US stock futures inch lower after Wall St marks fresh records on tech gains

Introduction & Market Context

Herc Holdings Inc. (NYSE:HRI) presented its second quarter 2025 results on July 29, revealing significant revenue growth driven by the recently completed H&E Equipment Services (NASDAQ:HEES) acquisition, though profitability was impacted by integration costs. The equipment rental company reported total revenues of $1,002 million, an 18.2% increase year-over-year, while posting a net loss of $35 million for the quarter.

The presentation comes after a challenging first quarter that saw the company miss earnings expectations, with the stock having declined over 40% year-to-date as of the Q1 report. Currently trading at $149.88, Herc’s share price has shown some recovery but remains well below its 52-week high of $246.88.

As shown in the following slide, the company’s executive team led by President and CEO Larry Silber outlined their strategy focused on "Scaling for Sustainable Growth" amid market challenges:

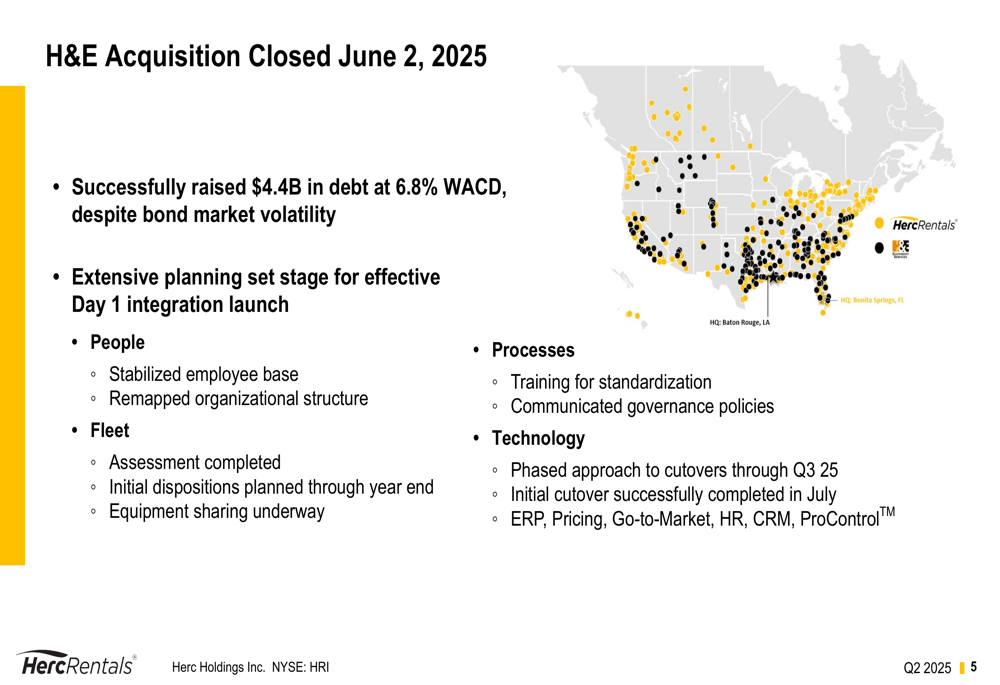

H&E Acquisition Integration Progress

A central focus of the presentation was the H&E Equipment Services acquisition, which closed on June 2, 2025. The company raised $4.4 billion in debt at a weighted average cost of debt (WACD) of 6.8% to finance the transaction, despite what it described as bond market volatility.

The integration process is progressing across multiple fronts, including stabilizing the employee base, completing fleet assessment, standardizing processes, and implementing technology systems. The acquisition significantly expands Herc’s geographic footprint, though early results show some challenges with H&E legacy branches reporting a 14.1% year-over-year decline.

The company’s acquisition strategy and integration progress is illustrated in this detailed slide:

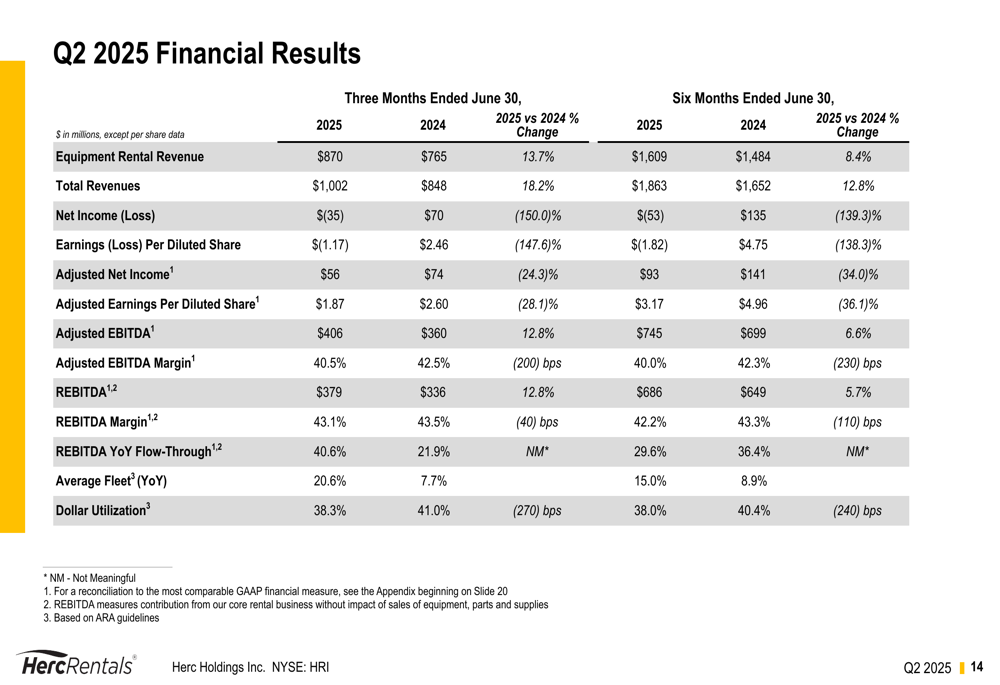

Quarterly Performance Highlights

Herc reported equipment rental revenue of $870 million for Q2 2025, representing a 13.7% increase compared to the same period last year. Total (EPA:TTEF) revenues reached $1,002 million, up 18.2% year-over-year. However, the company posted a net loss of $35 million for the quarter, contrasting with the positive net income reported in Q2 2024.

Adjusted EBITDA grew 12.8% to $406 million, with an adjusted EBITDA margin of 40.5%. The company’s rental equipment adjusted EBITDA (REBITDA) also increased 12.8% to $379 million, with a REBITDA margin of 43.1%.

The comprehensive financial results are presented in the following slide:

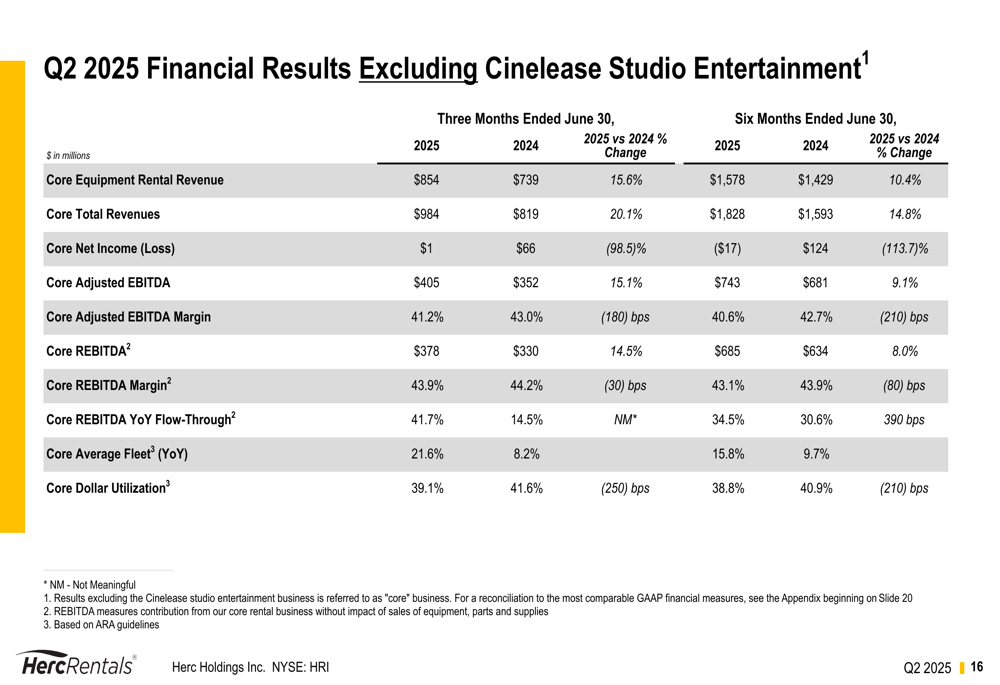

When excluding the Cinelease Studio Entertainment segment, which has been experiencing softness in the entertainment industry, Herc’s core business showed stronger performance. Core equipment rental revenue increased 15.6% to $854 million, and core total revenues grew 20.1% to $984 million. Core adjusted EBITDA rose 15.1% to $405 million.

The following slide details the performance of the core business excluding Cinelease:

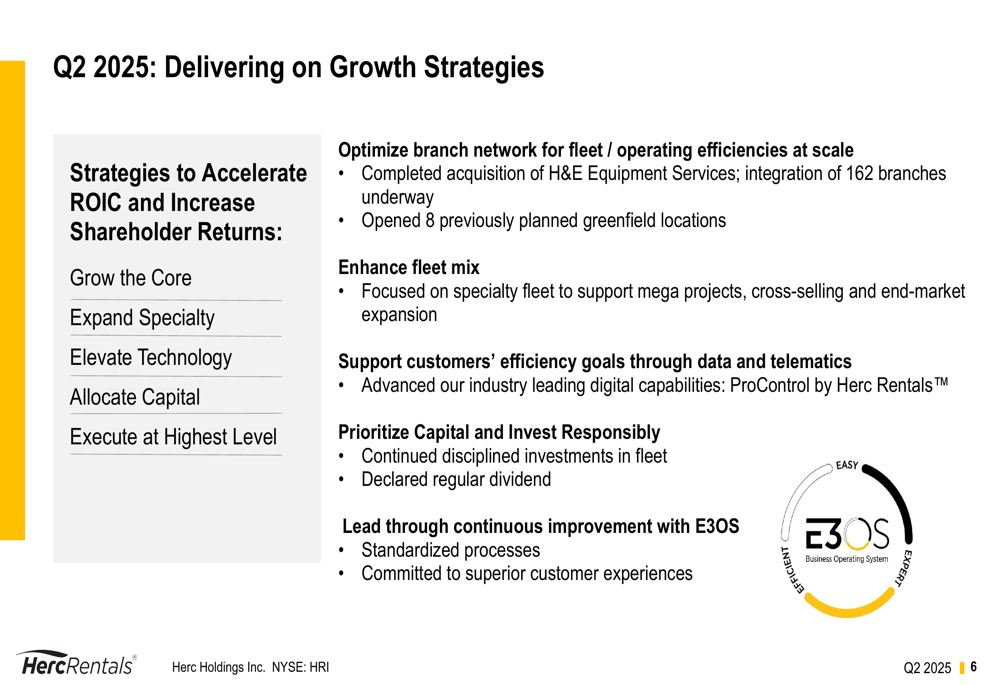

Strategic Initiatives

Herc outlined its growth strategies focused on five key pillars: growing the core business, expanding specialty offerings, elevating technology, allocating capital effectively, and executing at the highest level. The company opened eight greenfield locations in addition to the H&E acquisition, demonstrating its commitment to network expansion.

The company’s strategic focus areas are illustrated in this slide:

Safety remains a priority for Herc, with over 96% of days across all branches qualifying as "Perfect Days" with no OSHA reportable incidents, at-fault moving vehicle accidents, or DOT violations. The company’s Total Recordable Incident Rate of 0.92 is better than the industry standard of 1.0.

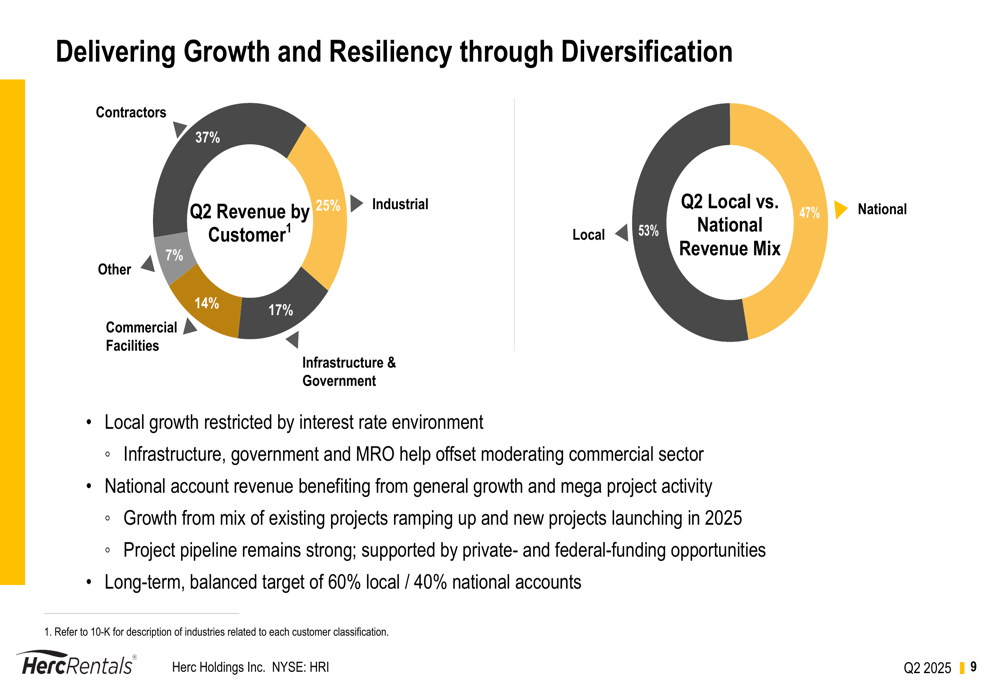

Market Diversification and Opportunities

Herc emphasized its diversified customer base as a key strength, with revenue coming from contractors (37%), industrial clients (25%), infrastructure and government (17%), commercial facilities (14%), and other sectors (7%). The company maintains a balanced approach between local (53%) and national (47%) revenue streams, with a long-term target of 60% local and 40% national.

The following slide illustrates this diversification strategy:

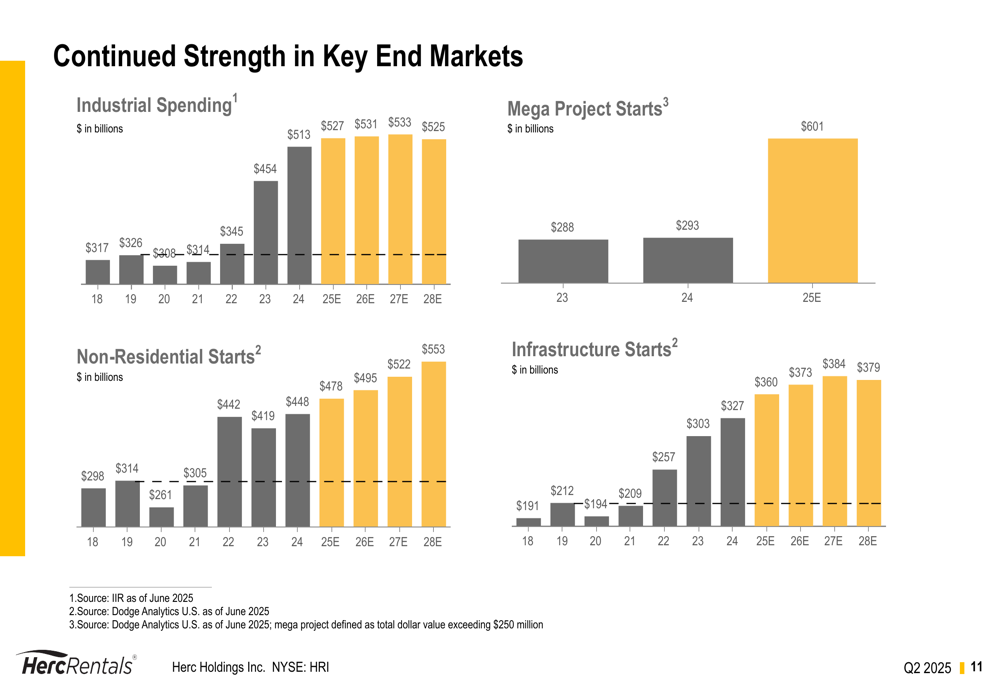

The company highlighted continued strength in key end markets, with industrial spending, non-residential starts, mega project starts, and infrastructure starts all projected to grow through 2028. Specific growth opportunities were identified in chip plants, data centers, renewables, EV/battery manufacturing, utilities, healthcare, infrastructure, and LNG plants.

As shown in the following market trend analysis:

The company’s diverse customer base and targeted growth opportunities are further detailed in this comprehensive overview:

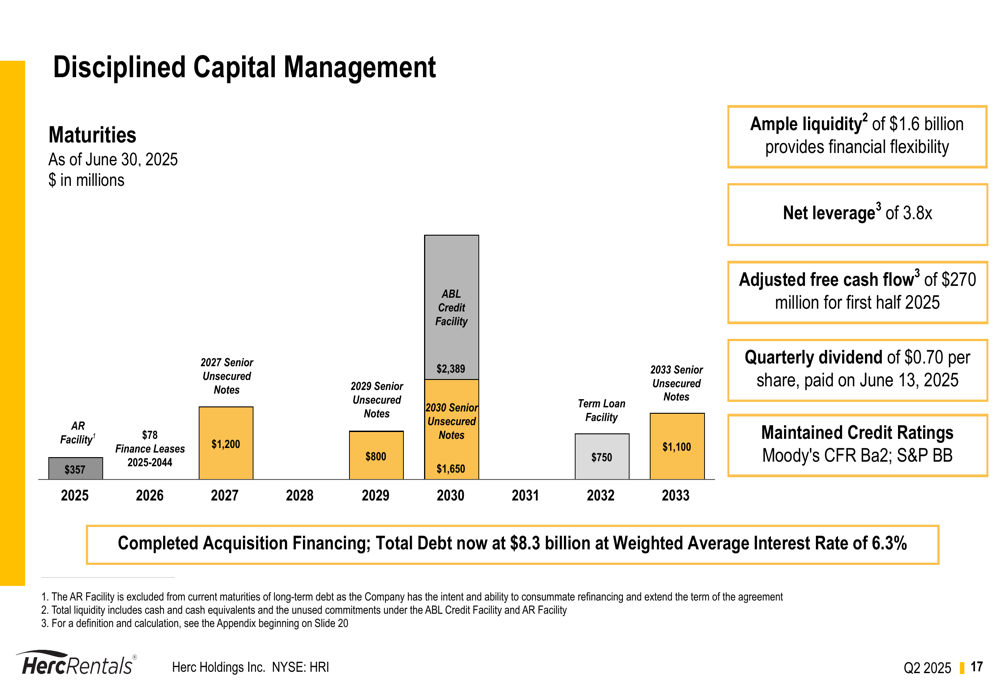

Financial Position and Capital Management

Following the H&E acquisition, Herc reported a net leverage ratio of 3.8x, with ample liquidity of $1.6 billion. The company generated adjusted free cash flow of $270 million for the first half of 2025 and paid a quarterly dividend of $0.70 per share on June 13, 2025.

The debt maturity profile shows a well-structured approach with maturities spread from 2027 to 2033, as illustrated in the following slide:

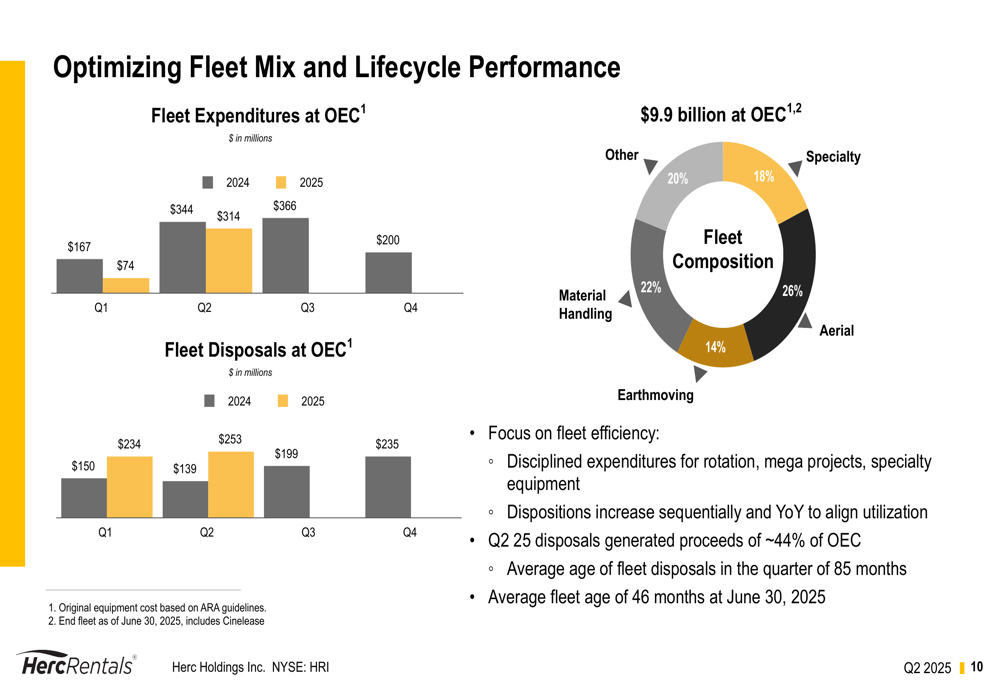

Fleet Management Strategy

Herc’s total fleet stands at $9.9 billion at original equipment cost (OEC), with a composition of aerial (26%), material handling (22%), other (20%), specialty (18%), and earthmoving (14%) equipment. The company is focusing on fleet efficiency, with disciplined expenditures and increasing disposals to align utilization.

The company’s fleet expenditures, disposals, and composition are detailed in this slide:

Forward-Looking Statements

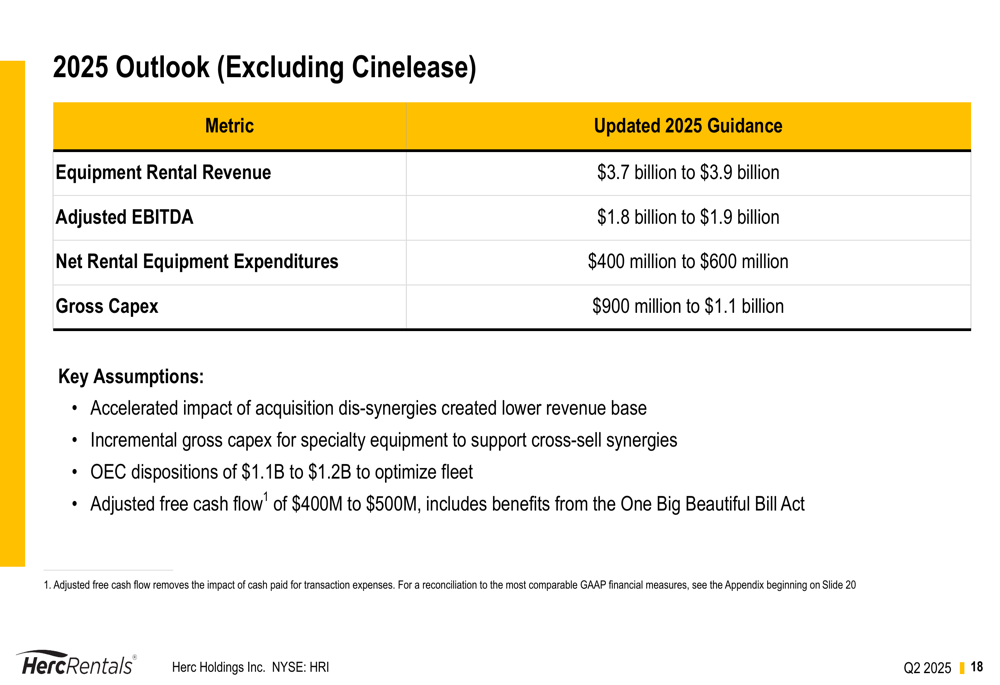

Despite the challenges associated with the H&E acquisition integration, Herc maintained its 2025 outlook (excluding Cinelease). The company expects equipment rental revenue of $3.7 billion to $3.9 billion and adjusted EBITDA of $1.8 billion to $1.9 billion. Net rental equipment expenditures are projected to be $400 million to $600 million, with gross capital expenditures of $900 million to $1.1 billion.

Key assumptions for the outlook include accelerated impact of acquisition dis-synergies creating a lower revenue base, incremental gross capital expenditures for specialty equipment, OEC dispositions of $1.1 billion to $1.2 billion, and adjusted free cash flow of $400 million to $500 million.

The company’s detailed 2025 outlook is presented in the following slide:

Conclusion

Herc Holdings’ Q2 2025 results reflect both the opportunities and challenges associated with its significant acquisition of H&E Equipment Services. While the company has achieved substantial revenue growth, the integration process has impacted profitability in the short term. Management remains confident in the long-term benefits of the acquisition and the company’s ability to capitalize on growth trends across its diverse customer and project base.

With a maintained outlook for 2025 and strategic focus on fleet optimization, market diversification, and operational excellence, Herc is positioning itself to navigate current challenges while building a foundation for sustainable growth. Investors will be watching closely to see how quickly the company can overcome integration hurdles and return to profitability in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.