Williams Wesley Hastie sells $328k in Cipher Mining shares

Introduction & Market Context

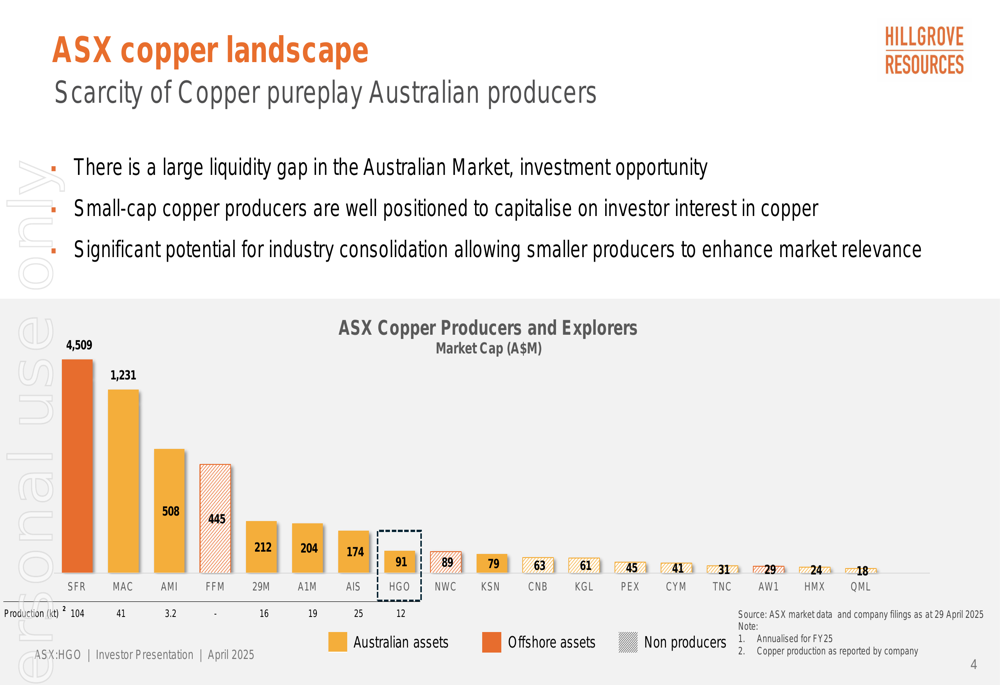

Hillgrove Resources Ltd (ASX:HGO) presented its Q1 2025 results on April 29, positioning itself as South Australia’s second largest copper producer in a market with limited pure-play Australian copper producers. The company highlighted its unique position in the ASX copper landscape, where a significant liquidity gap exists between major producers and smaller players.

As shown in the following chart comparing market capitalizations of ASX copper producers and explorers, Hillgrove sits in the mid-tier range with a market cap of approximately $94 million, presenting what the company describes as an investment opportunity in a consolidating sector:

With copper prices maintaining strength in global markets, Hillgrove’s presentation emphasized its debt-free status and strengthened balance sheet as competitive advantages. The company’s shares closed at $0.035 on May 5, 2025, representing a 2.94% increase on the day, though still well below its 52-week high of $0.089.

Quarterly Performance Highlights

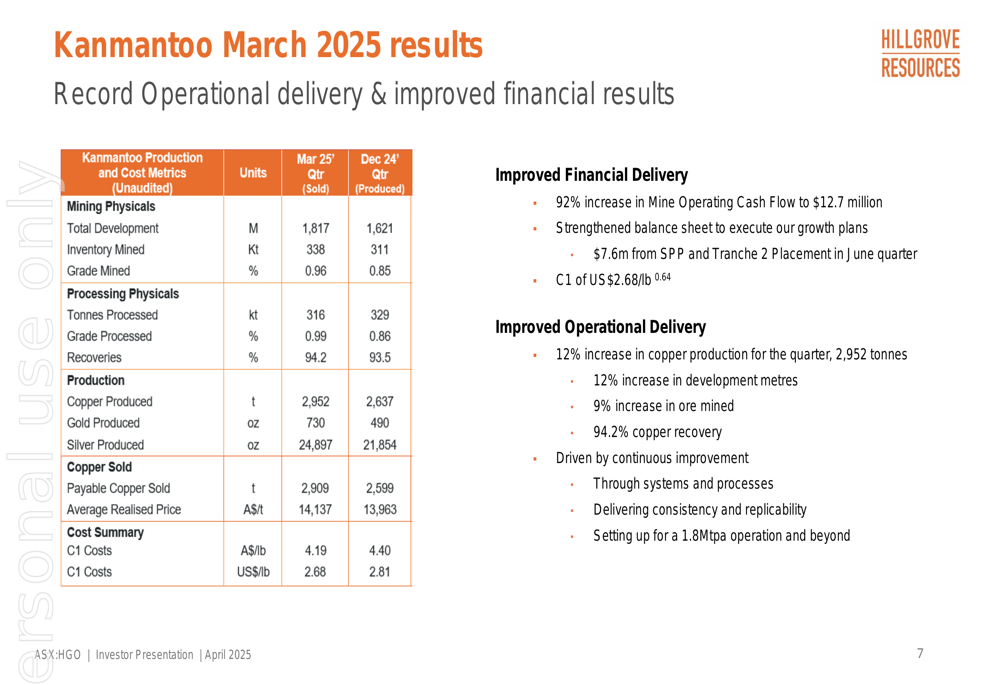

Hillgrove reported significant operational improvements in the March 2025 quarter, with record copper production driving substantial cash flow growth. The company produced 2,952 tonnes of copper, representing a 12% increase from the December 2024 quarter, while gold production rose by 49% to 730 ounces.

The detailed production metrics reveal improvements across multiple operational areas, including a 12% increase in development meters and a 9% increase in ore mined. Notably, the company achieved a copper recovery rate of 94.2%, up from 93.5% in the previous quarter:

These operational improvements translated directly to financial performance, with Mine Operating Cash Flow increasing by 92% to $12.7 million. The company also reported a 6% decrease in C1 costs to US$2.68/lb, down from US$2.81/lb in the previous quarter, reflecting enhanced operational efficiencies.

Strategic Initiatives & Growth Opportunities

Hillgrove’s presentation outlined a dual strategic focus: delivering consistent business performance while pursuing growth opportunities. The company’s stated ambition is "to be a mid-tier Australian, multi-asset copper producer unlocking value for a sustainable future."

The strategic roadmap details specific achievements for 2024, including reaching Commercial Production and establishing a Maiden Underground Ore Reserve, alongside priorities for 2025:

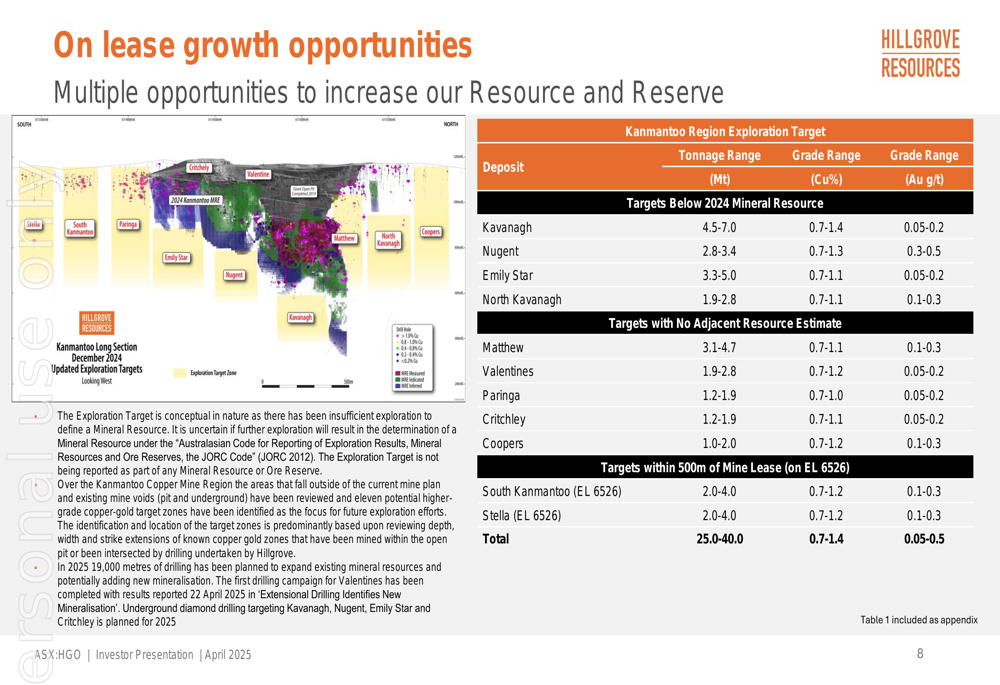

A key component of Hillgrove’s growth strategy involves expanding exploration at its Kanmantoo operations. The company has identified multiple opportunities to increase its resource and reserve base, with exploration targets totaling 25-40 million tonnes at grades between 0.7-1.4% copper:

The company specifically highlighted the Nugent extension as a priority growth area, with plans to accelerate its development to increase copper production and reduce unit costs in 2026.

Financial Position & Outlook

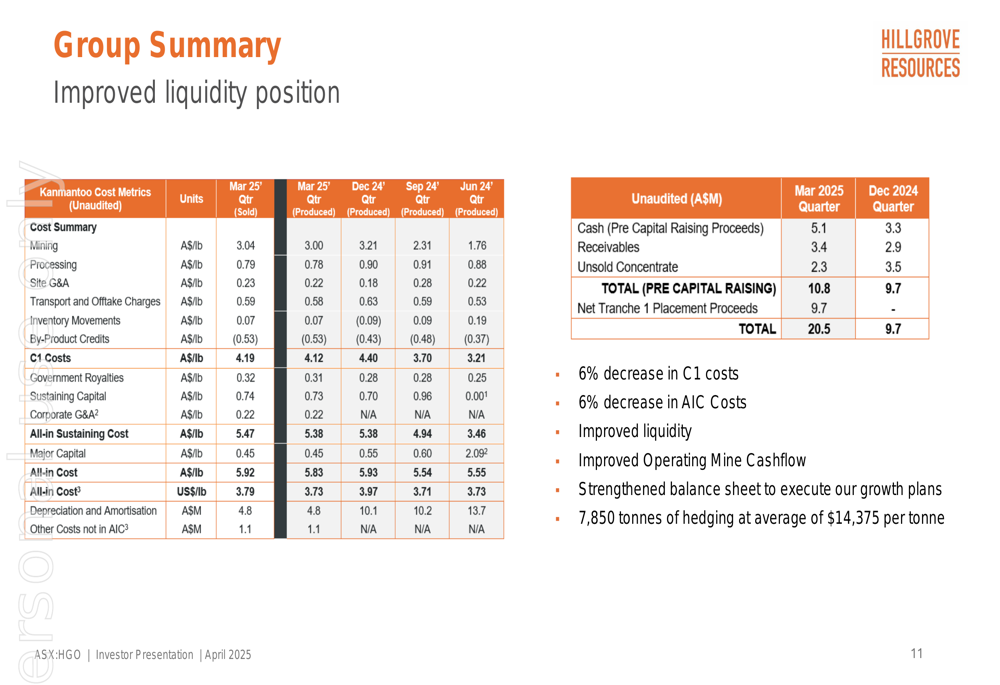

Hillgrove’s financial position strengthened considerably during the quarter, with its liquidity improving to $20.5 million by the end of March 2025, up from $9.7 million in December 2024. This improvement includes $9.7 million in net proceeds from a Tranche 1 Placement, with additional funds expected from an SPP and Tranche 2 Placement in the June quarter.

The detailed cost breakdown shows improvements in several areas, particularly mining costs, which decreased from A$3.21/lb to A$3.04/lb:

Looking ahead, Hillgrove has provided guidance that copper production in the June quarter is expected to exceed the March quarter results. The company has also implemented price risk management strategies, with 7,850 tonnes of copper hedged at an average price of $14,375 per tonne.

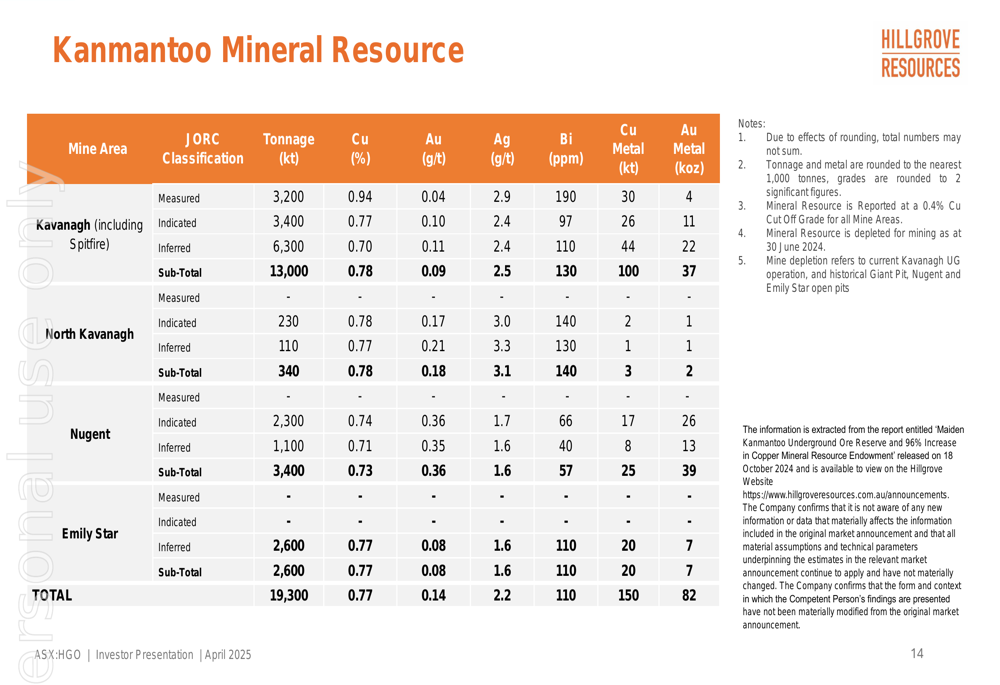

The company’s resource base provides a solid foundation for future operations, with a total Mineral Resource of 19.3 million tonnes at 0.77% copper and 0.14g/t gold, containing approximately 150,000 tonnes of copper:

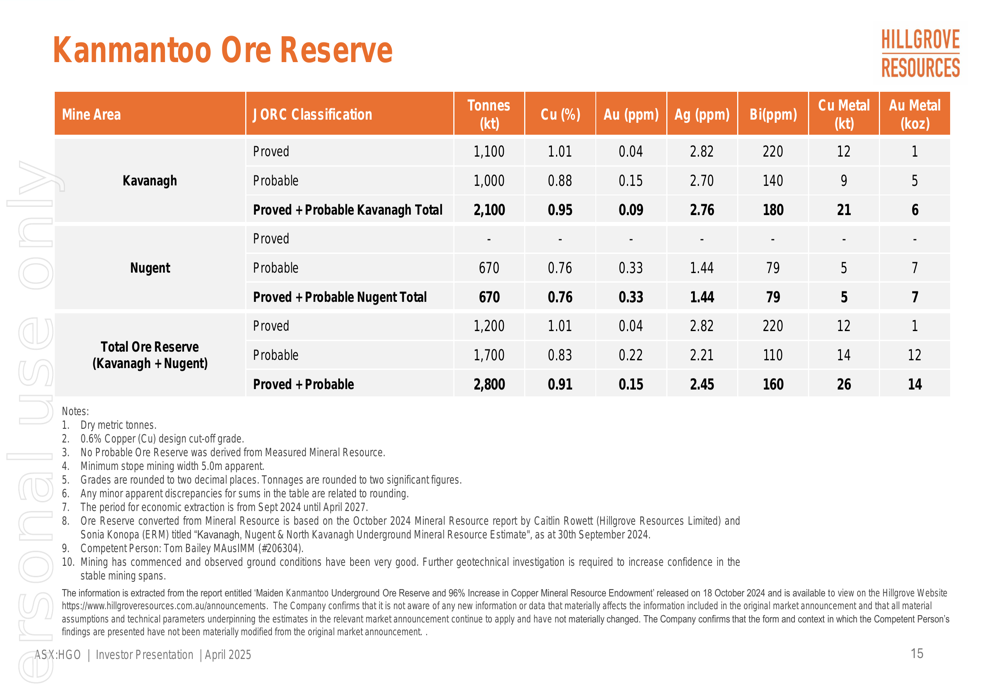

This is supported by a Maiden Underground Ore Reserve of 2.8 million tonnes at 0.91% copper, containing 26,000 tonnes of copper:

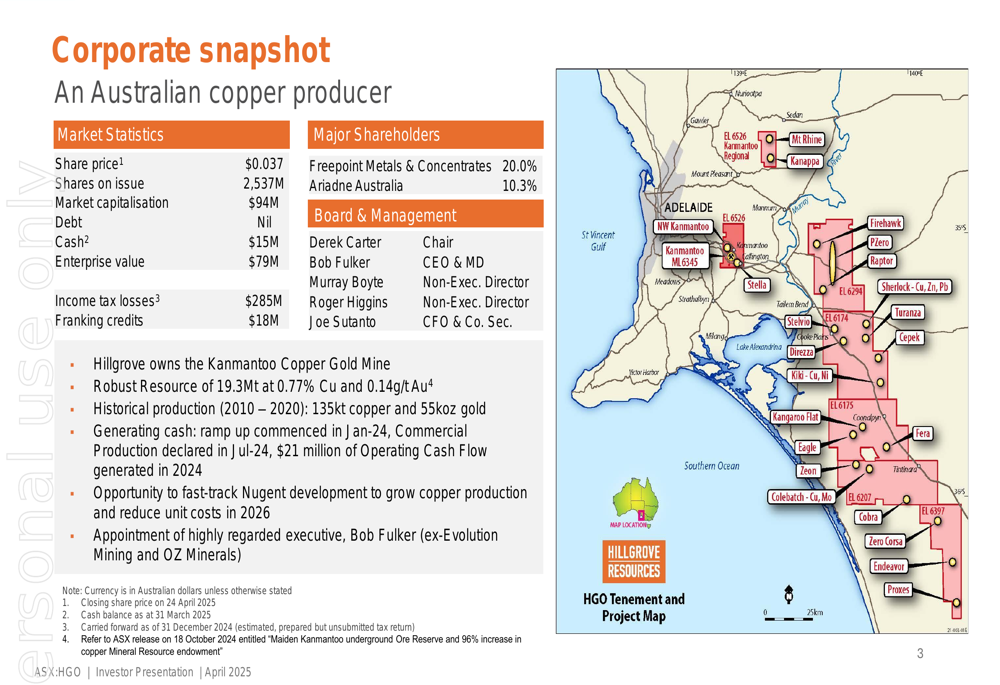

Hillgrove’s corporate snapshot reveals a debt-free balance sheet with $15 million in cash and significant potential tax advantages, including $285 million in income tax losses and $18 million in franking credits:

For the remainder of 2025, Hillgrove is focusing on maintaining production growth, cost control, and accelerating the Nugent development to expand its mining footprint. The company’s emphasis on both operational excellence and strategic growth positions it to potentially benefit from increasing global demand for copper, particularly as a pure-play Australian producer in a market with limited options for investors seeking exposure to this critical metal.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.