5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Hilltop Holdings Inc. (NYSE:HTH) presented its second quarter 2025 earnings results on July 25, 2025, showcasing significant year-over-year improvements across key financial metrics. The financial services holding company, which operates through its PlainsCapital Bank, PrimeLending, and HilltopSecurities subsidiaries, reported a 65% increase in net income compared to the same period last year. Following the earnings release, Hilltop’s stock price has shown positive momentum, trading at $32.25, reflecting a 3.29% increase.

The company’s performance comes amid a challenging environment for financial institutions, with anticipated interest rate cuts on the horizon that could potentially impact net interest margins in the coming quarters.

Quarterly Performance Highlights

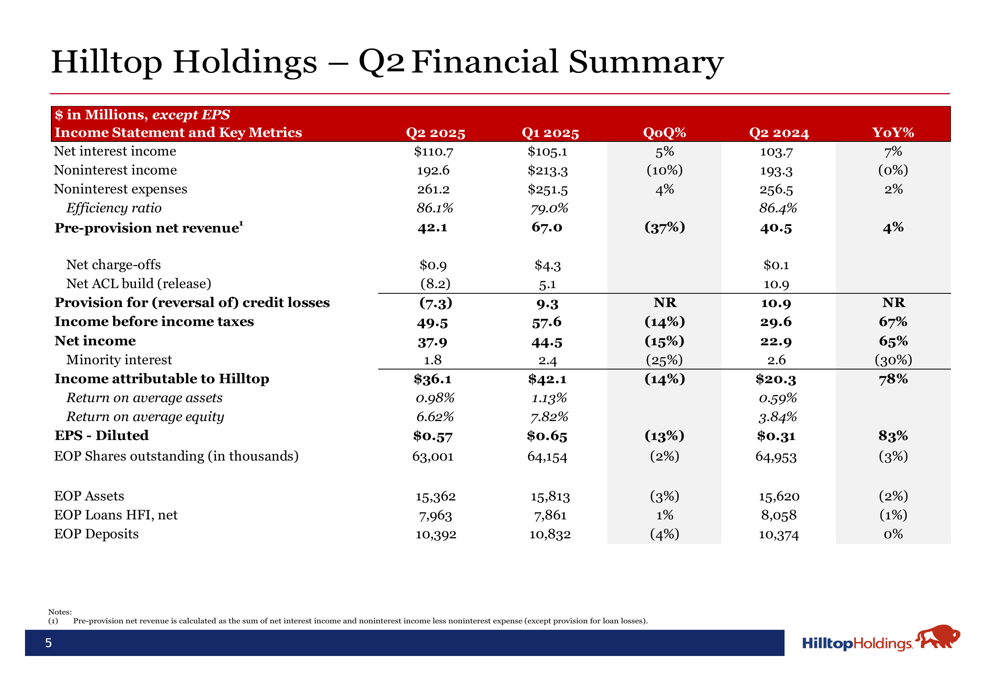

Hilltop Holdings reported net income of $37.9 million for Q2 2025, representing a substantial 65% increase year-over-year, though showing a 15% decrease from the previous quarter. Diluted earnings per share reached $0.57, marking an impressive 83% improvement compared to Q2 2024, but a 13% decline from Q1 2025.

As shown in the comprehensive financial summary below, the company delivered solid performance across key metrics:

Net interest income rose to $110.7 million, up 7% year-over-year and 5% quarter-over-quarter, driven by improved net interest margin which expanded to 3.01% from 2.90% in the prior year period. Noninterest income remained flat year-over-year at $192.6 million but decreased 10% from the previous quarter. Meanwhile, noninterest expenses increased slightly by 2% year-over-year to $261.2 million.

Each of Hilltop’s business segments contributed positively to the quarter’s results:

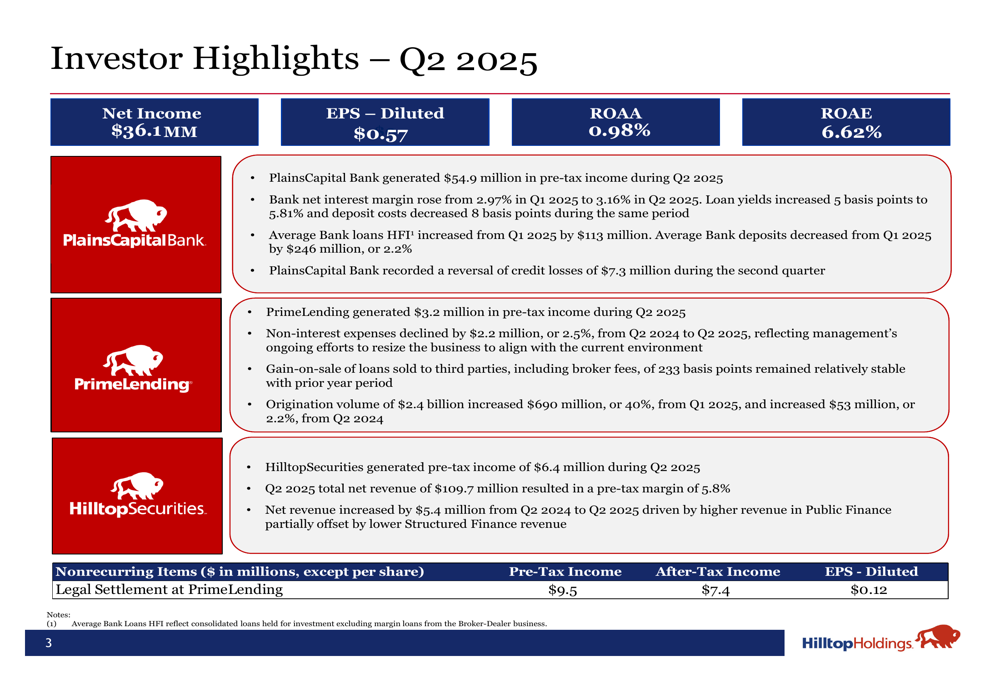

PlainsCapital Bank led the way with pre-tax income of $54.9 million, benefiting from net interest margin expansion from 2.97% to 3.16% and a $7.3 million reversal of credit losses. HilltopSecurities generated pre-tax income of $6.4 million with total net revenue of $109.7 million, while PrimeLending reported pre-tax income of $3.2 million despite challenging mortgage market conditions. Notably, PrimeLending’s results were boosted by a $9.5 million legal settlement.

Capital Management

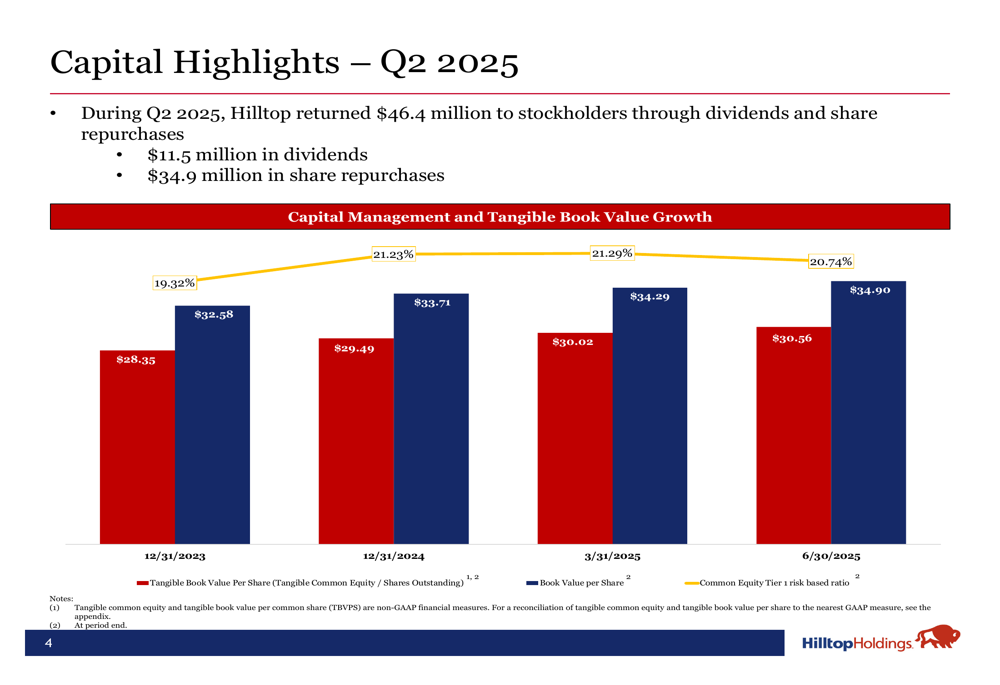

Hilltop Holdings maintained its commitment to shareholder returns during the quarter, distributing $46.4 million through dividends and share repurchases. This included $11.5 million in dividend payments and $34.9 million in share buybacks, demonstrating the company’s strong capital position and focus on delivering value to shareholders.

The following chart illustrates Hilltop’s consistent growth in tangible book value per share, which reached $30.56 as of June 30, 2025, representing a 20.74% increase:

This steady increase in tangible book value reflects the company’s effective capital management strategy and sustained profitability. The company has maintained dividend payments for 10 consecutive years, with a current dividend yield of 2.23% based on recent stock prices.

Credit Quality and Balance Sheet

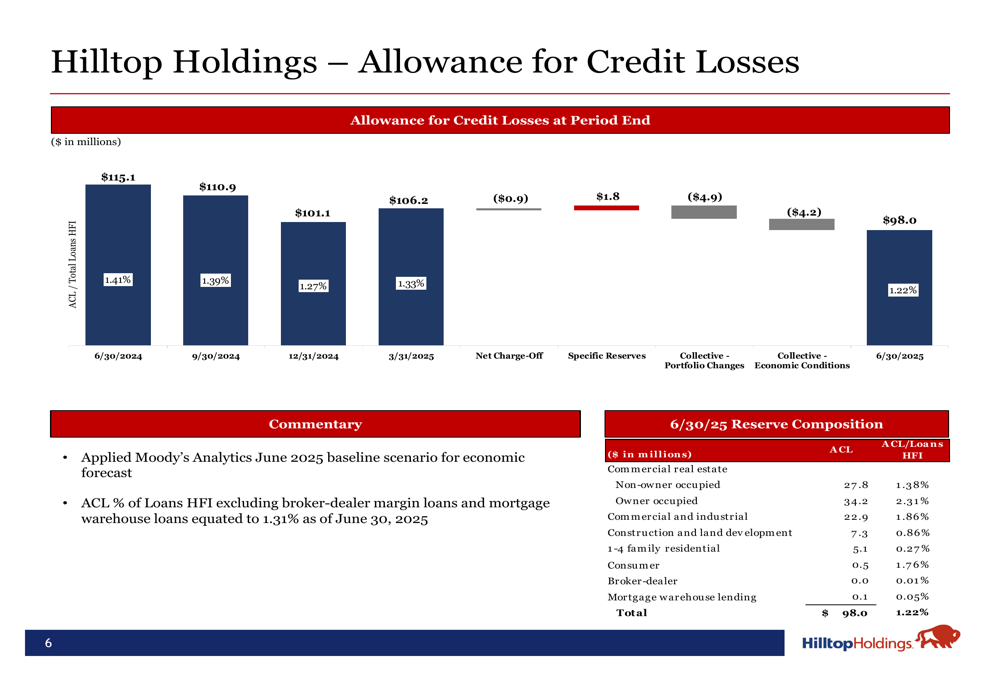

Hilltop Holdings continues to demonstrate strong credit quality, with its allowance for credit losses declining to 1.22% of total loans held for investment as of June 30, 2025, compared to 1.41% a year earlier. This reduction reflects the company’s improved credit outlook and effective risk management practices.

The following chart shows the trend in allowance for credit losses over the past year:

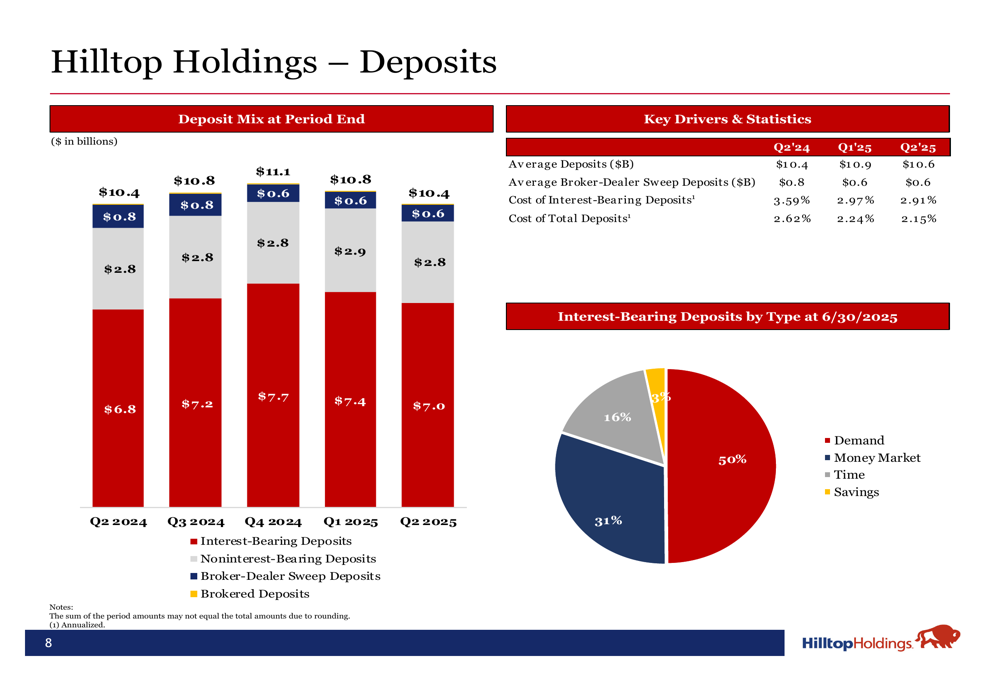

On the deposit front, Hilltop maintained a stable funding base with a well-diversified deposit mix. Interest-bearing deposits represented the largest component, with demand deposits accounting for 50% of the interest-bearing portfolio as of June 30, 2025.

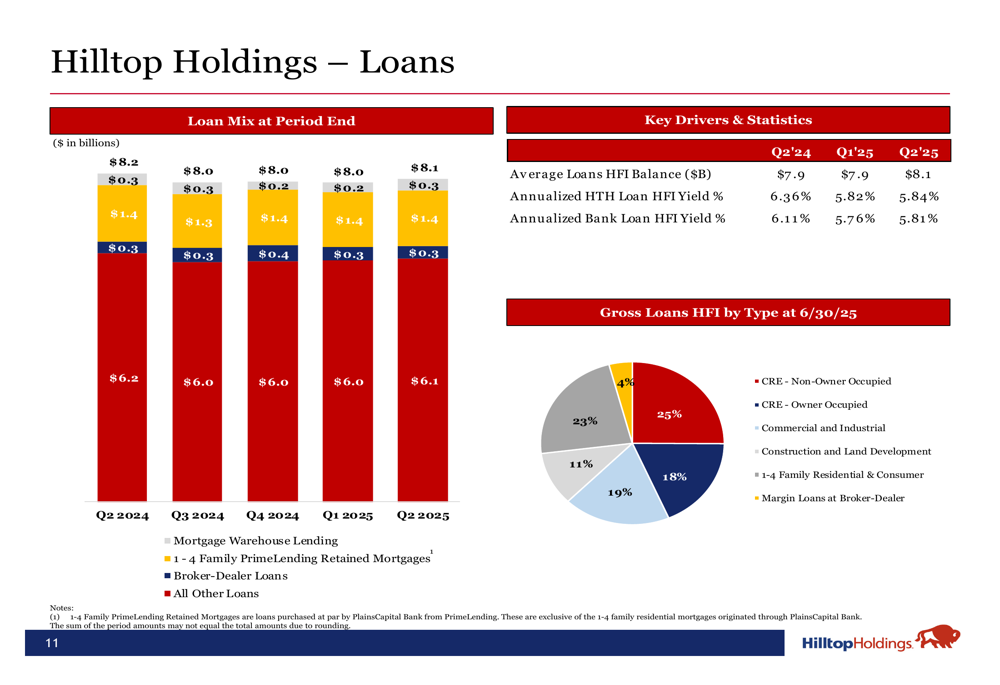

The loan portfolio remained well-diversified across various segments, including commercial real estate, commercial loans, and residential mortgages. Average loans held for investment increased by $113 million during the quarter, reflecting modest growth in line with the company’s strategic objectives.

Forward-Looking Statements

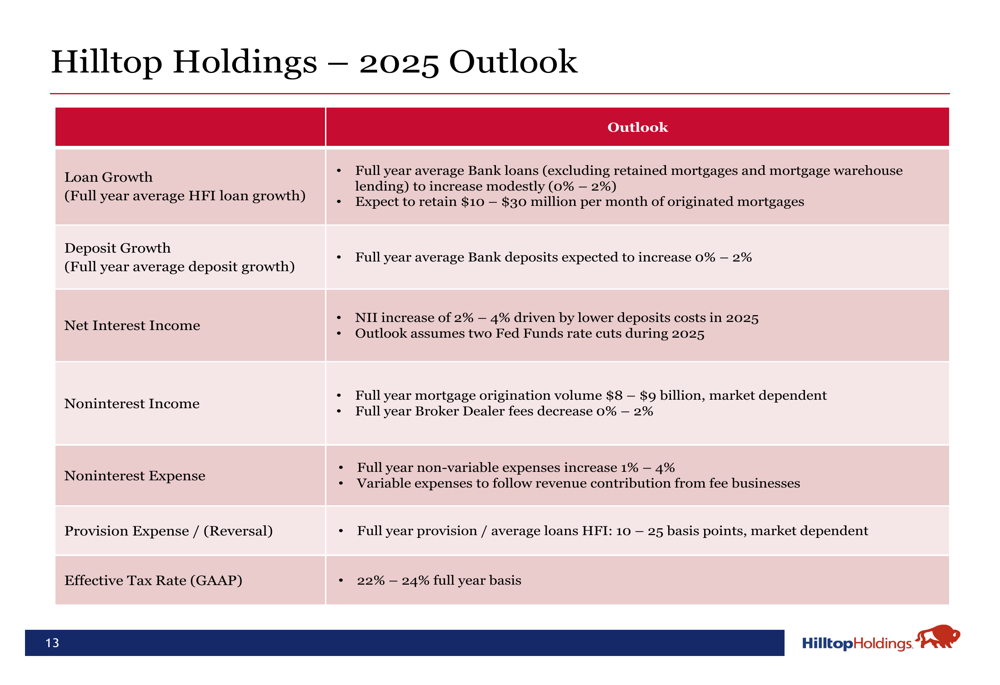

Looking ahead, Hilltop Holdings provided a cautiously optimistic outlook for the remainder of 2025, projecting modest growth across key business segments:

Management expects full-year average Bank loans (excluding retained mortgages and mortgage warehouse lending) to increase modestly by 0% to 2%, with a similar growth rate anticipated for average Bank deposits. Net interest income is projected to rise by 2% to 4%, primarily driven by lower deposit costs throughout 2025.

For the mortgage business, Hilltop forecasts full-year origination volume between $8 billion and $9 billion, with variable expenses expected to align with revenue contribution from fee businesses. The company also anticipates an effective tax rate of 22% to 24% for the full year.

These projections reflect management’s balanced approach to navigating the evolving interest rate environment, with expectations of two rate cuts in Q3 and Q4 of 2025 that could impact net interest income. Despite these potential headwinds, Hilltop’s diversified business model and strong capital position appear well-positioned to sustain profitability and continue delivering value to shareholders.

As the financial services landscape continues to evolve, Hilltop Holdings’ focus on maintaining strong capital levels, improving operational efficiency, and strategic risk management should help the company navigate market challenges while capitalizing on growth opportunities across its various business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.