US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

Great Southern Bancorp Inc (NASDAQ:GSBC) recently released its Q2 2025 loan portfolio presentation, revealing improved asset quality despite a contraction in overall loan volume. The presentation follows the company’s quarterly earnings report where it beat EPS expectations with $1.72 per share (29.32% above forecasts) while missing revenue targets with $51 million (8.29% below expectations).

The bank’s stock has shown resilience in a challenging market, trading at $60.51 as of July 18, 2025, despite a 2.67% daily decline. The shares remain comfortably above their 52-week low of $47.57 but below the high of $68.02, reflecting investor confidence in the company’s profitability despite revenue challenges.

Loan Portfolio Composition and Trends

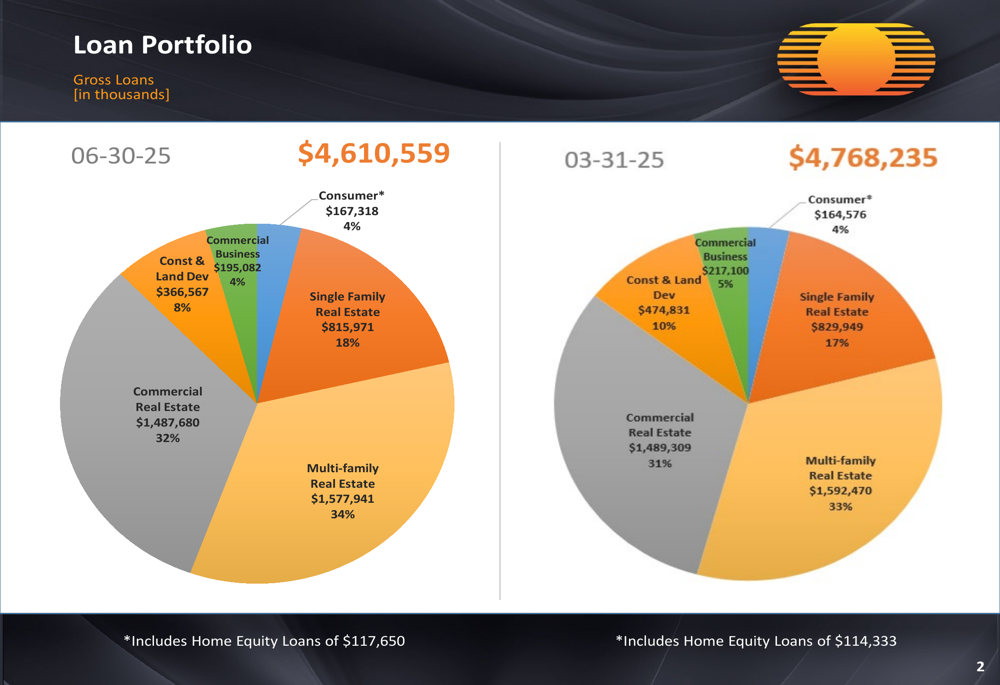

Great Southern’s loan portfolio totaled $4.61 billion as of June 30, 2025, representing a 3.3% decrease from $4.77 billion at the end of the previous quarter. This contraction aligns with management’s cautious stance on loan growth in what CEO Joe Turner described as a "pretty competitive environment" with "less opportunity than we’ve seen in bigger years."

The portfolio remains well-diversified across several loan categories, with Multi-family Real Estate and Commercial Real Estate comprising the largest segments at 34% and 32% respectively.

As shown in the following chart of the bank’s loan portfolio composition:

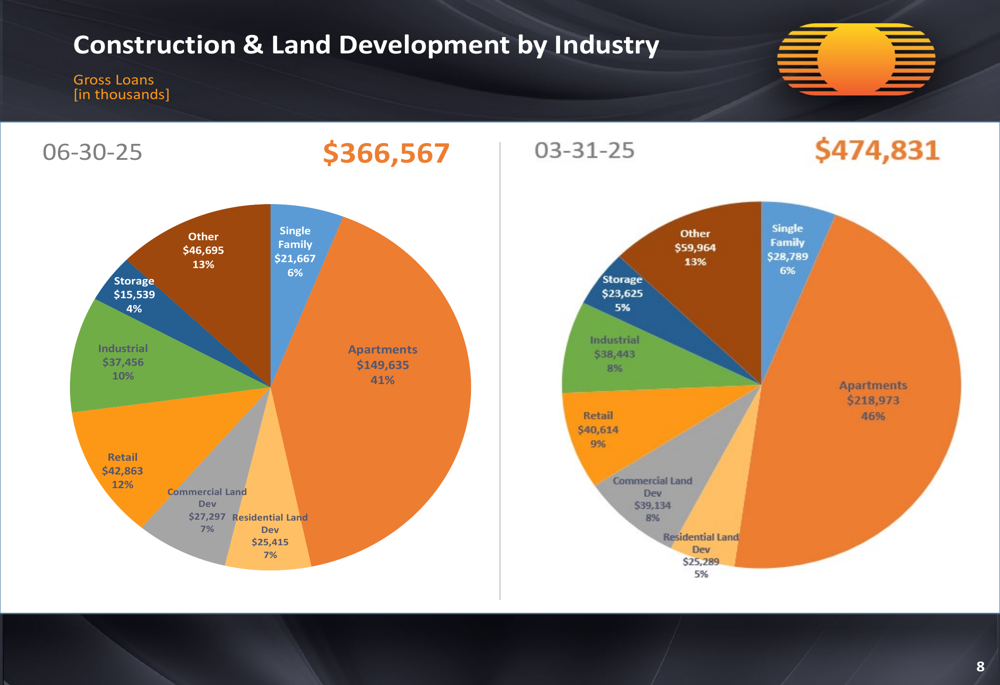

The most significant quarterly change occurred in the Construction & Land Development segment, which decreased by 22.8% from $474.8 million to $366.6 million. This reduction likely reflects the bank’s strategic decision to limit exposure in this sector amid economic uncertainties.

Geographic Diversification Strategy

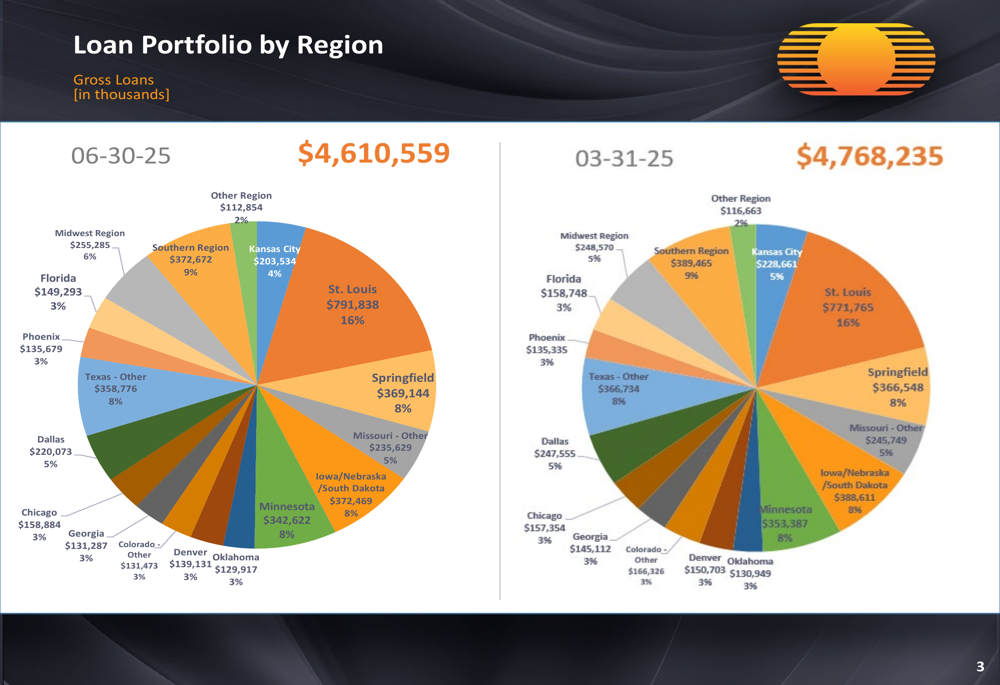

Great Southern maintains a geographically diversified loan portfolio spanning multiple regions, with St. Louis representing the largest concentration at 16%, followed by the Southern Region at 9%, and Springfield and Texas-Other each at 8%.

The following regional breakdown illustrates the bank’s geographic diversification strategy:

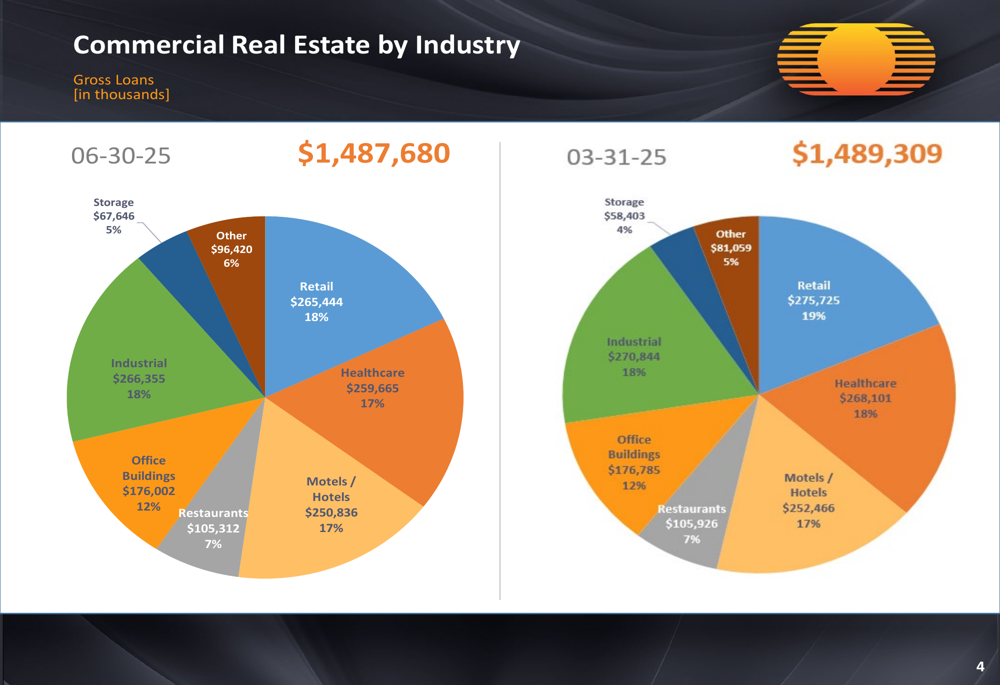

Within the Commercial Real Estate portfolio, which totals $1.49 billion, the bank maintains balanced exposure across various industries, with Retail, Industrial, Healthcare, and Motels/Hotels each representing 17-18% of the segment.

The Commercial Real Estate portfolio’s industry composition is illustrated here:

The geographic distribution of Commercial Real Estate loans shows significant concentrations in St. Louis (18%), Southern Region (13%), Midwest Region (10%), and Chicago (10%), demonstrating the bank’s focus on markets where it has established expertise.

Asset Quality and Risk Management

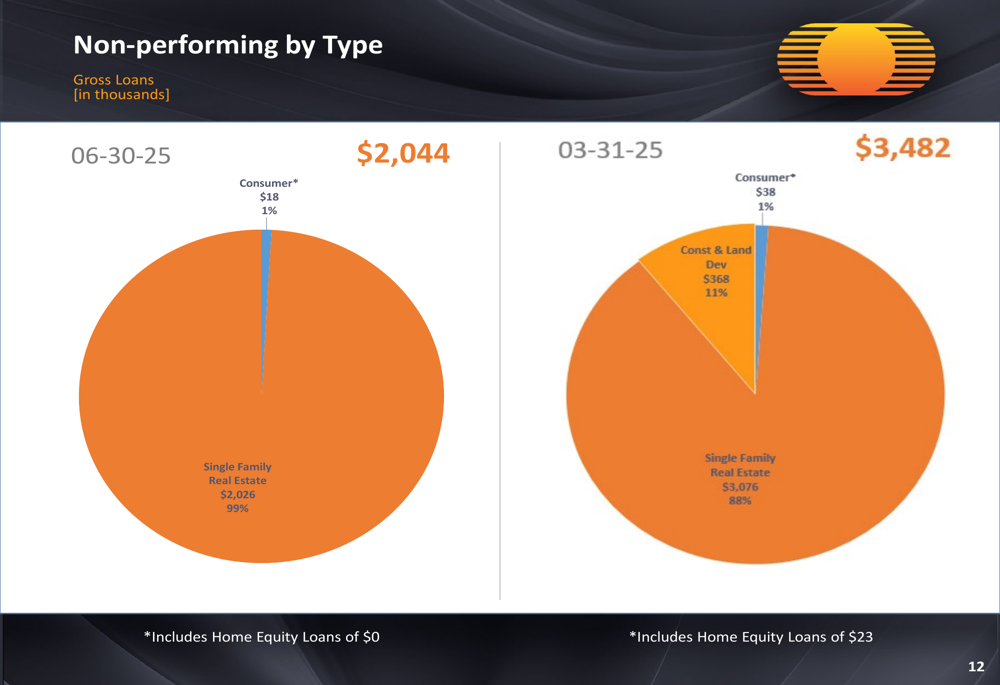

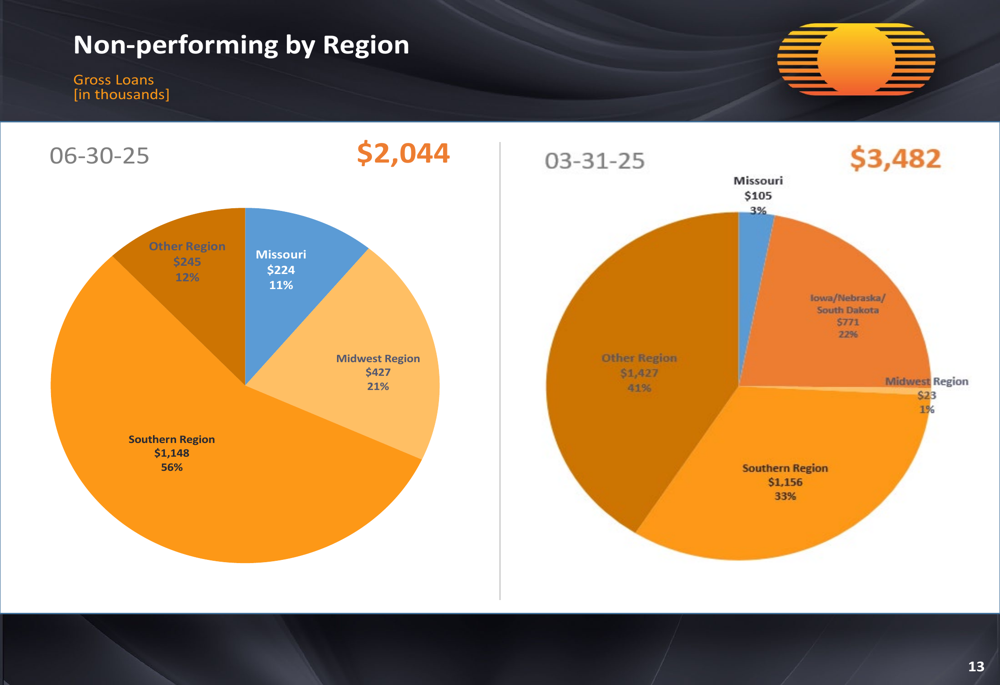

One of the most notable improvements in Great Southern’s portfolio is the significant reduction in non-performing loans, which decreased by 41.3% from $3.48 million in March 2025 to $2.04 million in June 2025. This improvement supports management’s assertion of "strong asset quality" mentioned in the recent earnings call.

The composition of non-performing loans has also shifted dramatically, with Single Family Real Estate now accounting for 99% of all non-performing loans, compared to 88% in the previous quarter.

The following chart details this improvement in non-performing loans:

The regional distribution of non-performing loans shows concentration in the Southern Region (56%) and Midwest Region (21%), with the remainder spread across Missouri and other regions.

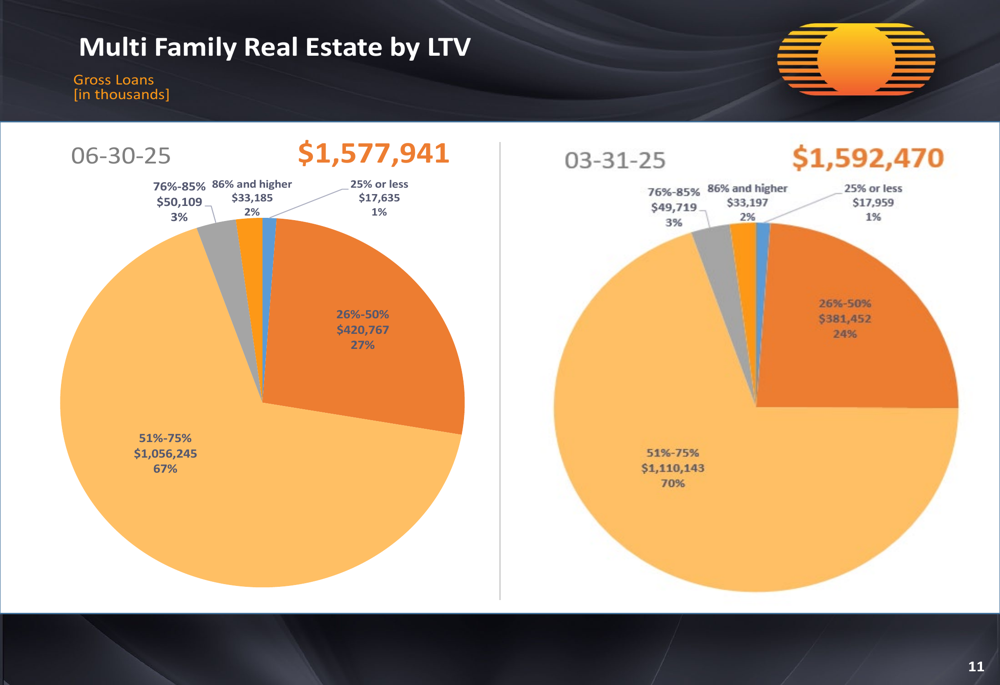

The bank’s risk management approach is also evident in its loan-to-value (LTV) ratios for Multi-Family Real Estate, where 67% of loans fall within the 51-75% LTV range and 27% in the 26-50% range, indicating conservative underwriting practices.

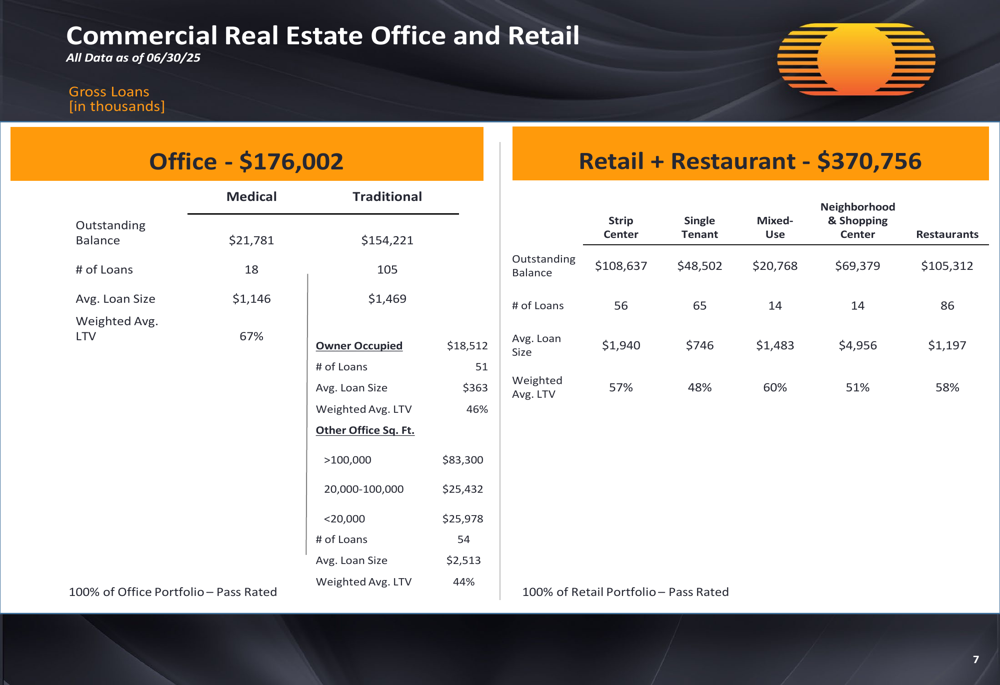

Further demonstrating the quality of the Commercial Real Estate portfolio, the presentation notes that 100% of both Office and Retail portfolios are Pass Rated, with weighted average LTVs ranging from 44% to 67% depending on the property type.

Strategic Positioning and Outlook

Great Southern’s presentation reveals a strategic focus on maintaining portfolio quality over growth in a challenging competitive environment. This approach appears to be paying dividends, as evidenced by the bank’s strong Q2 2025 profitability despite revenue challenges.

The detailed breakdown of Commercial Real Estate Office and Retail segments provides insight into the bank’s careful management of potentially vulnerable sectors:

The Construction & Land Development portfolio shows a strategic emphasis on apartments (41%), retail (12%), and industrial (10%) sectors, with a significant reduction in overall exposure compared to the previous quarter.

These strategic choices align with CFO Rex Copeland’s statement during the earnings call that the company is "focused on maintaining strong cost discipline by continually refining our operations." The bank’s cautious approach to lending in the current environment, combined with its focus on asset quality, positions it well for sustainable profitability despite the challenges of loan growth.

Looking ahead, Great Southern faces potential margin challenges in Q4 due to the termination of interest rate swaps, as noted in the earnings call. However, the bank’s strong asset quality, diversified portfolio, and disciplined approach to risk management provide a solid foundation for navigating these challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.