Futures lower; Tesla’s much-anticipated announcement - what’s moving markets

Hannon Armstrong Sustainable Infrastructure Capital Inc (NYSE:HASI) released its second quarter 2025 earnings presentation on August 7, showcasing 13% year-over-year growth in managed assets while reporting a slight decline in adjusted earnings per share compared to the same period last year.

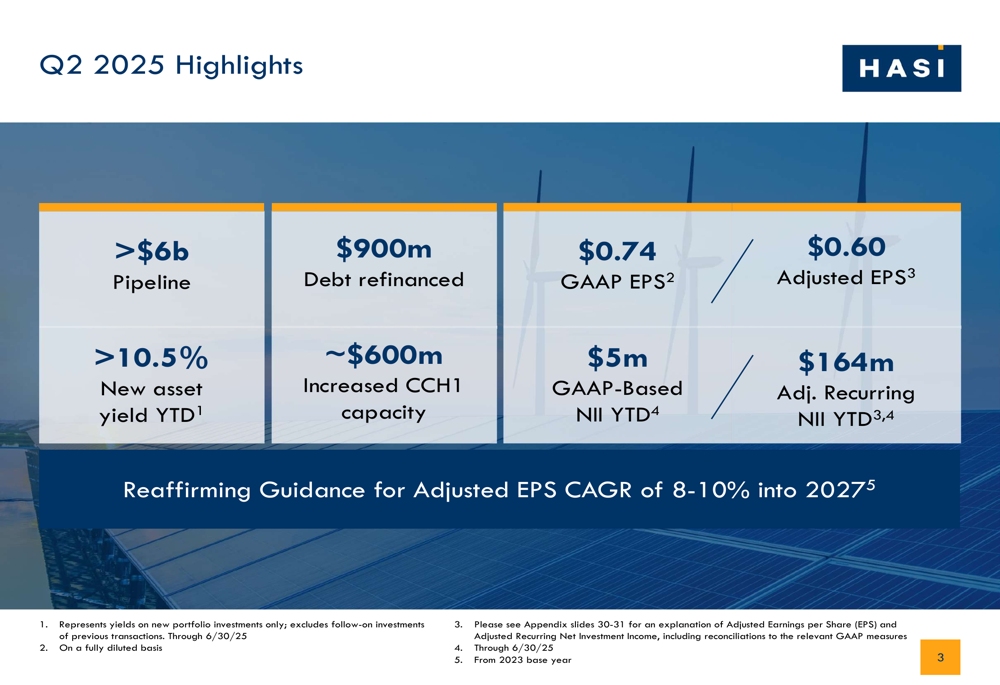

Quarterly Performance Highlights

HASI reported Q2 2025 GAAP EPS of $0.74 and adjusted EPS of $0.60, compared to $0.63 in Q2 2024. The company’s adjusted recurring net investment income reached $164 million year-to-date, representing a 19% year-over-year increase in the first half of 2025. The company successfully refinanced $900 million in near-term debt maturities during the quarter.

As shown in the following summary of key Q2 metrics:

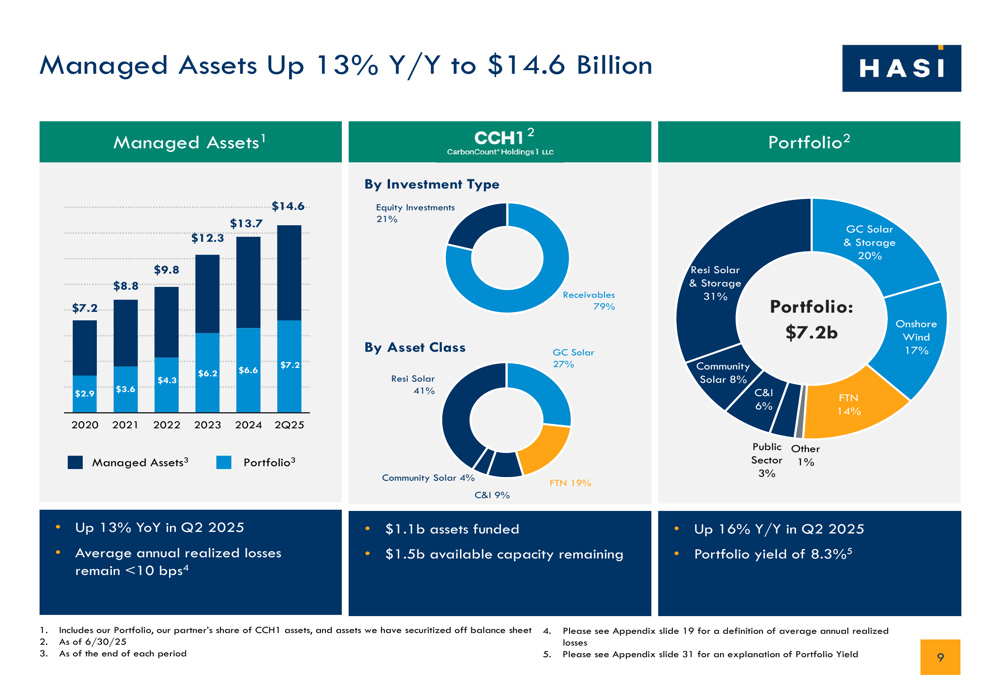

The company’s managed assets grew to $14.6 billion, up 13% year-over-year, with a portfolio yield of 8.3%. This growth reflects HASI’s continued expansion in climate-focused investments despite a challenging interest rate environment.

The following chart illustrates the steady growth in managed assets and their composition:

Strategic Positioning & Pipeline Growth

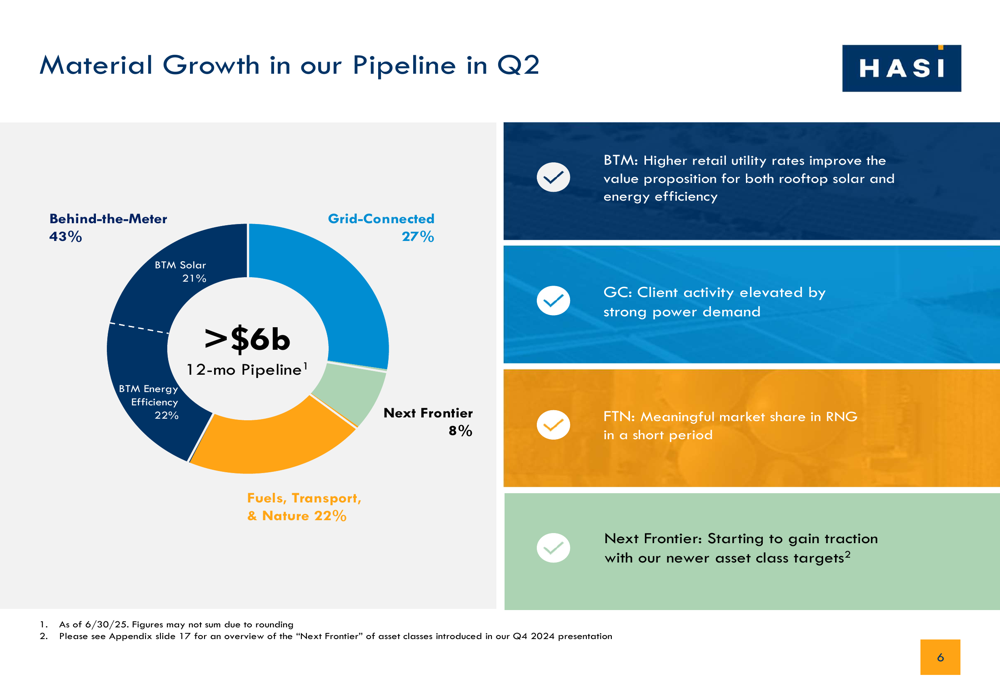

HASI reported significant growth in its pipeline, which expanded by over $500 million quarter-over-quarter to exceed $6 billion. The pipeline is diversified across multiple sectors, with Behind-the-Meter representing 43%, Grid-Connected 27%, Fuels, Transport, & Nature 22%, and Next (LON:NXT) Frontier initiatives accounting for 8%.

The company’s pipeline breakdown by sector is visualized here:

HASI continues to benefit from strong market tailwinds, including elevated U.S. power demand, higher power prices improving renewable economics, and the increasing economic viability of renewables even without incentives. The company’s strategic positioning in the project lifecycle—entering after construction begins—helps minimize risk while maintaining attractive returns.

Financial Performance Analysis

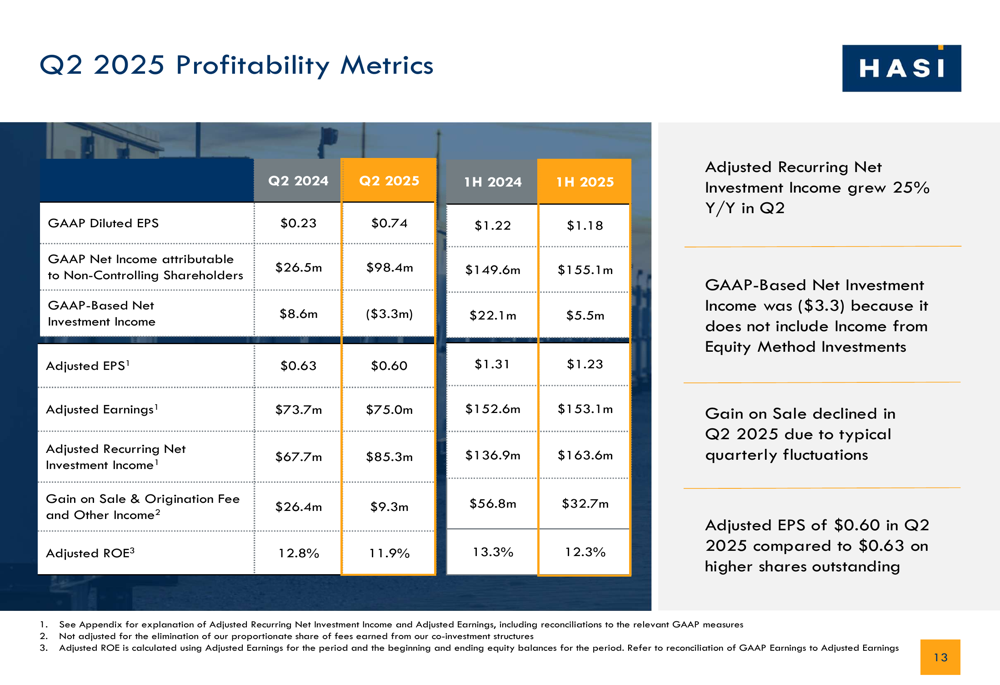

The company’s Q2 2025 profitability metrics showed mixed results compared to the prior year. While adjusted recurring net investment income grew 25% year-over-year in Q2, gain on sale declined due to typical quarterly fluctuations. Adjusted ROE was 11.9% for Q2 2025, down from 12.8% in Q2 2024.

The detailed profitability metrics are presented in the following table:

HASI has maintained strong margins despite the higher interest rate environment. The company’s portfolio yield increased to 12.3% in the first half of 2025, up from 10.5% in 2018, helping to offset the impact of higher interest expenses. However, adjusted ROE has declined from 11.1% in 2018 to 6.8% in the first half of 2025, partly due to a lower pace of gain on sale resulting from the company’s targeted asset rotation strategy in 2024.

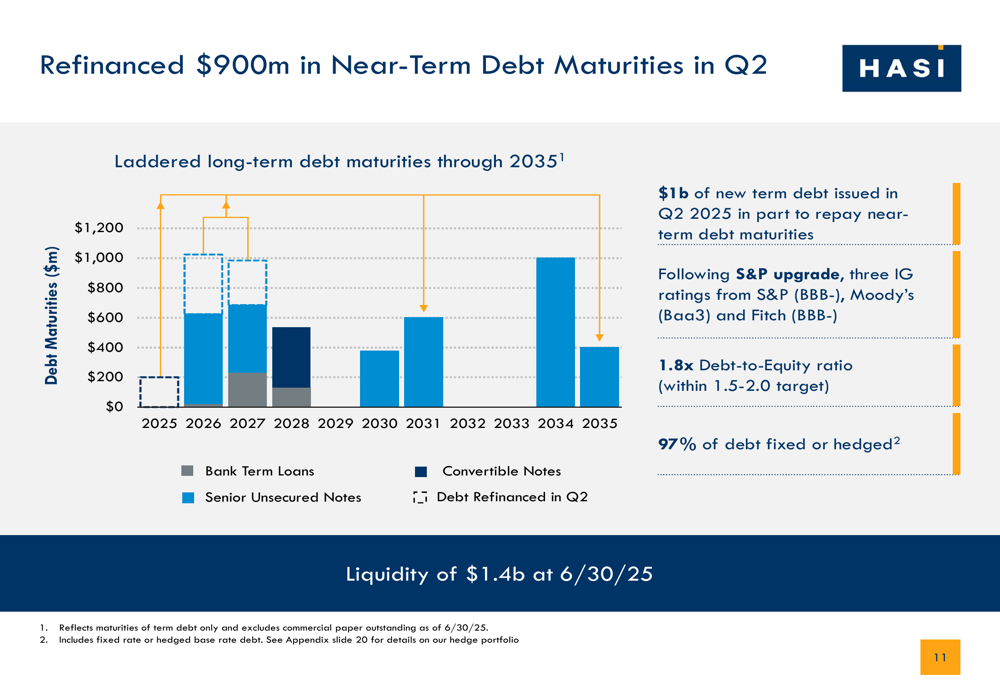

Capital Management & Debt Refinancing

A significant achievement in Q2 was the refinancing of $900 million in near-term debt maturities. HASI issued $1 billion of new term debt following an S&P upgrade, with the company now holding investment grade ratings from all three major rating agencies (S&P, Moody’s, and Fitch). The company maintains a 1.8x debt-to-equity ratio, within its target range of 1.5-2.0x, with 97% of debt fixed or hedged.

The following chart shows the company’s debt maturity schedule after the Q2 refinancing:

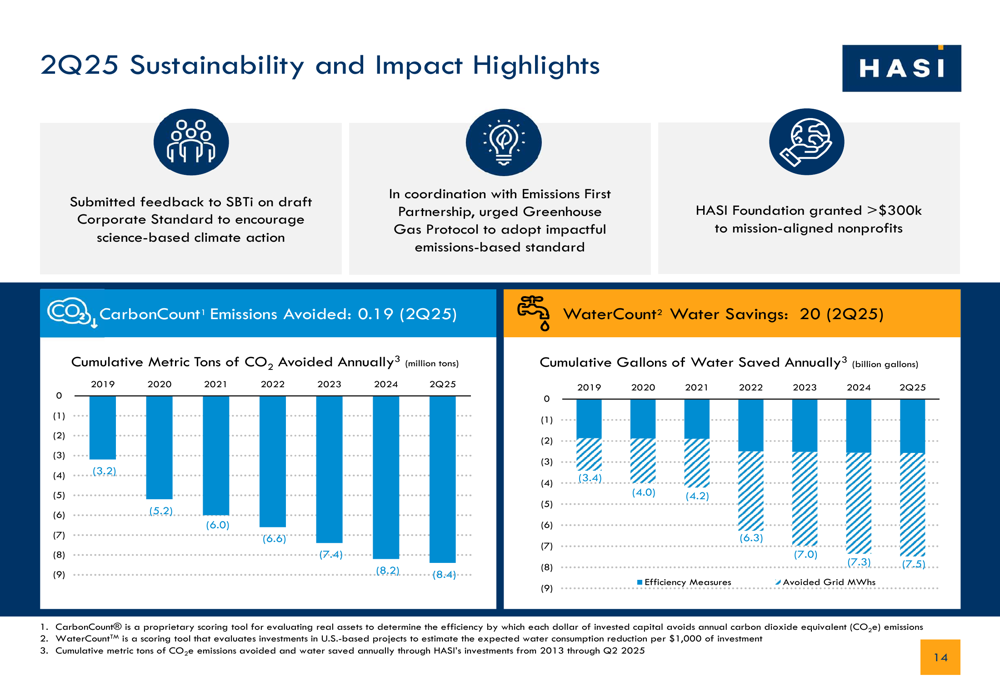

Sustainability Impact

As a climate-focused investment firm, HASI continues to track and report the environmental impact of its investments. In Q2 2025, the company’s investments helped avoid 8.4 million metric tons of CO2 annually, up from 8.2 million in 2024. Additionally, HASI’s investments contributed to saving 7.5 billion gallons of water annually.

The company’s sustainability metrics are highlighted in this chart:

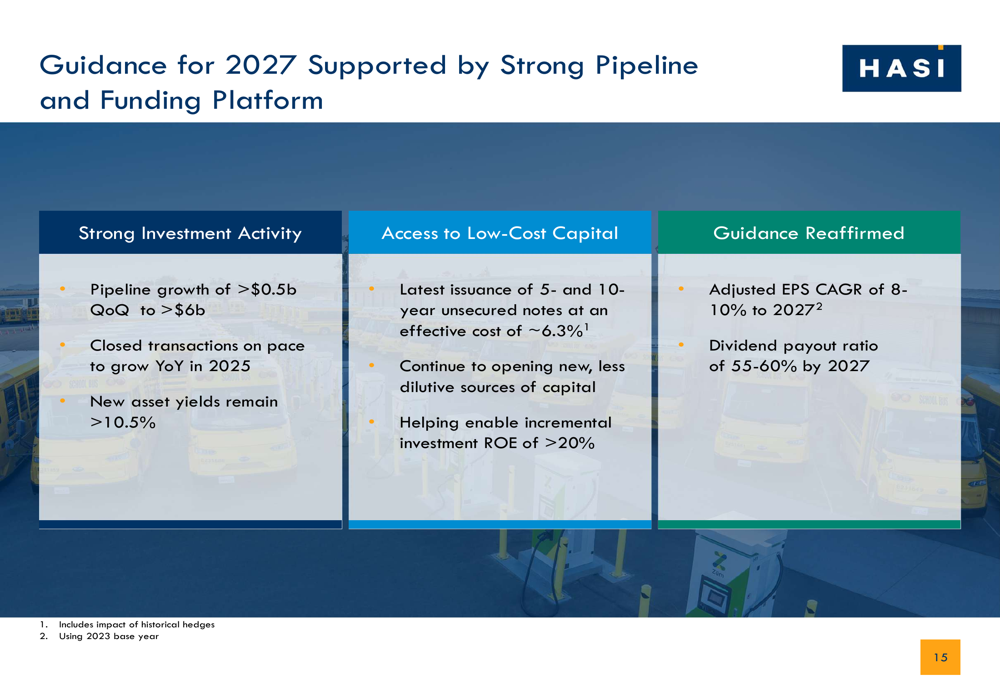

Forward Outlook & Guidance

HASI reaffirmed its guidance for 8-10% compound annual growth in adjusted EPS through 2027, supported by its strong pipeline and funding platform. The company expects to maintain new asset yields above 10.5% and is targeting a dividend payout ratio of 55-60% by 2027.

The guidance is summarized in the following slide:

Looking ahead, HASI’s management remains confident in the company’s ability to capitalize on the growing demand for climate solutions. The company’s strategy of focusing on higher-yielding assets, optimizing its capital structure, and expanding into new asset classes positions it well for long-term growth despite near-term challenges.

After the earnings presentation, HASI’s stock closed at $24.38, down 0.25% for the day. The stock has traded between $21.98 and $36.56 over the past 52 weeks, suggesting potential upside opportunity based on the company’s reaffirmed growth guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.