ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Hoist Finance (STO:HOFI) presented its Q3 2025 results on October 24, 2025, revealing a mixed financial performance with declining profit before tax but improved return on equity. The company's stock declined 1.96% following the announcement, closing at SEK 97.05, as investors digested the results against a backdrop of the company's strategic shift toward Specialized Debt Restructurer (SDR) status.

The debt purchasing specialist, which operates across 14 European markets, reported progress on its strategic initiatives while maintaining strong capital and liquidity positions. With a market capitalization of $872 million and trading at a P/E ratio of 9.6x, Hoist Finance continues to focus on portfolio growth and geographical expansion.

Quarterly Performance Highlights

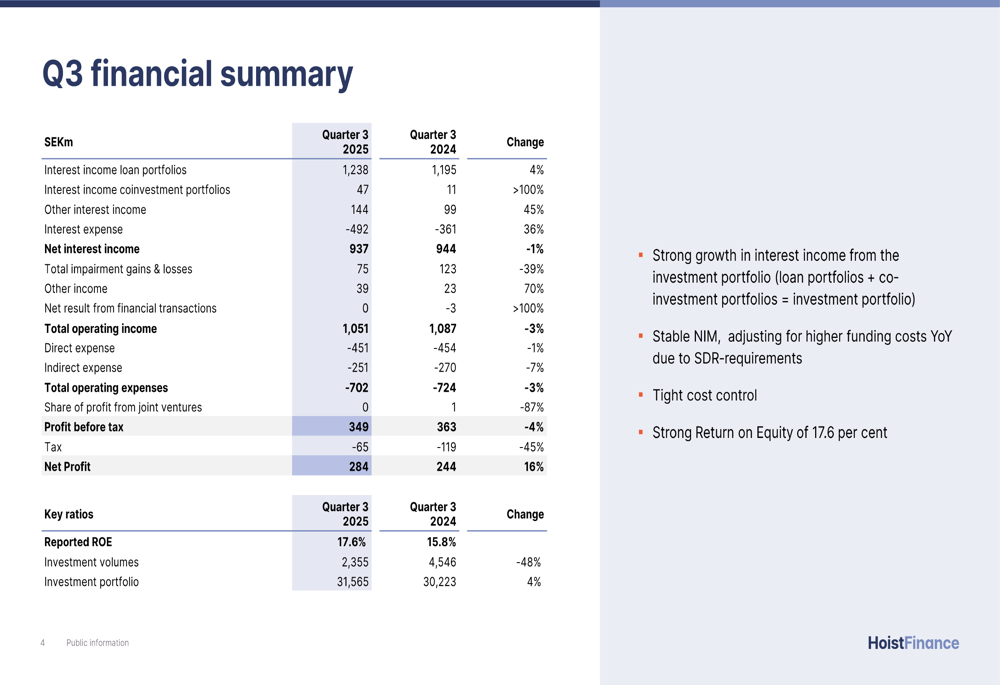

Hoist Finance reported profit before tax of SEK 349 million for Q3 2025, a 4% decrease compared to SEK 363 million in the same quarter last year. However, net profit increased by 16% to SEK 284 million, up from SEK 244 million in Q3 2024. The company achieved a return on equity of 17.6%, a significant improvement from 15.8% in the same period last year.

As shown in the following financial summary from the presentation:

Total operating income declined by 3% to SEK 1,051 million, compared to SEK 1,087 million in Q3 2024. The company attributed this performance to strong growth in interest income from the investment portfolio, stable net interest margin (NIM) when adjusting for higher funding costs, and tight cost control.

CEO Harry Vranjes emphasized the company's commitment to remaining banking regulated, stating, "We will stay banking regulated and can operate without the restrictions that we have been living under since 2019."

Investment Strategy and Portfolio Growth

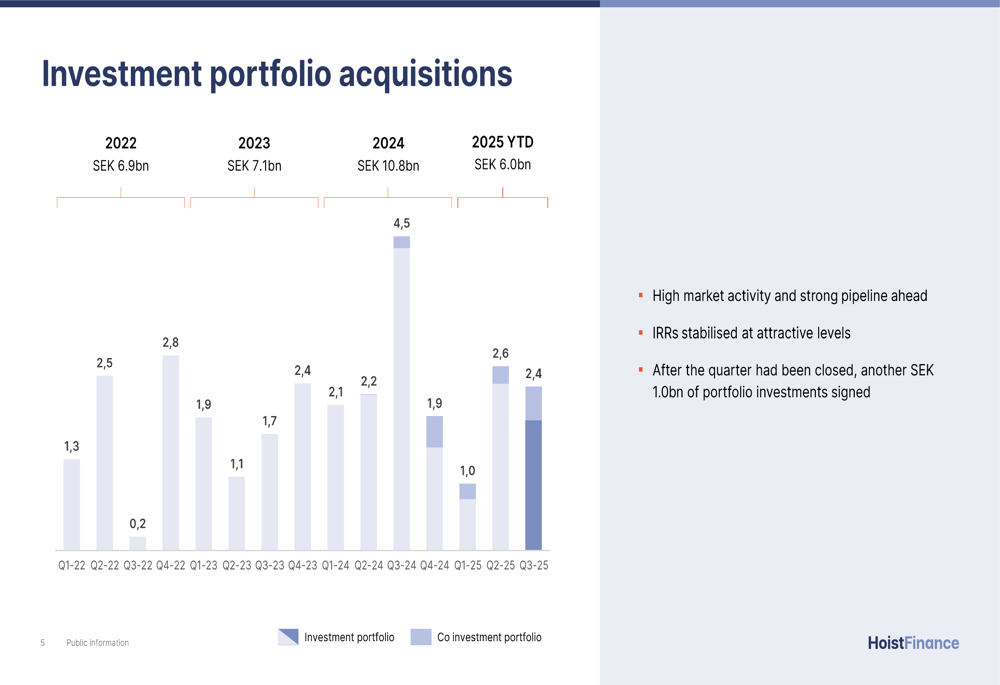

Hoist Finance's investment portfolio reached SEK 31.6 billion at the end of Q3 2025, representing a 4% increase compared to Q3 2024. The company invested SEK 2.4 billion in new portfolios during the quarter, though this represented a 48% decrease from the SEK 4.5 billion invested in Q3 2024. After the quarter closed, the company signed an additional SEK 1.0 billion in portfolio investments.

The presentation highlighted the company's investment acquisition trend over recent years:

A significant development during the quarter was Hoist Finance's expansion into Finland, strengthening its footprint in Northern Europe. The company now operates across 14 European markets, with a diverse geographic distribution of its investment portfolio.

The asset class mix has evolved significantly over the past three years, with secured assets increasing from 23% to 35% of the portfolio:

CFO Magnus Söderlund highlighted the company's disciplined approach to investments, saying, "We remain disciplined in everything we look at, and we are very careful with the return levels."

Capital Position and SDR Status Progress

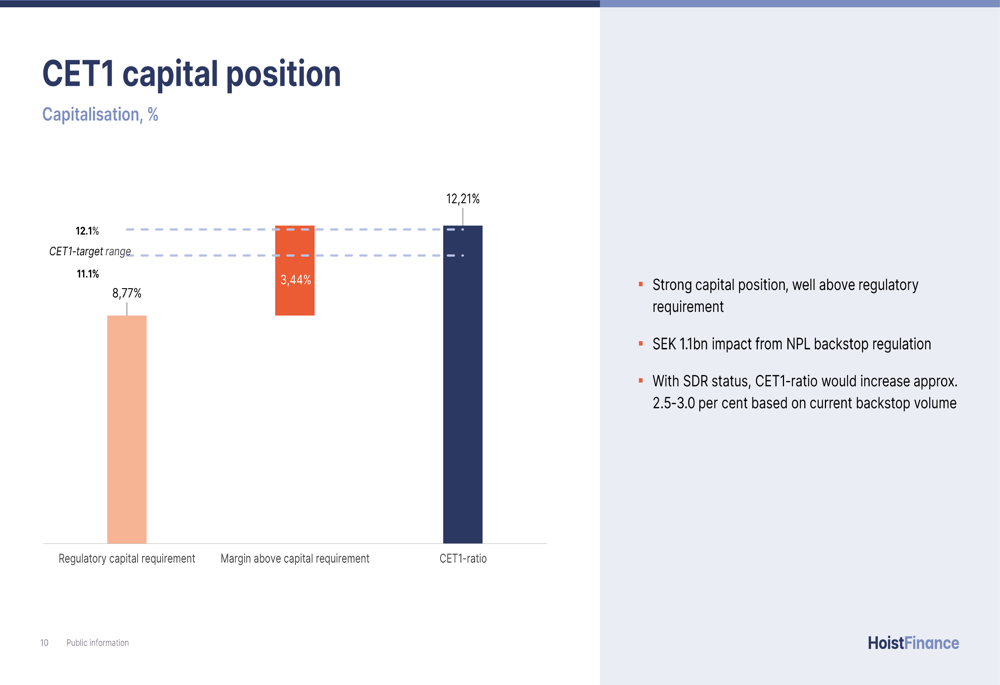

Hoist Finance maintained a strong capital position with a CET1 ratio of 12.21%, well above the regulatory requirement of 8.77%. The company's liquidity reserve stood at SEK 25 billion by the end of Q3, and its Net Stable Funding Ratio (NSFR) reached 142%, exceeding the 130% requirement for SDR status.

The capital position is illustrated in the following chart:

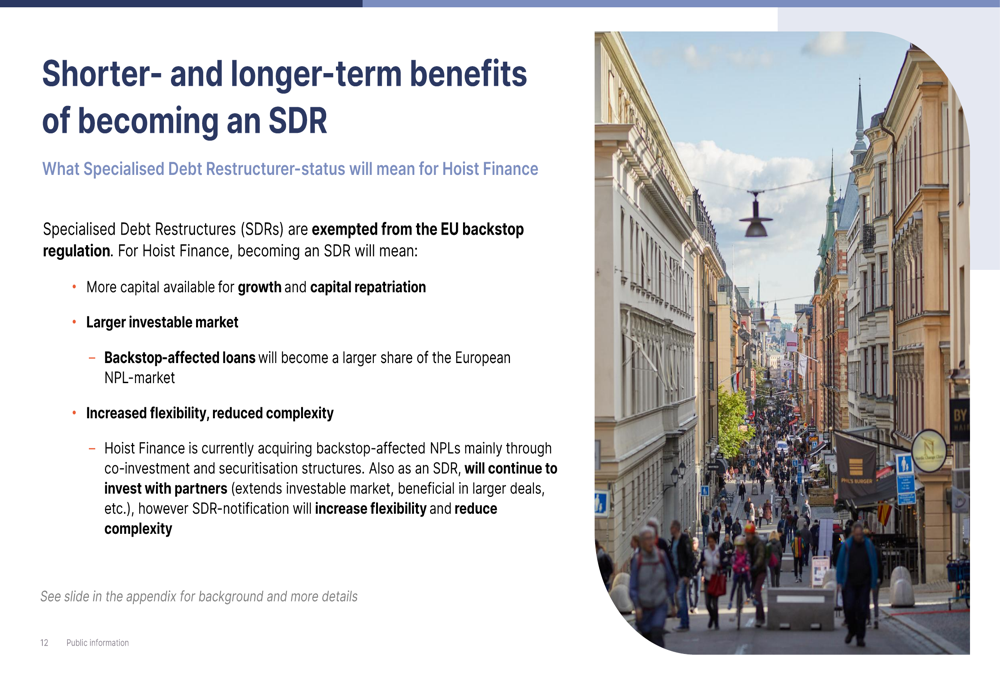

A key strategic focus for Hoist Finance is obtaining Specialized Debt Restructurer (SDR) status, which would exempt the company from EU backstop regulations. The company plans to notify its SDR status in connection with the upcoming Q4 report, which would increase its CET1 ratio by approximately 2.5-3%.

The benefits of achieving SDR status include more capital available for growth and capital repatriation, a larger investable market, and increased flexibility with reduced complexity:

During the quarter, Hoist Finance optimized its capital structure through the issuance of SEK 200 million AT1 capital with a coupon of STIBOR 3 months+500bps in August.

Forward-Looking Statements

Looking ahead, Hoist Finance aims to increase its portfolio size to SEK 36 billion by the end of 2026, according to the earnings call. The company anticipates a 25% increase in investment deployment after achieving SDR status.

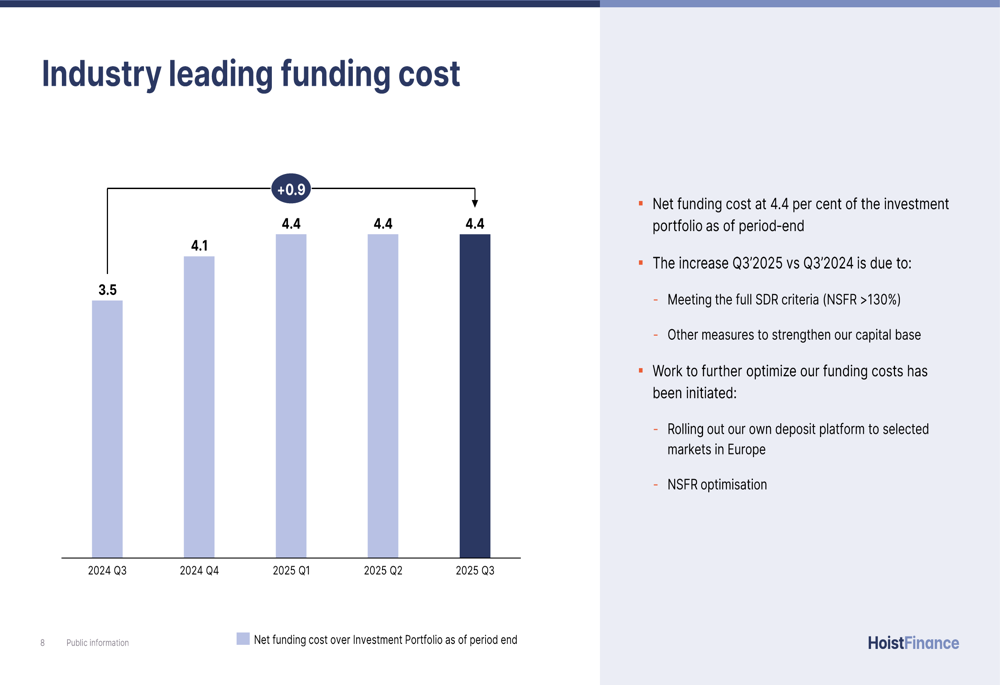

The company is working to optimize its funding costs, which have increased year-over-year:

Initiatives to reduce funding costs include rolling out its own deposit platform to selected markets in Europe and NSFR optimization. The company is also focused on maintaining tight cost control, with underlying direct and indirect costs remaining at stable levels despite inflationary pressures.

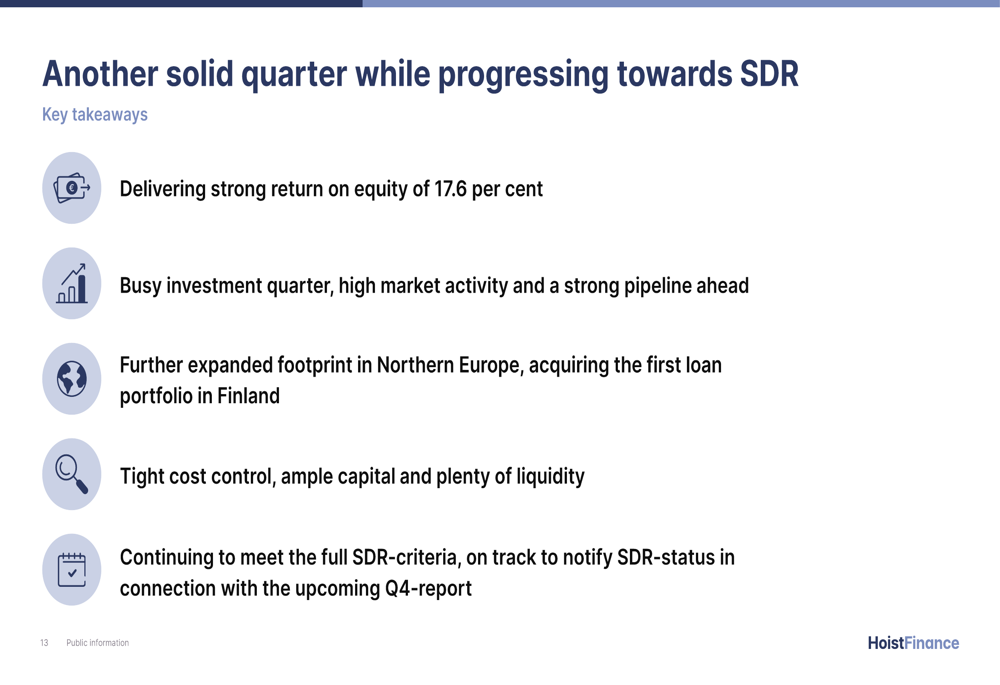

Hoist Finance concluded its presentation by highlighting another solid quarter while progressing toward SDR status:

With its strong capital and liquidity positions, geographic diversification, and strategic focus on achieving SDR status, Hoist Finance appears well-positioned to navigate market challenges while pursuing growth opportunities across its European markets. However, investors will be watching closely to see if the company can reverse the trend of declining profit before tax in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.