Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

GSK plc (NYSE:GSK) presented its Q1 2025 financial results on April 30, 2025, reporting solid performance with sales growth of 4% at constant exchange rates (CER). The pharmaceutical giant continues to execute its strategy of focusing on high-growth specialty medicines while advancing its robust pipeline of potential blockbuster treatments.

The company’s shares responded positively to the results, with premarket trading showing a 1.85% increase to $39.69, building on the previous day’s 2.39% gain. This performance comes as GSK maintains momentum from its strong 2024, when it reported 9% sales growth and 19% profit growth for the year.

Quarterly Performance Highlights

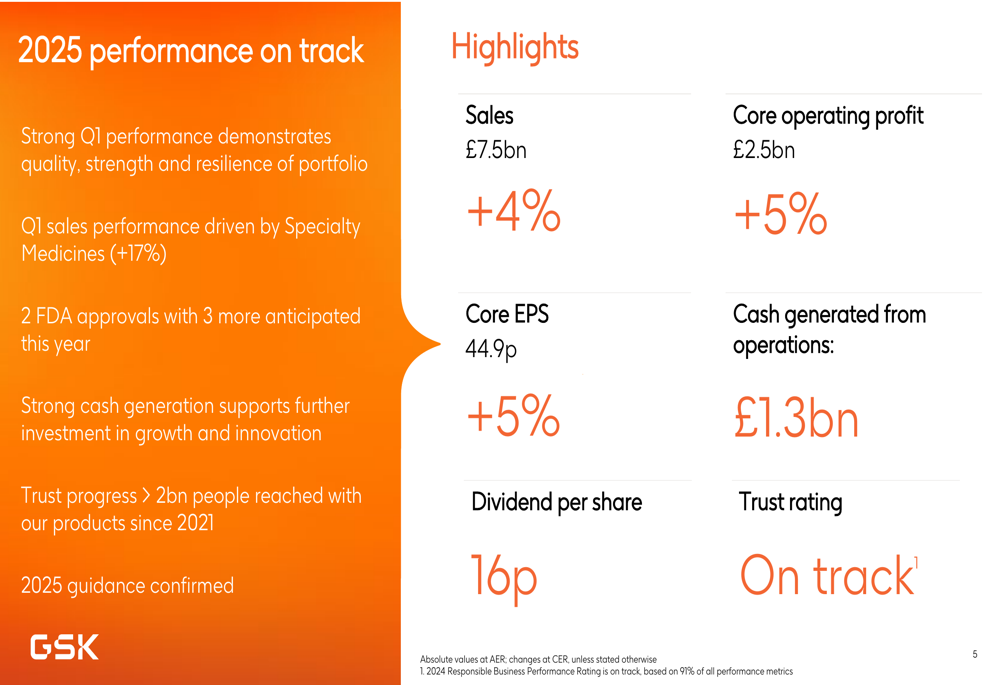

GSK reported Q1 2025 sales of £7.5 billion, representing a 4% increase at CER compared to the same period last year. Core operating profit rose 5% to £2.5 billion, while core earnings per share (EPS) grew 5% to 44.9p. The company declared a dividend of 16p per share for the quarter.

As shown in the following performance highlights slide, GSK’s trust rating remains on track, with the company reaching over 2 billion people with its products since 2021:

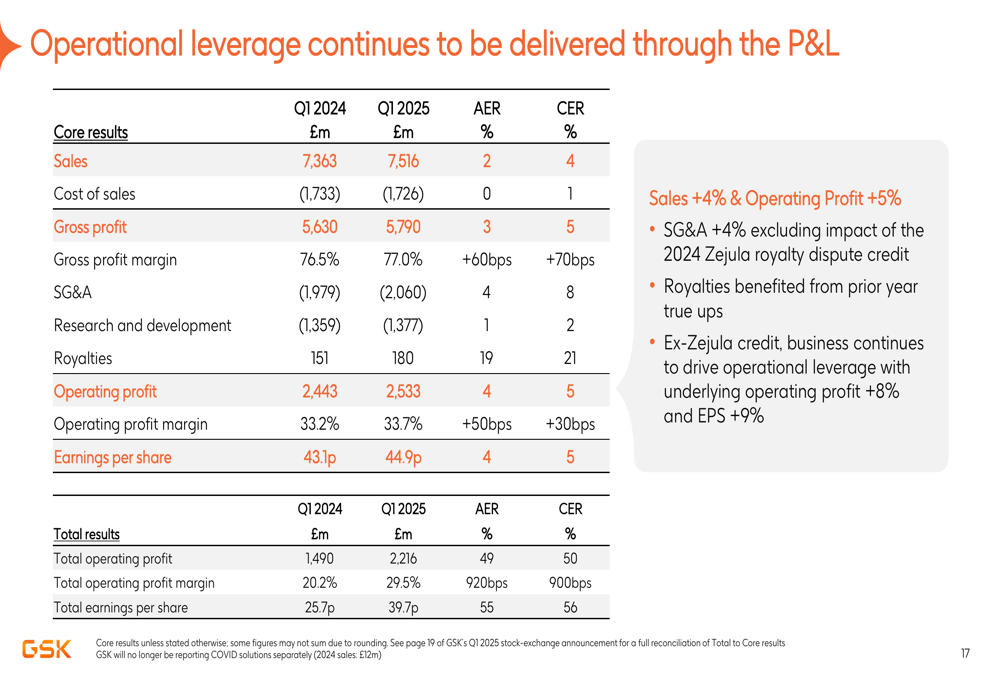

Cash generated from operations reached £1.3 billion, supporting continued investment in growth and innovation. The company’s operational leverage continues to improve, with the core operating margin increasing by 30 basis points at CER (130 basis points excluding a one-time Zejula settlement).

The following slide illustrates how operational leverage is being delivered through the P&L statement:

Product Portfolio Performance

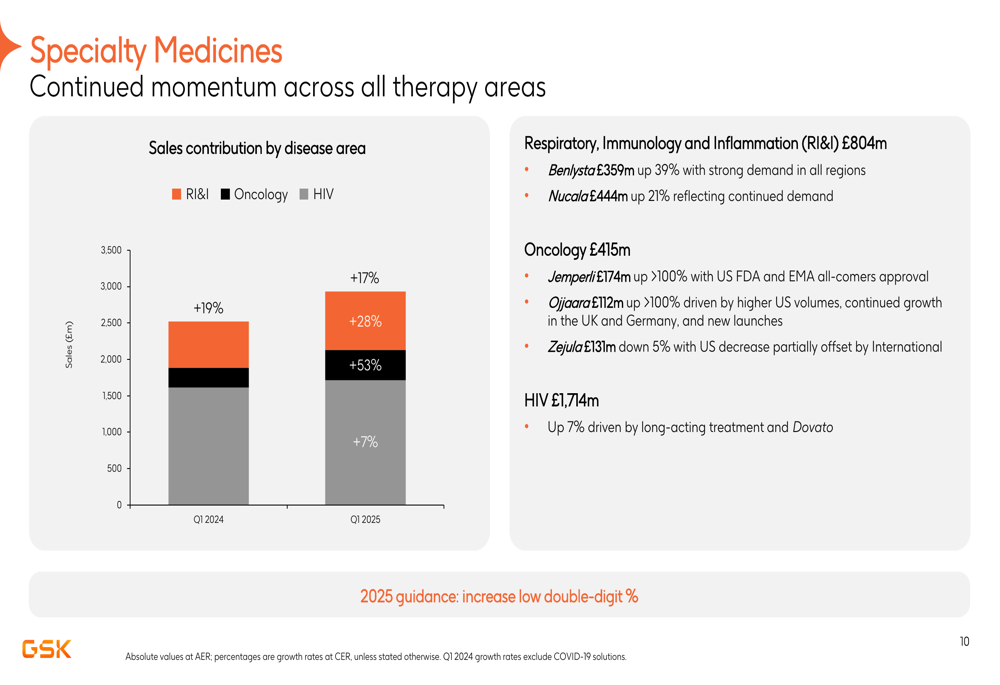

GSK’s growth in Q1 was primarily driven by its Specialty Medicines division, which grew 17% and now represents the company’s largest segment. Within this division, Respiratory, Immunology and Inflammation (RI&I) grew 28% to £804 million, Oncology increased 53% to £415 million, and HIV rose 7% to £1,714 million.

The following chart shows the strong momentum across all therapy areas within Specialty Medicines:

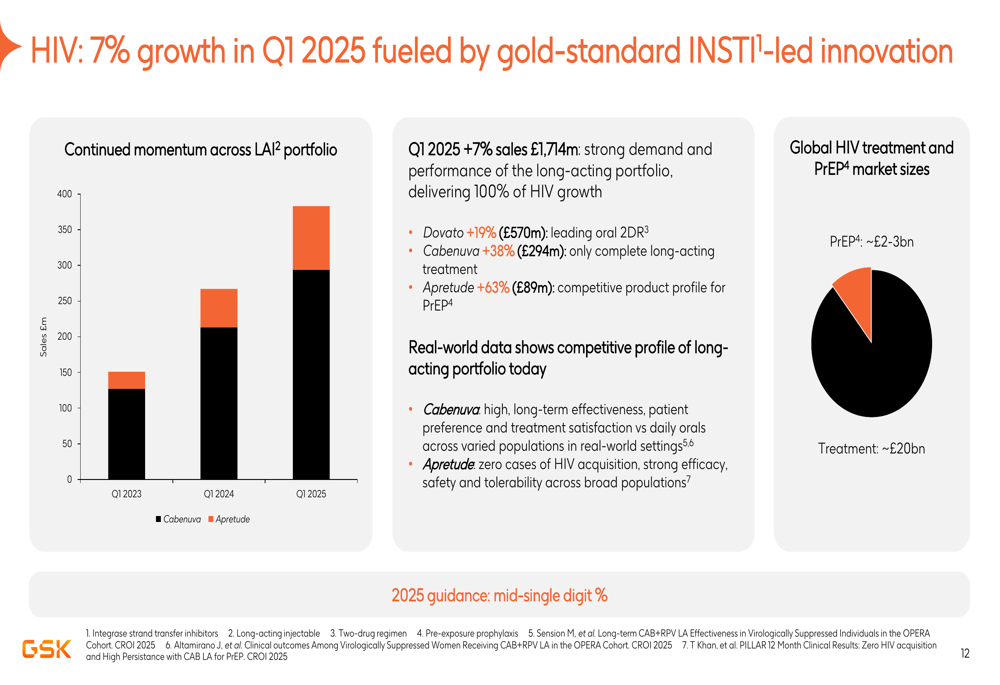

The HIV portfolio continues to perform well, with 7% growth in Q1 2025 fueled by innovation in integrase strand transfer inhibitor (INSTI)-led treatments. Dovato grew 19% to £570 million, while Cabenuva, the only complete long-acting HIV treatment, increased 38% to £294 million. Apretude, GSK’s preventive treatment, grew 63% to £89 million.

As illustrated in the following slide, GSK is targeting both the HIV treatment market (estimated at ~£20 billion) and the pre-exposure prophylaxis (PrEP) market (estimated at ~£2-3 billion):

The Vaccines segment faced expected headwinds, with Shingrix sales declining 6% and RSV vaccine Arexvy dropping 57%. However, Meningitis vaccines showed strong growth of 20%. General Medicines remained stable with 4% growth, supported by continued strong performance from Trelegy.

Pipeline and Future Growth Drivers

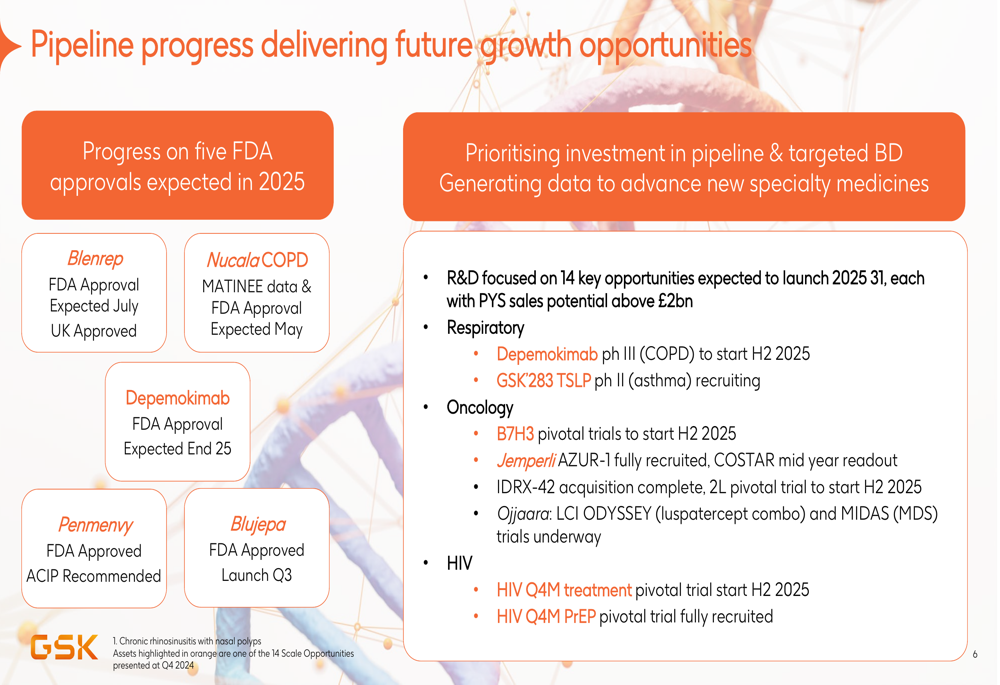

GSK highlighted significant pipeline progress that is expected to deliver future growth opportunities. The company anticipates five FDA approvals in 2025, including Blenrep for multiple myeloma (expected July), Nucala for COPD (expected May), and Depemokimab for respiratory conditions (expected end of 2025). Two products, Penmenvy and Blujepa, have already received FDA approval.

The following slide details these pipeline assets and their potential:

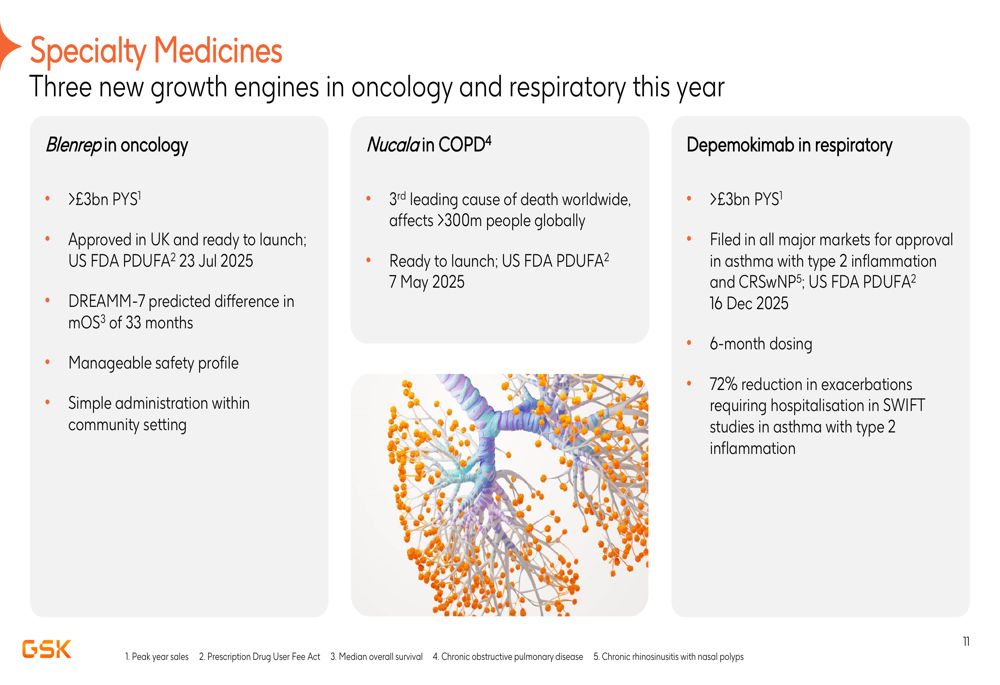

The company is particularly focused on three new growth engines within Specialty Medicines: Blenrep in oncology (with potential peak year sales exceeding £3 billion), Nucala in COPD (targeting a disease that affects over 300 million people globally), and Depemokimab in respiratory (with potential peak year sales exceeding £3 billion).

As shown in the following slide, these three products represent significant growth opportunities:

Financial Analysis

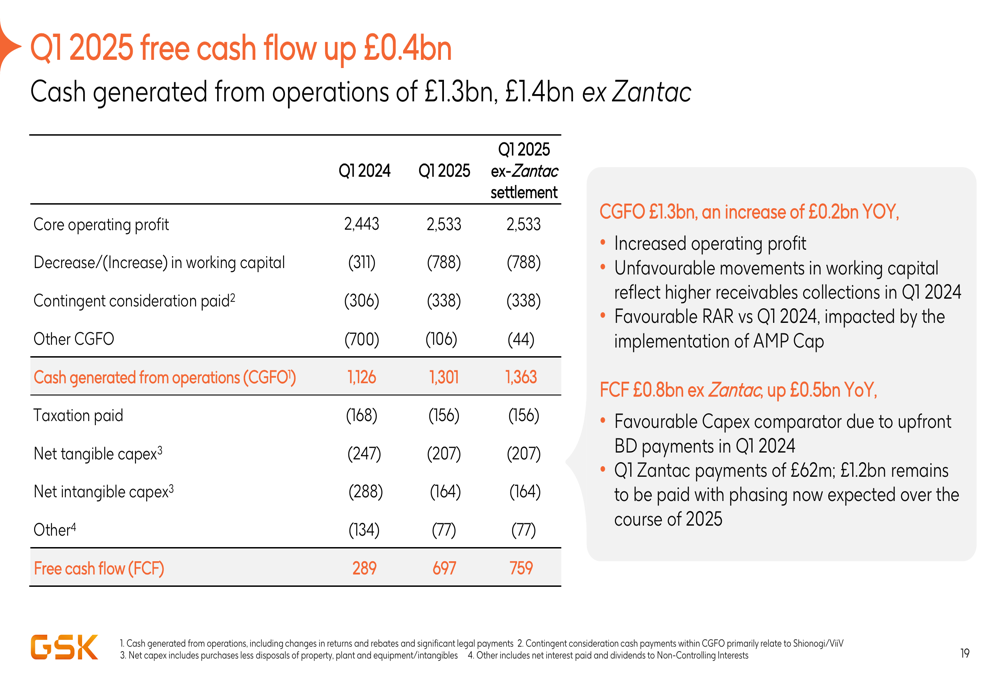

GSK’s free cash flow increased by £0.4 billion in Q1 2025, with cash generated from operations of £1.3 billion (£1.4 billion excluding Zantac-related payments). This strong cash generation supports the company’s capital deployment strategy, which prioritizes business growth and shareholder returns.

The following slide illustrates the company’s Q1 2025 free cash flow performance:

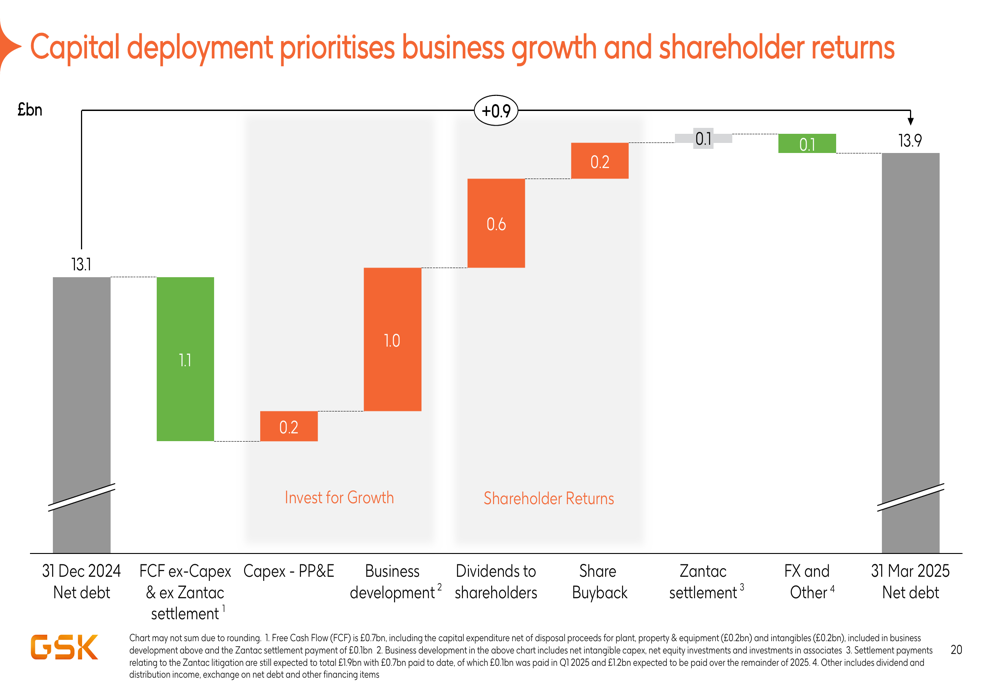

Net debt stood at £13.9 billion as of March 31, 2025, reflecting investments in business development, capital expenditures, dividends to shareholders, and share buybacks. The company continues to maintain a disciplined approach to capital allocation, as shown in the following capital deployment slide:

Forward-Looking Statements

GSK confirmed its full-year 2025 guidance, projecting sales growth of 3-5%, core operating profit growth of 6-8%, and core EPS growth of 6-8%. The company expects Specialty Medicines to grow at a low double-digit percentage rate, while HIV is forecast to grow at a mid-single-digit rate. Vaccines are expected to decline at a low single-digit rate, while General Medicines is projected to remain broadly stable.

Looking further ahead, GSK remains confident in its 2021-2026 outlook of more than 7% sales CAGR and more than 11% core operating profit CAGR. By 2031, the company aims to achieve sales exceeding £40 billion while maintaining margin improvement.

As CEO Emma Walmsley stated in the presentation: "We are on track to deliver 2025 guidance demonstrating agility, resilience and strength of portfolio. We remain focused on delivering future growth opportunities and investing in pipeline & targeted BD. We are confident in our ability to sustain profitable growth through the decade and beyond."

GSK’s robust pipeline, with 70 potential new vaccines and medicines in development, positions the company well for sustained growth despite near-term challenges in its vaccines business. The company’s strategic focus on high-growth specialty medicines, particularly in oncology, HIV, and respiratory areas, provides multiple avenues for future expansion as it continues to execute on its long-term growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.