submission declined by 15% to $724 from $856 in the prior-year period, suggesting potential pricing pressure or changes in product mix. The decline in revenue per customer acquisition is partially offset by the improved cost structure, but warrants monitoring in future quarters.

The following chart details these operational metrics:

The company’s PlanFit Save initiative and AI integration, which were highlighted in previous earnings reports as contributing to growth, appear to be delivering on operational efficiency promises, though the company did not provide specific updates on these initiatives in the Q1 presentation.

Forward-Looking Statements

While GoHealth did not provide specific guidance for the remainder of 2025 in the presentation materials, the company’s performance builds on the momentum established in Q4 2024, when it reported a 41% year-over-year revenue increase and a 107% jump in adjusted EBITDA.

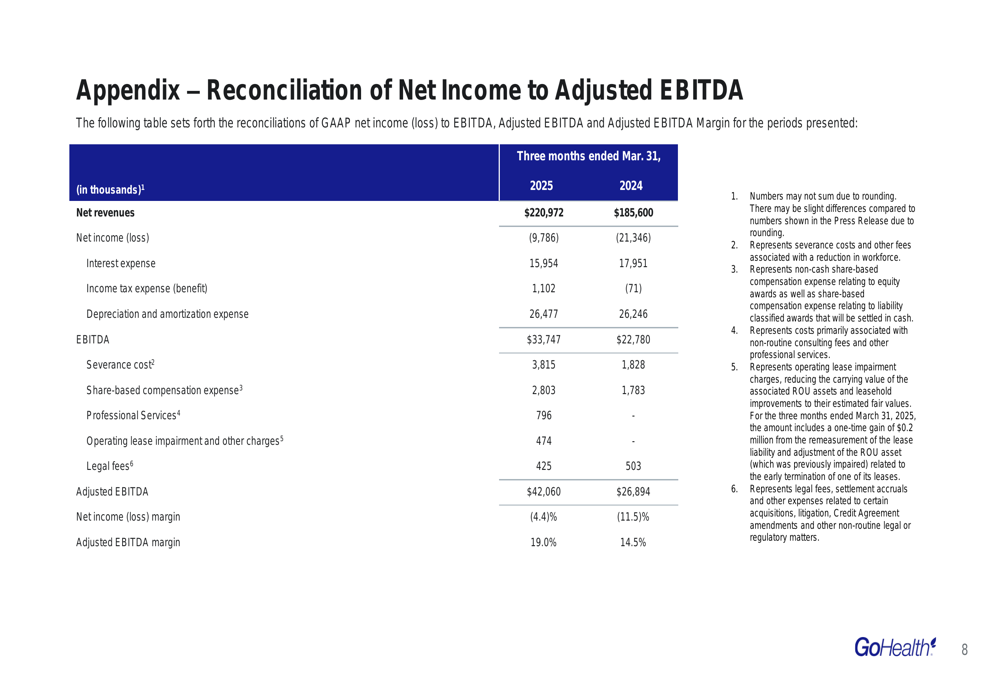

The reconciliation of net income to adjusted EBITDA reveals several non-recurring expenses that impacted the quarter’s profitability, including $3.8 million in severance costs, $2.8 million in share-based compensation, and smaller amounts for professional services, operating lease impairment, and legal fees. These adjustments totaled $8.3 million for the quarter.

The detailed reconciliation is shown below:

Looking ahead, investors should monitor whether GoHealth can reverse the negative trend in operating cash flow while maintaining its revenue growth and margin expansion. The company’s ability to improve sales per submission while continuing to reduce operating costs will be crucial for achieving sustainable profitability.

The Medicare Advantage market remains competitive, and GoHealth’s performance will depend on its ability to navigate potential regulatory changes and manage customer acquisition costs effectively. With the stock trading well below its 52-week high of $21.00, market sentiment appears cautious despite the company’s improving operational metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.