ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Horizon Technology Finance Corporation (NASDAQ:HRZN) unveiled details of its strategic merger with Monroe Capital Corporation (NASDAQ:MRCC) during its Q2 2025 earnings presentation on August 7. The announcement comes as Horizon reported quarterly earnings that met EPS expectations at $0.28 while exceeding revenue forecasts with $24.52 million against an expected $22.27 million.

Despite the revenue beat, HRZN shares fell 4.26% in post-market trading to $7.29, with premarket trading on August 8 showing a further decline of 4.59% to $7.07. The stock is currently trading near its 52-week low of $7.09, significantly below its 52-week high of $11.47, suggesting investor caution regarding the merger.

Executive Summary

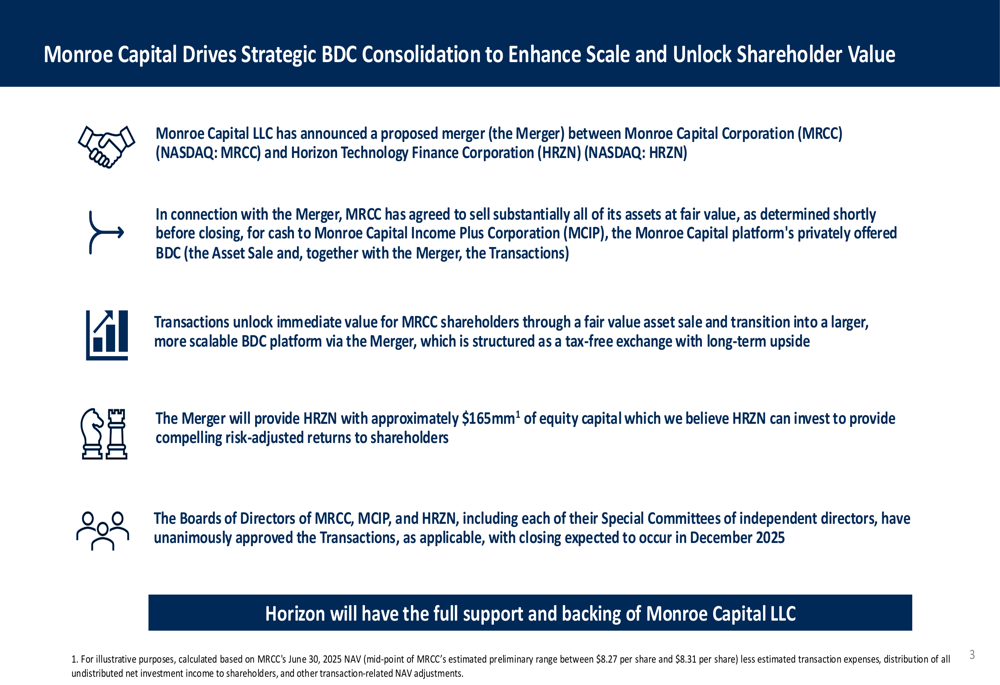

The proposed merger represents a significant strategic move for both business development companies (BDCs). According to the presentation, the transaction will add approximately $165 million in equity capital to Horizon, creating a combined entity with a pro forma net asset value (NAV) of approximately $446 million. The merger is structured as a two-step transaction, with MRCC first selling its assets at fair value to MCIP, followed by MRCC merging into HRZN through a NAV-for-NAV share exchange.

As shown in the following strategic overview slide, the transaction has received unanimous approval from the boards of directors of all involved entities and is expected to close in December 2025:

Ted Koenig, Chairman and CEO, stated during the earnings call, "We believe this transaction takes the best attributes of both MRCC and Horizon and creates a better business development company." Meanwhile, Mike Balkin, CEO, emphasized that "This is not just going to be a larger portfolio, it's going to be a more sophisticated and diversified portfolio."

Strategic Initiatives

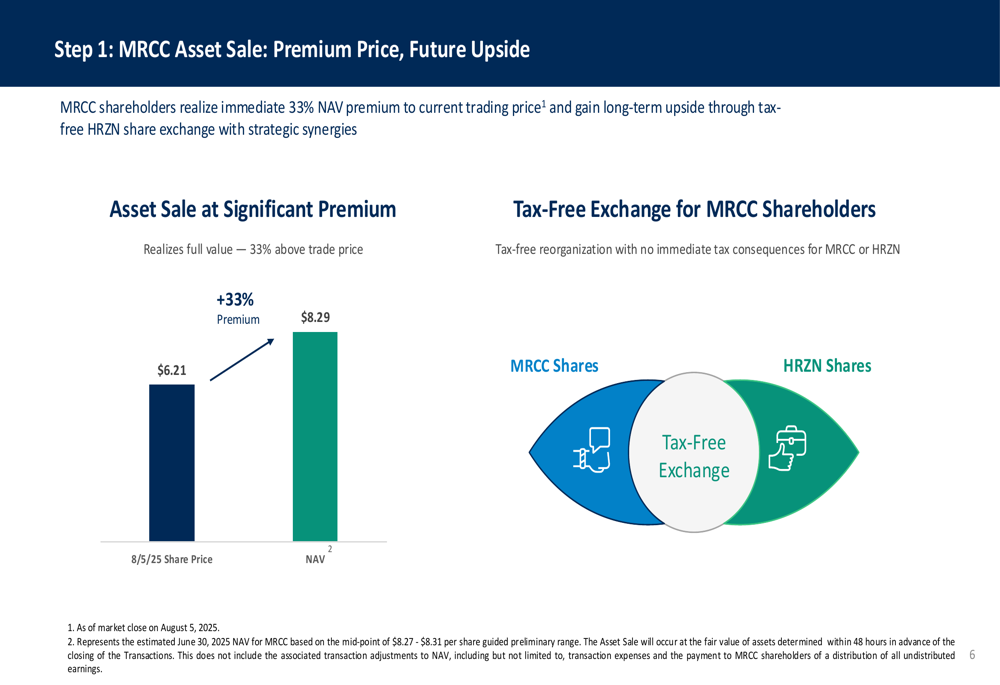

The merger is designed to deliver benefits to shareholders of both companies. For MRCC shareholders, the transaction offers an immediate 33% NAV premium to the current trading price, along with long-term upside through a tax-free HRZN share exchange. This premium is illustrated in the following slide:

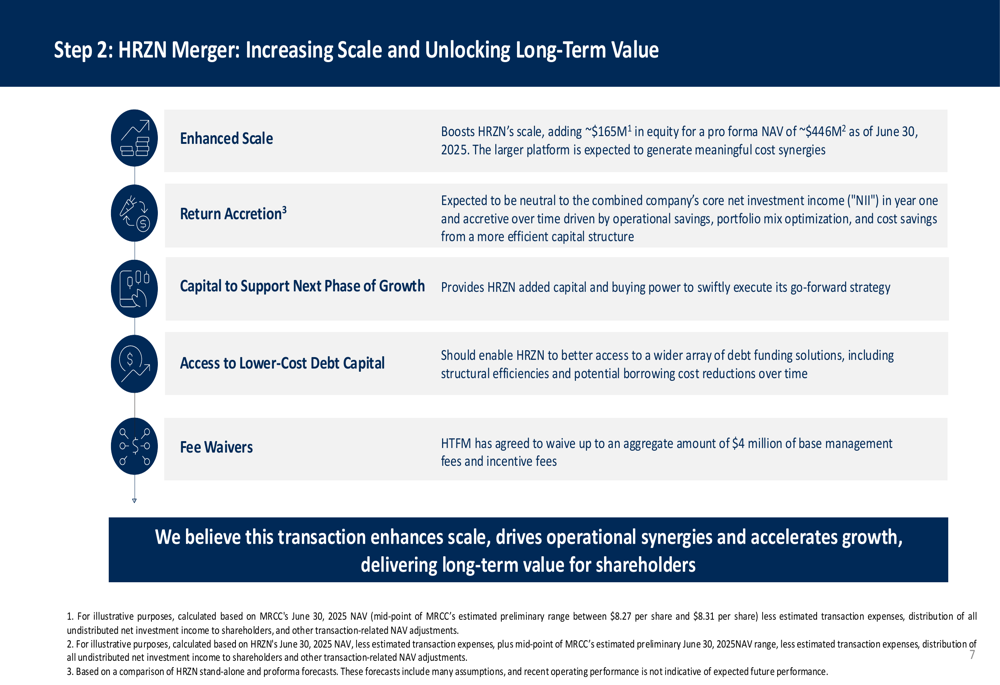

For HRZN, the merger is expected to enhance scale, provide capital for growth, enable access to lower-cost debt capital, and include fee waivers from Horizon Technology Finance Management (HTFM) of up to $4 million in base management fees. These benefits are detailed in the following slide:

The transaction structure involves a concurrent two-step process that aims to maximize value for shareholders of both entities. MRCC shareholders are expected to own approximately 37% of the combined company immediately following closing, based on an exchange ratio calculated from the respective NAVs of both companies.

Detailed Financial Analysis

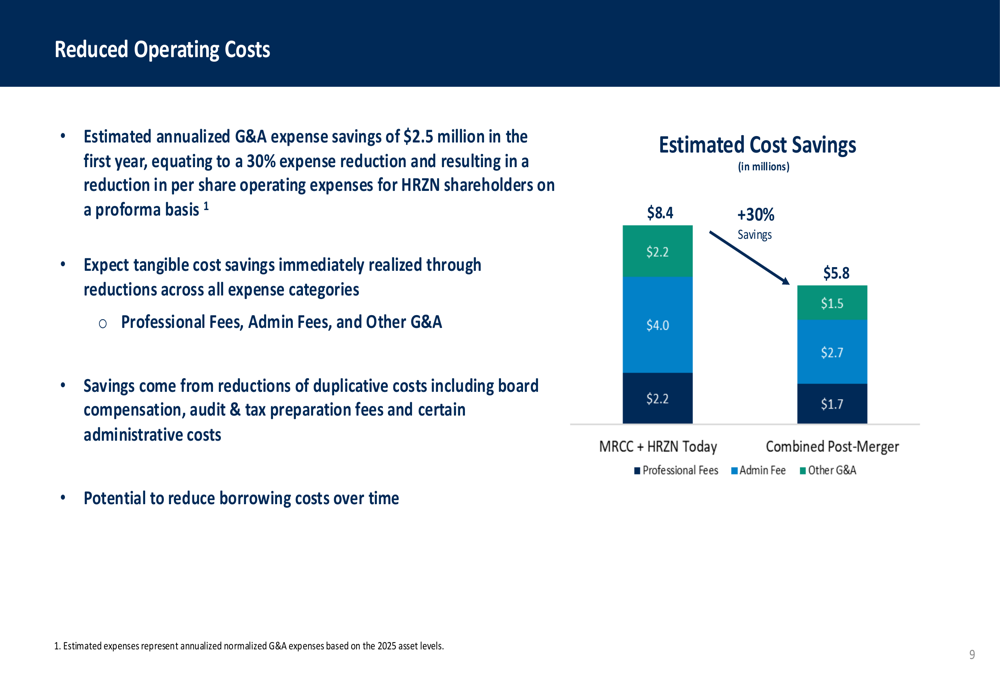

A key financial benefit highlighted in the presentation is the significant reduction in operating costs expected from the merger. The combined entity anticipates annualized G&A expense savings of $2.5 million, representing a 30% reduction in expenses. These savings are expected to come from reductions in professional fees, administrative fees, and other general and administrative expenses, as illustrated in this slide:

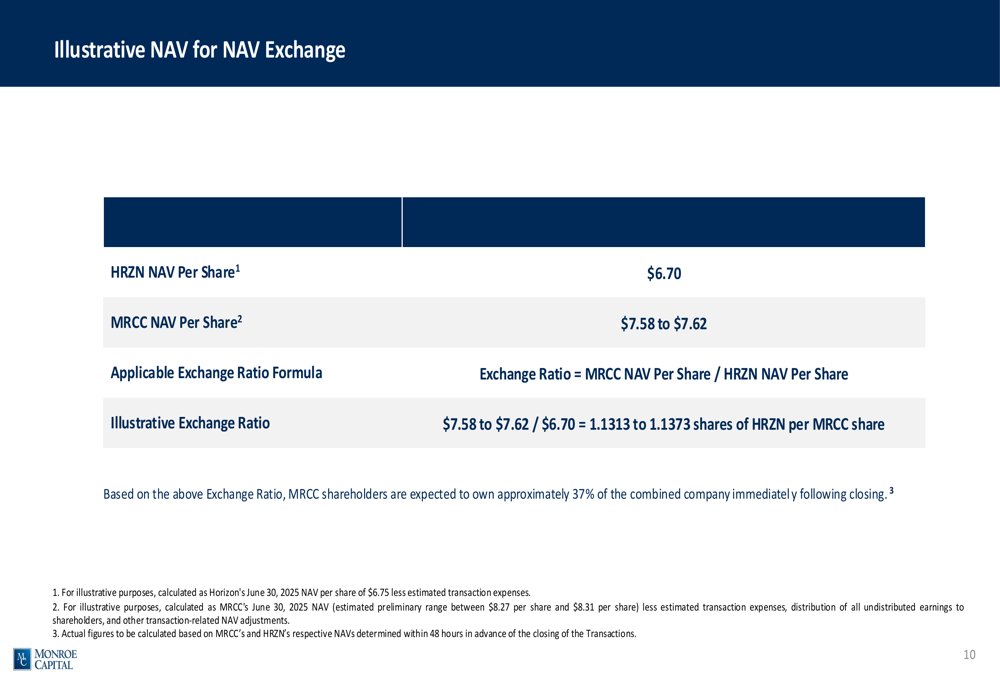

The presentation also provided details on the NAV-for-NAV exchange ratio. With HRZN's NAV per share at $6.70 and MRCC's NAV per share between $7.58 and $7.62, the illustrative exchange ratio is calculated at 1.1313 to 1.1373 shares of HRZN per MRCC share:

From a performance perspective, Horizon's Q2 2025 results showed stability in earnings while exceeding revenue expectations. The company reported EPS of $0.28, meeting analyst forecasts, while revenue of $24.52 million surpassed expectations by 10.1%. This revenue beat contrasts with previous quarters where the company often met or slightly missed forecasts, indicating an improvement in its revenue-generating capabilities.

Forward-Looking Statements

The combined company is positioning itself for long-term growth through several strategic initiatives. These include strengthened leadership with the appointments of Michael Balkin as CEO and Paul Seitz as CIO, broadening the investment mandate to include public small cap growth companies, ramping up deployment plans with new origination hires, and aligning with shareholders through management and incentive fee waivers.

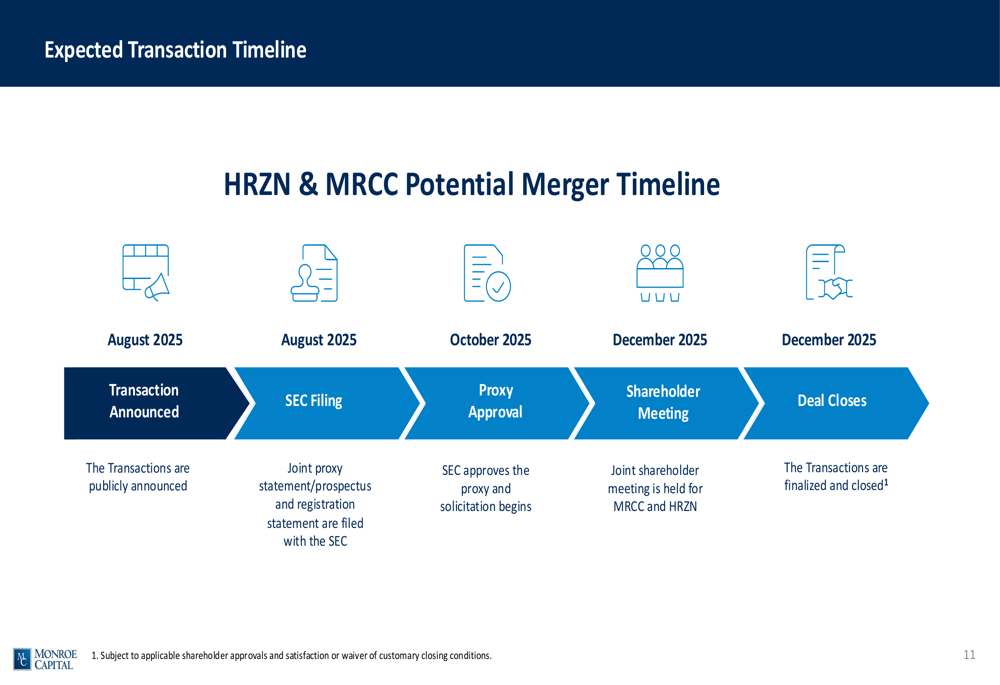

The expected timeline for the transaction shows a relatively quick process, with shareholder meetings and deal closing anticipated in December 2025:

Management expects the merger to be EPS-neutral in the first year post-merger and accretive over time. However, the market reaction suggests some investor skepticism about the execution risks and potential integration challenges. Key risks identified include integration complexities, market volatility affecting stock performance, execution of the rapid capital deployment strategy, potential regulatory hurdles, and competitive pressures in the venture debt market.

The backing of Monroe Capital, a $21.6 billion diversified private credit solutions provider founded in 2004, is expected to provide additional resources and capabilities to the combined entity. With the merger, Horizon aims to leverage Monroe's platform to enhance its competitive position in the venture debt market while broadening its investment mandate to include loans to public small-cap companies.

As the companies move toward the anticipated December 2025 closing date, investors will be watching closely for signs of successful integration planning and early indications of whether the promised synergies and growth opportunities will materialize.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.