Sprouts Farmers Market closes $600 million revolving credit facility

Introduction & Market Context

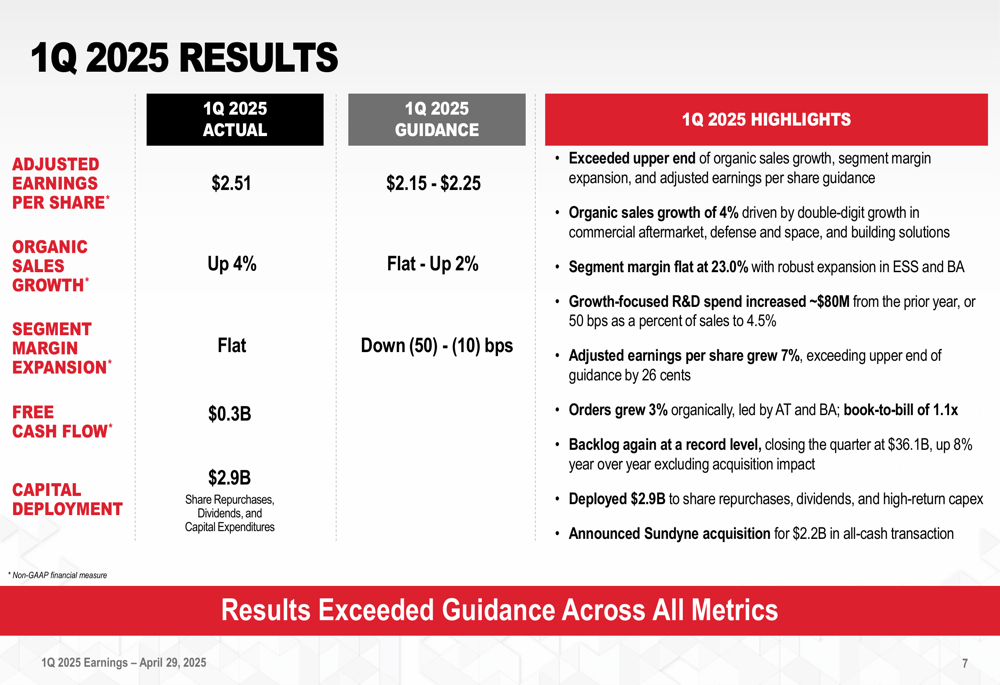

Honeywell International Inc (NASDAQ:HON) released its first quarter 2025 earnings presentation on April 29, showing strong performance across all guided metrics while advancing its strategic transformation plans. The industrial conglomerate reported adjusted earnings per share of $2.51, exceeding the upper end of its guidance range and driving shares up 5.14% in premarket trading to $210.97.

The company’s results come amid ongoing global trade uncertainties and follow its October 2024 announcement to separate into three independent public companies. Despite these challenges, Honeywell maintained its focus on strategic portfolio transformation while delivering solid financial results.

Quarterly Performance Highlights

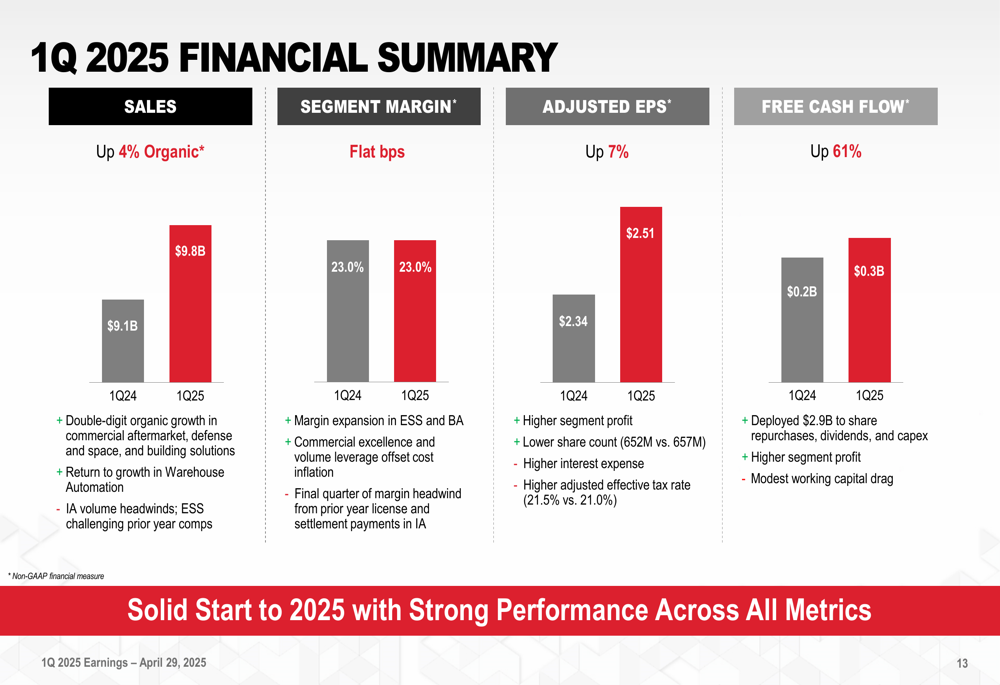

Honeywell reported organic sales growth of 4% in Q1 2025, significantly outperforming its guidance of flat to 2% growth. The company maintained segment margins at 23.0%, better than its guidance of a 10-50 basis point decline. Adjusted earnings per share grew 7% year-over-year, while free cash flow increased by 61%.

As shown in the following summary of Q1 2025 results versus guidance:

Orders grew 3% organically during the quarter, pushing backlog to record levels. The company deployed $2.9 billion to share repurchases, demonstrating confidence in its financial position and commitment to returning value to shareholders.

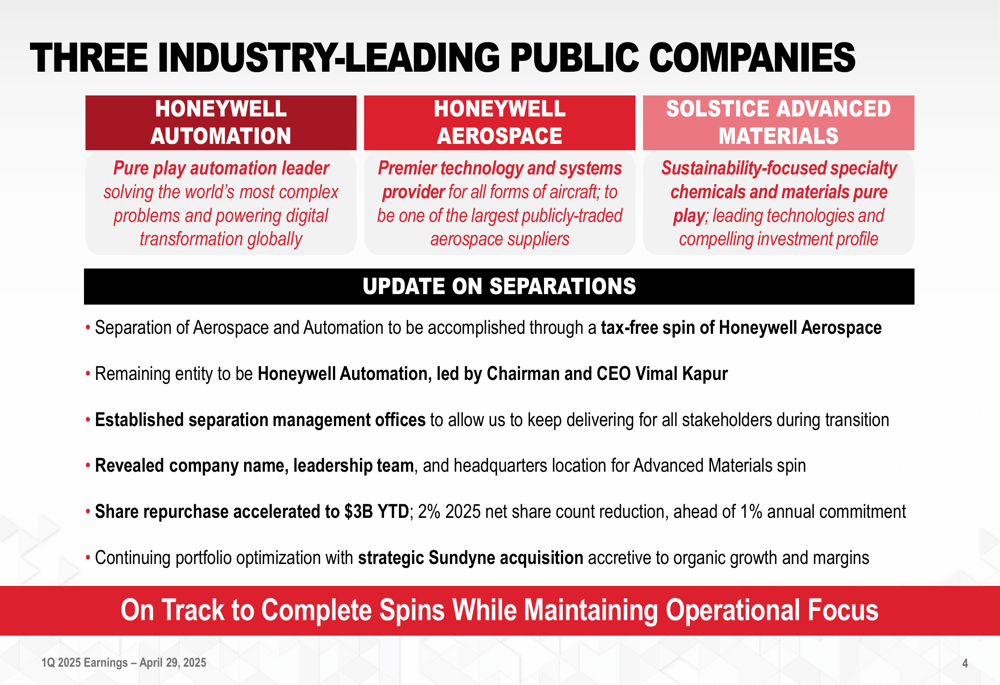

Strategic Initiatives

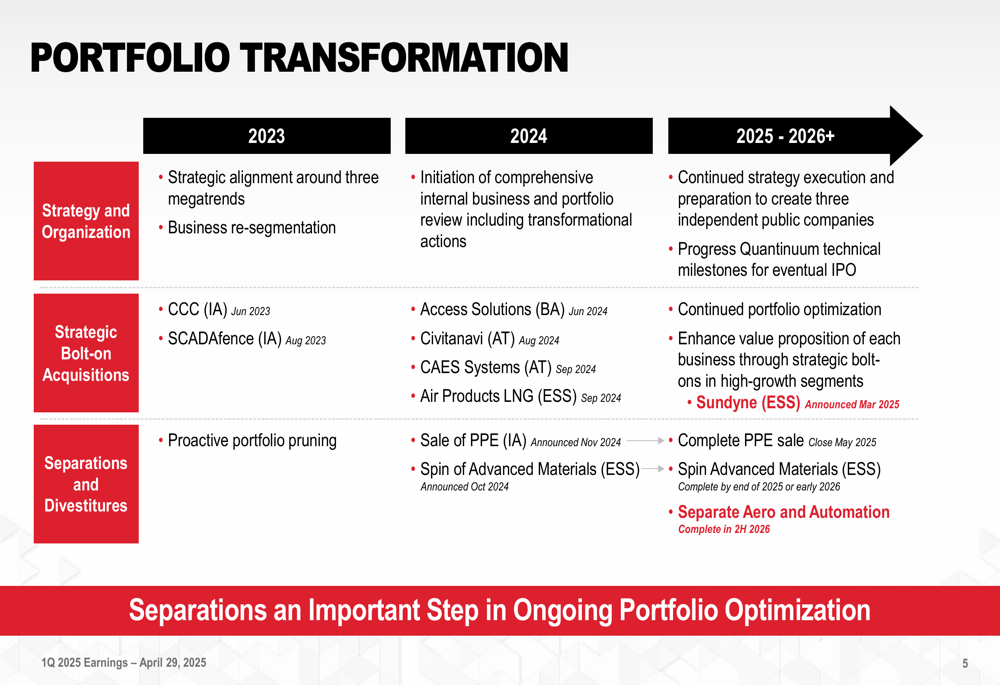

Honeywell continues to advance its planned separation into three independent public companies: Honeywell Automation, Honeywell Aerospace, and Solstice Advanced Materials. The separation of Aerospace and Automation will be structured as a tax-free spin-off of Honeywell Aerospace, with current Chairman and CEO Vimal Kapur leading Honeywell Automation.

The company’s transformation strategy is illustrated in this comprehensive timeline:

In March 2025, Honeywell announced the acquisition of Sundyne for $2.2 billion in an all-cash transaction, adding to its series of strategic acquisitions. The company also expects to complete the sale of its Personal Protective Equipment (PPE) business by May 2025, earlier than the previously planned June closure.

The following slide details the structure of the three planned companies:

Segment Analysis

Performance varied significantly across Honeywell’s business segments in Q1 2025. Aerospace Technologies led with 9% organic growth, while Building Automation delivered 8% organic growth. However, both Industrial Automation and Energy and Sustainability Solutions experienced 2% organic declines.

The detailed segment results reveal the mixed performance:

Aerospace Technologies maintained strong momentum despite a 190 basis point margin decline to 26.3%. Building Automation showed impressive margin expansion of 150 basis points to 26.0%. Industrial Automation faced challenges with margins declining 130 basis points to 17.8%, while Energy and Sustainability Solutions improved margins by 230 basis points to 22.2%.

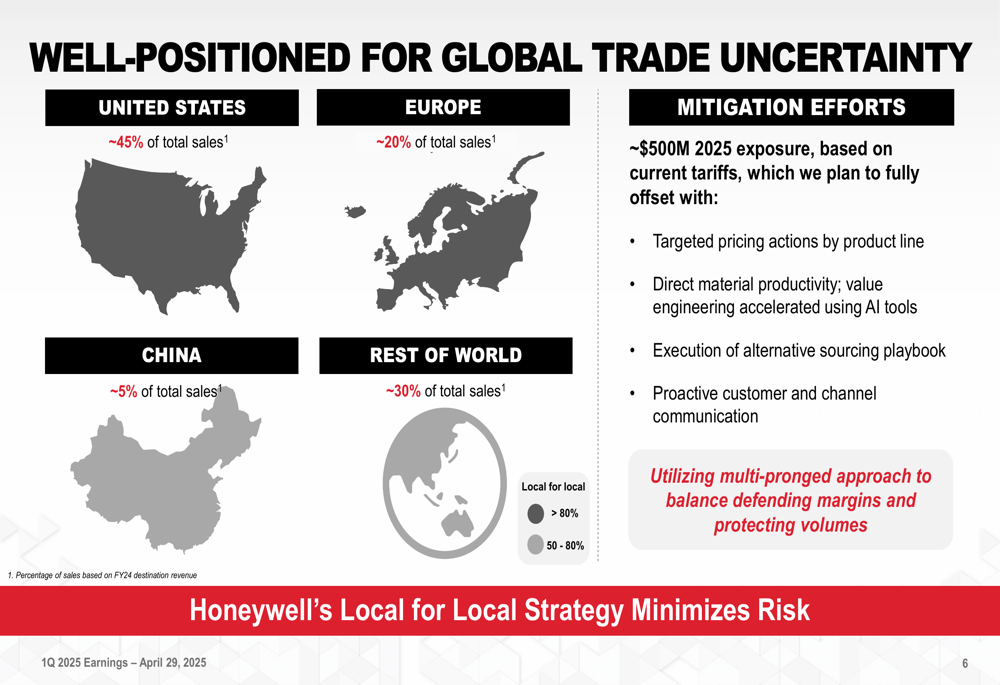

Global Positioning and Risk Management

Honeywell outlined its strategy to navigate global trade uncertainties, highlighting its geographical diversification and "Local for Local" approach to production. The company expects approximately $500 million in exposure from current tariffs in 2025 but plans to fully offset this through pricing actions, productivity improvements, alternative sourcing, and proactive customer communication.

The following geographical breakdown illustrates Honeywell’s global footprint:

With approximately 45% of sales in the United States, 20% in Europe, 5% in China, and 30% in the rest of the world, Honeywell’s diversified presence provides some insulation against regional economic fluctuations and trade tensions.

Forward-Looking Statements

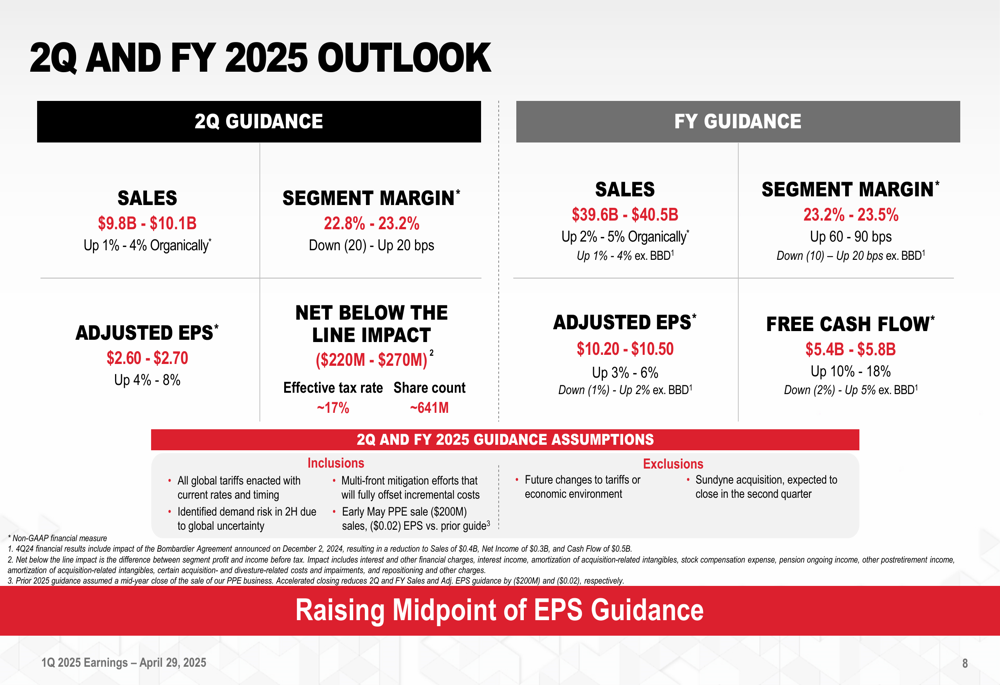

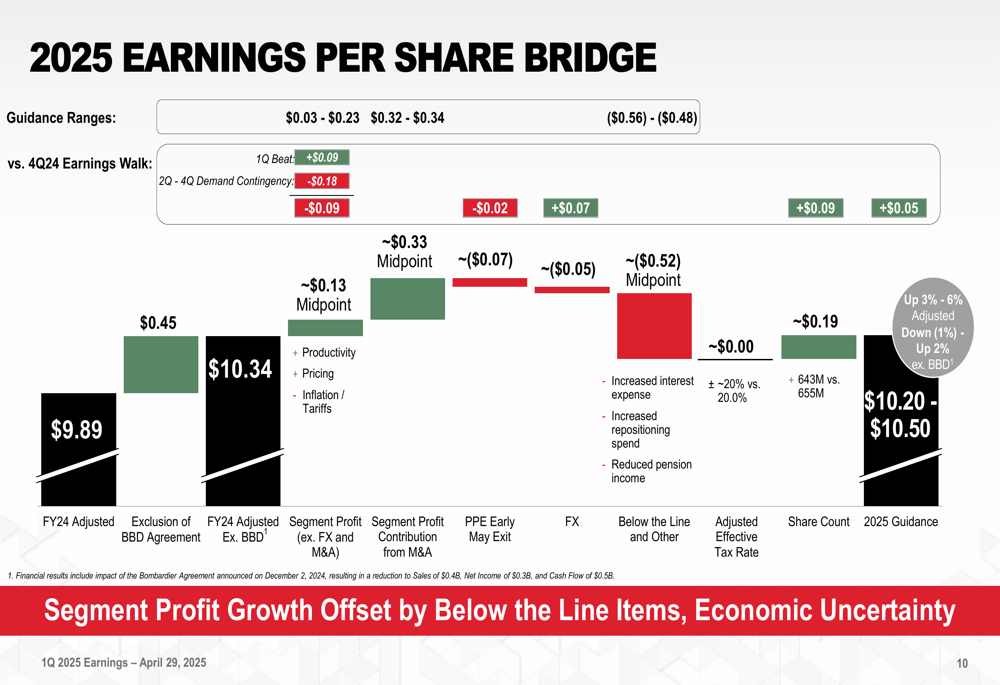

For Q2 2025, Honeywell expects sales of $9.8-$10.1 billion, representing 1-4% organic growth, with adjusted earnings per share of $2.60-$2.70, up 4-8% year-over-year. For the full year 2025, the company raised the midpoint of its EPS guidance, now projecting $10.20-$10.50 despite incorporating the impact of global tariffs and demand uncertainty.

The detailed outlook for Q2 and full-year 2025 is presented in the following guidance:

By segment, Honeywell expects high single-digit growth for Aerospace Technologies, mid-single-digit decline for Industrial Automation, mid-single-digit growth for Building Automation, and low single-digit growth for Energy and Sustainability Solutions for the full year 2025.

The company’s full-year guidance now accounts for an early May closure of the PPE business sale versus the previously expected June closure, which reduces 2025 sales by $200 million and adjusted EPS by $0.02 compared to the original guidance.

Executive Summary

Honeywell’s management emphasized the company’s ability to navigate an uncertain environment from a position of strength. The strong start to 2025 across all guided metrics provides momentum as the company progresses with its separation plans and portfolio transformation.

The following summary highlights Honeywell’s key messages:

"We’re laser-focused on delivering our commitments to all stakeholders," stated the company in its presentation, highlighting the progress of separation activities and continued disciplined capital deployment through the Sundyne acquisition and active share repurchases.

Honeywell’s first quarter performance demonstrates the company’s resilience and strategic focus as it works toward creating three industry-leading public companies while delivering strong financial results in a challenging global environment. With raised guidance and strategic initiatives progressing as planned, Honeywell appears well-positioned for the remainder of 2025 despite ongoing economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.