US stock futures inch lower after Wall St marks fresh records on tech gains

Introduction & Market Context

Hasbro Inc (NASDAQ:HAS) released its second quarter 2025 earnings presentation on July 23, revealing mixed results but an improved outlook for the full year. The company’s stock responded positively in premarket trading, rising 3.13% to $80.00, approaching its 52-week high of $78.83.

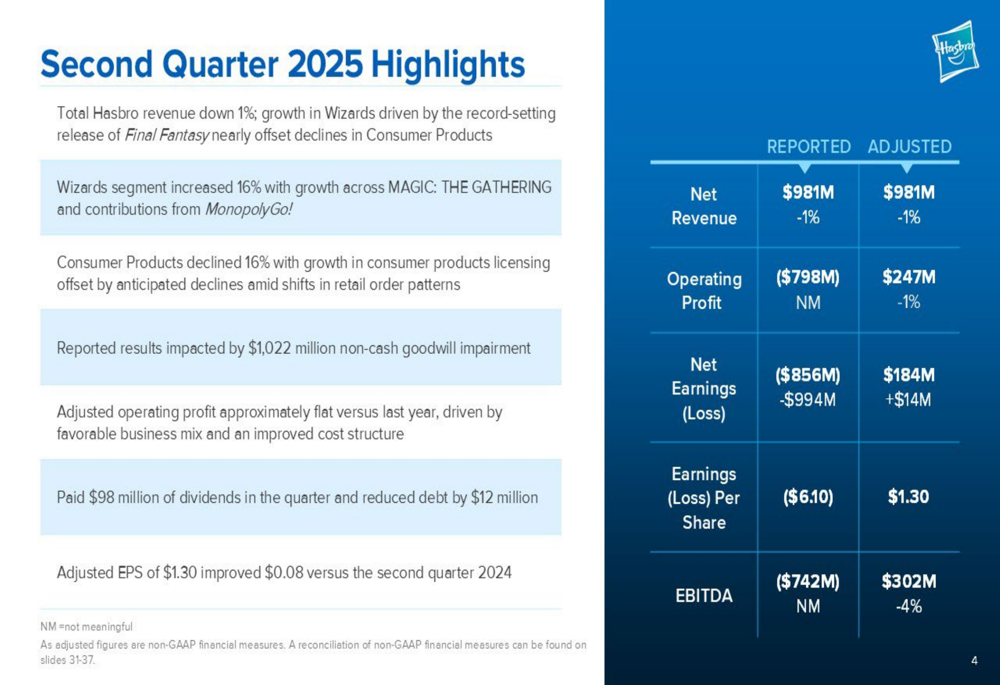

The toymaker reported Q2 revenue of $981 million, down 1% year-over-year, with strong performance in its Wizards of the Coast segment offset by weakness in Consumer Products. While reported results were significantly impacted by a $1.02 billion non-cash goodwill impairment, adjusted figures showed stability with slight improvements in profitability.

As shown in the following summary of Q2 performance highlights:

Quarterly Performance Highlights

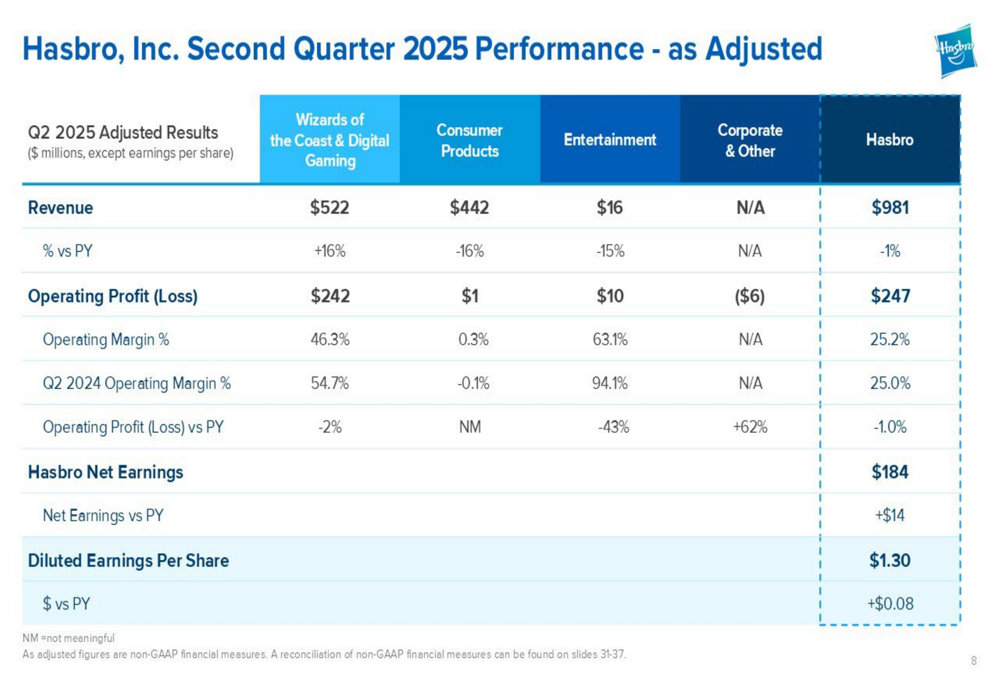

Hasbro’s second quarter results revealed divergent performance across its business segments. The Wizards of the Coast & Digital Gaming segment continued its strong momentum with 16% revenue growth to $522 million, driven primarily by Magic: The Gathering and Monopoly Go!. This segment maintained an impressive 46.3% operating margin.

In contrast, the Consumer Products segment declined 16% to $442 million, though the company noted growth in consumer products licensing partially offset anticipated declines amid shifts in retail order patterns. The Entertainment segment, now much smaller following previous divestitures, saw a 15% decline to $16 million.

The following table provides a detailed breakdown of Hasbro’s Q2 performance by segment on an adjusted basis:

Despite the revenue decline, Hasbro’s adjusted operating profit remained nearly flat year-over-year at $247 million, with adjusted operating margin improving slightly to 25.2%. Adjusted earnings per share increased to $1.30, up $0.08 from Q2 2024, reflecting the company’s ongoing cost-saving initiatives and favorable business mix.

Detailed Financial Analysis

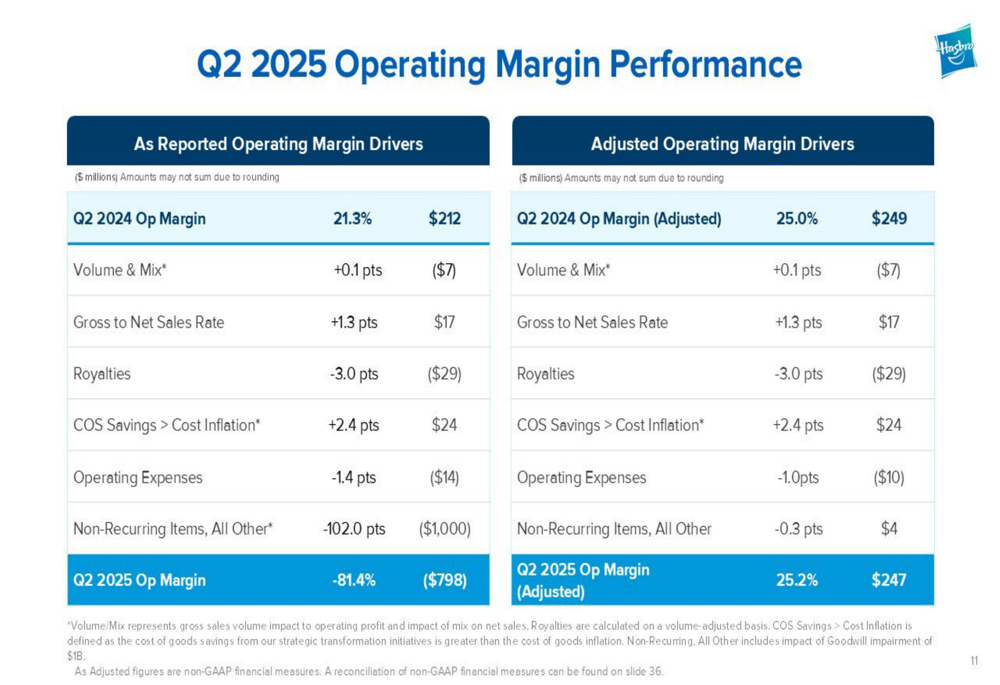

Hasbro’s reported results were significantly impacted by a $1.02 billion non-cash goodwill impairment, resulting in a reported operating loss of $798 million and reported loss per share of $6.10. However, on an adjusted basis, the company demonstrated resilience with improved profitability metrics.

The company’s operating margin performance reveals the underlying drivers of profitability:

Inventory levels increased 17% year-over-year to $417 million, driven by planned inventory builds and higher costs related to foreign exchange and tariffs. The company noted it restarted production and shipments from China to the U.S. in May, while maintaining aged inventory at historically low levels.

Cash flow declined year-over-year, with operating cash flow at $209 million for the first half of 2025 compared to $365 million in the same period of 2024. This reduction was primarily driven by tax payment timing and increased use of working capital. Despite this decline, Hasbro returned $196 million to shareholders via dividends and reduced debt by $62 million year-to-date.

Strategic Initiatives

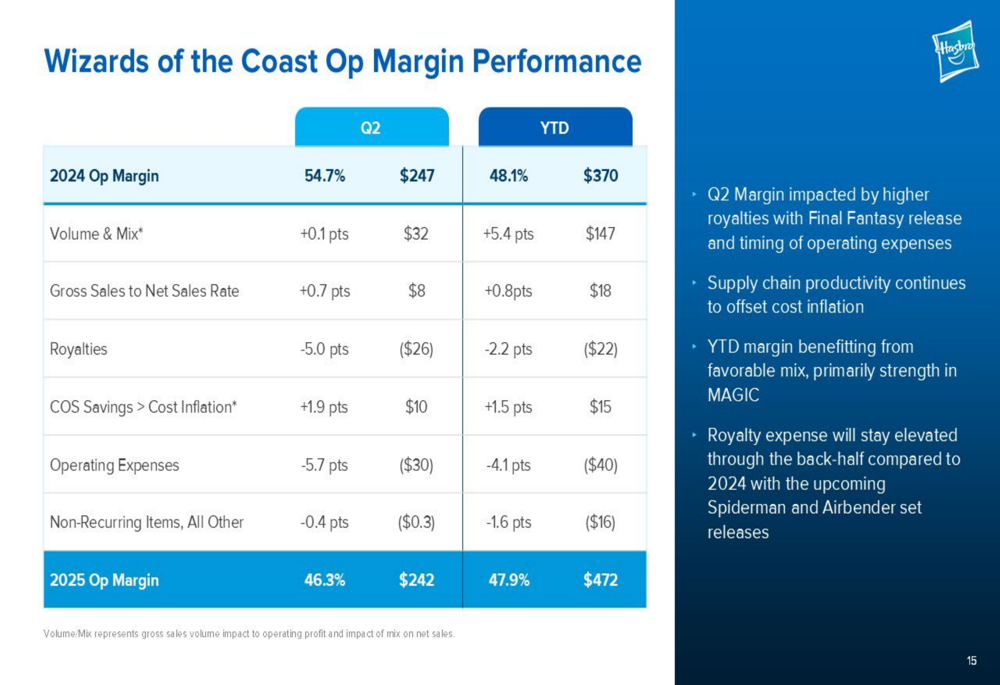

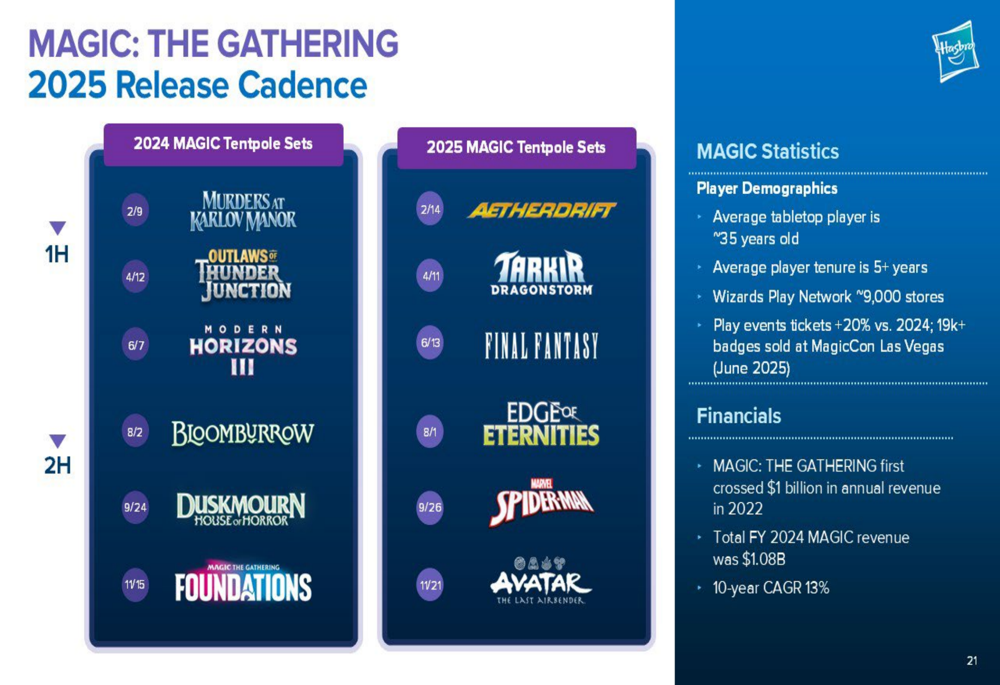

Wizards of the Coast continues to be Hasbro’s growth engine, with its tabletop business growing 21% in Q2 and 28% year-to-date. Magic: The Gathering, which first crossed $1 billion in annual revenue in 2022, remains the primary driver with a 10-year compound annual growth rate of 13%.

The following slide details the operating margin performance for the Wizards segment:

The company’s Operational Excellence Program delivered $98 million of gross savings year-to-date, primarily through supply chain cost productivity and reduction of managed expenses in Consumer Products. Hasbro remains on track to achieve its target of $1 billion in cumulative gross cost savings by 2027.

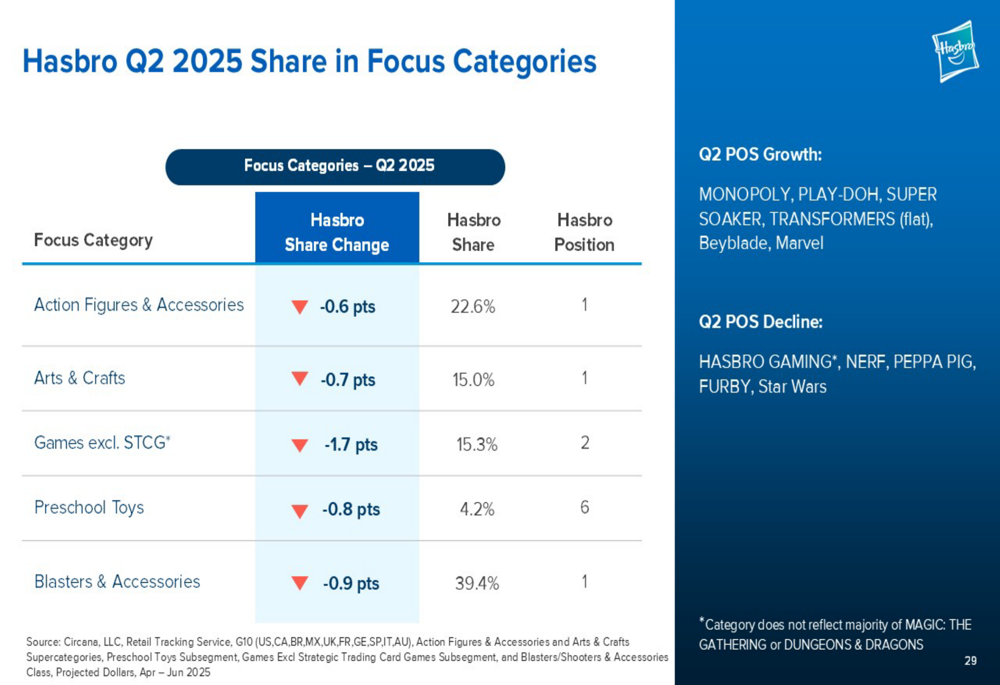

In the Consumer Products segment, despite revenue declines, Hasbro maintained its market leadership positions in several key categories. The company holds the #1 position in Action (WA:ACT) Figures & Accessories with a 22.6% market share, Arts & Crafts with 15.0%, and Blasters & Accessories with 39.4%. However, market share declined slightly across all focus categories compared to the previous year.

Forward-Looking Statements

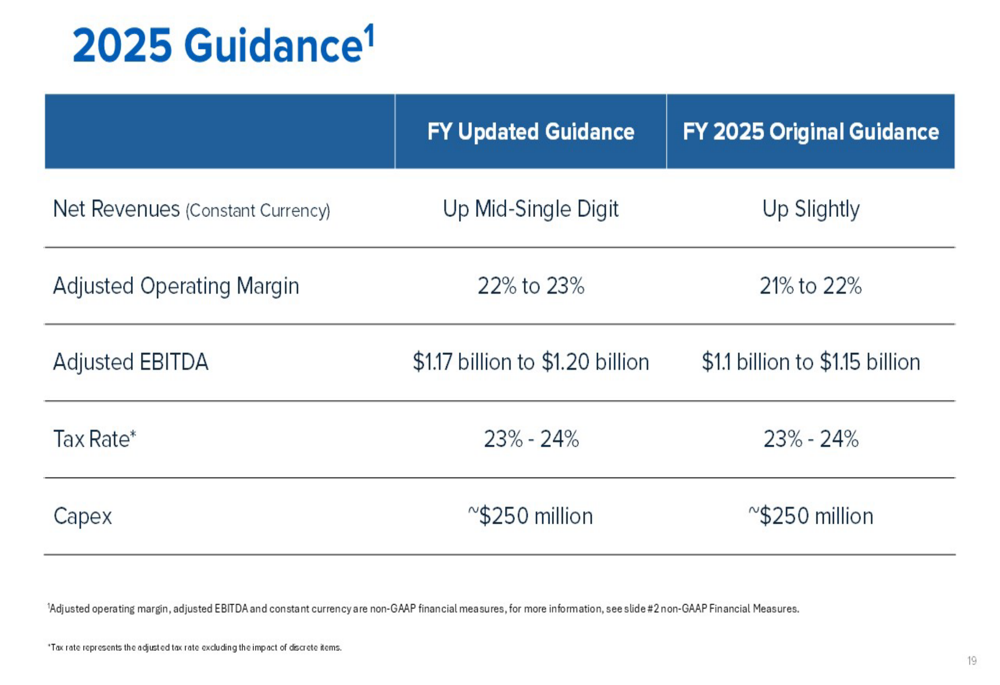

Based on the strong performance of its Wizards segment, Hasbro raised its full-year 2025 guidance. The company now expects revenue growth in the mid-single digits on a constant currency basis, up from its original guidance of "up slightly." Adjusted operating margin is now projected at 22-23%, an improvement from the original 21-22% range, and adjusted EBITDA is expected to reach $1.17-1.20 billion, up from the original $1.1-1.15 billion target.

The updated guidance is presented in the following slide:

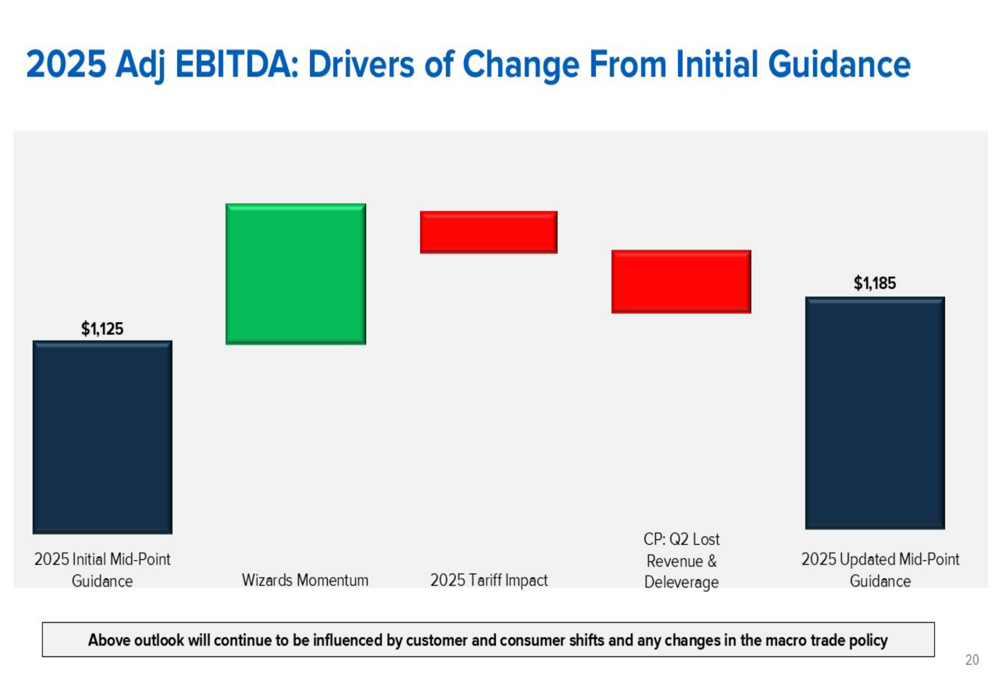

The primary drivers behind the improved EBITDA outlook include momentum in the Wizards segment, partially offset by tariff impacts and lost revenue in the Consumer Products segment:

For the medium term (2025-2027), Hasbro maintained its guidance for mid-single-digit revenue growth CAGR on a constant currency basis, with average operating margin expansion of 50-100 basis points per year. The company also reiterated its target of achieving a 2.5x gross debt to adjusted EBITDA ratio by 2026.

Magic: The Gathering will remain a key focus area, with a strong release cadence planned for the remainder of 2025:

Overall, despite mixed quarterly results and significant goodwill impairment, Hasbro’s presentation revealed underlying strength in its high-margin Wizards segment and progress on cost-saving initiatives, leading to improved full-year guidance and positive market reaction.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.