Hulk Hogan, wrestling icon, dies at 71 in Florida home

Introduction & Market Context

Heron Therapeutics (NASDAQ:HRTX) presented its Q1 2025 earnings results on May 6, 2025, revealing a significant milestone as the company achieved profitability for the quarter. The biopharmaceutical company, which specializes in oncology care and acute pain management products, reported earnings that surpassed analyst expectations, driving a notable premarket stock surge of 12.67% to $2.40 following a 7.79% decline in the previous session.

The company’s performance comes amid increasing demand for post-operative pain management solutions and oncology supportive care products, with Heron’s strategic positioning in these markets beginning to yield financial returns after years of investment.

Quarterly Performance Highlights

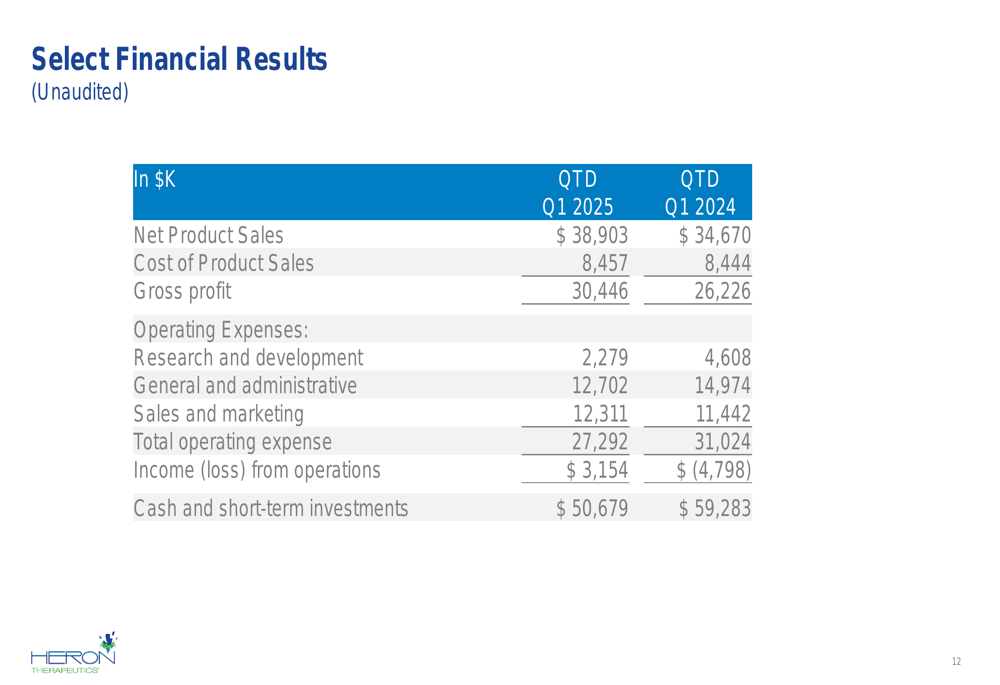

Heron Therapeutics reported Q1 2025 net revenue of $38.9 million, exceeding analyst expectations of $34.25 million. More significantly, the company achieved net income of $2.6 million, translating to earnings per share of $0.01, compared to the forecasted loss of $0.02. This marks a substantial turnaround from the $3.16 million net loss reported in Q1 2024.

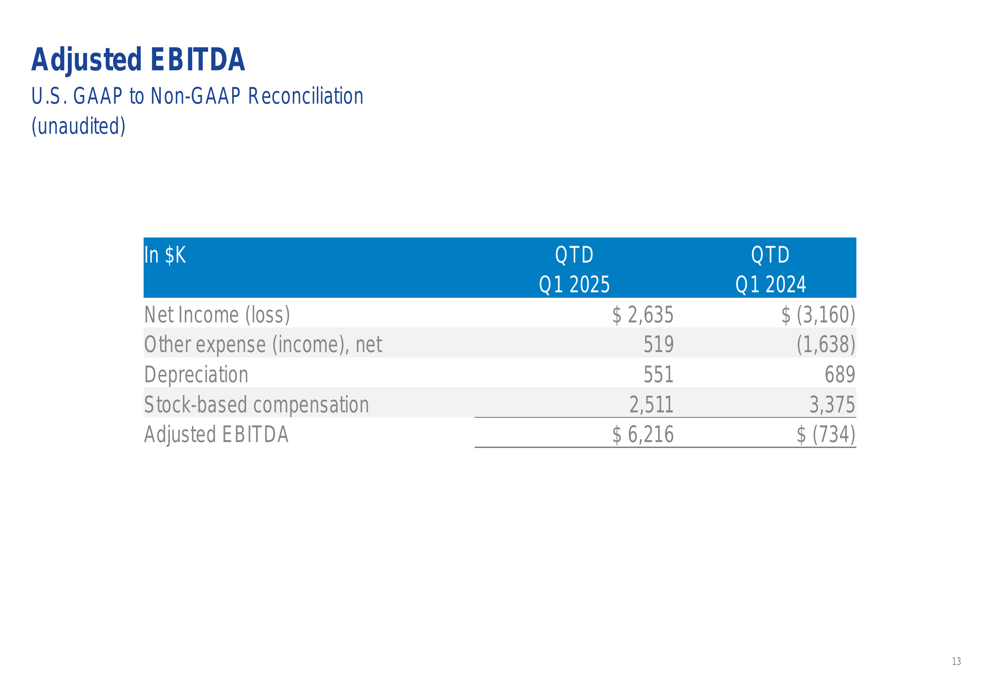

The company also delivered record quarterly adjusted EBITDA of $6.2 million, compared to a negative $734,000 in the same period last year, demonstrating significant operational improvement.

As shown in the following financial results comparison:

Beyond the financial performance, Heron announced a settlement with Mylan (NASDAQ:VTRS) Pharmaceuticals regarding CINVANTI and APONVIE patent litigations, securing market exclusivity until June 1, 2032. The company also strengthened its executive team with the appointment of Mark Hensley as Chief Operating Officer.

Product Portfolio Performance

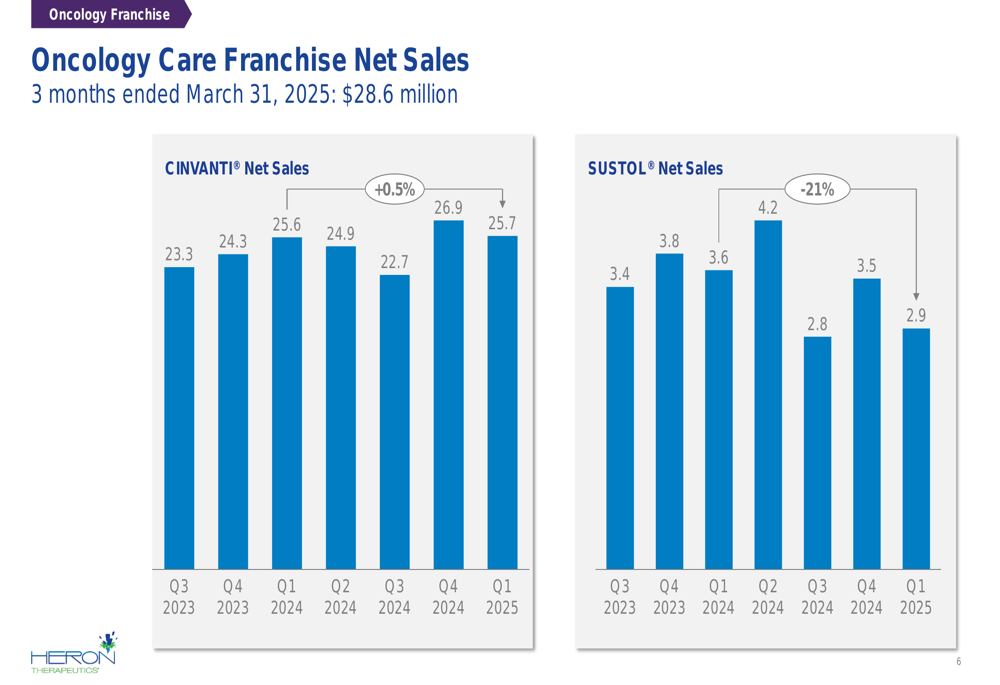

Heron’s product portfolio is divided into two main franchises: Oncology Care and Acute Care. The Oncology Care franchise, consisting of CINVANTI and SUSTOL, generated combined net sales of $28.6 million in Q1 2025.

CINVANTI, the company’s leading oncology product, maintained stable performance with sales of $25.7 million, a slight increase of 0.5% year-over-year. However, SUSTOL sales declined by 21% to $2.9 million compared to the same period last year.

The quarterly performance of the Oncology Care franchise is illustrated in the following chart:

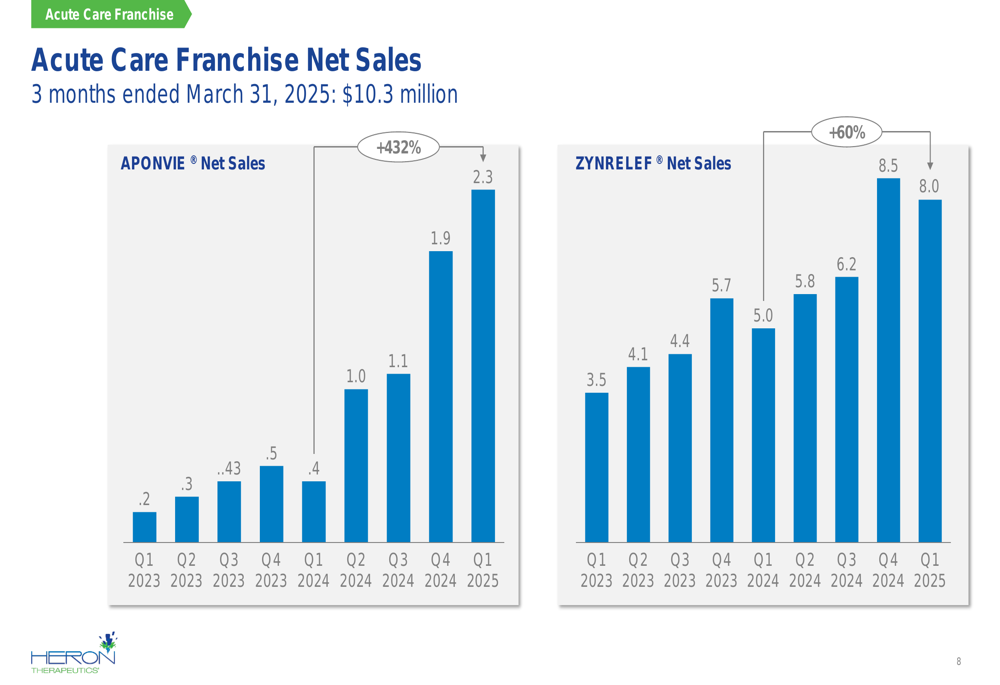

The Acute Care franchise, comprising APONVIE and ZYNRELEF, showed remarkable growth with combined net sales of $10.3 million in Q1 2025. APONVIE, used for postoperative nausea and vomiting, demonstrated exceptional growth with sales of $2.3 million, a 432% increase year-over-year. ZYNRELEF, a non-opioid analgesic for post-surgical pain, also performed strongly with sales of $8.0 million, up 60% from Q1 2024.

The quarterly performance of the Acute Care franchise is illustrated in the following chart:

APONVIE’s growth is supported by its recognition as the "#1 ranked most efficacious anti-emetic" and its inclusion in Enhanced Recovery After Surgery (ERAS) protocols, particularly as healthcare facilities shift toward more outpatient procedures. The company has seen steady increases in both average daily units and ordering accounts for this product.

Similarly, ZYNRELEF has benefited from an expanded label increasing the number of indicated procedures, improved delivery efficiency with the Vial Access Needle, and the strategic partnership with CrossLink for awareness and operating room education.

Detailed Financial Analysis

Heron’s financial performance shows significant improvement across multiple metrics. Gross profit increased to $30.4 million in Q1 2025 from $26.2 million in Q1 2024, while operating expenses decreased to $27.3 million from $31.0 million in the same period last year.

The company achieved income from operations of $3.2 million, compared to a loss of $4.8 million in Q1 2024. This operational improvement was driven by both revenue growth and cost control measures, particularly in research and development expenses, which decreased by 50.5% to $2.3 million, and general and administrative expenses, which fell by 15.2% to $12.7 million.

The company’s adjusted EBITDA reconciliation highlights the path to profitability:

Heron’s cash position stood at $50.7 million at the end of Q1 2025, compared to $59.3 million in Q1 2024. While this represents a decline, the achievement of positive adjusted EBITDA suggests improved cash flow dynamics moving forward.

Forward-Looking Statements & Guidance

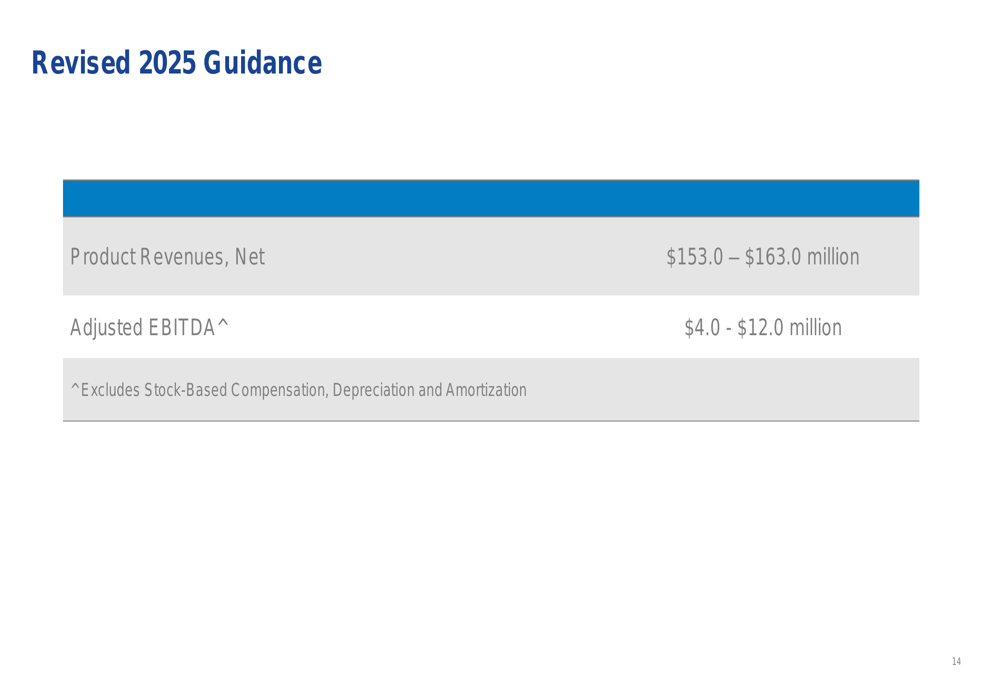

Based on Q1 performance, Heron Therapeutics has provided revised guidance for 2025, projecting net product revenues between $153.0 million and $163.0 million, and adjusted EBITDA between $4.0 million and $12.0 million.

The company’s growth strategy focuses on expanding its Acute Care franchise, particularly APONVIE and ZYNRELEF, which have shown substantial year-over-year growth. For APONVIE, Heron is emphasizing its efficacy, safety profile, and critical role in PONV (postoperative nausea and vomiting) prophylaxis, especially as healthcare facilities shift toward outpatient procedures.

For ZYNRELEF, the company is leveraging its expanded label, the CrossLink partnership for increased awareness, and the introduction of the Vial Access Needle for improved efficiency. The product also benefits from increasing adoption of ERAS protocols and the shift toward outpatient procedures, where effective pain control is essential for reducing length of stay and improving patient satisfaction.

The recent patent settlement with Mylan provides long-term market exclusivity for CINVANTI and APONVIE until 2032, securing a stable revenue stream for these products. This, combined with the strong growth trajectory of ZYNRELEF and APONVIE, positions Heron Therapeutics for continued improvement in financial performance throughout 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.