US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

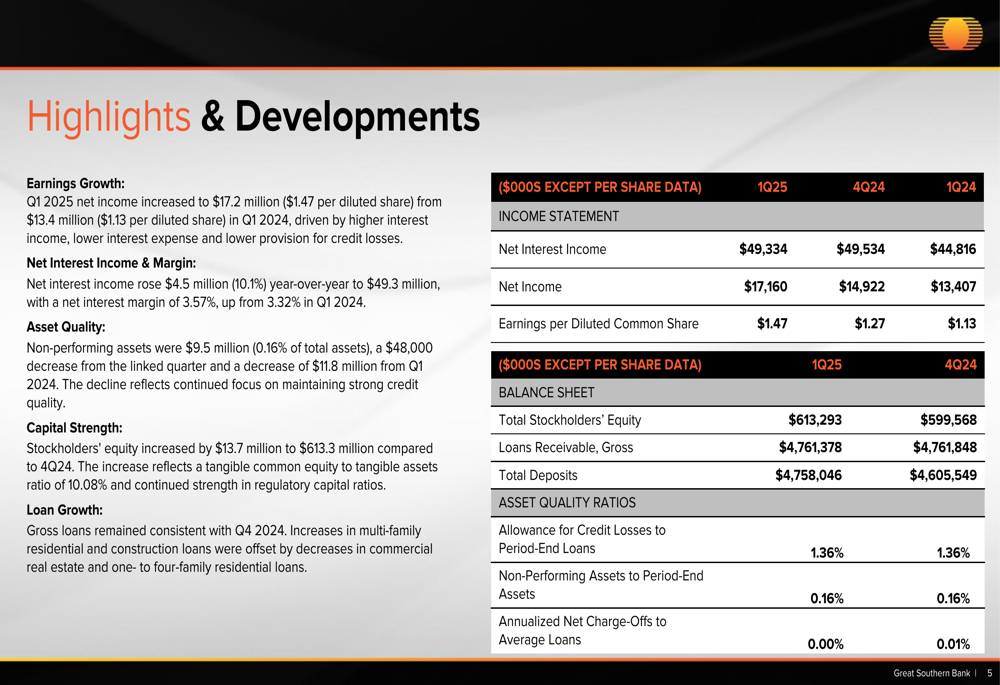

Great Southern Bancorp (NASDAQ:GSBC) reported strong first-quarter results for 2025, with net income rising 28% year-over-year as the company successfully navigated a challenging banking environment. The financial institution’s April 17 earnings presentation revealed significant margin expansion and disciplined expense management, helping drive the stock up 3.55% to close at $53.95 in the session following the announcement.

The Missouri-based regional bank demonstrated resilience amid ongoing economic uncertainties and competitive pressures in the lending market. With total assets of nearly $6 billion, Great Southern continues to maintain a conservative credit posture while focusing on relationship-based banking and strategic investments in technology.

Quarterly Performance Highlights

Great Southern reported net income of $17.2 million ($1.47 per diluted share) for Q1 2025, a substantial increase from $13.4 million ($1.13 per diluted share) in Q1 2024. This performance significantly exceeded analyst expectations of $1.29 per share, representing a positive surprise of approximately 14%.

As shown in the following highlights and developments summary, the company achieved notable improvements across several key metrics:

Net interest income rose by $4.5 million (10.1%) year-over-year to $49.3 million, with the net interest margin expanding to 3.57% from 3.32% in the prior-year period. This improvement reflects the company’s effective balance sheet management and strategic approach to controlling funding costs.

During the earnings call, CEO Joseph Turner emphasized the strength of the company’s core banking franchise, stating: "Our first quarter results reflect the strength of our core banking franchise and the continued resilience of our earnings in a dynamic operating environment amid ongoing economic and financial sector challenges."

Detailed Financial Analysis

The company’s income statement revealed strong performance, with total interest income increasing to $80.2 million, up 3.7% from Q1 2024. Meanwhile, interest expense declined to $30.9 million, a 5.1% reduction year-over-year, primarily driven by an 11% decrease in deposit-related costs.

The following chart illustrates the positive trend in net interest margin and income:

Non-interest income totaled $6.6 million for the quarter, representing a modest 3.2% decrease from $6.8 million in Q1 2024. This decline was primarily attributed to small decreases in commissions, overdraft fees, and net gains on mortgage loan sales.

On the expense side, Great Southern maintained tight control, with total non-interest expense remaining relatively flat at $34.8 million, just a 1.2% increase from the prior-year period. This disciplined approach to cost management helped improve the efficiency ratio to 62.27% from 66.68% in Q1 2024.

Asset Quality & Loan Portfolio

Great Southern’s asset quality metrics remained exceptionally strong, with non-performing assets at just $9.5 million or 0.16% of total assets. The company did not record a provision for credit losses on its outstanding loan portfolio during the quarter, compared to a $500,000 expense in Q1 2024, reflecting confidence in the quality of its loan book.

The following chart highlights the company’s solid asset quality metrics:

The loan portfolio remained essentially flat at $4.77 billion compared to year-end 2024, reflecting both limited loan demand and the company’s disciplined approach to credit underwriting. The portfolio remains well-diversified across various categories, with multifamily ($1.59 billion) and commercial real estate ($1.49 billion) representing the largest segments.

Geographically, the loan portfolio shows diversification across multiple regions, with significant concentrations in the Midwest, Florida, and Texas:

Capital Management & Shareholder Returns

Great Southern’s capital position remained robust, with stockholders’ equity increasing to $613.3 million, or 10.23% of total assets, up from $565.2 million at March 31, 2024. This strong capital base provides flexibility for both organic growth and shareholder returns.

The following chart illustrates the company’s solid capital position:

All regulatory capital ratios exceed requirements by a comfortable margin, as shown in this comparison:

During the quarter, the company repurchased approximately 173,000 shares for $10.2 million while declaring cash dividends of $4.6 million. The Board of Directors approved a new stock repurchase authorization for up to an additional 1 million shares once the existing program (with approximately 270,000 shares remaining) is completed.

CFO Rex Copeland noted during the earnings call: "We remain committed to managing costs effectively through continuous optimization of our operations and streamlining of expenditures. At the same time, we are making strategic investments in key areas that will drive long-term growth and enhance our competitive position."

Strategic Initiatives & Outlook

Looking ahead, Great Southern remains focused on protecting margins and proactively managing credit quality. The company anticipates modest benefits from certificate of deposit maturities in the coming quarters, though management indicated these would not be substantial.

Regarding the interest rate environment, the company maintains a neutral interest rate risk posture. Management noted that while an immediate 50 basis point rate cut might have a slightly negative impact initially, they expect to recover quickly due to their balanced asset-liability structure.

The competitive lending environment continues to present challenges, with Turner acknowledging during the earnings call that "activity is maybe down a little bit. There’s quite a bit of competition among banks for what loans there are. And so but there’s not a lot of loans to start with."

Despite these challenges, Great Southern’s strong capital position, disciplined expense management, and focus on relationship banking position the company well to navigate the current economic environment and continue delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.