Trump announces trade deal with EU following months of negotiations

Introduction & Market Context

Graco Inc . (NYSE:GGG) reported its first quarter 2025 financial results on April 24, showing 7% year-over-year sales growth, though much of this increase came from acquisitions rather than organic growth. The fluid handling equipment manufacturer’s shares dropped 4.76% in premarket trading to $75.21, suggesting investors may be concerned about underlying performance despite the headline growth numbers.

The company’s Q1 results follow a disappointing fourth quarter 2024, when Graco missed earnings expectations with an EPS of $0.64 against a forecast of $0.77. This latest quarter shows some improvement but continues to reflect challenges in certain segments and regions.

Quarterly Performance Highlights

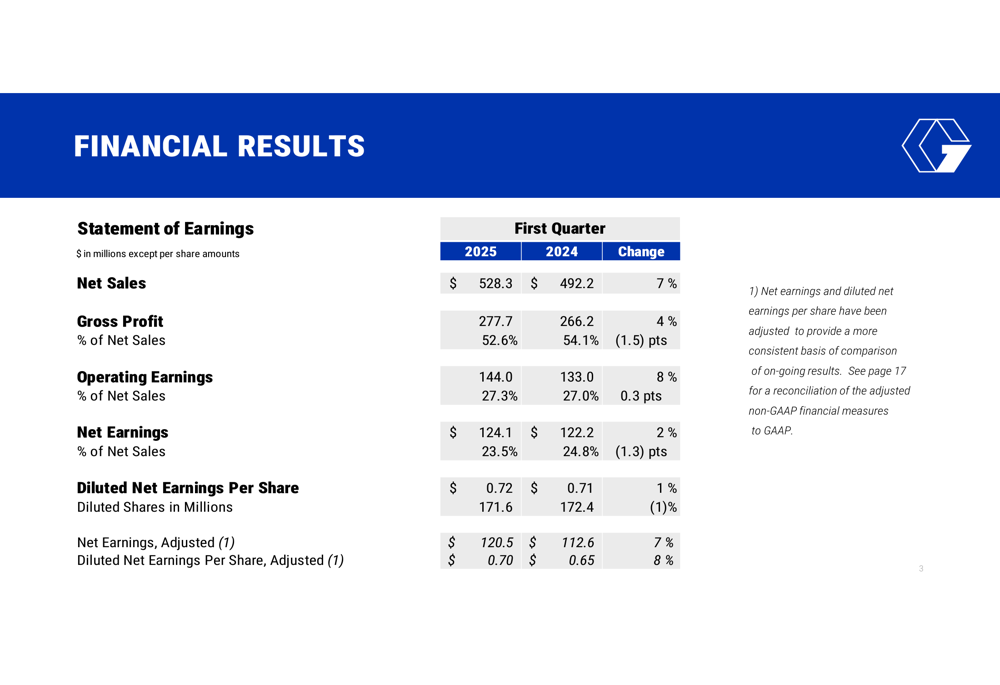

Graco reported first quarter net sales of $528.3 million, a 7% increase from $492.2 million in the same period last year. However, acquisitions contributed 6 percentage points of this growth, while organic volume and price increases accounted for just 3%. Currency translation had a negative 2% impact on sales.

As shown in the following financial results summary:

Operating earnings rose 8% to $144.0 million, with the operating margin improving slightly to 27.3% from 27.0% a year earlier. Net earnings increased 2% to $124.1 million, though the net earnings margin declined 1.3 percentage points to 23.5%. Diluted earnings per share grew 1% to $0.72.

On an adjusted basis, which excludes the impact of excess tax benefits from stock option exercises, EPS was $0.70, representing an 8% increase from the prior year. The company’s gross profit margin declined 1.5 percentage points to 52.6%, primarily due to the unfavorable effects of lower average margin rates from acquired operations and higher product costs.

Segment Analysis

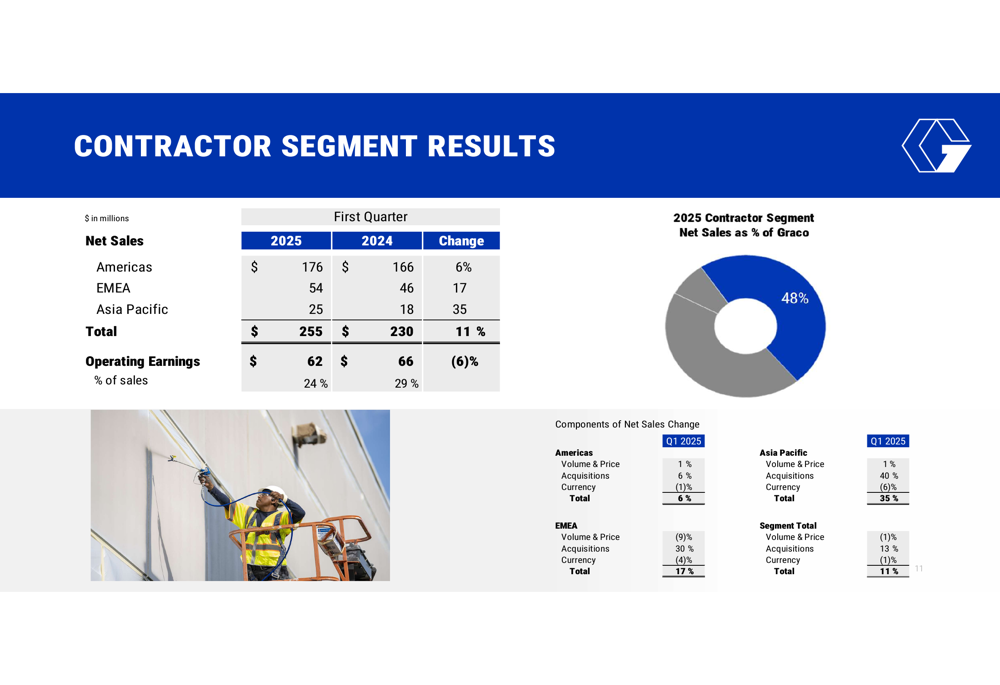

Graco reorganized its reporting structure in 2025, now operating in three segments: Contractor, Industrial, and Expansion Markets. Each segment showed distinctly different performance patterns in the quarter.

The Contractor segment, which represents 48% of Graco’s sales, posted 11% revenue growth to $255 million. However, this growth was primarily acquisition-driven, with organic volume and price contributing just 1% in the Americas and declining 9% in EMEA. More concerning was the 6% drop in operating earnings to $62 million, with margins falling from 29% to 24%.

The segment breakdown shows the varying performance across regions:

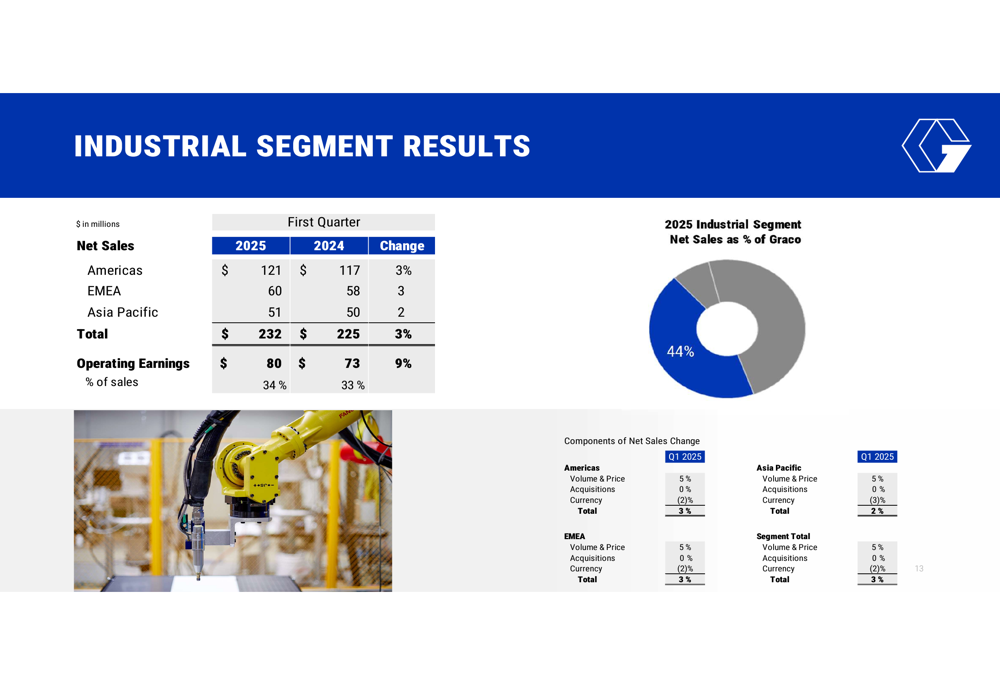

The Industrial segment, accounting for 44% of total sales, delivered more balanced results with 3% revenue growth to $232 million and 9% operating earnings growth to $80 million. This segment achieved a healthy 5% organic growth across all regions, offset by currency headwinds. Operating margins improved to 34% from 33% in the prior year.

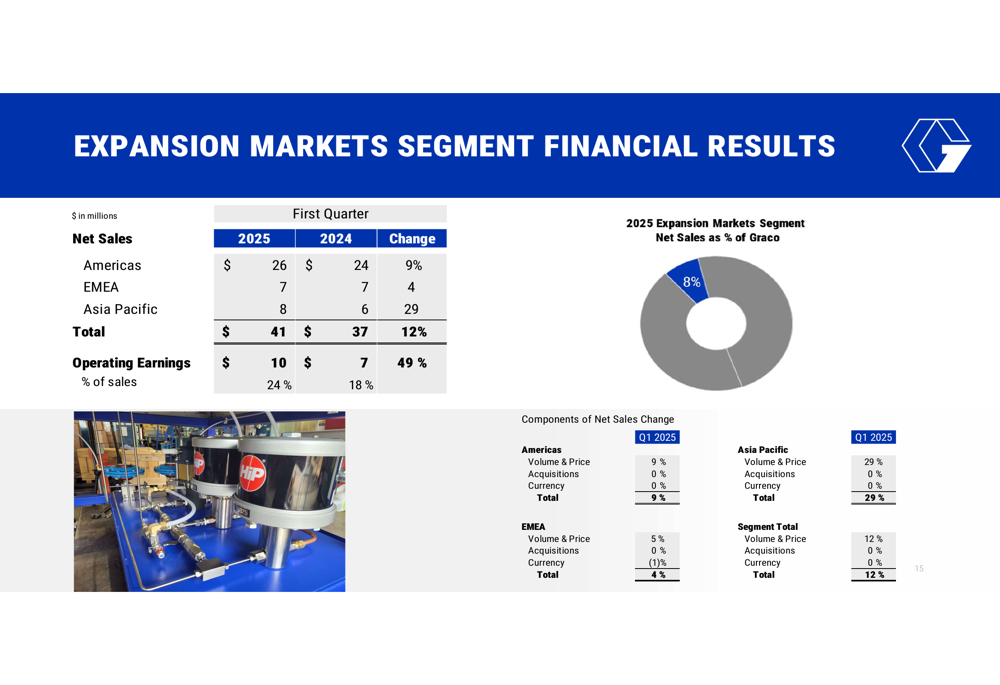

The Expansion Markets segment, though the smallest at 8% of sales, showed the strongest performance with 12% revenue growth to $41 million and an impressive 49% increase in operating earnings to $10 million. This segment’s growth was entirely organic, with operating margins expanding significantly from 18% to 24%.

Cash Flow and Capital Allocation

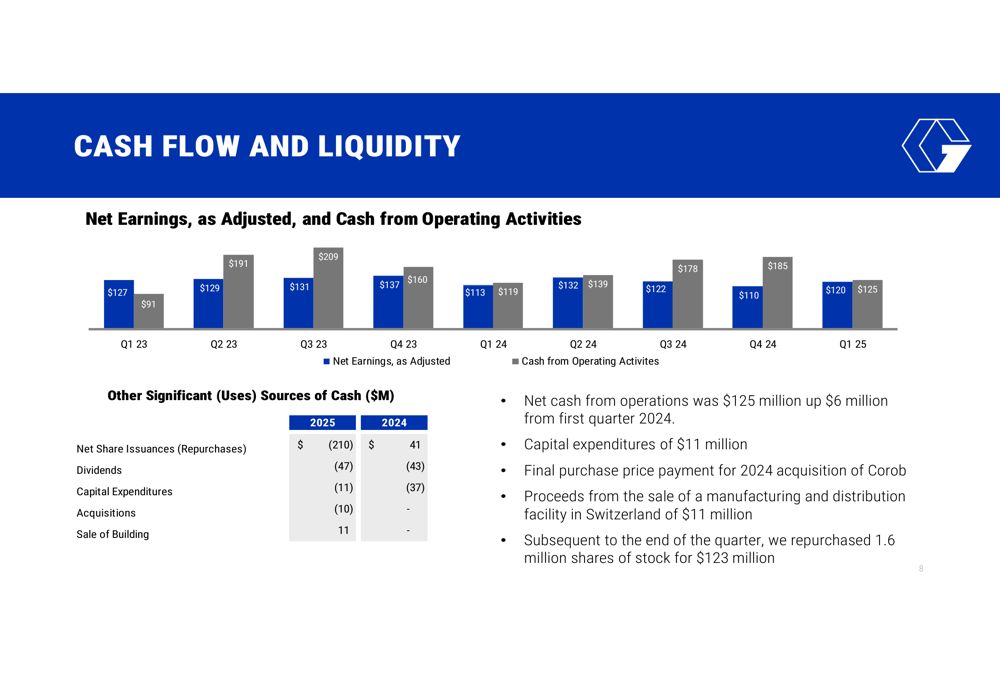

Graco maintained strong cash generation in the first quarter, with cash flow from operations reaching $125 million, up $6 million from the first quarter of 2024. Capital expenditures decreased significantly to $11 million from $37 million in the prior year.

The company’s cash allocation strategy is illustrated in the following chart:

Graco continued its shareholder return program, repurchasing 2.8 million shares during the quarter and an additional 1.6 million shares after quarter-end, for a total of 4.4 million shares year-to-date. The company paid $47 million in dividends during the quarter, up from $43 million in the first quarter of 2024.

Operating Earnings Analysis

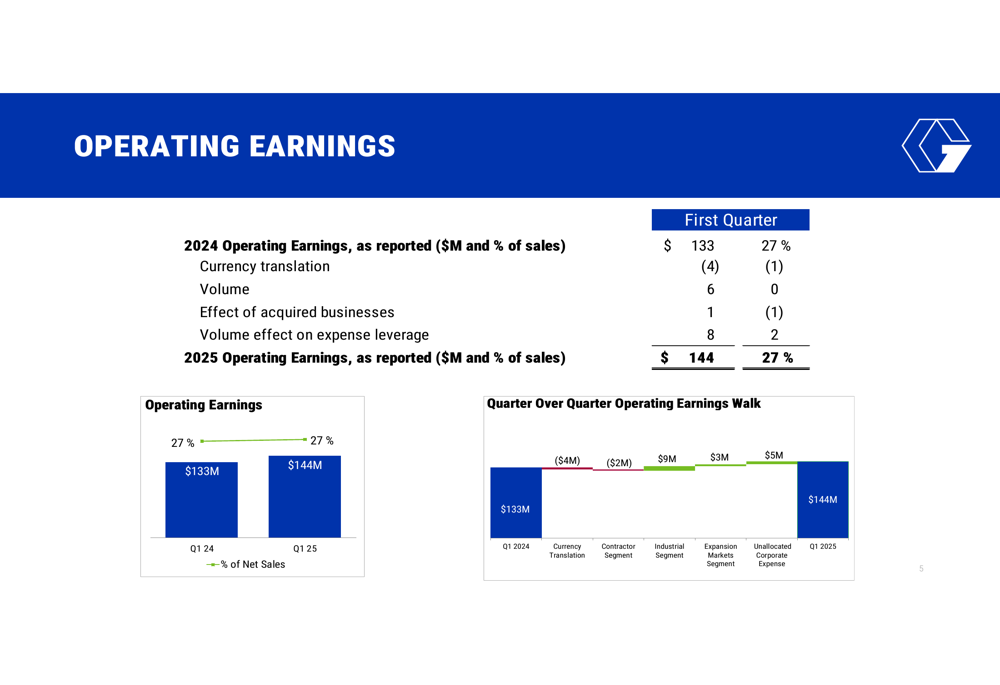

A deeper look at Graco’s operating earnings reveals the factors driving the 8% year-over-year increase. While volume growth and expense leverage contributed positively, currency translation had a negative impact.

The following chart breaks down the components of the operating earnings change:

Currency translation reduced operating earnings by $4 million, while volume added $6 million. The effect of acquired businesses contributed $1 million, and volume effect on expense leverage added $8 million. These factors combined to increase operating earnings from $133 million in Q1 2024 to $144 million in Q1 2025.

Forward Outlook

Graco management provided limited specific guidance for 2025 but noted several factors that will influence performance. The company expects capital expenditures of $50-60 million for the full year and anticipates an effective tax rate between 19.5% and 20.5%.

Management highlighted potential negative impacts from trade policies and tariffs with China, which could affect sales by 1-2%. The company also indicated it may continue opportunistic share repurchases throughout 2025.

At current exchange rates, Graco expects no impact from currency movements on full-year 2025 sales or net earnings, assuming the same volumes, mix of products, and mix of business by currency as in 2024.

Investor Implications

Despite reporting growth in sales and earnings, Graco’s heavy reliance on acquisitions for growth may concern investors, particularly as organic growth remains modest at 3%. The decline in gross margin and the significant drop in Contractor segment profitability despite sales growth suggest underlying challenges.

The premarket stock decline of 4.76% indicates investors may be focusing on these concerns rather than the headline growth numbers. However, Graco’s strong cash flow generation, active share repurchase program, and solid performance in the Industrial and Expansion Markets segments provide some positive counterbalance.

For investors, the key question will be whether Graco can successfully integrate its recent acquisitions to drive sustainable organic growth while addressing the profitability challenges in its Contractor segment. The company’s reorganization into three reporting segments may help provide greater focus and accountability in addressing these challenges going forward.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.