Veeco launches Lumina+ MOCVD system, receives Rocket Lab order

Introduction & Market Context

Harmony Biosciences Holdings (NASDAQ:HRMY) presented its Q2 2025 financial results on August 5, 2025, highlighting continued revenue growth and significant profit expansion. Despite the strong quarterly performance, the company’s shares were trading down 5.74% in pre-market at $33.50, suggesting investors may have had higher expectations or were responding to other market factors.

The biopharmaceutical company, focused on developing and commercializing therapies for patients with rare neurological diseases, reported its sixteenth consecutive quarter of growth for WAKIX (pitolisant), its flagship narcolepsy treatment that is now approaching blockbuster status.

Quarterly Performance Highlights

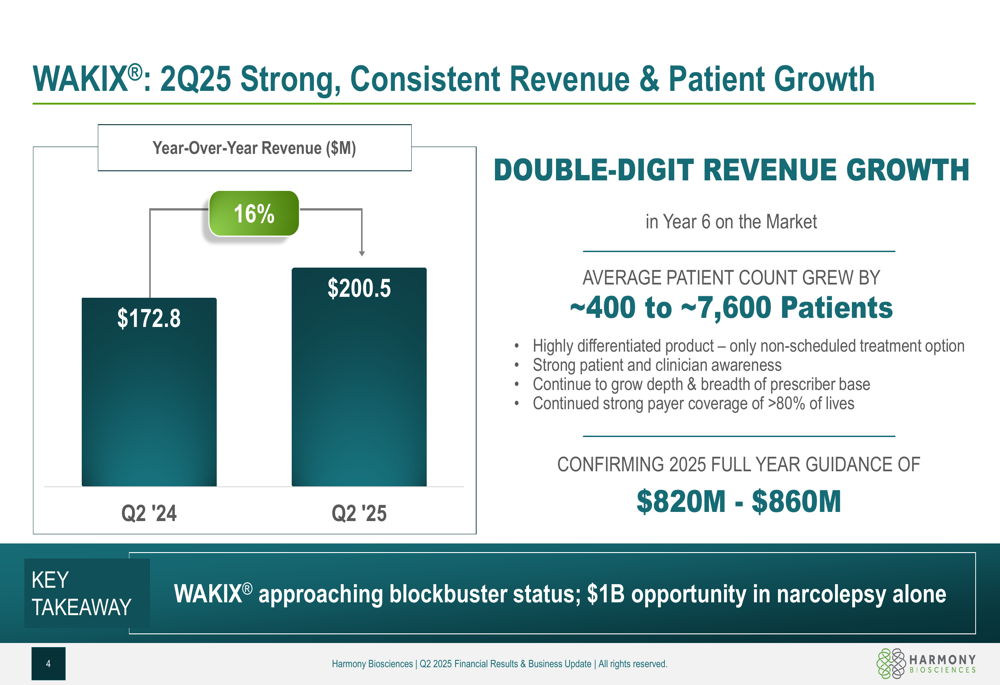

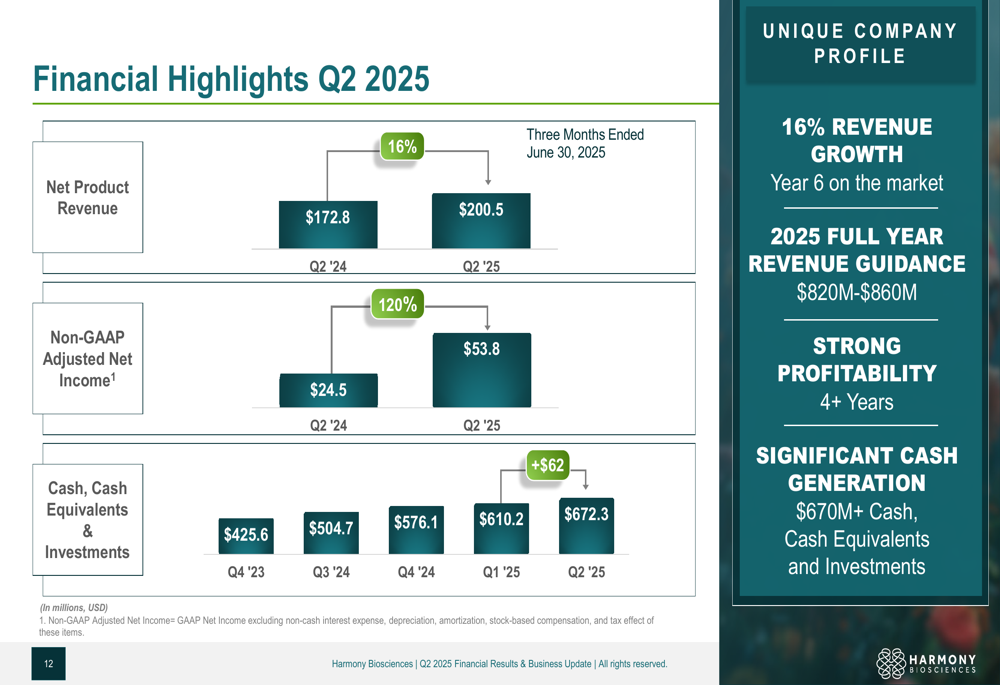

Harmony (JO:HARJ) reported Q2 2025 net product revenue of $200.5 million, representing a 16% increase compared to $172.8 million in the same period last year. The company’s non-GAAP adjusted net income surged 120% year-over-year to $53.8 million, while GAAP net income reached $39.8 million, a remarkable 243% increase from Q2 2024.

As shown in the following quarterly revenue comparison:

The company’s average patient count grew by approximately 400 patients to reach 7,600 in the quarter. Management attributed this growth to WAKIX’s differentiated product profile, strong patient and clinician awareness, continued expansion of the prescriber base, and robust payer coverage exceeding 80% of covered lives.

WAKIX Commercial Success

WAKIX continues to be the primary growth driver for Harmony, with the company highlighting that the product is approaching blockbuster status, representing a $1 billion opportunity in narcolepsy alone. The company reaffirmed its full-year 2025 revenue guidance of $820-$860 million.

The company’s unique profile combines commercial success with pipeline development, as illustrated in this overview:

Harmony emphasized its self-funding capabilities across the enterprise, with over four years of consistent profitability and a strong balance sheet showing $672.3 million in cash and investments, a 55% increase year-over-year.

Pipeline Development and Catalysts

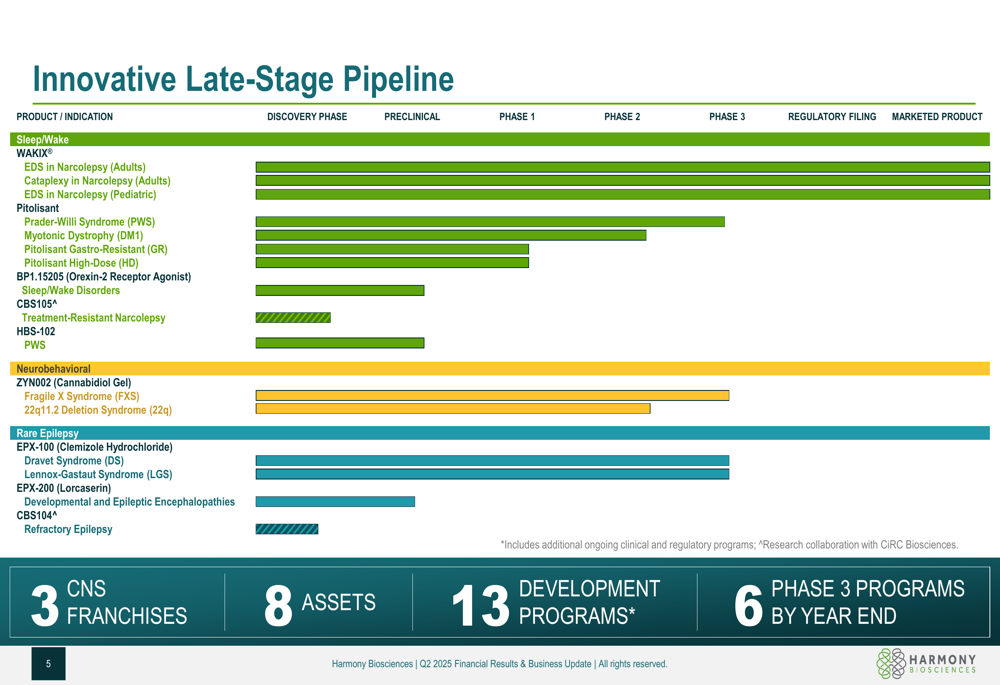

The company’s presentation highlighted its expanding late-stage pipeline across three CNS franchises: Sleep/Wake disorders, Neurobehavioral disorders, and Rare Epilepsy. By year-end, Harmony expects to have eight assets in development across 13 programs, including six Phase 3 programs.

The following pipeline overview demonstrates the breadth of the company’s development efforts:

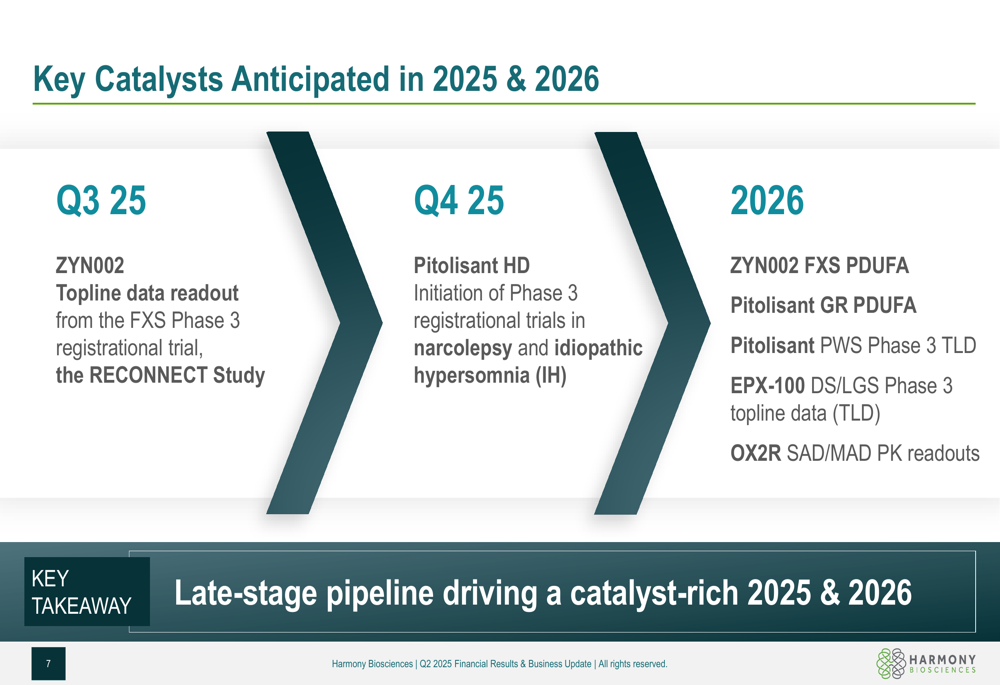

Key upcoming catalysts include ZYN002 topline data readout from the Phase 3 RECONNECT study in Fragile X Syndrome expected in Q3 2025, and the initiation of Pitolisant HD Phase 3 registrational trials in narcolepsy and idiopathic hypersomnia in Q4 2025.

The timeline for these and other significant developments is illustrated below:

The company highlighted ZYN002 as a potential first-to-market treatment for Fragile X Syndrome, a condition affecting approximately 80,000 patients in the US with high unmet medical needs. The RECONNECT study has been designed to increase probability of success based on insights from previous trials.

Financial Analysis

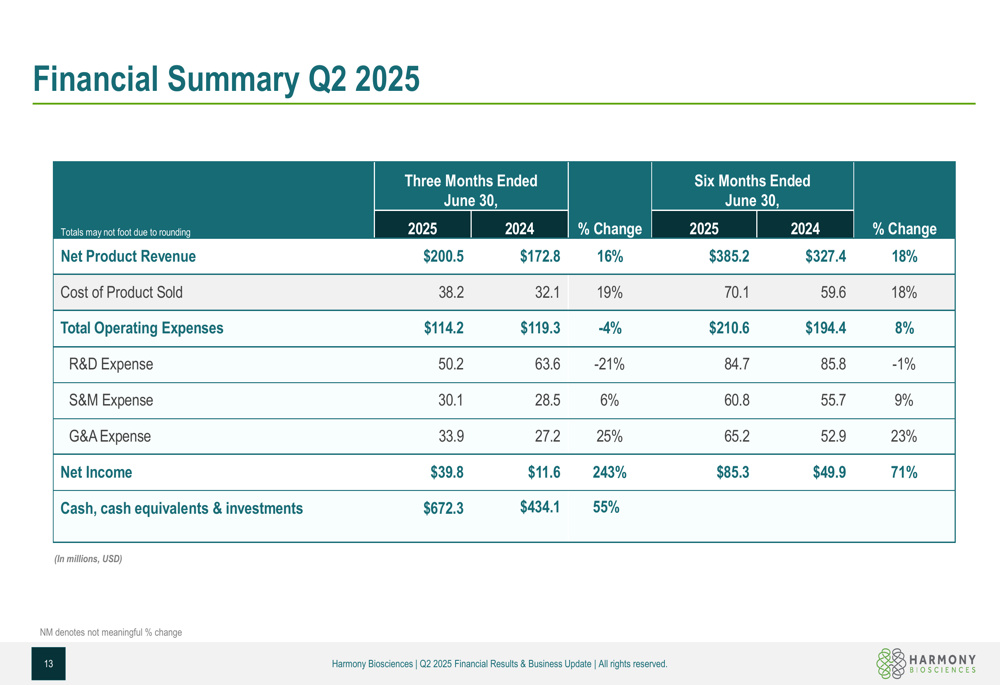

Harmony’s financial performance showed strength across multiple metrics. The company’s operating expenses decreased by 4% to $114.2 million for the quarter, with R&D expenses declining 21% to $50.2 million compared to the same period last year.

The following financial summary provides a comprehensive view of the company’s performance:

The company’s non-GAAP adjusted net income of $53.8 million for Q2 2025 reflects adjustments for non-cash interest expense, depreciation, amortization, stock-based compensation, and related tax effects. This represents a substantial improvement from the $24.5 million reported in Q2 2024.

The financial highlights demonstrate Harmony’s continued growth trajectory:

Forward-Looking Statements

Looking ahead, Harmony emphasized several growth drivers across its portfolio. In the Sleep/Wake franchise, the company plans to initiate Phase 3 registrational trials for Pitolisant HD in Q4 2025 and commence first-in-human studies for BP1.15205 in the second half of 2025.

For its Neurobehavioral franchise, the company expects topline data from the ZYN002 Phase 3 RECONNECT study in Q3 2025, with plans to initiate another Phase 3 trial in 22q deletion syndrome in Q4 2025. In the Epilepsy franchise, ongoing Phase 3 trials for EPX-100 (ARGUS & LIGHTHOUSE studies) are expected to yield topline data in 2026.

Harmony’s management expressed confidence in the company’s ability to deliver on its dual mission of providing meaningful treatments for patients with unmet medical needs while delivering strong value to shareholders. The company’s catalyst-rich pipeline, profitability, and strong cash position position it as a meaningful investment opportunity in the biotech sector, despite the pre-market stock decline following the earnings presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.